Is It Worth Relocating for a Job? How to Weigh All the Relevant Factors

- Published on

- 10 min read

-

Christine Bartsch Contributing AuthorClose

Christine Bartsch Contributing Author

Christine Bartsch Contributing AuthorClose

Christine Bartsch Contributing AuthorFormer art and design instructor Christine Bartsch holds an MFA in creative writing from Spalding University. Launching her writing career in 2007, Christine has crafted interior design content for companies including USA Today and Houzz.

Since the 1980s the rate of people who seek jobs and ultimately choose to relocate for one has dropped from 40% to 10%. The job market is tight, and you can work from virtually anywhere thanks to the internet. So the desire or need to uproot for employment just isn’t what it used to be.

That doesn’t mean you shouldn’t do it, but there’s good reason to set the bar for “is it worth relocating for a job” high, especially when you have a house in the mix. The job itself and your stage of life should check a lot of boxes across different areas:

- Your current housing and financial situation

- Salary and cost of living considerations

- Your new employer’s relocation package

- How your family feels about it

- Your personal career goals

- Quality of life and local attractions

Let’s cover all these bases so you can better sort through this difficult decision.

Homeownership and your level of mobility right now

Gone are the days of apartment hopping from one lease to another… when you could up and go live like a nomad if you so well pleased for the cost of an awkward phone call to your landlord and a few thousand dollars to break your rental contract.

Owning a house makes relocating for a job a lot more complex.

Here are the factors you need to weigh in order to figure out if you can swing it:

1. How much equity have you built up and how long have you owned the house?

The beauty of owning a house is that in theory it should only go up in value over time, and even if you’ve lived there a short while, you should be able to sell it for at least what you paid for if not more. But you likely bought a house thinking you’d settle down for awhile and build up some equity.

The longer you’ve owned the house, the more home equity (the value of the house minus what you owe) you should walk away with. Every dollar you paid toward your principal balance is equity that could go toward a bigger, better house in your new hometown.

At minimum, you want to sell your house at a point when the price will cover what you owe plus any seller closing costs, which can range from 7%-12% of the sale price. If the sale price of your home leaves you short of the necessary funds, then relocating for a job could put you in a position where you have to come up with the extra money or potentially rent out the house from afar until it makes sense to sell it.

You also want to consider the tax implications of selling your house at this moment in time. The federal government allows homeowners to exclude up to $250,000 of capital gains on the sale of their primary residence.

However, to qualify for the gain, you’ll need to have lived in the house for at least 2 of the past 5 years. If you’re relocating for a job shortly after moving in or after you’ve rented out the house to a tenant, you could lose out on this exemption and have to pay taxes on your home sale profit.

And as far as writing off what it cost you to get you (and everything you own) into your new home, you’ll be footing the bill- unless you’re active military. This is thanks to the 2017 tax reforms that limited the long-standing job relocation exemption, according to the IRS Armed Forces’ Tax Guide.

The bottom line is—if you’ve owned your house for a while, you’re likely in a better position to sell it and relocate as opposed to if you just bought it.

2. How do home prices in the new city compare to your current neighborhood?

When you’re moving within the same city, home prices will be somewhat comparable from one location to the next in the sense that when you’re ready to move out of your starter house, your built-up equity helps you afford a bigger and better home.

However, this isn’t always true when you relocate. Homes with a similar lot size, square footage, and number of rooms could be significantly cheaper or more expensive depending on their location.

For example, the median home price for Las Vegas is $266,000, but move less than 300 miles away to Los Angeles, and the median price you’ll pay for a house is $634,000.

Higher home prices doesn’t immediately have to kill your relocating dreams, though—especially if you’re willing to commute.

“People who are willing to commute to work, can find some really affordable housing within an hour or two of major cities. And those suburban homes will be three or four times better in size and amenities than those closer to their workplace,” explains Dustin Parker, a real estate agent with relocation experience who ranks in the top 1% of agents in the Seaford, Delaware area.

“We have people who move to Delaware from Washington, D.C., and find they can get a $400,000 house that would’ve cost them well into the millions in D.C.”

3. How far will your salary go toward housing in the new location?

Even if it’s your dream job, relocating for work may not be the smart move if buying a home in the new location will put you in the hole financially for the foreseeable future.

On the flip side, an offer with a so-so salary may actually put more money in your pocket if the new locale is less expensive.

Let’s say your current job pays you $85,000 annually in D.C., putting you at around $5,200 a month after taxes. You’re paying about $2,000 of that a month toward the mortgage on your $400,000 home—leaving you around $3,000 monthly.

Now you’ve got a job offer in Delaware, but the salary offered is only $65,000 annually, putting you at just over $4,000 a month after taxes.

Some might automatically answer “thanks, but no thanks” to a $20,000 salary cut, but not so fast. Delaware’s median home price is $237,000, which puts you at a $1,100 monthly mortgage payment with a 20% down payment.

Do the math, and you’ve still got around $3,000 left each month after paying your mortgage. Plus, you’ll have all that equity from selling your $400,000 which means you’ll be able to make a larger down payment.

If the sale of your $400,000 home nets you $85,000 after the principal balance, closing costs and all other expenses are paid, that gives you a 36% down payment for the new $237,000 house—which will drop your mortgage payment down to $965.

Cost of living and taxes

Calculating whether or not it pays to relocate depends a lot on the area that you’re moving from and moving to—because the cost of living can vary greatly from state to state, as can how much you’ll pay in taxes across the board.

Property taxes

A 2019 analysis by WalletHub shows that average annual property tax payments range from $525 in Hawaii (which claims the lowest average real estate tax rate) to $4,725 in New Jersey (the state with the highest average real estate tax rate).

“We get a lot of people relocating from places like New York or New Jersey where the cost of living and taxes are significantly higher,” advises Parker.

“They’re not going to earn the same amount of money as they used to, but in Delaware, our property taxes are typically only 25% of those in Jersey or New York. So relocators usually get a little bit more bang for their buck.”

Residents in neighboring cities may also pay different tax rates depending on factors like local parks and schools. As you look into the possibility of relocation, do some digging into what kind of property taxes you’d pay based on where you’d like to move.

Sales tax

Sales tax is the tax you pay on various goods and services from the candle you buy at the mall to the burger you eat at the food court. Rates vary by state and local jurisdictions (check out this evolving list of state sales tax rates, including the range of local rates).

As of Jan. 2019, the top 5 states with the highest sales tax rates include:

- California (7.25%)

- Indiana (7%)

- Mississippi (7%)

- Rhode Island (7%)

- Tennessee (7%)

By contrast, some states such as Oregon and Delaware have no sales tax.

How does a tax on the everyday stuff you pay for impact your finances in the long term, and whether you decide to relocate for a job?

Let’s take an example:

You order the exact same thing at your local chain restaurant in Chandler, Arizona each time you visit. You know the total by heart. The $9.99 cost of the meal totals out to $10.77 every single time, including taxes. Then one day you grab your favorite meal at a location across town in Phoenix, AZ and the bill rings up at $10.85.

No, they didn’t raise their prices by a random $.08—Phoenix, AZ simply has a higher sales tax. You’re paying 7.8% in Chandler, but in Phoenix they’re paying 8.6%.

That $.08 difference doesn’t sound like much—after all, you’d just be spending an extra $4 a year if you got your favorite meal once a week at that higher rate.

But multiply that $.08 on every dollar you spend every month. Say you spend $1,500 of your monthly salary on food, gas, etc.. That .8% difference in sales tax (between the 7.8% rate and the 8.6% rate) will cost you an extra $12 a month and $144 annually.

That $144 isn’t enough to make you turn down an offer to relocate. But let’s say you’re living in Phoenix paying an extra 8.6% on all products and services subject to sales tax.

Now you’ve got a job offer in Oregon where they have 0% sales tax. In Phoenix, you’re paying $1,550 annually on your purchases if you spend only $1,500 a month or $18,000 a year.

In Oregon you’ll be paying $0.

A savings of $1,550 adds up over time. In five years, you’ll have an extra $7,750.

Now sales tax may not be enough to determine whether or not to relocate, but it can help you decide which area of town to live in. (So, if you’re moving to Phoenix, you might consider living in its Chandler suburb for its lower sales tax rate).

Other taxes

Property and sales have long-term implications for your relocation budgeting, but there are a handful of taxes that can significantly alter your short-term expenses.

A handful of higher-tax states are seeing residents flee to lower-tax states—to combat this, they’ve imposed what’s known as an exit tax.

“Every state has different rules and regulations regarding relocating out of state. Some have what they call an exit tax, so if you relocate out of state, they will charge you a tax to do so,” advises Parker.

Just ask high-earning residents of New York who try to move, only to have the state’s Department of Taxation and Finance tracking their financials and issuing subpoenas. They’ll do everything within their power to verify that you’ve actually relocated, and when—so that they can collect every tax dollar they can get.

Some states like New Jersey claim it isn’t really an exit tax—but whatever you call it, you’ll have a hefty tax bill if you move out of some states, even if you can eventually get some of it back.

General cost of living

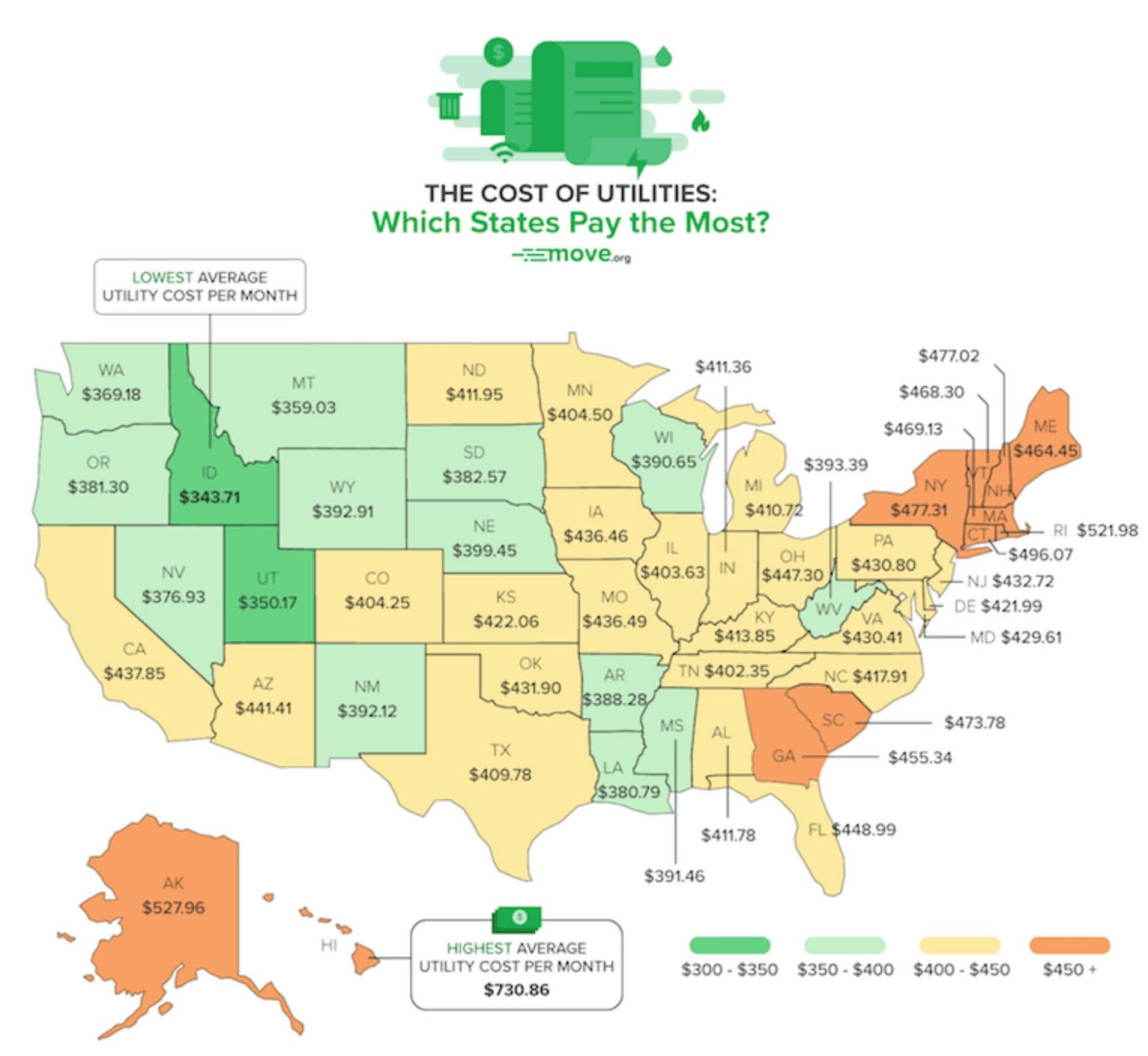

Calculating both long and short-term relocation costs isn’t all about taxes. There’s also lots of other cost of living expenses to consider, like the cost of food, gas, utilities, and anything else you currently spend your money on.

For example, if you move from Minnesota to Colorado, you’ll be paying about $400 a month for utilities in both states. But move to Rhode Island from either state, and you can expect to pay $530 a month for utilities—that’s an extra $120 a month, or $1,440 a year.

Food prices differ across the country, too. Take milk for example: you’ll pay an average of $2.59 a gallon in Phoenix, AZ, but as low as $1.85 in Louisville, KY and as high as $4 in Minneapolis, MN, Kansas City, MO, and Chicago, IL.

Costs vary on all sorts of products and services from state to state, from everyday items, like gas pump prices, to major monthly expenses, like health insurance premiums.

The Bureau of Labor Statistics tracks national cost of living expenses with their consumer price index, which averages the prices for a similar basket of goods, like food, gas, and healthcare, in regions across the country.

You can access this data through their website—and the data might surprise you.

For instance, you’d think that both San Francisco area and the New York City area were both equally expensive places to live. In June 2008, you would’ve been right—as both hovered around a 4% CPI. However, in April 2019, San Fran is up around 4%, while the NYC area is down to 1.6%.

There are even easier ways to get a quick snapshot of the cost of living between where you are and where you’re headed. You can check out both state’s rankings on state-by-state cost of living lists, or simply pop your data into a cost of living calculator.

Online resources can’t paint you a perfect picture of your existing and projected cost of living expenses, because they can’t factor in your unique variables. Your employer may offer to cover a percentage of your healthcare costs, provide a housing subsidy, or provide other salary package perks, like tuition reimbursement or even a wardrobe allowance.

Relocation package

Long-term perks work to offset any cost of living differences, and some employers may help out with the short-term costs, too. It’s not easy to afford the costs that come with selling one house, buying another, and moving across the country, all in one shot—and the strength of your employer’s relocation package could make a big difference in whether you decide to take the plunge or stay put.

“Don’t be afraid to ask for housing related assistance as part of your relocation package from your new employer. Those things are negotiable and the worst that they can do is say no,” says Parker.

Here’s just a taste of what companies may be willing to offer as relocation enticements:

1. Get moving, travel, temporary accommodation expenses covered

Most employers hiring out of state expect to pay at least a portion of their new employee’s moving expenses. How much you’ll get often depends on years of experience and uniqueness of skills.

If you’re fresh out of college, you might get a minimal lump sum just to help you get started, whereas someone with in-demand cloud computing or artificial intelligence experience, may be able to negotiate significantly more.

“You can ask for airline tickets to help you travel back and forth while you’re working to sell your former house. Or they may agree to pay for your hotel while you’re house hunting in your new neighborhood,” says Parker.

Your new employer may reimburse you for airline tickets, full service movers, and even temporary housing if you’re waiting for your former house to sell before buying a place in your new home city.

2. Accept a relocation mortgage

If your employer is feeling super generous, they may even offer to help you out with your mortgage.

Known as a relocation mortgage (relo mortgage), this loan type allows your employer to make financial contributions to the deal. This contribution can be made toward covering closing costs, or even used to reduce the interest rate for the life of the loan.

The company’s financial investment combined with your own down payment contribution lowers the lender’s risk and increases confidence, which often leads to a faster and less-expensive loan.

It doesn’t hurt to ask your new employer to help you out with a relocation mortgage, but don’t count on getting a yes—unless your job title comes with an impressive abbreviation like VP or CEO. These high dollar perks are often reserved for high-level hires.

3. Alternate home selling (and buying) help

Luckily, a relo mortgage isn’t the only option employers have to help offset housing expenses for their homeowner hires.

Some employers help cover housing-related expenses. All incurred costs, from closing costs, inspections, transfer fees, to the real estate agent’s commission, could be covered by your new employer through a direct reimbursement.

Others have set up guarantee-against-loss programs to protect new hires from the expense of carrying two mortgages if it takes a while for their former home to sell.

These programs offer relocating employees the option of having the company assume the mortgage for their former home until it sells. They may even provide the down payment amount for a new home purchase on a short term basis—which will be paid back when the previous home sells.

Another option some companies offer relocating employees is a home purchase plan. In this scenario, if your previous house doesn’t sell within 30 or 60 days, your employer—or the relo company hired to help you relocate—will purchase the home at the agreed-upon appraised value.

This practice is common enough that home buying experts recommend that buyers look into purchasing homes from relo companies.

There is one housing help offer you may want to steer clear of—and that’s letting your new employer pay for your real estate agent directly.

“I would be a bit leery of accepting the services of a real estate agent as part of a relocation package,” advises Parker.

“Most often, they’ll want you to work with a specific agent or company—which could lead to you receiving poor service or overpaying for a house, because the agent is working for your employer, not you.”

Family happiness

Last but not least, are all the intangibles that can’t be measured with facts and figures.

It’s not easy to determine if moving will make you happier or lead to regrets down the line. Multiply those emotions by the number of family members relocating with you, and the thought of moving becomes overwhelming.

What’s right for your partner and kids, depending on their stage of life

Let’s say your spouse is always up for an adventure, and your youngest is already packing—but your eldest is sobbing at the thought of leaving friends behind, and your middle kid won’t go until you finish that treehouse you promised to build together.

How do you quantify these types of intangibles? It may be as simple as drawing up a pros-and-cons list.

Set aside the hard financial data, ask every family member to create their own list of positives and negatives, then come together to compile them into one family assessment on whether or not relocating is right for the whole family.

Your kids’ lists may be heavily biased in whichever direction their emotions lean, so they can’t call the shots. But this activity gives them a voice and will go a long way toward persuading them into giving the new locale a chance if you do relocate.

There’s a whole host of questions you can ask yourself (and your family) to help you get your pro/con lists started:

- Will our new jobs/schools be better than our current ones?

- Will we be living closer to family or old friends who’ve moved?

- Will we like the location and the weather better?

- Will we be able to live the same or better lifestyle than we are now?

- Will we be closer to favorite vacation destinations?

Many of these surface questions will require a deeper exploration to get to the real answers of whether or not relocating will make you happier.

Change in housing situation and lifestyle

Let’s say you’ve got three kids, but you can only afford a two-bedroom house in your current city. Relocating to a less-expensive city might open up the possibility of affording a four-bedroom, giving each child their very own room.

On the other hand, maybe you currently live in a spacious, suburban house on a cozy cul-de-sac where your kids can safely ride their bikes along the no-traffic roads.

If that’s the case, relocating to an urban area like New York City may be hard on the whole family. It won’t be easy if your kids need to adjust to sharing bedrooms, and can only play outside with adult supervision in a park that’s several blocks away.

You also have to consider the change in climate. For families used to relaxing barefoot in the grassy backyard of a Midwest house, moving to a desert state where the lawns aren’t quite so lush can be quite a challenge.

Quality of life and local attractions

When work is the reason you’re considering relocating, it’s easy to forget: you won’t be working the whole time.

A week has a total of 168 hours to fill. You’ll only be on the job 40 to 50 hours a week on average, and you’ll spend another 50-60 hours sleeping. That leaves you with an extra 58-78 hours of free time to fill.

Looking at it another way, and you’ll be spending over one-third of your time awake and with no job or school to keep you all occupied. So, how will you fill your time?

Let’s say you live in Orlando and your family spends at least one weekend a month putting their annual theme park passes to good use. It may be difficult to relocate to Arizona, where you’ll only find a handful of handful of tame coasters and rides at smaller entertainment venues.

It’s not just the big attractions you need to consider. If your spouse is an avid mountain climber, a move to flat state could be jarring.

And maybe your kids are working towards earning a black belt or achieving unparalleled pointe techniques in their advanced ballet class. Then you’d better make sure that new home has a selection of dojos and dance schools to meet their needs.

Personal and career goals

One of the biggest ways companies entice new employees to completely relocate is with financial incentives in their salary and relocation packages. And it’s easy to get fooled by all those dollar signs.

However, more money will only make you happy in the short term. If you make a lateral move into a position that offers you no new challenges, and leaves you with the same, dreary work that led you to leave your old job—such a move could send you back to square one.

Even if the money, bonuses, and other company perks are amazing, you need to ask yourself if the new job will satisfy you in other ways, too:

- Is the new position a step up?

- Does the new position offer more interesting work?

- Will the new position teach me new skills?

- Does accepting the offer fulfill my career goals?

- Will the position help me transition into the career track I really want?

Relocating for a job, when you’re also a homeowner

Making the relocation decision when you’re a homeowner only complicates an already complex dilemma.

No matter how much you love your house, you can’t take it with you. And there’s no way to guarantee that you and your family can achieve a similar or better level of joy and satisfaction in the proposed new location.

However, you can get a good idea of what life will be like somewhere new. Crunch the numbers, analyze all the data you can get your hands on, and carefully consider the social, emotional, personal, and professional impact the move will have on you and your family.

Finally, hire a top local real estate agent (or two) on both sides of the equation. The best agents are local experts and will have helped many individuals and families navigate the challenges of a move to a new city.

In fact, HomeLight’s agent matching service will connect you with a professional who can sell your current house fast if that’s what you need. We’ll also help you find someone who’s done lots of transactions in your area of interest in your new city.

Ultimately, a top local agent will ben one of your best resources, there to answer your questions on everything from property taxes to the quality of the local coffee shops. In a situation as stressful as relocating for a new job, don’t be afraid to ask for a little help from the experts.

Header Image Source: (Austin Neill/ Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.