How Long Does It Take to Close On a House With Cash in 2026? Here’s Your Timeline

- Published on

- 11 min read

-

Dena Landon, Contributing AuthorClose

Dena Landon Contributing Author

Dena Landon, Contributing AuthorClose

Dena Landon Contributing AuthorDena Landon is a writer with over 10 years of experience and has had bylines appear in The Washington Post, Salon, Good Housekeeping and more. A homeowner and real estate investor herself, Dena's bought and sold four homes, worked in property management for other investors, and has written over 200 articles on real estate.

-

Richard Haddad, Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

Why pay cash for a home? Mortgage interest is tax-deductible, and many homeowners appreciate the deduction. If you only pay cash for the down payment and take out a mortgage for the remainder of the purchase price, it keeps more money in your pocket. Despite this, there are benefits to a cash offer.

In a competitive market, paying cash could help you beat out other homebuyers. Sellers tend to prefer all-cash offers because those deals close more quickly. Byron Ford Jr, an agent in New Bedford, Massachusetts, works with 76% more single-family homes than other agents in his area. Given the persistent low supply of homes on the market over the last few years and rising interest rates, he’s seen a sharp uptick in cash offers.

Need Assistance Buying a House With Cash?

Find a top-rated real estate agent who can help you navigate the entire process, from determining which homes are well-priced to making your offer stand out.

Even the challenging market conditions of 2026, as described by top agents surveyed by HomeLight, haven’t significantly dimmed the appeal of cash offers. The volume of real estate transactions has fluctuated in the first half of the year, and there is more inventory on the market. As of June 2026, the National Association of Realtors (NAR) estimates a 4.6-month supply of unsold homes on the market (a 6-month supply is considered balanced).

That means the market remains fairly competitive, which is reflected in both consistently elevated home prices and the ongoing ubiquity of cash offers. NAR reported that the share of buyers making all-cash purchases accounted for 25% of home sales in June 2026.

Ford speculates that one reason cash is popular is that “you don’t have to go through the appraisal or the bank approval process — it’s cleaner.”

But other than reaching the closing table faster with cash, especially if you need to sell your house fast, another advantage to a cash offer is that it saves you money long-term, especially when buyers are facing higher interest rates.

Michael Simpkins, a real estate agent in Apollo Beach, Florida, says another advantage to paying cash over taking out a mortgage to buy a home is that you’ll save on closing costs. He estimates that on a $200,000 house, you could save between $5,000 and $6,000 in closing costs.

Paying cash saves you money, and you might need a place to live sooner rather than later. But just how long does it take to close on a house with cash, compared to a traditional loan?

Setting the standard

If you’re buying a house with a standard mortgage, closing takes about 43 days. Why does it take this long?

Buying a home is a large financial transaction with many legal ramifications. Everyone involved will need time to perform their due diligence. The bulk of the time, however, is consumed by loan underwriting and processing.

A cash buyer can skip everything related to a mortgage, from the home appraisal to income verification, which saves them a ton of time. But there are still some loose ends that the cash buyer should tie up before racing to the closing table.

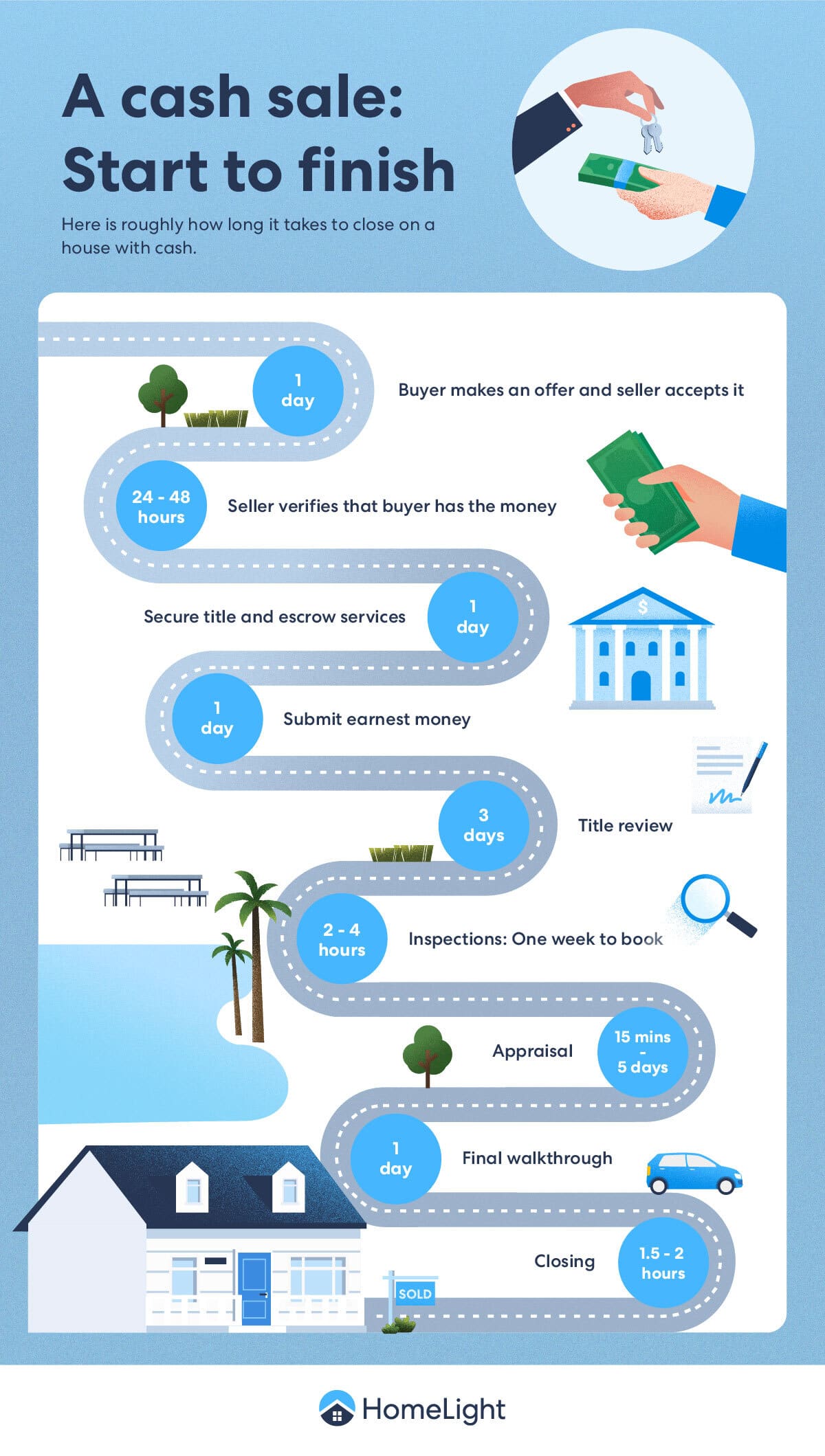

A cash sale: Start to finish

Every home sale has its quirks, but in general, “a cash sale can be turned over in a week to two weeks,” according to Suz Poepke Pohl, owner and escrow agent at Cygneture Title Solutions for more than 10 years. With a cash sale, you can skip a few steps in the typical closing process.

Here is roughly how long it takes to close on a house with cash.

The cash buyer makes an offer, and the seller accepts it: 1 day

Making an offer and having it accepted works a lot like any other home sale — unless you’re asking for a cash discount. If the seller has an urgent need to close quickly, they might be willing to negotiate a lower price in exchange for a quick close.

Simpkins points out: “When you can do a cash offer and a quick close in 7 to 10 days, it certainly makes sense to that seller, who has a payment due at the end of the month or who needs to move out quickly.”

A cash offer can also work in your favor if the owner has put in an offer on another home, and they need a solid offer on their home to move forward.

The seller needs to verify that the cash buyer has the money to buy the house: 24 to 48 hours

With a mortgage, the bank verifies that the buyer has the down payment available to close. Without a lender to verify funds, the seller will likely request proof of funds and earnest money from the buyer.

Some cash buyers may choose to supply this information with their offer letter; others may need to contact their bank and arrange for funds verification. This can be done before you make the cash offer to streamline the process.

Secure title and escrow services: 1 day

The escrow company will hold onto all the money while the deal is done, such as any earnest money you’re putting down. They’re a third party in your proceedings, ensuring that all the conditions of your real estate transaction are met. Many companies combine title and escrow services under one roof, as their functions are closely interrelated.

Your agent can help you find a title company to handle the title search and title insurance, which is always recommended. This task can happen while you’re obtaining the funds verification (if you didn’t do that in advance), as your bank will need information on where to transfer the money.

Submit earnest money: 1 day

An earnest money deposit demonstrates your good faith to go through with the offer. In some cases, violating the terms of the purchase agreement allows the seller to keep your earnest money. Earnest money could be a flat amount or a percentage of the total sale price.

Whether you arrange for a wire transfer or write a good old-fashioned check, it will take at least a day for the earnest money to clear. Once it’s in the escrow company’s account, you can move forward.

Title search: 3 days

The title search goes back through a home’s title history to make sure there are no outstanding liens or heirs listed on the title. Even in a cash deal, you “still have to make sure that the property is clear of any encumbrances and any title issues at all,” Pohl says. Failing to verify a clean title could result in financial and legal headaches down the road.

While this typically takes just a few days, if the home has been through a foreclosure or short sale, it could take longer.

Mortgage lenders buy title insurance for themselves — it’s a good idea for buyers to do it, too. Before becoming an escrow agent, when Pohl bought her first home, she didn’t purchase title insurance. Years later, when the time came to sell, the title search discovered an outstanding judgment against the property. Even though it wasn’t her debt, she had to pay it off to sell the house.

Inspections: One week to book; 2 to 4 hours to complete

Cash buyers can waive an inspection in their purchase agreement, but it’s a very good idea to still have the property inspected “for informational purposes only.” This language in a purchase agreement reassures the seller that you’ll still go through with the purchase even if the home inspector finds issues.

An inspection can identify a serious hidden problem that could impact the home’s value. You also want to know what you’re getting into in terms of repairs, upgrades, and permits. It can take up to a week to book a standard inspection, and most inspectors will spend two to four hours in the home. Specialized inspections, such as a sewer scope or radon testing, might take more time.

Appraisal: 15 minutes to 5 days

An appraisal isn’t necessary in a cash deal, but Simpkins says that “unless it’s obvious that they’re getting a steal, I think they should still do an appraisal.” He points out that most cash buyers are buying, at the very most, once a year, and have less experience in the marketplace. Even though he closes five to eight homes a month, he’d still get an appraisal if he was doing a cash deal.

It’s a good idea to ask for an appraisal and include it in your purchase agreement to make sure that the home is worth the full purchase price. If you were working with a lender, the appraisal fee would be part of your closing costs; otherwise, it will typically cost anywhere between $300 and $500 for an appraisal.

An appraisal can take as little as 15 minutes (for a desktop appraisal) up to two weeks, including the time taken to write up the report. This time frame depends on many factors, such as the level of local market activity and how easy it is for the appraiser to find recent comparable home sales.

If the home appraises lower than the purchase price, it’ll be up to the cash buyer whether to move forward with the deal as-is or renegotiate. Ford says, “The biggest delay we’ve had is getting the appraiser out there; they’re going two or three weeks before they can get to an appointment,” which could add some time to closing.

Final walkthrough: 1 day

The day before you’re scheduled to close, you and your real estate agent will do a final walkthrough. Your agent takes you through the home to make sure that the previous owners have completely moved out and that it’s move-in ready. If the sellers agree to perform any repairs after the home inspection, you should check to see that they’ve been done.

Essentially, you’re ensuring that the house is in the same (or better!) condition that it was when you agreed to buy it.

Closing: 1.5 to 2 hours

When all these tasks have been completed, it’s time to close. Without the mortgage paperwork to sign, this should be pretty simple — less than an hour, and you’re finished. But Pohl has seen some closings in which the buyer was paying cash drag on for more than three hours because of improper purchase agreements.

In one case, she says the parties “were walking in and out; they didn’t have a Realtor and didn’t have a properly executed purchase agreement. In the end, the buyer paid for the seller’s fees so we could get it closed.” Even though you can skip some steps in a cash deal, you still need experienced professionals to help with paperwork.

Adding it all up

When you add everything together, here’s the absolute fastest you could close on an all-cash deal: about two weeks.

If you’re ultra-efficient, you could shave some time off: Ford notes that he’s had cash offers close in as fast as seven to 10 days. Keep in mind that many of these steps, such as an appraisal and your home inspection, can happen at the same time.

What can stretch out the timeline when you buy with cash?

Despite your and your agent’s best efforts to get a fast close, things can come up. Here are some common situations that can add days to the closing process.

Liens on the house

Unfortunately, not all title searches return a clear title. The title company could find past due property taxes or assessments, a lien from an unpaid contractor, or unpaid homeowners association dues. The sale can’t close until these liens have been cleared.

Bankruptcy

What if the seller has declared bankruptcy? Then they might need the court to approve the sale.

When someone on the title is no longer living

If someone listed on the title has passed away, you’ll have to take some extra steps to obtain a clear title. Required additional documentation will depend on whether the estate has cleared probate.

If not all of the heirs are verified, and not all of them agree to the sale terms, that can slow the process. If the deceased had a mortgage or reverse mortgage on the property, that will be another hurdle to clear.

Seller dishonesty

Unfortunately, sometimes people lie during the home sale process. A seller might have intentionally left something off the seller’s disclosures (in states where those are required) or tried to conceal a major defect. The title company or home inspector could find an issue that delays the sale while you work to clear it up — or choose to walk away.

Option periods

If you have concerns about your home purchase — whether you feel rushed or nervous about spending that much cash — your agent might suggest adding an option period into the contract. During this time period, you could change your mind. Option periods typically allow you to back out of the sale without any legal or financial issues.

Be aware that, in a hot market, many sellers dislike option periods even if you’re paying cash.

Low appraisals

When you’re paying with cash, the appraisal isn’t as important. You don’t need the house to appraise to qualify for a mortgage. However, it’s not a comfortable feeling to buy a house for more than it might be currently worth.

If an appraisal comes in low, you have a few choices. You can try to renegotiate the price, request a different appraisal, or back out of the purchase.

Save thousands when buying a home

HomeLight-recommended real estate agents are top-tier negotiators who understand the market data that helps you save as much as possible when buying your dream home.

What if you don’t have cash?

As of June 2026, the median sale price of a home in the United States is $440,600. You might be wondering — how are people paying cash for houses?

One way to do it is with a cash-purchase product like Flyhomes or Homeward. These products allow buyers to make a highly competitive all-cash offer on a home. Without a financing contingency, you’re more likely to win the home.

It’s possible to buy a house with cash and move the sale along quickly. If you’ve partnered with an experienced team of real estate agents, escrow agents, and title companies, closing on a home that you’re buying with cash will be a much simpler process than working with a lender.

Header Image Source: (Vivint Solar / Unsplash)

- "Publication 936 (2025), Home Mortgage Interest Deduction," IRS (April 2026)

- "Existing-Home Sales Housing Snapshot," NAR (June 2026)

- "REALTORS® Confidence Index," National Association of Realtors® (June 2026)

- "What Issues Require a Specialized Home Inspection?," ISN (October 2023)

- "Reverse Mortgages: How They Work And Who They’re Good For," Forbes (November 2025)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.