Ultimate Checklist: 20 Key Documents You’ll Need to Buy a House

- Published on

- 15 min read

-

Dena Landon, Contributing AuthorClose

Dena Landon Contributing Author

Dena Landon, Contributing AuthorClose

Dena Landon Contributing AuthorDena Landon is a writer with over 10 years of experience and has had bylines appear in The Washington Post, Salon, Good Housekeeping and more. A homeowner and real estate investor herself, Dena's bought and sold four homes, worked in property management for other investors, and has written over 200 articles on real estate.

-

Taryn Tacher, Senior EditorClose

Taryn Tacher Senior Editor

Taryn Tacher is the senior editorial operations manager and senior editor for HomeLight's Resource Centers. With eight years of editorial and operations experience, she previously managed editorial operations at Contently and content partnerships at Conde Nast. Taryn holds a bachelor's from the University of Florida College of Journalism, and she's written for GQ, Teen Vogue, Glamour, Allure, and Variety.

Buying a home comes with excitement, but also a fair amount of paperwork that can feel overwhelming at first. From loan applications to final signatures, every step of the process depends on having the right information ready at the right time. Understanding the documents needed to buy a house can make the journey a lot smoother and help you avoid delays when things start moving quickly.

And thankfully, your agent, mortgage lender, and title company will collect and monitor much of the paperwork.

Find a top real estate agent near you

We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs. It takes just two minutes to match you with the best real estate agents, who will contact you and guide you through the process.

Minnesota-based agent Becky O’Brien, who works with 67% more single-family homes than other agents in Maple Grove, explains that while you might have to sign some papers, “The good news is that buyers don’t need to handle very many documents, especially after they sign the purchase agreement and their house is under contract because their agent will handle most of it.”

But you might still have to manage documents from your lender, print out a pay stub, or make copies of your driver’s license. While you don’t need to worry about preparing many of the forms in the stack, here are 20 key documents needed to buy a house that you should be aware of and pay close attention to.

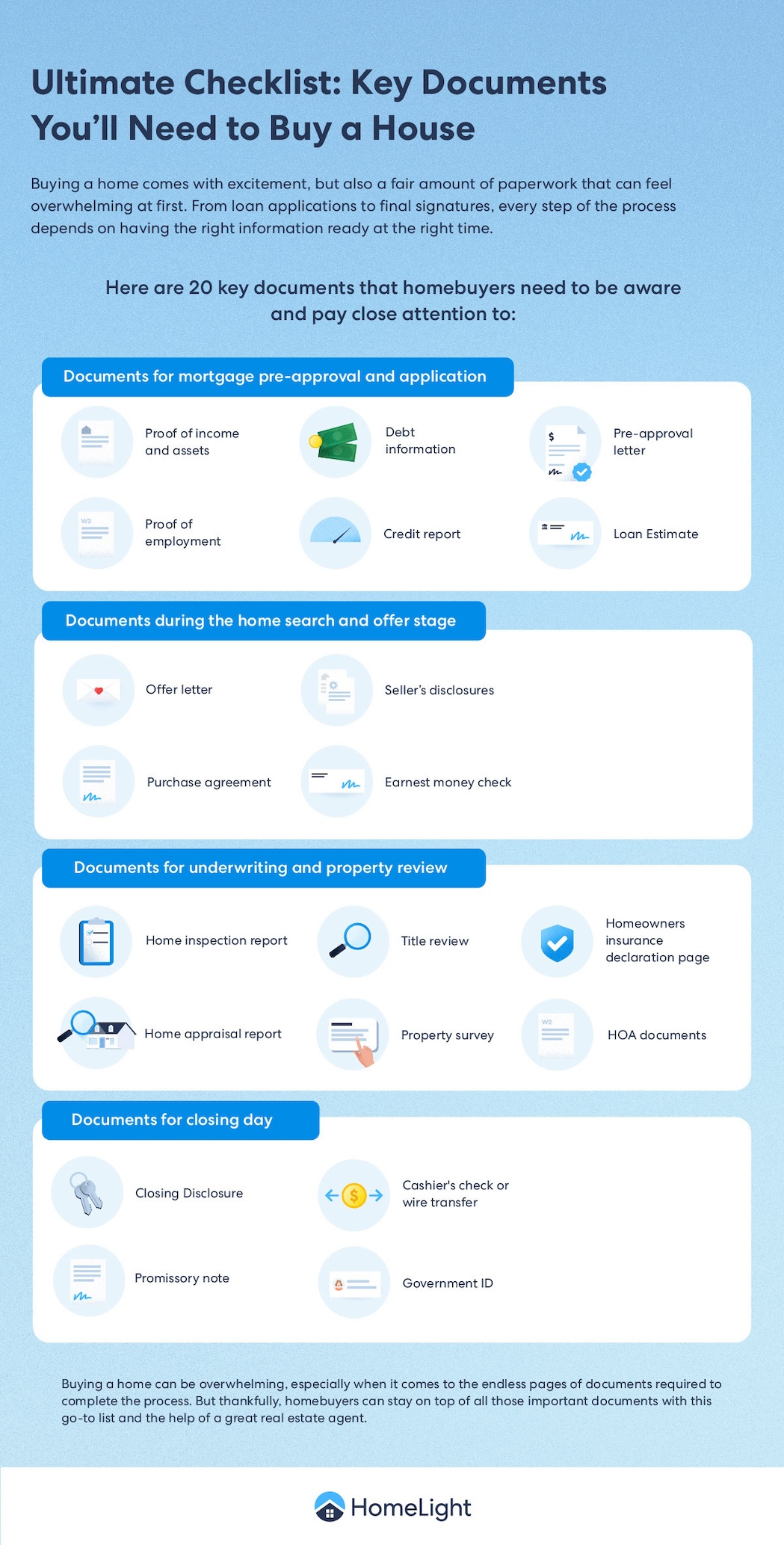

Documents for mortgage pre-approval and application

Before you can start seriously shopping for a home, you’ll need to show lenders that you’re financially prepared to take on a mortgage. This first phase focuses on the documents used to verify your income, assets, debts, and overall financial health during the pre-approval and loan application process.

1. Proof of income and assets

When you apply for a mortgage pre-approval with a lender, you’ll need to show them proof of income. Depending on the lender, they could request these documents:

- Pay stubs or other proof of employment

- Bank statements

- Retirement account statements

- Tax returns

- Gift letters

- Form 4506-T (gives your lender permission to pull a copy of your taxes from the IRS)

All of these documents prove that your income is what you’ve claimed it is and will also show the sources of your down payment.

2. Proof of employment

How do you plan on paying your mortgage? And how much can you pay each month? A lender wants to know that you can consistently make your payments, and will base your mortgage pre-approval amount in part on your monthly income.

Lenders could request pay stubs, W-2s, or 1099s, and the lender may also call your employer to verify employment. Expect them to re-verify employment a few days before the mortgage closing, too.

On self-employment and non-traditional income sources: If you’re self-employed or own a small business, expect lenders to request additional paperwork to verify your income. In addition to personal tax returns, you may need to provide business tax returns, profit and loss statements, and bank statements to give lenders a clearer picture of your finances.

Buyers with non-traditional income sources may also need extra documentation during the mortgage process. For example, you may be asked to provide lease agreements for rental income, court orders for child support or alimony, or statements showing investment income, pension payments, or Social Security benefits.

These documents help lenders determine whether your income is stable and sufficient to support a mortgage.

3. Debt information

Lenders also want to know what debt you already carry. This helps them determine if you can make payments on existing debt and pay a mortgage.

They could request divorce decrees with evidence of spousal or child support that you owe, information on student loans or car loans, or bankruptcy paperwork.

4. Credit report

A credit report contains information on your debts, payment history, and collections. Credit bureaus use this information to generate a credit score, and the higher it is, the better. Lenders pull your credit report and score to assess your ability to repay a loan. You won’t see this document yourself unless you request a copy.

It’s better to do the homework upfront to find out what your closing costs are going to be.

![]()

![]()

![]()

![]()

![]()

5. Pre-approval letter

Up until now, you’ve just been getting the ball rolling with lenders to set your homebuying budget. Once they’ve verified your income and assets, debts, and credit score, the lender issues a pre-approval letter stating how much you can borrow. Because this letter sets your home shopping budget, most agents wait until you have the pre-approval letter in hand before they begin showing you houses.

Matt Laricy, a top real estate agent in Chicago, advises homebuyers to get pre-approved because often, buyers will change their home shopping budget once they have an idea of the loan’s total costs.

“It’s better to do the homework upfront to find out what your closing costs are going to be,” he suggests. He’s had buyers lower their budget from $500,000 to $400,000 once they saw the mortgage’s total costs, for example.

You might be thinking, “But I got prequalified online, and the lender didn’t ask for all this information!” That’s because while pre-approval and pre-qualification are sometimes used interchangeably, they aren’t typically the same thing.

When you get prequalified, lenders only request an estimated overview of your financial picture, including your credit score, income, debts, and assets. They’re taking what you input in the online form at face value, and they don’t generally verify it.

Because you can typically enter your ballpark information online and get a pre-qualification letter in just a few minutes, the pre-qualification could only give you a rough idea of how much home you can afford. With a pre-approval letter, however, your lender usually confirms at least some of your credit or financial information.

They could perform a soft pull of your credit or complete a full financial underwrite and verify your financials (with evidence like your W-2s and bank statements). Because the pre-approval actually verifies some information, a pre-approval letter carries more weight with sellers and their agents.

Note that any pre-approval letter is not considered a commitment to lend. There are several scenarios where your mortgage can fall through, even after receiving a fully underwritten pre-approval. For example, if you take on further debt during the lending process or quit your job, the lender can refuse to fund the loan. Nonetheless, a pre-approval letter a key document in your homebuying journey.

»Learn more: Pre-approval tells you what lenders might offer, but your comfort zone may look different. The Home Affordability Calculator helps you bridge that gap so you can plan your home search wisely.

6. Loan Estimate

This document is a form the lender sends within three business days of receiving your complete loan application. It’s a brief but complete financial picture of the applied-for loan.

Consider it a cheat sheet that shows you everything you’re committing to if you accept the loan terms, including your:

- Estimated interest rate

- Monthly mortgage payment

- Estimated tax and insurance costs

- Estimated closing costs

- Potential penalties (including prepayment penalties)

The Loan Estimate isn’t an indication of your loan status. At the time it’s sent out, the lender may not have made any decisions about approving or denying your application.

The three-page document is simply a snapshot of your proposed loan terms. It’s especially helpful if you’re submitting mortgage applications to multiple lenders or for multiple loan types, so that you can compare and contrast the loans before deciding which one fits best.

Documents during the home search and offer stage

Once you’ve sorted out mortgage matters, the focus shifts from preparing your finances to finding the right home and making an offer. During this phase, you’ll encounter documents related to your offer, negotiations, and the early steps of the purchase agreement.

7. Offer letter

If you’re in a seller’s market, your agent might have urged you to write an offer letter. This short “love letter” to the sellers explains why you want to buy the property. In competitive markets, personalizing your offer letter can sway sellers in your favor.

Ideally, this letter will include a bit of personal information about who you are and why you love the house. It’s your best attempt to make a personal connection with the seller.

“Keep it relatable and personable, but not obnoxious or pushy,” says Laricy. “Include basic things, a quick synopsis of who you are, and why the place is a perfect fit for you.”

Keep your eyes peeled during showings for any common interests you share with the seller to mention in your offer letter. Whether it’s because you’re both dog lovers or you adore their garden and promise to maintain it, find ways to connect.

Laricy recalls one of his clients getting the condo they were eyeing because they went to the same college as the sellers or were at the same stage in life that the sellers were when they bought.

An offer letter is also your opportunity to explain any finer details of your offer, such as why you’re requesting contingencies or why the seller should consider your less-than-asking-price offer.

8. Purchase agreement

This is the document that, when signed by both the buyer and the seller, formalizes the purchase and commits both parties to the contract terms.

The real estate contract spells out all of the financial nitty-gritty, including:

- Identification details for both buyer and seller

- Property description and condition

- Purchase price

- All contingencies and conditions

- Rights and obligations of both parties

- All items included in the sale, including appliances

- Earnest money deposit amount

- Closing costs (itemized according to who’s paying for what)

- Closing date

- Terms of possession (in other words, when you’ll get the keys to the place)

- Signatures of both buyer and seller

While you won’t actually have a hand in creating this document, it is the heart of your home sale. The purchase agreement is vital to keeping on top of your responsibilities. According to Laricy, filling it out correctly shows sellers that you and your agent are on top of the transaction and won’t be a problem.

9. Seller’s disclosures

These are documents where a home seller shares what they know about the property’s condition and history. This can include issues like past repairs, structural problems, water damage, pest infestations, or anything that could affect the home’s value or safety. They’re meant to provide transparency so you can make an informed decision before closing the deal.

However, note that seller’s disclosures aren’t required in every state. If a seller does provide them, read them carefully and review the details closely. Even then, it’s important to do your own due diligence and complete independent inspections rather than relying on disclosures alone.

10. Earnest money check

An earnest money check is a payment you make when you submit an offer on a home to show the seller you’re serious about buying it. It’s usually held in an escrow account and later applied toward your down payment or closing costs if the purchase goes through. If the deal falls through, whether you get it back depends on the terms of your contract.

If you have offered earnest money as part of the deal, you’ll have to get a cashier’s check (or order a wire transfer) to move it into the escrow account.

»Learn more: Not sure how much earnest money is enough to make your offer stand out? Use the Earnest Money Calculator to guide your strategy before you submit your bid.

Documents for underwriting and property review

After your offer is accepted, your lender takes a closer look at both your finances and the property you’re planning to buy. During this phase, you’ll need documents that support the underwriting process and help verify that the home meets the lender’s requirements for financing.

11. Home inspection report

The home inspection report is a detailed list of the condition of your new home, including, but not limited to the:

- Foundation: cracks, crumbling, or gaps

- Exterior: siding, gutters, downspouts, and grading

- Bathroom fixtures

- Appliances, if they’re included in the sale

- Roof: estimated age and condition

- Plumbing system

- HVAC systems

- Electrical and gas system

A home inspection contingency is one of the most frequent contingencies written into purchase agreements. Only 19% of buyers waived it in April 2026, down from 20% during the same period last year.

If the home inspector finds problems, you can negotiate with the seller to have them fixed, get a credit at closing, or back out of the purchase if the house needs too much work and you have an inspection contingency.

12. Home appraisal report

While the inspection report focuses on your future home’s condition, the home appraisal determines the property’s value in the current real estate market. The lender typically arranges for this because it’s important to your mortgage approval.

The house you’re buying serves as collateral for the loan. If you failed to make payments on the mortgage loan, the lender could seize possession of the house to recoup their losses. Because of this, the lender uses the appraisal to verify that the property is actually worth what you’ve agreed to pay.

The appraisal matters a lot to you as a buyer, too. “If it comes in less, the buyer will have to either walk away or come out of pocket,” explains Laricy. That’s because a bank won’t fund a mortgage loan above the home’s appraised value, so a low appraisal means that someone is going to have to compromise.

If the appraisal finds that the property is valued significantly less than your offer price, you have a few options. You can negotiate a lower price with the seller, pay the difference in cash, or walk away from the home. Laricy sees that “a lot of first-time or younger buyers don’t have the difference in funds,” and they typically have to walk away from the purchase.

13. Title review

The home’s title report is the document that lists information related to the legal right of ownership of the property.

Jen Staggs is a certified and licensed title professional in Indiana, with more than 22 years in the business. According to her, “The title search is to protect the buyers and the sellers, to make sure that there are no liens or judgments or anything against the property, and that it’s actually owned by the person who is selling the property.”

A title search sifts through public records to verify that the seller has the legal right to sell the property. It also checks for any pending legal issues with the property, such as unpaid property taxes, liens, or judgments against the seller that list the home as an asset.

Mortgage lenders require title reviews, and they secure their own title insurance on the home to protect their interests (as the buyer, you’ll likely pay for this policy). Even if you’re paying cash for the house, don’t bypass a title search, and consider purchasing your own title insurance. If it’s discovered that a foreclosure fifteen years ago wasn’t properly cleared off the title, you could be in hot water without insurance.

14. Property survey

A property survey determines the legal boundaries of the parcel of land you’re buying. It’s a good idea to have a survey performed so that you’ll have legal proof of exactly what you’re buying. It could also identify any encroachments, like a neighbor’s fence built a few feet over the property line.

“If they’re in an old community with a plat map from the 1800s, and the metes and bounds lines are a little cloudy, we recommend they get a property survey,” says Staggs.

This document is especially important if you’re purchasing property that may contain disputed assets, such as a road, a body of water, or a beach.

15. Homeowners insurance declaration page

Mortgage lenders won’t grant you a mortgage without proof of homeowners insurance. Why? Because until your mortgage is fully paid off, the bank has a stake in your home’s condition.

If you stop making payments on your loan, the home’s ownership reverts to the bank. The bank wants to know that its collateral is protected and insured at the proper valuation in case something happens to it before the loan is paid off. The lender won’t fund the mortgage until they’ve seen proof of insurance.

The homeowners insurance declaration page summarizes your homeowners’ insurance coverage and proves that you’ve obtained coverage.

16. Homeowners association (HOA) documents

These are the set of rules and records provided by a homeowners association for properties that fall under its jurisdiction. These typically include the HOA bylaws, financial statements, meeting minutes, and rules about property use, fees, and community standards.

As part of the documents needed to buy a home, they help you understand what living in the community will be like before you commit. You’ll also see details about monthly dues, special assessments, and any restrictions on things like renovations, rentals, or exterior changes.

It’s important to review these documents closely because the HOA can have a big impact on your costs and everyday life.

Documents for closing day

Closing day is the final step where all the paperwork comes together, and ownership of the home officially changes hands. During this phase, you’ll review and sign several important documents that finalize your mortgage, transfer the property, and complete the purchase.

17. Closing Disclosure

The Closing Disclosure is a form from your mortgage lender detailing the terms of the loan. It includes the same information in the Loan Estimate, but it has concrete figures rather than estimates:

- Interest rate

- Monthly mortgage payment

- Tax and insurance costs

- Closing costs

- Potential penalties (including prepayment penalties)

In most states, the Closing Disclosure should be in your hands at least three business days before closing on the house so you can review the terms of the mortgage.

This document is important when getting your cashier’s check for the down payment and closing costs, as it will also provide the exact amount you’ll need to cover with the check.

18. Promissory note

A promissory note, also called a mortgage note, is a legal document that outlines your promise to repay your home loan. It details key terms of your mortgage, including the loan amount, interest rate, payment schedule, and what happens if you miss payments. You’ll typically sign this document on closing day as part of the final paperwork needed to buy a home.

Unlike the mortgage itself, which secures the loan with the property, the promissory note is your personal commitment to repay the debt. Because it legally binds you to the loan terms, it’s important to read and understand it before signing.

19. Cashier’s check or wire transfer

“The main ‘document’ that the buyer needs to provide for the closing is a cashier’s check to the title company once they know what the final closing costs amount will be,” says O’Brien.

The title company requires a cashier’s check because it guarantees funds, unlike a personal check that you could write for any amount, whether or not you have the cash available in the bank. Without this piece of paper, the deal won’t close.

The check or wire transfer typically covers closing costs, prepaid interest, and property taxes. The title company will provide you with the official amount a few days before the closing, and you can either go to your bank and get a cashier’s check or arrange a wire transfer into an escrow account.

The check could include the down payment, depending on whether your lender has bundled your closing costs and down payment into “cash due at closing.” If not, you’ll have to provide another check for the down payment or follow your agent’s instructions for a wire transfer.

20. Government ID

Once it’s time to close the sale, you have to prove your identity. A driver’s license, passport, or other government-issued photo ID is required at closing to prove that you have the legal right to sign the closing documents and assume ownership of the house.

According to Staggs, bringing an expired or inaccurate driver’s license is the most common issue at closing. In one instance, a couple was married two weeks before they closed on the house.

“The wife hadn’t gone and changed her driver’s license,” Stags explains. “But the way she wanted to hold the title didn’t match what she was bringing to us. It was a bit of a debacle.” To solve the problem, the title company had to obtain a copy of the marriage license to add to the file.

Getting your docs in a row

Buying a home involves more than finding the right property. It also means staying on top of the paperwork that keeps the transaction moving forward. From financial records and loan documents to disclosures and closing forms, each document plays an important role in the process.

Knowing what to prepare ahead of time can help you avoid delays and feel more confident at every stage of your homebuying journey. While the paperwork may seem overwhelming at first, having the right guidance can make it much more manageable.

A knowledgeable real estate agent can help you understand what documents you need and when to have them ready. Connect with a local agent through HomeLight to get expert support and navigate the homebuying process with confidence.

Closing On a House? Here's a Checklist to Keep You Organized

Closing on a house can be overwhelming, especially if it’s your first time. Keep track of where you are in the process, what you still need to do, and how long it will take with our checklist.

FAQs about documents needed to buy a home

When applying for a mortgage, you typically need to provide documents such as proof of income (pay stubs, W-2 forms, tax returns), bank statements, employment verification, and a list of your assets and liabilities.

To complete the home purchase, you’ll need documents like a signed purchase agreement, a preapproval letter from your lender, a copy of the home inspection report, and proof of homeowners insurance. Additionally, you’ll need your identification (driver’s license or passport).

Yes, it’s essential to review the title and deed documents. The title search ensures the property has a clear title, free of liens or disputes. The deed is the legal document that transfers ownership, and you’ll want to ensure it’s accurate and reflects your purchase.

At the closing, you’ll typically sign documents, such as the closing disclosure, promissory note, deed of trust or mortgage, and various affidavits and disclosures. You’ll also receive the settlement statement, which outlines the financial details of the transaction.

Yes, there may be documents related to inspections and repairs. You might receive a home inspection report detailing any issues found during the inspection. If repairs were negotiated as part of the sale, there should be documentation of those agreements.

Header Image Source: (Cytonn Photography / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.