Your Dream Home Appraised Lower than Your Offer: Now What?

- Published on

- 15 min read

-

Dena Landon, Contributing AuthorClose

Dena Landon Contributing Author

Dena Landon, Contributing AuthorClose

Dena Landon Contributing AuthorDena Landon is a writer with over 10 years of experience and has had bylines appear in The Washington Post, Salon, Good Housekeeping and more. A homeowner and real estate investor herself, Dena's bought and sold four homes, worked in property management for other investors, and has written over 200 articles on real estate.

-

Taryn Tacher, Senior EditorClose

Taryn Tacher Senior Editor

Taryn Tacher is the senior editorial operations manager and senior editor for HomeLight's Resource Centers. With eight years of editorial and operations experience, she previously managed editorial operations at Contently and content partnerships at Conde Nast. Taryn holds a bachelor's from the University of Florida College of Journalism, and she's written for GQ, Teen Vogue, Glamour, Allure, and Variety.

When you get an appraisal lower than your offer price, it can go one of two ways: it gives you a chance to negotiate a lower price with the seller, or it can put the entire transaction at risk. Either way, you’ll need to figure out what the low appraisal means for your purchase and decide what your next move should be.

A low appraisal doesn’t automatically mean the deal is dead, but it can create challenges that both buyers and sellers will need to address. The good news is that low appraisals happen from time to time, and there are several ways a transaction can move forward. Here’s a closer look at the options you can take when faced with this dilemma.

Find an Agent To Help Make Sense of Your Home Appraisal

Working with a top agent can help you take the stress out of evaluating your low appraisal options.

What is an appraisal?

What exactly is an appraisal? Simply put, it’s a professional estimate of what the home is worth to make sure the purchase price lines up with its market value. As California real estate agent Ed Kaminsky explains, an appraisal is a “verification process” that confirms the market has done its job and that the home’s value is in line with what buyers are willing to pay.

If you’re getting a mortgage to buy a home, your lender will almost always require an appraisal from an independent third party. And since 74% of homebuyers financed their purchase with a mortgage in 2025, most buyers will go through the appraisal process at some point. That’s because lenders want to make sure the home is worth what you’re paying for it and that they’re not lending more money than the property is worth.

In other words, the appraisal helps protect the lender’s investment. They want to know that if the loan ever goes into default, the home’s value would be enough to help cover their losses.

How does an appraisal work?

If you’re curious about how an appraisal is calculated, it’s actually pretty simple, Kaminsky says. First, a licensed appraiser, usually hired by your lender, completes a thorough evaluation of your home, taking into account its location, condition, upgrades, and any other features. After that, they dig through the paperwork.

They look at comparables (or comps) in the area to see how your home compares. They’ll find at least three homes, Kaminsky says, that are similar in size, age, location, and condition to compare sale prices and evaluate market conditions. They might look at tax records and other real estate indicators as well.

Appraisers tend to “sandwich” the property, finding homes valued slightly above and slightly below to see how your home stacks up. Once their work is finished, they’ll complete a standard appraisal report and send it to both you and your lender with all relevant information.

What does “appraisal lower than offer” mean?

When an appraisal comes in lower than your offer, it means the lender’s valuation of the home is less than the price you agreed to pay. The difference between those two numbers is often called an “appraisal gap.” In simpler terms, it’s the space between what you offered and what the bank thinks the home is actually worth.

For lenders, this matters because it affects the loan-to-value (LTV) ratio, which compares how much you’re borrowing to what the home is worth. If the appraisal comes in low, that ratio goes up, and the lender may not approve the full loan amount. That can leave you needing to cover the difference or renegotiate the price.

Why appraisals sometimes come in low

Here are a few common reasons why lower appraisal happens:

- Homes listed too high or bidding wars: In competitive markets, buyers sometimes push prices above what the home would normally sell for.

- Fast-changing market conditions: Prices can move more quickly than appraisals can keep up.

- Not enough comps: If there aren’t many similar recent sales nearby, it’s harder to justify a higher value.

- Unique features or condition issues: One-of-a-kind homes or properties needing work can be harder to value.

- Appraiser differences or mistakes: Appraisals involve judgment, so different appraisers may see things differently or miss key details.

How common are low appraisals?

Not extremely common, Kaminsky says, but it does happen. Only around 1 in 10 homes appraise for less than the asking price. Moreover, only 6% of delayed contracts in April 2026 were because of appraisal issues.

However, fluctuations in market conditions can increase the appraisal gap. For example, in 2021, we were in the middle of a “hyper-appreciating market,” according to Kaminsky, which meant home prices were constantly increasing. And since appraisers look at past home sales, the comps might not have caught up to where the home prices were at the moment.

For example, if a home sells for $500,000 in a highly competitive market, the comps, usually taken from home sales in the last 90 days, might still show similar homes selling for closer to $450,000. That would cause the appraisal to come in lower than the purchase price, even though the market allows for higher home sales.

“Because you’re looking in the past and the appreciation could have taken place, it is possible that a home sells for more than it has ever sold for in a particular neighborhood,” Kaminsky says.

Now, what should you do if that happens? Let’s take a look at a few options.

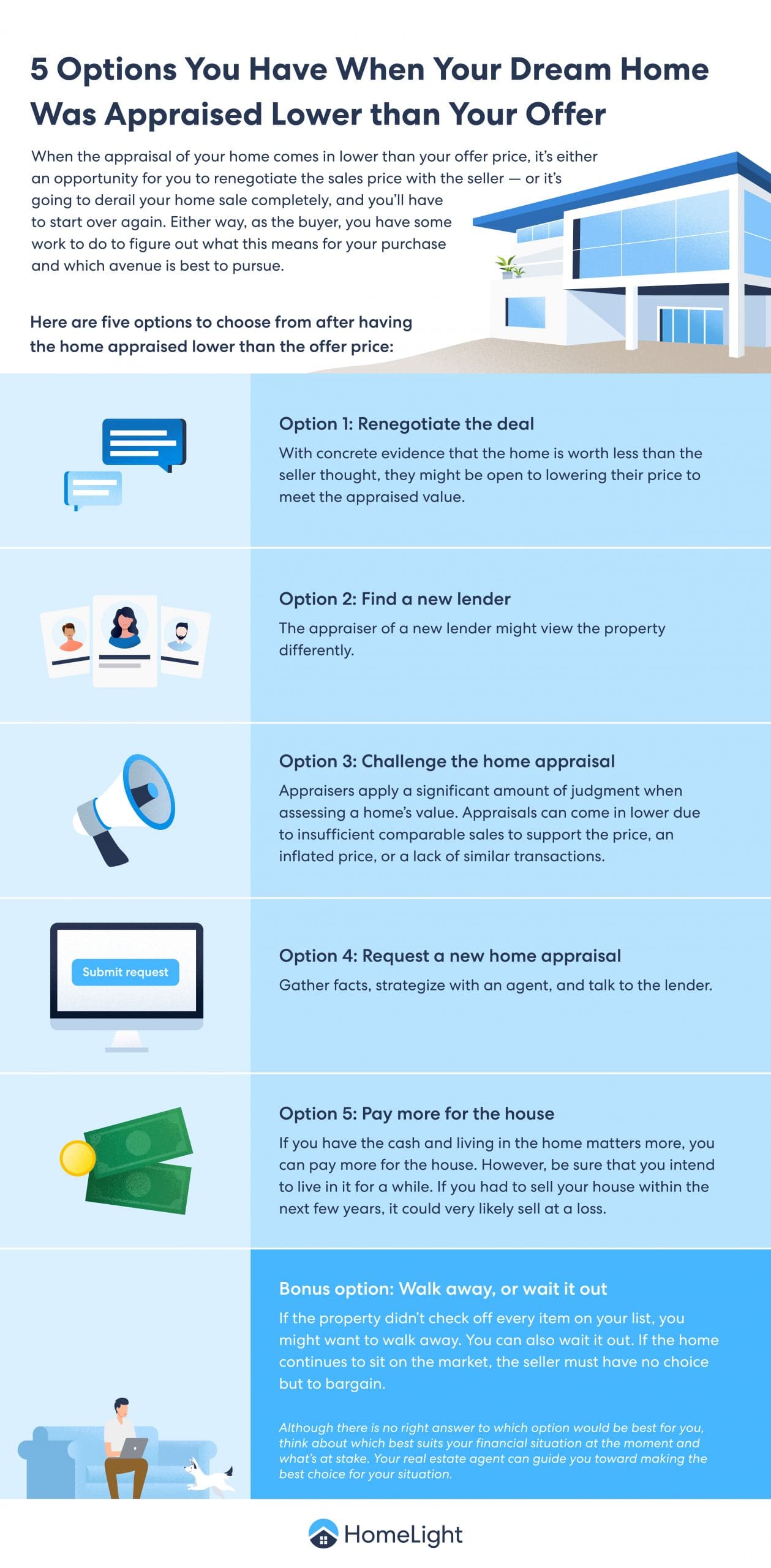

Option 1: Renegotiate the deal

Instead of viewing an appraisal lower than your offer as a deal killer, think of it as an opportunity to negotiate with the seller. With clear proof that the home is worth less than the offer price, the seller may be willing to drop the price to match the appraised value. And if they listed the home too high or had unrealistic expectations about the market, the appraisal can act as a reality check.

Sellers can choose not to lower the price and wait for another offer, but that can be a gamble. If one appraisal comes in low, there’s a strong chance the next buyer will run into the same financing issue. Once a home has already appraised below the list or offer price, it’s often a signal that it may not appraise higher the next time around. And if the market is slowing down or it’s late in the homebuying season, putting the home back on the market could mean sitting longer than expected.

If they are unwilling to budge on price, you can also renegotiate seller concessions. Offer to split the difference. If the home is under-appraised by $20,000, they could lower the price by $10,000, and you could put an additional $10,000 into the transaction.

Jesse Zagorksy, a top-performing San Diego, California agent with over two decades of experience, advises: “Have your buyer’s agent talk to the listing agent and find out what is truly important to the seller in addition to the price of the house. Are there any other terms that matter, such as the close of escrow date, furniture, and possessions, or offering free rent?”

For example, if the seller doesn’t want to move that huge entertainment console or hasn’t found a new place to live yet, sweeten the deal by offering to let them leave the console and make you responsible for its disposal, or to let them stay in the house rent-free for a month.

Explore an alternative type of financing: In some situations, you might be able to ask about seller financing. With seller financing (also called a “seller carryback”), you set up a private loan directly with the seller instead of going through a traditional lender. It’s not common, but it can work.

Zagorsky has seen it happen when a seller was retiring, downsizing, and had a lot of equity built up in the home. This can make sense if the seller already owns the home outright and likes the idea of getting steady monthly payments, kind of like a passive income stream.

Option 2: Find a new lender

If you moved fast and only got pre-approved through one lender, you may not have explored other options yet. When an appraisal comes in lower than expected, it can be worth getting a second opinion from a different lender. Another appraiser may evaluate the home differently, which could help change the outcome.

When multiple appraisers value the same home, Tom Cullen of Cullen Real Estate and Appraisal Company says that “invariably two appraisers will arrive at slightly different values due to comparable sale selection and subjective property characteristics, such as quality and condition.” Because banks use different appraisers and methods, another lender could land on a different price for the same home.

Consider looking for a different lender if:

- You have strong credit.

- You have access to other financing options.

- You think another lender will better understand the situation.

If you have excellent credit, it may be easier to get pre-approved with another bank. You’re under no obligation to inform the new lender that the home appraised low with another lender, and if you apply within 30 days of the last application, it won’t hurt your credit score. However, you may have to pay application and appraisal costs again.

Unfortunately, individuals with poorer credit have a harder time qualifying for a mortgage. If you struggled to get pre-approved, you may have fewer financing options and less flexibility in the upper limit of your price range.

If you switch lenders, you will get a new appraiser. But switching lenders will cost you time and money, so be sure that you truly want this specific home before applying elsewhere.

Option 3: Challenge the home appraisal

An appraisal is not automatically final, and in some cases, it can be reviewed again. This usually involves pointing out issues or missing details that may have affected the value. While it won’t always change the outcome, it can sometimes lead to a revised appraisal that better reflects the home’s worth.

Throughout his 30-year career as a home appraiser, Cullen has seen borrowers in this situation request a re-examination by the original appraiser. According to him, “Often, the borrower will supply comparable sales that they feel might be beneficial to their cause and sometimes clarification of salient facts about their property that the appraiser might have overlooked.”

Appraisals can come in lower due to insufficient comparable sales to support the price, an inflated price, or a lack of similar transactions. An appraisal is “a defensible document that needs to show supporting data,” says Cullen, so if you give the appraiser data to defend a higher price, you might be successful in challenging the original appraisal.

Option 4: Request a new home appraisal

To get a new home appraisal, gather your facts, strategize with your agent, and talk to your lender. They will ask you to complete a “Reconsideration of Value” form, which lets you:

- Point out what seems off in the appraisal, like missing details or anything that doesn’t look accurate.

- Share up to five other recent home sales you think are better comparisons.

- Explain why those homes are better matches, like location, size, condition, or features.

If you are using FHA or VA financing, the appraisal doesn’t expire for 90 days. You might not be able to get a new appraisal right away, though this could work in your favor. Comp data could have time to catch up with your offer.

“Because appraisals are based on historical data, they often lag the market, especially when prices are going up,” Zagorsky explains, so waiting a few months to have the property re-appraised could result in a different appraisal.

The lender doesn’t have to honor your request, though. If they do decide to allow another appraisal, they will likely require you to pay a second appraisal fee.

Option 5: Pay more for the house

If you have more money that you can put into the purchase, you can pay more for the property than its appraised value. This isn’t against the law, and there are many reasons why you might value a property more highly than a bank does.

Cullen thinks that “living next door or in close proximity to family or work, sentimental reasons, or the necessity of obtaining a property quickly” are all reasons that you might be willing to pay more than market value for a house.

Ultimately, if you have the cash and living in the home matters more to you than what you pay for it, this is always an option. Before you decide to pay more than what the house is actually worth, make sure you’re planning to stay there for a while.

Remember, you’re going in knowing you paid above market value. Even if you’re not “underwater” right now, which means you owe more on your mortgage than the home is worth, you’re taking on some risk. If prices don’t rise the way you expect, you could end up in that situation. And if you had to sell within the next few years, there’s a good chance you might have to take a loss.

»Learn more: When an appraisal comes in lower than your offer, it can force you to rethink what you can comfortably afford or adjust to make the deal work. Use the Home Affordability Calculator to see how different scenarios could impact your budget and help you decide your next move with confidence.

Bonus option: Walk away or wait it out

Depending on how much you love the home, walking away could be your last option or your first. Most real estate contracts have clauses that let you back out, and not being able to secure financing is often one of them.

Challenging the appraisal or trying to negotiate with the seller can also take time, and there’s no guarantee it’ll work out. While you’re waiting, you could miss out on another home that fits your needs and appraises at your offer price. If the property wasn’t a perfect match to begin with, it might make more sense to walk away.

If one of Zagorsky’s clients decides to walk away, but still loves the house, “we always keep an eye on that property and keep in touch because you never know when something might change on the seller side, and they might become more flexible.”

If the home sits on the market, or other buyers also can’t get it to appraise at the offer value, the seller must sell eventually. They’ll have no choice but to bargain.

Find a top real estate agent near you

We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs. It takes just two minutes to match you with the best real estate agents, who will contact you and guide you through the process.

So, which option is best for me?

The simple answer: it depends. Every sale and every buyer is different, so there’s no one-size-fits-all rule here. That said, Kaminsky points out that the first thing you should look at is your own financial situation.

Think about which of the above options best suits your financial situation at the moment and what’s at stake. Can you stretch your down payment to get your dream home? Would dipping into your savings put you in a tough spot? And if the deal falls through, what does that look like for you financially?

Next, it’s fair to ask yourself and your real estate agent, “Am I overpaying for the property?” If so, you may consider renegotiating or getting a second opinion. If not, consider if it’s possible that there is hyper-appreciation in the market and what that means for the sale.

Kaminsky says in the case of hyper-appreciation, it might be wiser to grab the home while you can. After all, in a highly competitive seller’s market, there’s no guarantee the next home that goes up for sale isn’t thousands of dollars more, and, suddenly, you’re in a worse situation.

“You have to consider, ‘where is the market going?’ and ‘what is the buyer’s financial capabilities?’ to decide which option is best,” Kaminsky says.

When you first hear that your potential new home didn’t appraise, don’t panic. Yes, it’s stressful, but your agent can guide you toward making the best choice for your situation. If you can do that, you should be on your way to your dream home, no matter what the appraisal says.

Find an experienced agent today who can help you navigate every step of the process and advocate for you when challenges come up.

Frequently asked questions (FAQs) about low appraisals

Most of the time, the buyer is expected to cover the difference. That can mean bringing extra cash to closing or adjusting the loan amount if possible. Sometimes the seller can also lower the price. It all depends on the buyer-seller negotiations.

Yes, the seller can absolutely say no to lowering the price. If that happens, the buyer has to decide whether to cover the gap or walk away. It often turns into a negotiation point between both sides.

It’s a part of your offer that protects you if the home doesn’t appraise for the price you agreed to pay. If the appraisal comes in low, it gives you the option to renegotiate or walk away from the deal.

You can waive it, but it comes with risk since you’d be responsible for covering any gap between the appraisal and the purchase price. Some buyers do this to make their offer more competitive in hot markets. Make sure you’re financially comfortable before going that route.

Add an appraisal contingency to your offer. This gives you a way out or room to renegotiate if the appraisal comes in low. Before making an offer, do your homework on market value first. Don’t rely only on the seller’s price. Instead, look at recent sales so you know what the home is really worth.

But if you’re really determined to secure the property, think about an appraisal gap clause, especially when you’re in a competitive market. This means you’re willing to cover a certain amount if the appraisal falls short, making your offer more appealing.

Header Image Source: (fran hogan/ Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.