Anatomy of a Home Appraisal Report: What Do the Different Sections Mean for Sellers?

- Published on

- 2-4 min read

-

Valerie Kalfrin Contributing AuthorClose

Valerie Kalfrin Contributing AuthorClose Valerie Kalfrin Contributing Author

Valerie Kalfrin Contributing AuthorValerie Kalfrin is a multiple award-winning journalist, film and fiction fan, and creative storyteller with a knack for detailed, engaging stories.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.

The hundreds of checkboxes and data fields that make up a home appraisal report are enough to make anyone’s eyes glaze over. But together all the inputs determine the fate of your home sale so get ready to put on your study cap and readers.

“When I go on a listing appointment, if people seem like they’re being unrealistic about the list price, I bring up the appraisal,” said Al Urban, a top-selling agent in Kansas City, MO. “The appraisal has to come in at least at the sale price.”

The report, which will contain the appraiser’s opinion of value and the factors they used to come up with that number, could hold the keys to why your home didn’t appraise or reveal opportunities to add value to the house. Let’s review each section of the report and its applications so you can approach it with the literacy of an informed homeowner, if not an amateur appraiser.

What happens leading up to the appraisal report delivery?

The home appraisal is a big step on the road to closing after you accept an offer from a buyer. Before the buyer’s financing can go through, the mortgage lender hires the appraiser to protect their investment and confirm that the buyer is getting a fair price.

During this part of the home sale process, a home appraiser will research the basic data points around your house such as square footage, number of beds and baths, lot size, etc. using resources like the multiple listing service to pull those numbers. They’ll compare your home’s size and features against others on the block based on recent sales of comparable properties.

Next the appraiser will come out to your house for an on-site visit. They’ll walk through the property and take measurements, snap photos, and review your home’s condition as part of their visual assessment.

The appraisal report containing your home’s appraised value and all the appraiser’s notes should come back within a week. As the seller, you won’t automatically get a copy of the report, but you can request one and the lender will have to provide it to you in 30 days time.

A home appraiser compiles the appraisal report, which determines the true, unbiased value of your home and property. The appraisal (including the report results) normally costs from $400 to $600, and the buyer is responsible for paying for this assessment.

In some cases a seller may opt to get a pre-listing home appraisal, which can be helpful in the event that you have to price a unique property or hope to speed up the closing process with an accurate pricing strategy from the start. However, most sellers just use the comparative market analysis put together by their real estate agent.

It’s common for sellers to leave some negotiating room by asking for slightly more than they expect, but this is typically 5% to 10% above the value determined by looking at comparable properties. An appraisal stops sellers from being “unrealistic” with an astronomical asking price, Urban said. “You would need to either adjust the sale price to the appraisal, or let that deal go.”

So what will you find on the appraisal report? Let’s dive in for details

Appraisers use the Uniform Residential Appraisal Report, which has specific sections to support the appraiser’s opinion of the property’s market value. The sections cover dozens of internal and external factors that contribute to the property’s value. These include:

Subject: the basics about your property

This opening part of the report has all the basics about your property in public records: its address, census tract, legal description, and assessor’s parcel number. It also includes any special assessments such as HOA (homeowners’ association) fees, and provides space for the appraiser to note the lender, the borrower, and “assignment type,” or type of transaction: a property purchase or refinance.

Contract: the key players in this transaction

Here, the appraiser notes whether the property seller is the owner of public record. The form also lists the contract price, the date of the contract, and whether any financial assistance (such as loan charges) are to be paid by any party on behalf of the borrower.

Neighborhood: how your area looks in the market

Your neighborhood may feel cozy, but that’s not a consideration in this section of the appraisal report, which also doesn’t use demographics. Rather, it notes the neighborhood’s:

- Legal boundaries

- Price range

- Designation as urban, suburban, or rural

- Degree of development, defined by Fannie Mae as “the percentage of available land in the neighborhood that has been improved” (it will note over 75%, less than 25%, or between 25% and 75%)

- Price trends (increasing, stable, or declining)

Site: your property’s size and utility supply

If you’ve ever wondered about your property’s dimensions, area, shape, view, zoning description or zoning classification, you’ll find that here. This part of the appraisal report also notes:

- whether the property has public or private utilities (electricity, gas, water, sanitary sewer)

- any off-site improvements to a public or private street or alley

- whether the property is located within a FEMA Flood Hazard Area or FEMA Flood Zone

- any “adverse site conditions,” such as encroachments, easements, or particular environmental conditions.

Improvements: your home’s condition and features

This is probably the most sobering section of the appraisal report. Here, your property truly is reduced to square feet of living area above grade—nothing removable in the décor, like ceiling fans. You’ll see:

- the year built

- the design style

- the type of foundation (crawl space, concrete slab, partial or full basement)

- a description of the materials and condition of the exterior walls, foundation walls, roof surface, window type, gutters and downspouts, and screens

- a description of the materials and condition of the interior walls, floors, trim/finish, bath floor, and bath wainscot

- the type of car storage (none, driveway, how many cars fit in the garage)

- the type of driveway surface

- the type of attic (drop stair, heated, finished)

- the type of heating and cooling

- amenities such as a pool, patio or deck, fireplace, fence, porch, or wood stove

- appliances such as a refrigerator, oven, dishwasher, washer/dryer, or disposal

- any “physical deficiencies or adverse conditions” that affect structural integrity, soundness, or livability.

If your property has features such as energy-efficient appliances, that may be noted here if it adds value, Urban said.

Sales comparison approach: How does your home stack up to others in the area?

Once the appraiser has all the above information, it’s time to calculate your home’s worth. The Sales comparison approach, or “market data approach,” is what appraisers use most often.

Although you’ll find lots of details for the appraiser’s methodology, this section boils down to analyzing three or four comparable properties that have sold recently. You’ll see how the report compares homes based on square footage, location, property condition, number of bathrooms and bedrooms, and amenities (garage, swimming pool, etc.)

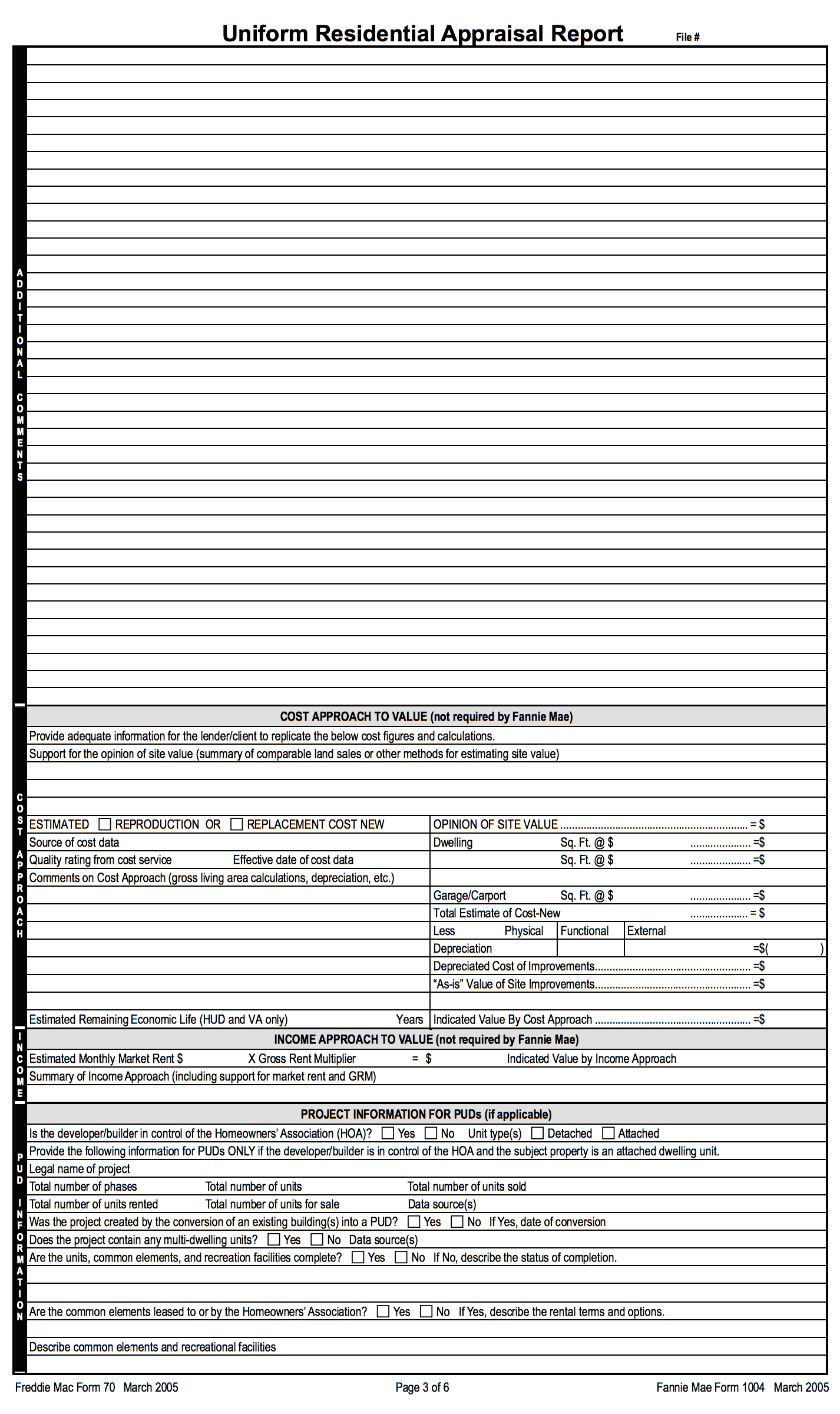

Cost approach to value: rebuilding from the bottom up

Here, an appraiser assesses your home’s worth based on whether it would cost more or less to build a new home with the same features from scratch. (You’ll often find this used in commercial appraisals or appraisals of newly constructed property.)

To do the math of the cost approach, this section includes the cost of land, the cost of building on top of that land, and depreciation. Add the cost of land and cost of building, subtract the depreciation, and you get your home’s value.

Income approach to value: Does your property make money?

If your property is primarily a rental or other form of income, such as an Airbnb or investment property, the appraiser will use this section to calculate the worth. The income approach considers the annual rental income your property generates, minus your expenses, and also calculates your “capitalization rate,” or Net Operating Income (NOI) to property asset value.

The capitalization rate, or cap rate, represents the percentage return an investor would receive on an all-cash purchase. To calculate this accurately, an appraiser again would look at recent sales of similar types of buildings in the same market.

PUD information: community maintenance fees and land ownership

Lastly, an appraisal form includes a section for information about PUD, or Planned Unit Development. According to financing provider Fannie Mae, PUD is a project or subdivision that has common property and improvements that an HOA owns and maintains for each unit in exchange for mandatory assessments (fees).

Appraisal report extras

In addition to the above sections, the appraisal report also might include additional notes pertinent to the buyer’s financing. First-time homebuyers often have FHA financing, which requires not only an appraisal but a property inspection to ensure that the home meets the Department of Housing and Urban Development’s minimum standards for health and safety.

These include:

- sufficient heating

- whether the property’s lot is graded to prevent moisture from entering the foundation or basement

- whether all bedrooms have egress to the exterior, such as a window, for fire safety

- whether a home has lead-based paint, and whether any paint is peeling or chipped

- whether steps and stairways have handrails

“If it’s a conventional loan, then it’s more or less purely value,” Urban said.

And where can sellers find that crucial number, the bottom line on what an appraiser says their home is worth?

Where to find the opinion of value on a home appraisal report

In the section labeled “Reconciliation,” on the appraisal report, look for the bolded text that reads:

“Based on a complete visual inspection of the interior and exterior areas of the subject property, defined scope of the work, statement of assumptions and limiting conditions, and appraiser’s certification, my (our) opinion of the market value, as defined, of the real property that is the subject of this report is $_______, as of ________. “

It’s there (circled in red below) that you’ll find what the appraiser believes your home to be worth.

An FHA appraisal will require that any health or safety issues be addressed before approval. Urban said that if a home appraises at least at sale price, and the lender’s conditions are reasonable, then generally, sellers are OK with doing such repairs.

If your appraisal comes in lower than you’d hoped, look into minor fixes that show your home in a better light. Review your options for negotiating with the buyer or if you think the appraiser did your house an injustice, talk to your real estate agent about the possibility of ordering a second opinion.

Article Image Source: (Sarah Pflug/ Burst)