Process of Selling a House for Cash in 9 Steps

- Published on

- 12 min read

-

Richard Haddad Managing EditorClose

Richard Haddad Managing Editor

Richard Haddad Managing EditorClose

Richard Haddad Managing EditorRichard Haddad is the managing editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.

If you need to sell your home quickly, finding a cash buyer for your house may be the solution you’re looking for. In this post, we’ll show you the process of selling a house for cash.

In former days, the decision to sell your house for cash was primarily associated with a neglected or distressed property whose value had fallen, leaving homeowners with few options.

While a cash offer can still benefit a seller who can’t afford repairs or is facing challenging property issues, cash sales have expanded beyond the distressed homes market, as sellers discover the ease and benefits of new technologies and instant sale online platforms. But for many sellers, the process of selling a house for cash is unclear.

“A lot of sellers think selling a house ‘for cash’ means the buyer is going to show up with a briefcase full of money for them, but that’s not the case,” says Lucas Machado, a real estate investor and owner of House Heroes, LLC.

Step one to selling a house for cash

Tell us about your home and speak to a home consultant. We use your local neighborhood data and our extensive investor network to find the best offer for your home.

A “cash offer” simply means the buyer has cash readily available to pay for the home, and the offer is not dependent on being able to secure a mortgage. But that doesn’t make the process of selling your house for cash any less mysterious if you’ve never done it.

How long does it take to sell a house?

Transaction speed is typically the primary sought-after benefit of finding a cash buyer for a house. How long it takes to sell a house depends on a number of factors, including the type of home you’re selling, its size and age, property conditions, location, and current market conditions.

According to recent Federal Reserve economic data, homes can spend a median of 61 days on the market (DOM) — meaning the time between when a house is listed and when it goes under contract with a buyer. For home sellers working with a financed buyer, you’ll need to factor in an additional 45 days on average to close a purchase loan, according to data from Ice Mortgage Technology.

This means from list to close, you might need to plan for more than three months to complete your home sale transaction. And the 106-day average estimate does not account for your time spent preparing the property to be placed on the market.

Selling a home for cash can be a much faster process; allowing you to close a sale in as little as 8 to 16 days. Depending on your situation and selling objectives, a cash offer might be the solution you’re looking for. Let’s take a look at the process of selling a house to a cash buyer.

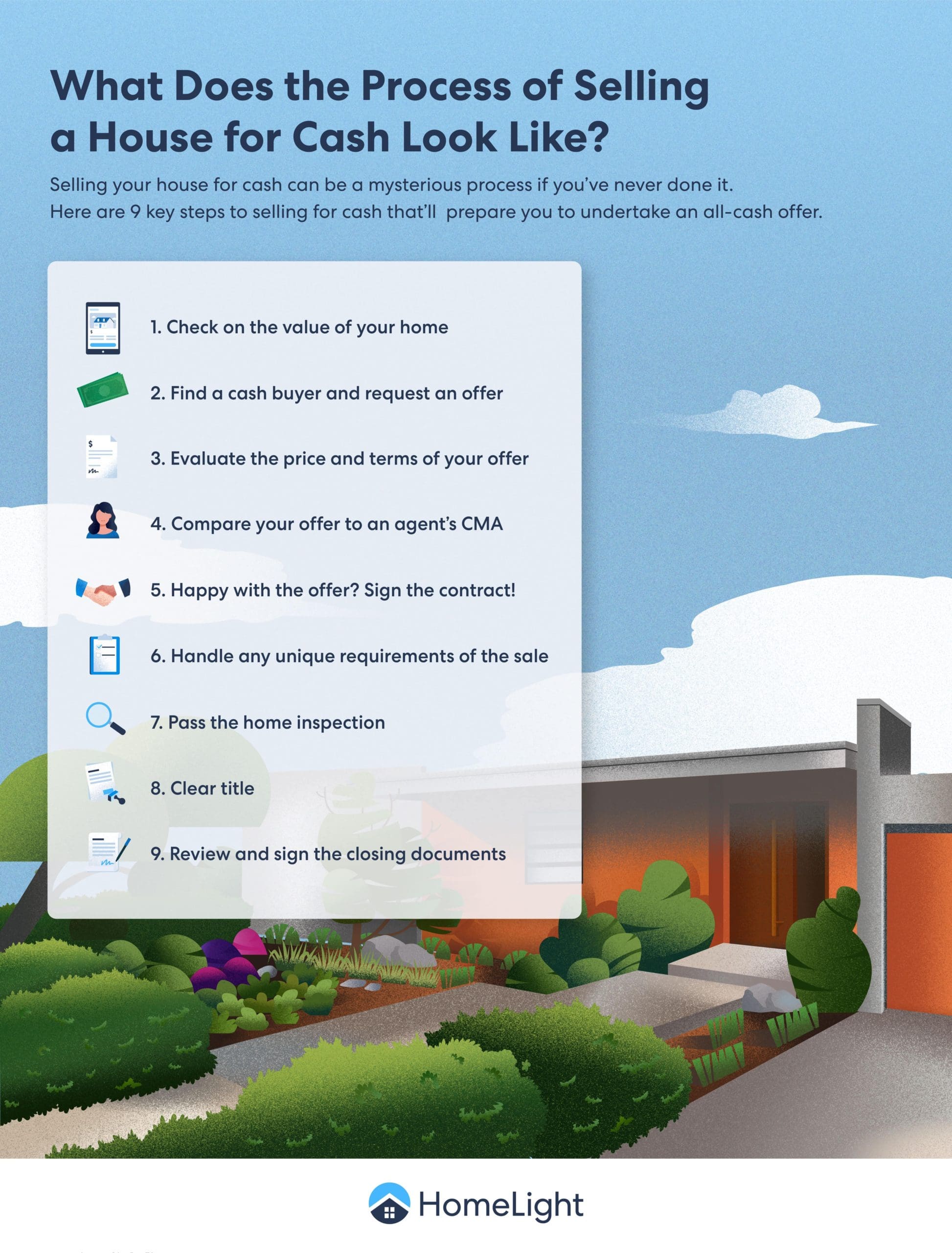

9 steps to selling your home for cash

In this section, we walk you through the process of selling a house for cash, step by step, so you can make an informed decision about whether it’s right for you.

1. Check on the value of your home

Cash buyers provide a variety of conveniences to sellers, including a shorter closing, increased level of certainty, and the option to sell “as is” and save money on repairs.

However, cash offers tend to be lower than financed offers. So while you can expect to receive somewhat of a discount on price — how much so will depend on market competition and the state of your home — you should get a ballpark idea of your home’s current fair market value, so you can recognize if you’re getting lowballed.

Homeowners can request a free home value estimate online thanks to the development of algorithmic automated valuation model (AVM) pricing tools. These online tools gather data from a variety of places, including county assessors, recorder’s offices, real estate property listing websites, title companies, and user-generated questionnaires to provide near-instant property value estimates.

While an online valuation won’t deliver the same level of accuracy as a professional appraisal or a real estate agent’s comparative market analysis, requesting one is quick — not to mention often completely free. HomeLight’s Home Value Estimator is a good place to start.

Need a Simple Way to Sell Your House?

Get an all-cash offer through HomeLight whenever you’re ready. Receive your offer within a week and close in as little as 10 days. No showings, no repairs, no open houses. Available to sellers across the U.S.

2. Find a cash buyer and request an offer

You know your home’s worth, and you’re ready to search for a qualified cash buyer. Below are some of the most common cash buyer options:

Types of cash home buyers

Franchisors: These are real estate investment companies that franchise their model under their company name in multiple locations, such as We Buy Ugly Houses or Express Home Buyers. They usually buy homes “as is” and offer only about 50% to 70% of a home’s after-repair value to account for the amount of work the house needs.

iBuyers: The typical iBuyer uses an automated valuation model (AVM) to generate a competitive offer closer to market value on a home that needs only minimal work. Because of that, they tend to pay more than franchisors. Most charge a service fee of about 5%-6%, similar to an agent’s commission. Some well-known iBuyer companies include Simple Sale, Opendoor, and Offerpad.

With HomeLight Simple Sale, simply fill out an easy questionnaire about your property and receive a no-obligation cash offer for your home within a week. This online platform matches sellers with network buyers who use a variety of investment strategies and buy a wide array of properties, including homes that need a little or a lot of work. Simple Sale and HomeLight have a track record of satisfied customers. With a cash buyer platform such as HomeLight’s Simple Sale, you can skip the repairs and showings and sell your home in as little as 10 days.

House flippers: House flipping companies such as “We Buy Houses” purchase homes in need of repair, renovate them, and then sell them quickly as turnkey properties. They’re looking for a bargain, so they can maximize profits. Flippers generally follow a 70% rule, which stipulates to offer no more than 70% of a property’s after-repair value (ARV). Estimated repair costs are typically subtracted from the 70%.

Buy-and-hold investors: This type of buyer buys a home and then converts it into a rental property. They may sell the property once it has appreciated in value enough, as part of a long-term investment strategy. Unlike flippers, buy-and-hold investors will calculate the rental income potential of a property, making it difficult to identify an offer range. Location and condition will play big roles in the offer you receive.

Buy before you sell services: Companies that provide buy-before-you-sell programs can help you buy — and move into — your new home before you sell your current home. These companies allow you to seamlessly unlock equity from your current home so you can make a strong offer on your new home without a Home Sale Contingency. (You also only move once.) Some examples of “buy before you sell” services include HomeLight, Knock, and Orchard. These companies often provide a backup cash offer to purchase your home if it does not sell on the open market in a specified time period, such as 90 days. To learn about HomeLight’s innovative “Buy Before You Sell” program, check out this short video.

Consult with a top real estate agent

Maybe requesting a cash offer online right off the bat isn’t your style. You’d like an advisor to walk you through the process. No problem!

You can ask a knowledgeable real estate agent experienced in cash sales for a cash buyer recommendation. Many agents are active in their local investor community and have an inside track to finding cash buyers.

Indar Lange, the owner of Honolulu-based Our Home Investments, Hawaii’s largest home-flipping company, says 60%-70% of his cash investments are the result of his relationships with agents. “We work with multiple agents who know we can buy for cash, including homes no one wants.”

3. Evaluate the price and terms of your offer

Evaluating a cash offer can be tricky. There’s no one-size-fits-all formula to calculate the strength of an offer. And there are other factors to weigh besides the amount of profit you’ll make.

Here are some key things to keep in mind when assessing an offer:

Your home’s condition: If your house is in great shape, Travis Steinemann, a real estate investor and founder of BuyHousesBR.com, says you can look at comparable properties that have sold recently in your area with a similar size and level of finish, and then subtract the agent’s commission and throw in whatever discount you feel the benefits are worth.

“That will depend on your situation,” Steinemann shares from his experience working with a variety of sellers. “Someone who is going through a foreclosure or who has a vacant house may value the speed and benefits of cash more than someone who just wants a bigger house.”

If your house needs work, he suggests taking the approximate value of updated houses in your area and subtracting what it would cost to get your house in that condition. Then deduct the commission, subtract the investor profit (usually 15%), and you will arrive at a fair price.

Terms (it’s not just about the price): Price is one thing, but not all cash offers will offer sellers the same terms either. Read the fine print to determine which steps the buyer is requesting to take before closing. For example, some investors will purchase the home “as is” but still require an inspection; some will offer to waive the inspection entirely, though it may mean accepting a reduced price to hedge the investor’s risk of finding major issues with the property.

While the use of all cash eliminates the need for a lender-ordered appraisal, some buyers may still request to have the house appraised before closing. What type of terms you can negotiate will depend on factors like the condition of your home and whether it’s a seller’s market. The fewer contract contingencies, the better (if you’re the seller).

Legitimacy of the offer: Before you move forward with the offer, you should review the following:

- Does the buyer plan on depositing an appropriate amount of earnest money?

- Does the buyer have a good track record of closing transactions?

- Is the buyer using a standard contract? If not, will you need an attorney to review the terms of the contract?

You should also request proof of funds to confirm that the buyer actually has the available cash to complete the purchase. This verification can come in the form of a certified bank letter with the official letterhead and should have the signature of the authorized bank personnel.

Pro tip: Top real estate agents recommend going a step further to confirm that the proof of funds letter hasn’t been forged. It’s wise to call the buyer’s bank to verify that the funds are available.

4. Compare your offer to an agent’s CMA

When you’re considering a cash offer, there is real value in reaching out to a trusted real estate agent to do a comparative market analysis of your home. This advanced pricing tool calculates the market value of your home by pulling in details about nearby properties of a similar size and style that have recently sold in your area. An agent uses these sale prices as a benchmark to set a home’s list price.

As an alternative, you could also order your own home appraisal. “Although appraisals vary quite a bit and aren’t an absolute guarantee, it could help if you’re really struggling to pinpoint what would be a good price,” says Joanne McCoy, a top real estate agent in Lincoln, Nebraska, with nearly 20 years of experience. “At the end of the day, if you’re going to get less than market value, you have to decide whether the benefits outweigh that loss.”

5. Happy with the offer? Sign the contract!

After accepting a cash offer, it’s time to sign the contract. This part of the process is very similar to what happens during a conventional home sale. You can choose to sign and accept the contract or have an attorney review the terms. The contract, which is usually prepared by the buyer, should include the following key details:

- Purchase price

- Deposit amount

- Any additional required fees

- Closing date

6. Handle any unique requirements of the sale

Depending on the buyer and local laws governing residential home sales, there may be some tasks you are required to complete to keep the sale process moving forward.

For example, home sellers are usually required to disclose any known information about a property that could impact its value or the ability to live there safely. Every state has its own rules about what’s legally necessary to disclose, and you can ask a real estate attorney or representative from the title company to provide you with the right documentation for your locale.

There may also be extenuating circumstances that can lengthen the cash sale process a bit. For example, if the house is in a homeowners association, the HOA may require 30 days to process the buyer’s application.

Another aspect of a real estate closing is the municipal lien search. In some municipalities, it only takes a few days. In others, it can take up to three or four weeks.

7. Pass the home inspection

Some cash buyers require a home inspection. Others may purchase a home “sight unseen” or choose to waive the inspection.

“They would do this if they know their price is so good that anything wrong with the home is not an issue, or if they are planning on tearing down the home, and the land value is all that matters to them,” explains Steinemann. Those types of offers usually close very fast, in around seven to 10 days.

But buyers who opt for an inspection may renegotiate the final offer price to cover any required repairs, so it’s smart to anticipate and plan for more back-and-forth and a potential price reduction if an inspection is required for your sale.

8. Clear title

Title problems can delay your closing, and a title search will be necessary to close the sale regardless of whether your buyer is paying all cash or needs a mortgage. Unpaid taxes, a second mortgage, mechanic’s liens for past work done on the property, and outstanding alimony or child support are all common defects that can appear on your title and prevent the sale from moving forward until cleared.

You can get ahead of any surprises by ordering a preliminary title report and handling any disputes or paying off liens ahead of time.

9. Review and sign the closing documents

The closing will likely be held at the office of a title company, escrow company, or real estate attorney, depending on customs for your state. You’ll sign the same documents as you would in a traditional sale, such as the deed, settlement statement, and any property disclosures that haven’t already been completed. You can choose to have the title company draft the paperwork or let an attorney handle it.

What are the advantages of selling a house for cash?

Now that you’re familiar with the process of selling a house for cash, should you do it? Here are a few benefits that can make this avenue more enticing.

Fast and guaranteed closing

Across the board, the main draws of a cash sale are speed and certainty. There’s always a chance a financed deal could fall through if the buyer doesn’t get approval for the loan or if the appraisal comes in lower than the contract price — a long and frustrating process may take a seller back to square one.

“With cash, you can close fast without any hassles,” says Lange. “With a mortgage, lenders can take 60 days, sometimes more, to clear everything — there are a lot of hoops to jump through.”

Check out this table for a snapshot of how much faster each step of a cash sale moves compared to a financed sale.

| Steps | Typical number of days for a cash sale | Typical days for financed sale |

| Prepping | 0 | 30 – 90 |

| Getting an offer | 1 – 3 | 30 – 60 |

| Closing | 7 – 14 | 30 – 60 |

| Total: 8 -16 days | Total: 90 – 210 days |

Less stress

Selling a house can be stressful, but when working with a cash buyer, many of the common headaches and uncertainties of selling a home — such as staging, showings, and appraisals — are off the table, which means a simpler, more straightforward process.

Reduced fees

Although the offer amount from an investor will likely be lower than what you could get in a traditional sale, it can be offset with money you don’t have to spend on commission, concessions, and prep work.

“In a retail market sale, most of the transactional costs, such as agent commissions for both listing and buyer’s agents and closing costs for escrow, fall on the seller,” notes Johell Aponte, founder and acquisitions manager with Move On House Buyers.

“Plus, the seller is often asked to support buyers with closing cost concessions, pre-listing repairs and updates, post-inspection repairs, and possible extended hold times, all of which can add up to substantial costs.”

Flexibility

In addition to speed, a flexible schedule is another benefit of selling for cash. For example, if you need to close on your next home before moving, an investor or flipper will be more likely to delay possession after closing than a traditional buyer would.

Quicker path to your next home

Let’s say you’ve found the perfect home that checks off all the items on your list and is within your price range, but it’s getting a lot of interest and multiple offers. By taking a cash sale on your current house, you may be in a better position to secure your next home, because that seller won’t have to wait around on any contingencies or financing delays.

Skip repairs and sell “as is”

Some loan programs that a traditional buyer would use to purchase a home come with strict guidelines that can make fixer-uppers more difficult to sell. “Many of the houses we purchase are not livable — the owners couldn’t get a loan even if they wanted to,” says Lange. “Sometimes the bank is knocking on their door, or there are eviction notices in the window. Cash gives them a way out.”

A cash buyer might make an offer that’s close to list price, but then they often ask for pricey repairs at the inspection stage. When all is said and done, the final price might be up to 15% below fair market value.

Kevin Kendrick Real Estate AgentCloseKevin Kendrick Real Estate Agent at Keller Williams, Advantage III Realty

Kevin Kendrick Real Estate AgentCloseKevin Kendrick Real Estate Agent at Keller Williams, Advantage III Realty

- Years of Experience 14

- Transactions 418

- Average Price Point $449k

- Single Family Homes 341

What are the disadvantages of selling a house for cash?

A cash offer isn’t always a silver bullet (no solution to selling your home is), so before you move forward, you should be aware of these common drawbacks.

Lower price

When selling for cash, all of that speed and convenience comes at a cost: You’ll generally sacrifice a chunk of change on the sale price, as cash buyers are typically looking to pay below market value.

“It depends on the market hold times and costs, but sellers may expect to leave on the table anywhere between 8% to 15% of what they would have projected to get from a successful retail sales process,” says Aponte.

At the end of the day, investors are running a business — a low-margin one, at that — and they need to make money to keep buying homes. “Investors need to buy at a discount because they’re often putting hundreds of thousands of dollars into a property,” says Lange. “They have to find a way to get value out of a purchase. Selling a home for cash should be a win-win for both sides. Both parties should feel comfortable with what they’re getting.”

Wondering how much you might make selling your home on the traditional market? Estimate the cost of selling your home and the net proceeds you could earn from the sale using HomeLight’s Net Proceeds Calculator.

Potential for fraud

The cash-buying market can be riskier, and some have been called out for predatory tactics. Before entering into any contract, thoroughly research the company or person and ask for references from past sellers.

Be wary of any buyers who show no interest in seeing your home in person and who only correspond via email, as those could be red flags of a scam. HomeLight, which provides cash offers through our Simple Sale platform, is accredited by the Better Business Bureau and holds an A+ rating.

To avoid getting lowballed, perform a few price checks using a home value estimator or ask a reputable real estate agent for a second opinion.

Possibility of “bait and switch”

Kevin Kendrick, a top Orlando agent who is also a certified iBuyer, sometimes sees reasonable cash offers come in for his sellers, which can be exciting at first — but that offer isn’t set in stone until the contract is finalized.

“A cash buyer might make an offer that’s close to list price, but then they often ask for pricey repairs at the inspection stage,” he explains. “When all is said and done, the final price might be up to 15% below fair market value.”

Is cash king? When selling a house for cash, it’s your call!

Now that we’ve demystified the process of selling a house for cash, you can decide if speed and peace of mind outweigh the possible drawbacks.

As a home seller, one of the big things you want to do is eliminate as many question marks as possible and find a solution that fits your needs. If the questions involve a need for speed or simplicity — a cash offer can do both and more.

Writer Dorothy O’Donnell contributed to this story.

Header Image Source: (Drew Dau / Unsplash)