What Is a CD in Real Estate? (Closing Disclosure)

- Published on

- 7 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

Buying a home involves a flurry of paperwork, but perhaps the most important document is the closing disclosure, also known as a CD in real estate. This finish-line form is key to understanding the costs and commitments associated with your purchase.

This guide will break down what a CD includes, why it’s so important, and the most common mistakes to watch for so your closing doesn’t get delayed.

Achieve Greater Buyer Confidence With a Top Agent

HomeLight can connect you with the most experienced buyer’s agents in your home shopping area. These top professionals can help you make the best buying decisions and protect your interests.

What is a CD in real estate?

A closing disclosure, or CD, is a five-page form that provides final details about the mortgage loan you have selected. It includes the loan terms, your projected monthly payments, and how much you will pay in fees and other costs to get your mortgage.

“The closing disclosure also explains to all the parties involved what exactly each one is being charged,” explains Deborah Lucci, a top-rated Massachusetts real estate agent with 28 years of experience. “For example, the CD will show how much tax is allotted to the seller and how much is allotted to the buyer, based on when the property sale is closed and when the taxes were last paid.”

The CD is given to homebuyers at least three business days before closing, allowing time to review and ensure everything is correct. This document is not just a formality; it’s a critical piece of the homebuying puzzle, ensuring there are no surprises on closing day.

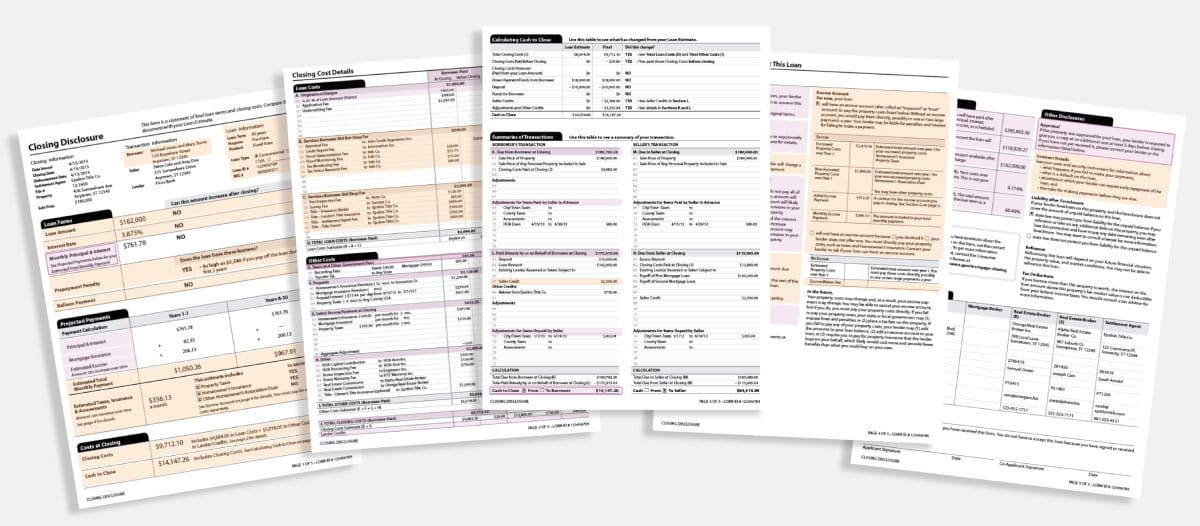

Sample closing disclosure (CD)

A typical CD will contain several key sections:

- Loan information: Details about the type of loan, interest rate, and term.

- Loan terms: This includes your loan amount, interest rate, and whether these can change after closing.

- Projected payments: Breakdown of your monthly payment, including principal, interest, mortgage insurance, and estimated escrow.

- Costs at closing: Summary of transaction costs, including loan fees, property taxes, and homeowner’s insurance.

Take a closer look: The Consumer Financial Protection Bureau (CFPB) has created a sample CD interactive checklist that guides you through each section of the 5-page closing disclosure form.

Formerly known as a settlement statement

Before Aug. 1, 2015, the CD was known as the HUD-1 Settlement Statement, which was long and difficult to read. Buyers would typically not receive it until the day of closing, which didn’t allow much time for review. The document was redesigned and implemented under the TILA-RESPA Integrated Disclosure (TRID) rules to make it easier for consumers to understand. Lenders are now required to provide a CD at least three business days before the closing date.

What is an LE in real estate?

A loan estimate (LE) is a three-page document that outlines the proposed terms and costs associated with your mortgage. Provided by your lender within three business days after you apply for a loan, the LE includes detailed information about the loan’s interest rate, monthly payments, and total closing costs, including lender fees, real estate taxes, and homeowners insurance premiums.

This estimate allows you to compare different loans and negotiate with lenders, helping you make informed decisions early in the homebuying process.

Lucci says buyers should carefully review the LE, but “the closing disclosure is the final number, and shows what’s really going to happen for both the buyer and the seller.”

Sample loan estimate (LE)

A typical loan estimate (LE) will outline much of the same information as a CD, such as loan terms, projected payments, estimated closing costs, and a summary of the total amount of money you will need at closing, including your down payment and all fees.

Take a closer look: This CFPB page contains sample loan estimate forms — both blank and completed.

Compare your CD and LE

Comparing your closing disclosure (CD) with your loan estimate (LE) is a key step in the mortgage process.

“Go over every line item and make sure you understand them,” Lucci advises. “You may not know what some of these fees really are, and so I would go over these with your attorney or the closing attorney to simplify everything for you. That way, on the day of the closing, you’ll be very clear on what’s being charged to you.”

This comparison ensures that there are no surprises between what was initially offered and the final terms you are committing to. Discrepancies in numbers can happen, and it’s important to catch these changes early. Look for differences in interest rates, fees, and cash needed at closing. Question anything you don’t understand.

12 things to confirm are correct on your CD

By law, you will receive your closing disclosure at least three business days before your scheduled closing. This period is designed to give you ample time to confirm all details are accurate. Here are key items to review:

- Name spelling: Ensure your name is spelled correctly.

- Property address: Verify the address of the property you are buying.

- Length of your loan (loan term): Confirm the duration of your loan is what you agreed upon.

- Loan type: Check whether it’s a fixed-rate, adjustable-rate, or another type of loan.

- Interest rate: Make sure the rate matches what was promised.

- Loan amount: Review the total amount borrowed.

- “Cash to close” amount: This should match your most recent estimates.

- Closing costs: Confirm these are as expected.

- Estimated monthly payment: Ensure this matches your expectations.

- Prepayment penalty amount: If applicable, check this figure.

- Estimated taxes, insurance, and other payments: Verify these amounts are correct.

- Balloon payment: If your loan includes a balloon payment, ensure the amount and due date are accurately listed.

You’ll also want to review other items in your CD, but these are some of the key factors that can cause delays or create unwanted surprises.

What if you find a mistake on your CD?

If you discover an error on your closing disclosure, it’s important to act immediately. Contact your lender to discuss the discrepancy and request a corrected version. The error could be related to the loan terms, fees, or other critical details that affect your closing costs and monthly payments. Addressing these issues before closing ensures that you agree to terms that are accurate and fair, preventing any future financial surprises.

Most common CD errors

Here are some of the most common errors to watch out for in your closing disclosure:

- Inaccurate or missing CD completion date

- Incorrect personal information or property address

- Wrong loan amount

- Incorrect insurance and assessment amounts

- Miscalculated estimated taxes

- Inaccurate or missing HOA dues

- Misplacement of third-party fees

- Miscalculations in cash to close table

- No mention of liabilities for partial payments

- Misstated or missing incentives (seller credits or buyer rebates)

- Missing signatures

A top agent can guide you through a CD

Navigating the complexities of a closing disclosure can be challenging, but a top real estate agent can provide invaluable assistance. With their expertise, they can help you understand every detail of your CD, from deciphering legal jargon to ensuring that all financial information is correct.

“I think it’s important to hire local people — your real estate agent, your mortgage broker, your attorney, all those parties concerned,” Lucci recommends. “If you hire local people, they’re more likely to understand what’s going on in your market, more so than somebody farther away. This can make your transaction much easier for you.”

An experienced agent also acts as your advocate, ensuring that your homebuying process is as smooth and error-free as possible.

HomeLight can connect you with a top-performing, trusted agent in your market. We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs.

Header Image Source: (Johnson Johnson / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.