How Often Do Contingent Offers Fall Through? Breaking Down the Risk

- Published on

- 5 min read

-

Presley Attardo Contributing AuthorClose

Presley Attardo Contributing AuthorClose Presley Attardo Contributing Author

Presley Attardo Contributing AuthorPresley is a Seattle based writer covering interior design trends, home improvement, and market updates. She has lived in San Francisco, Los Angeles, Chicago, and Washington, D.C., giving her a unique perspective on the diversity of U.S. real estate.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.

In real estate, an offer typically doesn’t constitute a done deal. As a seller you want to know: how often do contingent offers fall through, and what are your odds of actually closing?

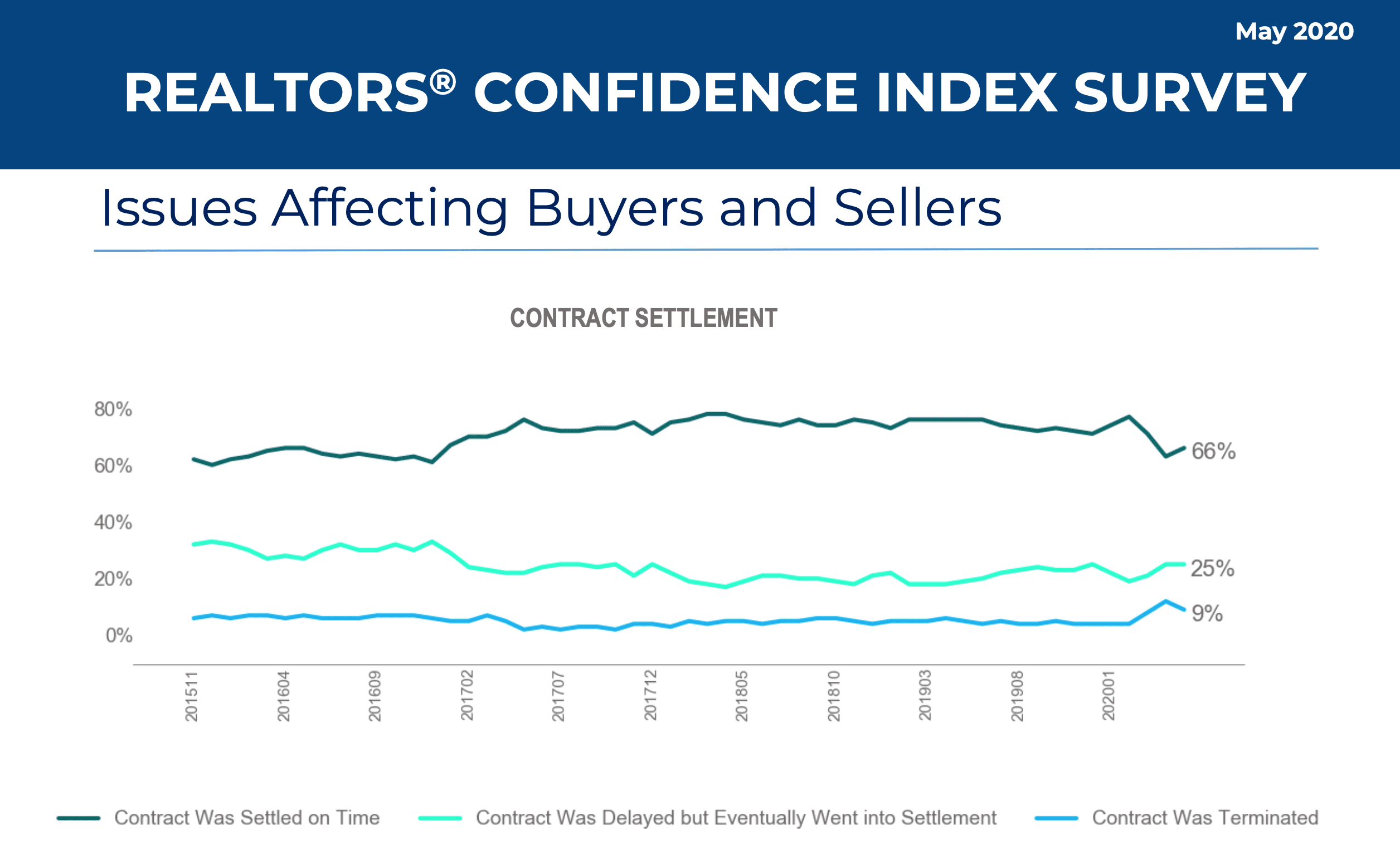

As you measure your risk, here’s what you should know. The majority of real estate offers contain contingencies, i.e., these “if and only if” clauses. A recent survey by the National Association of Realtors (NAR) reveals that in May 2020, 76% of recent closed sales contained purchase contingencies and 9% of contracts were terminated.

The top reasons for contract termination recently include the buyer lost their job (28% — a higher-than-normal cause due to COVID-19), issues related to obtaining financing (21%), home inspections (17%), and other contingencies stated in the contract (7%).

In previous months, however — prior to the impact of the pandemic — NAR has reported that terminated contracts only represented 2% to 5% of deals in a given month. So based on these numbers, you could reasonably conclude that a real estate contract has anywhere from a 1%-10% chance of falling out of contract, which means the odds of settlement are pretty good even in uncertain times. It’s far more likely that your contract will get delayed and still close, NAR’s data consistently shows.

But any risk when you’re selling your home is a bad thing.

For an in-depth analysis of how often contingent offers fall through, we’ve rounded up additional relevant stats and consulted top real estate agent Liz Donnelly, who closes 17% more sales than the average agent in Ventura, CA. We’ll explain the riskiest contingencies and what you can do as a seller to protect your sale.

The usual suspects: Contingencies to watch out for

Contingencies are legal clauses stating that certain requirements must be met for the contract to close. Contingencies mostly protect the buyer’s interest, allowing them to exit the contract with their earnest money if they cannot fulfill the stated requirements. Here’s a rundown of the most common contingent offers and how likely they are to fall through:

Home sale contingency

- The deal: The buyer’s offer is contingent on them selling their home first.

- Risk level: High

- Stats we know: In May 2020, 6% of offers included a home sale contingency.

- Top real estate agent advice: Avoid entering a contract with an offer that includes this contingency. There is a high risk that the contingent offer could fall through and jeopardize your sale. Donnelly explains:

“Picture yourself five days before your closing, when you’ve already paid $X amount of money for your moving van, or even moved everything out of your house. If that other house falls through, now you’re in a situation where you need to start over, and you have a house that’s not showing as well as it was when you first put it on the market because now you have little dents in your carpet from where your sofa was and the faded areas on the walls where the bed frames were.”

Financing contingency

- The deal: The buyer’s offer is contingent on their lender approving their mortgage.

- Risk level: Moderate

- Stats we know: Financing issues caused 21% of terminated contracts in May 2020. With 86% of recent buyers financing their home purchase, on average financing around 88% of the purchase, financing contingencies are commonplace. Nonetheless, a financing contingency entails risk since even pre-approved buyers may fail a mortgage application if they lose a source of income or acquire debt after their initial application.

- Top real estate agent advice: If you’re considering an offer with a financing contingency, reach out to the buyer’s lender to vet their financial strength before entering a contract. Your agent can ask the lender for details on the buyer’s employment to better gauge the likelihood that the loan will approve.

Inspection contingency

- The deal: The buyer’s offer is contingent on the home inspection report. Buyers use the findings as leverage to negotiate a better deal, asking the seller to handle the repairs or include repair credits in the sale to cover the costs. If the seller refuses, the buyer can walk away with their earnest money.

- Risk level: Moderate

- Stats we know: In May, 17% of contracts were terminated due to home inspection and environmental issues. The home inspection contingency is expected in most offers, with 95% of recently purchased homes undergoing inspection. Since the average home purchased in 2019 was over 30 years old, it’s no surprise that the inspection is the culprit behind many contract terminations and delays.

- Top real estate agent advice: To avoid tension and dispute in the final hour, conduct a pre-listing home inspection before you list your home. Costing on average $278 – $399, a pre-listing inspection allows you to discover issues and tackle repairs before buyers enter the picture. Even better, the completed inspection gives your buyers confidence in the condition of your home before they offer, empowering them to submit a higher offer than they would if they anticipated repairs.

Appraisal contingency

- The deal: The buyer’s offer is contingent on the home appraising for an equal or higher value than the offer amount.

- Risk level: Low to moderate

- Stats we know: 6% of contracts in May fell through from appraisal issues. According to Fannie Mae, the largest backer of 30-year fixed-rate mortgages, only 5% of home appraisals come in low. HomeLight’s recent research suggests a higher figure, with interviewed experts estimating that appraisals come in low 10% to 20% of the time.

- Top real estate agent advice: Lenders will require an appraisal as a condition of financing. Still you can negotiate to remove the contingency whether you’re selling to a cash or a financed buyer, though the financed buyer incurs greater risk. If their appraisal comes in low, they’ll need to make up the difference between their offer amount and the loan (covering the appraised value) in cash, or cancel the sale and forfeit their earnest money. You’re most likely to negotiate waiving the appraisal if you’re selling in an ultra-competitive market where buyers will do anything to win a bidding war.

Market conditions increase the risk of some contingencies

In theory, you want to accept an offer with few contingencies — the fewer contingencies, the more likely the deal is to close. But the reality is, the market will largely dictate your ability to avoid contingent offers or not, not to mention influence the probability that a contingent offer will succeed or fall through.

Buyer’s market: With fewer offers, sellers agree to more contingencies

In a buyer’s market, the inventory of homes is high compared to the number of buyers. With fewer buyers offering on homes, you’re more likely to deal with contingencies to secure a sale. Donnelly explains that in slow markets, even offers with home sale contingencies are desirable:

“I remember feeling that way about two years ago when we weren’t selling much and hit a low for three or four months. During that time, not knowing what the future brings, it’s like, hey, a buyer’s a buyer, and maybe it’s going to take you a little bit longer to close this sale, but it may be something you want to look into.”

Seller’s market: Expect more offers with fewer contingencies

In a hot seller’s market where the buyer pool greatly exceeds the inventory of homes for sale, buyers may cut contingencies out of their offer to compete for the limited housing options. As a seller, you’re also more likely to receive multiple offers, allowing you to pass up those with risky contingencies.

On the other hand, when your home sparks a bidding war, effectively driving up the price of your home higher than market value, you need to watch out for buyers’ appraisal contingencies. If the home appraises for less than the winning buyer’s offer, you may need to adjust the deal accordingly.

Unsteady economy: Financing contingencies break deals due to unexpected job losses

When the economy dips, contingent offers are more likely to fall through. Buyers who unexpectedly lose income may fail to qualify for a loan, walking away from the deal via financing contingency. Likewise, buyers with home sale contingencies may lose their buyer from the same cause, or themselves may decide against moving until the economy improves.

Donnelly confirms that more contingent offers fell through in her market than usual in the past few months due to pandemic related job losses:

“There was a really nice young couple who I had been showing houses to for a while. We found the perfect home, we wrote the offer, and I mean honestly, it was literally the next day that they closed their business — she owns a gym. So they canceled their offer on an $800,000 home.”

Donnelly’s client was one of nearly 11,700 transactions that fell out of escrow in March 2020 in neighboring Los Angeles, Orange, Riverside, and San Bernardino counties.

Hedge the risk of contingencies falling through

While the market’s movements are out of your hands, you hold power to avoid contingencies or at least to negotiate them in your favor.

Skip financing contingencies with a cash buyer

The best way to avoid contingencies? Sell your home to a cash buyer. Cash buyers have the funds to pay for your home today, guaranteeing a shorter, more straightforward closing. HomeLight’s Simple Sale platform is the fastest way to match with a pre-approved cash buyer. Just answer a few questions about your home online, and we’ll connect you to the highest bidding buyer in our network in 48 hours or less.

Need to Sell Your House Fast?

Find out what cash buyer are willing to pay for your home right now.

Add a kick-out clause to home sale contingencies

Though never ideal, there are scenarios where an offer contingent on a home sale is your best option (e.g., if it’s a slow buyer’s market or if the contingent offer is significantly higher than competing offers).

If you accept an offer with a home sale contingency, add a kick-out clause to the contract stating that you can cancel the contract if you receive a better offer from another buyer. Before pursuing the new offer, you’ll need to provide the original buyer with adequate notice (such as 72 hours) to give them an opportunity to remove their contingency and close.

Will your contingent offer fall through? Consult your agent

When in doubt, ask your agent for advice on approaching a contingent offer. A top real estate agent can inform you how often contingent offers fall through in your market and devise a plan to best ensure your home sale closes.

Header Image Source: (Brooke Cagle / Unsplash)