Selling a House for a Job Relocation: Tips, Tools, and Taxes

- Published on

- 15 min read

-

Valerie Kalfrin, Contributing AuthorClose

Valerie Kalfrin Contributing Author

Valerie Kalfrin, Contributing AuthorClose

Valerie Kalfrin Contributing AuthorValerie Kalfrin is a multiple award-winning journalist, film and fiction fan, and creative storyteller with a knack for detailed, engaging stories.

-

Sam Dadofalza, Associate EditorClose

Sam Dadofalza Associate Editor

Sam Dadofalza is an associate editor at HomeLight, where she crafts insightful stories to guide homebuyers and sellers through the intricacies of real estate transactions. She has previously contributed to digital marketing firms and online business publications, honing her skills in creating engaging and informative content.

Packing up your belongings and starting a new life in a different state, coast, or overseas to pursue an excellent job opportunity is no easy task, but it’s also incredibly common. Many professionals find that relocating for work can open doors to career growth, new experiences, and a fresh perspective on life. But when you own your current home, having to sell house for a job relocation adds a huge to-do to your moving checklist.

This guide will help you prepare for the move and anticipate what to expect from the process. We’ll cover corporate packages and relocation assistance, options for selling your house for a job relocation, and common tax questions like whether you’ll pay capital gains when you move for a job.

Stressed About a Quick Job Move?

It’s difficult to sell a house, especially under the pressure of a job relocation. Simple Sale provides cash offers for homes nationwide for when a traditional listing doesn’t work. No staging, no repeated showings, no agent commissions. Receive a cash offer within a week. Close in as little as 7 days.

You focus on your new job, we’ll help with the house!

Questions to ask as you prepare for the move

In preparing to relocate for a job, run through these questions to make sure you have your main bases covered.

First, what’s your home worth?

Relocating for a job can mean moving sooner than intended. If you purchased the home recently, such as a year or two ago, you probably haven’t built up much equity yet. Home equity is a homeowner’s financial stake in their property that they own free of their mortgage loan obligation.

When you sell, ensure that your home’s value will cover your outstanding mortgage balance in addition to selling fees and costs amounting to around 6% to 10% of the home’s sale price. Otherwise, you may need to pay money at closing to settle up.

To get an idea of your financial situation and an estimate of home equity, consider plugging your address into a free online tool such as HomeLight’s Home Value Estimator.

Our tool aggregates publicly available data, such as tax records, recent sales records for nearby properties, and your home’s last sale price, to offer a preliminary estimate of your home’s value in under two minutes.

Although it’s not a substitute for a home appraisal or an agent’s comparative market analysis (CMA), it can be a helpful starting point in determining how much equity you have.

From there, you can input your estimated home value into our Net Proceeds Calculator to calculate the cost of selling your home and the proceeds you could earn from the sale.

We always recommend following up on an online price estimate with the opinion of a top local real estate agent. If you need assistance finding an agent, HomeLight would be happy to connect you with a few highly qualified candidates in your area.

What’s included in your relocation package?

While your home’s value plays a role in your asking price, so might your moving expenses. According to Angi, the average cost of moving cross-country is approximately $4,600, with prices varying between $2,400 and $6,900. The total cost depends on factors such as the size of the home and the distance traveled.

The median distance between a recently purchased home and the buyer’s previous home was 20 miles. Factoring in how far you plan to move can help you better estimate the costs tied to your transition.

Beyond hiring professional movers, moving can incur other expenses, such as packing supplies, insurance, cleaning services, and storage. However, an employer’s relocation package might ease some costs.

According to Remote, a human resources platform, the average relocation package ranges from $2,000 to $20,000 or more, depending on an employee’s role and company budget.

Some packages include:

- Moving expenses: Covers professional movers, packing services, and transportation of household goods

- Temporary housing: Provides short-term accommodations while the employee finds a permanent home

- Travel costs: Includes airfare, mileage reimbursement, or rental car for the employee and sometimes their family

- Home sale or purchase assistance: Offers help with selling a current home or buying a new one, covering all or a portion of the closing costs or real estate agent commissions

Miscellaneous allowance: Covers incidental costs like utility hookups, driver’s license updates, or meals during travel

Depending on where you’re moving, you could receive even more to offset these costs. A handful of states offer financial relocation incentives to attract new residents. For instance, a program called Ascend West Virginia will pay you up to $12,000 to move to the Mountain State, providing perks like free coworking space and access to free outdoor recreation, including gear rentals.

Will you pay capital gains if you move for a job?

So long as certain requirements are met, homeowners can generally avoid paying capital gains on up to $250,000 — or $500,000 when married and filing jointly — of profit when selling their home. Those requirements include:

- Ownership: You owned the property for at least two of the last five years.

- Use: You lived in the property for at least two of the last five years.

- Look-back: You did not exclude the gain from the sale of another house within two years of the sale of this house.

However, let’s say you don’t meet the eligibility test because this job opportunity came up shortly after purchasing your current home. You may still qualify for a partial exclusion of paying capital gain taxes for a work-related move if you meet any of these conditions:

- Your new work site is at least 50 miles farther from your current home than your previous work location.

- You had no previous work site and began a new job at least 50 miles from your home.

- Either of the above is true of your spouse or the home’s co-owner.

The IRS has a worksheet to determine your exclusion based on your time in the home or your length of homeownership, and a resource with guidance for work-related moves. Talk with a tax professional to determine the details of your particular situation.

Can I deduct work-related moving expenses?

Moving expenses related to a job relocation are not tax-deductible unless you are an active member of the Armed Forces permanently relocating due to a military order.

If you’re thinking, “Wait, I thought any job relocation qualified for this.” Your memory serves you correctly. You used to be able to deduct moving expenses if your new home was at least 50 miles closer to your new job than your old home was (the distance test) and you’d been working that job full-time for 39 weeks within the first year after you moved (the time test).

However, the Tax Cuts and Jobs Act of January 2018 excluded all but active military from the opportunity to claim this deduction. So, unless you’re military, do not budget using this tax break.

How’s the real estate market?

Your timeline for starting your new job and the housing market conditions will determine how long it will take to sell your house or if you’re better off renting it out for a bit. (More on that below.)

If the demand for housing outpaces supply, you can breathe a little easier, knowing that your home likely won’t sit on the market for long. A tight market can also mean that eager buyers can find themselves in a bidding war, raising the offers you’ll get on your home.

Of course, if you’re also looking to buy a new home in your new location where the market is similarly hot, you might find yourself on the other side of the coin. When it’s a buyer’s market, you’ll likely find plenty of options in your new area at good prices, but your old home may take longer to sell.

What’s your plan for housing once you sell?

When selling a house for a job relocation, you must also plot where you’ll live next.

Some homeowners become so frazzled that they focus solely on the home sale and wind up with their homes under contract without knowing whether they will buy or rent in their new location, says Jessica Arledge, a top real estate agent in Savannah, Georgia, who sells 76% more single-family homes than the average agent there.

“You don’t want to find yourself homeless,” she reminds home sellers. “You also want to give yourself a reasonable amount of time to get out of the house.”

Have a realistic conversation with your real estate agent about the best way to handle the changeover. You might consider a sale-leaseback agreement for a few weeks, she suggests.

Also known as a seller rent-back agreement or a holdover, this allows you to stay in your home for a designated period of time after you sell. Essentially, it makes the buyer your landlord, so you have time to rent or buy a new home and arrange for the movers to collect your belongings.

Anne Sena, a real estate agent in Nashville, Tennessee, with 19 years of experience, says that rent-back situations are common in hot markets when homes sell quickly, and sellers need more time to transition.

Options to sell your home for a job relocation

Now that you’ve prepared yourself with some solid info, here are three top options for selling your home when you’re relocating for a job.

Option #1: Request a cash offer for your home

A new job can come with a ticking clock: Most employees are expected to move and settle into their new job location and position within a month.

If you’re operating on a crazy-tight deadline, you might not have the time to wait the usual 43 days for a traditional buyer to close on a purchase loan. This doesn’t even include the time to stage and clean the house for showings.

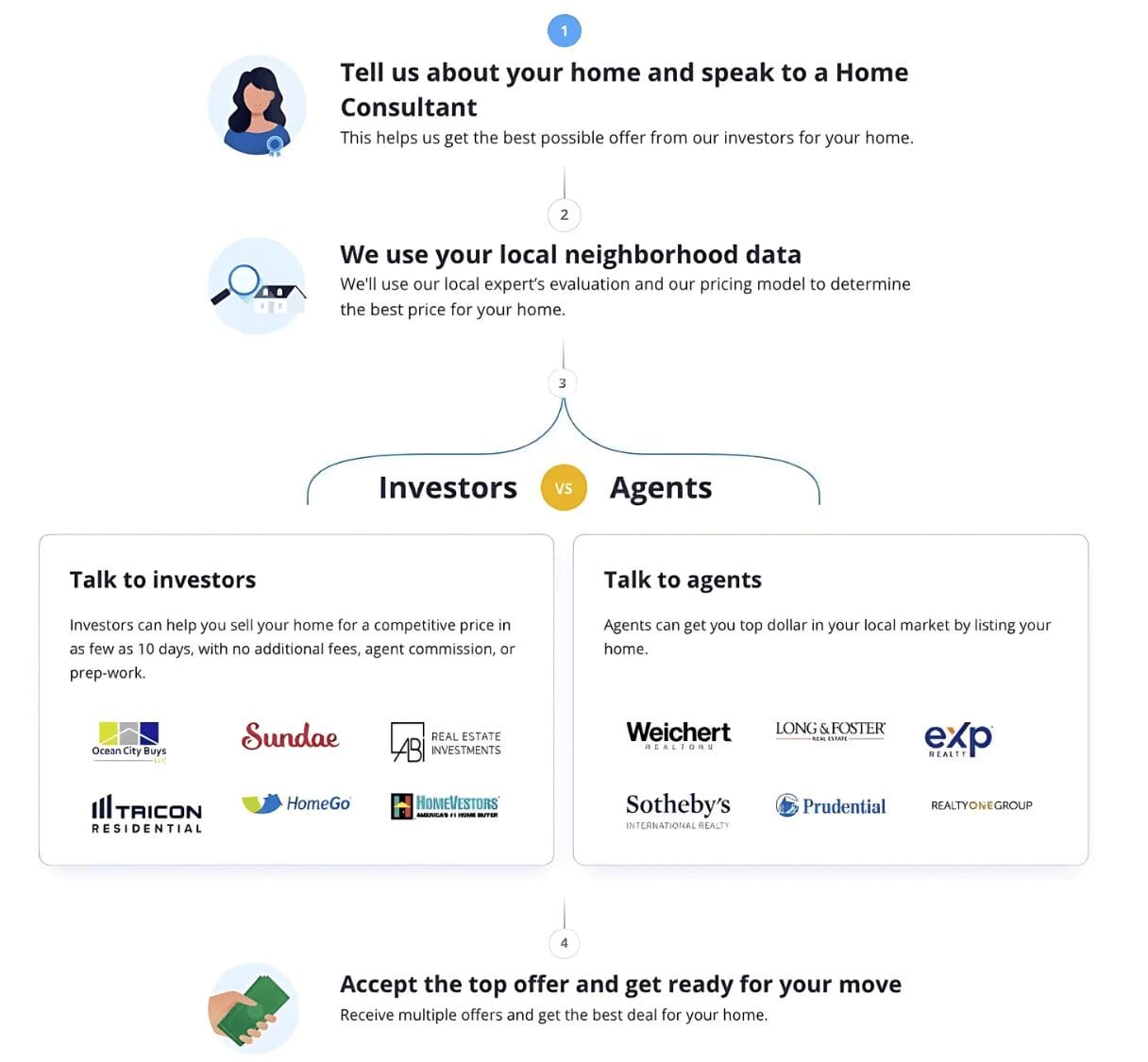

For a fast, low-fuss sale, consider selling your house for cash to a house-buying company or investor. HomeLight’s Simple Sale platform is a helpful resource for people selling their homes for a job relocation.

Simple Sale provides cash offers for homes in almost any condition nationwide. Just answer a few basic questions about your property, and you’ll receive a competitive cash offer within 24 hours.

Sellers can close in as little as 7 days and pick a move-out date up to 30 days from closing. There’s no need to worry about staging, repairs, or open houses.

Here are the four easy steps in the Simple Sale process:

While you’ll likely get a lower offer than if you listed your home on the open market, you can sell it as-is, eliminating the cost and time you’d typically have to put into home prep and repairs. Working with a cash buyer can also reduce a seller’s closing costs, including eliminating agent commissions.

Below, you can hear about how Baohan Wu, a seller who used Simple Sale to sell his high-rise apartment, closed within three and a half weeks, and what he thought of the process overall.

Consider this route if:

- You need to move quickly, as in, your new employer wants you there yesterday.

- Your home has significant issues that would hinder a buyer with traditional financing. “I [had] a client […] whose house has no power and no water, and they’re not in a situation to get those things turned on. For them, an investor is going to be their best choice,” Arledge says.

Avoid this route if:

- You want the highest possible price. While a platform such as Simple Sale provides a competitive offer, expect to get less for your home than you would if you were to sell the traditional way with a top real estate agent. You’re trading speed and convenience for a lower price, and sometimes, the discount can be steep.

- You have a decent relocation package or a generous time frame that eases the pressure to sell. Although some employees are only given a month to settle in, others can take their time, as they’re provided with three months or more to move.

Option #2: Hire a real estate agent who moves homes fast

Even if you have some time before you start your new job, moving for work adds pressure, especially if you’re headed out of state, and the process hits a snag. Fortunately, the experienced real estate agents in HomeLight’s network know how to handle those pressures.

Bonnie Roseman, a top-selling agent in Portland, Oregon, once sold a couple’s 1,200-square-foot two-bedroom home in about a week after the husband had to move for a job in Colorado Springs.

Speed up your home sale with these three key steps from our experts:

Clean and declutter so the home looks fresh and bright

According to HomeLight’s Top Agent Insights for Q3 2025, the most common home prep mistake sellers make is skipping decluttering and depersonalizing, which can affect how well the home sells. Clearing out excess items and personal touches helps people picture themselves in the house.

Buyers love to see available space, especially in photos. Roseman used a professional photographer to shoot photos, video, and a 3-D Matterport image of the layout of the Portland home, offered at $379,000. Within two days, a buyer wrote an offer with a substantial down payment.

With a pending move, you’re packing and purging anyway, so here’s where the sweat equity pays off. If you need a hand, hire a pro to deep clean your home before putting it on the market. For a 1,500-square-foot home, expect to pay between $180 and $375, according to Angi.

Enlist a junk removal service to take away the trash and old furniture, or call a charity such as the Salvation Army or Habitat for Humanity to pick up anything you’d like to donate.

Ramp up the curb appeal

Your home’s curb appeal makes a stunning first impression, enticing buyers before they even cross the threshold (implying that you maintain your house well). According to HomeLight’s Top Agent Insights for Q3 2025, a little landscaping and curb appeal work can boost a typical home’s value by about $7,919.

“Usually buyers will go do a drive-by first,” says Carey Lambert, a top real estate agent with almost three decades of experience in the Greater New Orleans area. “The home has to look great from the outside.”

You don’t have to invest a lot, either. Simple tasks like cutting the grass, controlling weeds, and adding a fresh layer of mulch can enhance the look of your outdoor space. Place a couple of planters with colorful flowers in your doorway to make it pop, or install uplighting to create a memorable first impression for buyers viewing your home at night.

Address any mechanical issues ASAP

A pre-listing inspection before you promote your home will flag any issues that could pose a health or safety risk or stall negotiations between getting a contract and closing.

While you’ll have to disclose the results to buyers, address minor repairs before hitting the market, such as servicing the air conditioning and heating systems. For anything that might give buyers pause, such as an aging roof or appliances, talk with your agent about offering a home warranty or adjusting the list price.

The house that Roseman sold in Portland underwent a home inspection, a radon inspection, and visits from a chimney mason and an arborist, but it needed no significant repairs.

Use the CMA to set the right price

If you’re in a hurry, it’s even more crucial to price your home right so it doesn’t languish on the market for weeks — or drop in price after you’ve moved. To determine home value, your real estate agent will conduct a CMA that analyzes local comparable sales or “comps.”

Comps are homes similar in size, amenities, structure, and age to yours that recently sold in your area. Real estate professionals and home appraisers use comps as a reference point for the subject home and then make dollar adjustments based on competitive differences. The analysis will take into account significant features that drive or reduce value.

Consider this route if:

- You want top dollar for your home and assurance that you’ve promoted it well. A great real estate agent can reach not only your local market but also the surrounding areas where people may be moving from.

- You have the time and inclination to make minor repairs. A seasoned agent can advise you on what’s worth fixing and what to leave off your to-do list. “Sometimes small details can make a large return on your investment,” Arledge says.

Avoid this route if:

- You’re pressed for time. When you list your home, there’s no guarantee that you will receive a cash offer. When working with a financed buyer, sellers need to consider the 43 days for mortgage processing and approval in addition to the time it takes to find a buyer (approximately 46 days as of January 2026).

- You don’t have the budget or the bandwidth for anything but a quick and clean break. If you’re stressed about finding schools or housing in your new location, you might want a quick and clean break from your old home, even if you don’t have to do much to sell it in the current market. Talk with your agent about your options.

Option #3: Rent it out rather than sell

If your current home location has a high demand for rentals or if you’re considering returning to the area soon, you could keep your home as a rental property. Renting it out can provide a steady monthly income and the potential for long-term property appreciation. It also allows you to hold onto your investment in case the market improves or you decide to move back.

There are instances where people have bought their house for a great price, have low payments, and can make a lot of money renting it out.

Jessica Arledge Real Estate AgentCloseJessica Arledge Real Estate Agent at Associate Broker Keller Williams Realty CAP5.0Currently accepting new clients

Jessica Arledge Real Estate AgentCloseJessica Arledge Real Estate Agent at Associate Broker Keller Williams Realty CAP5.0Currently accepting new clients

- Years of Experience 17

- Transactions 805

- Average Price Point $252k

- Single Family Homes 731

On the flip side, you’ll need to account for property management fees, vacancy periods, and ongoing maintenance costs, which can eat into your profits. Moreover, rental income is taxable, though you may be able to deduct expenses like repairs, property management, and mortgage interest. If you still have a mortgage on the home, confirm with your lender whether converting it to a rental affects your loan terms.

On top of the costs, of course, there’s the burden of finding a good renter and figuring out how to manage the property from afar.

Consider this route if:

- Your area is a booming rental market. If you’re not sure what’s going on with rents in your area, there are several great reports on the rental property market that you can consult.

- Your home has amenities that a renter might like, such as proximity to a park, a private backyard, or a finished basement with a walk-out.

- You plan to return to this area or have a sentimental attachment to the house. “I know people who absolutely love Savannah and want to retire here,” even if they have to leave in the interim, Arledge says.

Avoid this route if:

- You haven’t heavily vetted who will occupy your home. If you’re moving long-distance, you want to be confident both in your property manager and in your tenants. “Sometimes you get the best tenants in the world, and sometimes people trash a place,” Arledge says.

- You don’t have the focus to build a rental portfolio. Being a landlord involves more than collecting a rent check. You’ll need to use state-specific contracts and be aware of your tenants’ rights, for starters. You’ll also have to ensure you handle your taxes correctly.

Selling before vs. after you move

If you’re relocating for a new job or opportunity, one big question is when to sell your current home, before you move or after you’ve settled in. Both options come with their own set of perks and challenges. Here’s a quick breakdown to help you figure out what might work best for you.

Sell before relocating

Pros:

- You avoid overlapping housing expenses such as mortgage payments, utilities, and property taxes.

- You do not have to manage a home sale remotely, which can be logistically challenging and time-consuming.

- Selling first can simplify financing for your next home, especially if you need the proceeds from the sale for a down payment.

- You reduce the stress and risk associated with leaving a vacant home behind.

Cons:

- A tight timeline may force you to rush important decisions about your new home or location.

- If your next home is not immediately available, you may need temporary housing or storage for your belongings.

- You could miss out on additional home value if your current market is appreciating and you sell too quickly.

Move first and sell remotely

Pros:

- You gain more flexibility to stage the home, make improvements, or wait for a better market before selling.

- You can fully settle into your new location and focus on the transition before handling the home sale.

- If your employer provides a relocation package that covers housing costs, this option can be more financially manageable.

Cons:

- Maintaining two households temporarily can be costly and may put strain on your finances.

- You will need to rely heavily on a local real estate agent or property manager to coordinate the sale.

- If you need the proceeds from the sale to buy a new home, the delay could affect your ability to purchase promptly.

What to do if your home doesn’t sell before you move?

In case your home doesn’t sell before you move, you still have options to ease the transition. One solution is HomeLight’s Buy Before You Sell program, which lets you purchase your new home before selling your current one.

This short-term financing helps cover the down payment on your new home, helping you make a strong offer on your next home without a home sale contingency. Overall, it reduces the stress of timing both transactions perfectly. With the right approach, you can move forward without being financially stuck in your previous home.

Tips for your big move

Figuring out how to sell your house for a job relocation is a huge decision. While that’s in the works, experts recommend keeping these other things in mind to ensure a smooth move:

Book the moving company as soon as you go under contract:

Movers’ schedules fill up fast, especially during the summer months. Ask whether they charge any fees if your date changes, such as if repairs take longer than expected.

Ask how long the movers will take to deliver:

For long-distance moves of several thousand miles, moving companies typically take anywhere from one to three weeks to deliver your belongings. The duration depends on weather conditions, traffic congestion levels, and transportation laws that limit how many miles and hours drivers can be on the road each day.

Have a contingency plan if the moving company cancels:

Lay the groundwork for hiring a container or freight company if something happens to your movers at the last minute. Tell them you may hire a professional mover, but you’d like to consider their services as well. Let them know when and where you’re moving and how much you have. Then ask about their turnaround time.

Plan for moving your car:

Depending on how far you’re moving, talk with the moving company about transporting your car or hire an auto shipper. Also, be prepared for unexpected fees. Some states, such as Georgia, charge an ad valorem tax on a newly registered vehicle based on its market value.

Selling a House for a Job Move Is Stressful

Enlist the help of a top real estate agent in the area to lighten your load and help the process go smoother. We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you. Our service is 100% free, with no catch. Agents don’t pay us to be listed, so you get the best match.

Your new job (and city) await

If the world is your oyster and a career change feels right, you can orchestrate a smooth move even when you own a house. Whether you sell your home to an investor, work with a top agent to sell it at a competitive price, or opt to rent it out for a while, rest assured that the stress over selling a house for a job relocation is only temporary.

Soon you’ll be exploring a new place, building relationships with colleagues, and settling into a new home ready for fresh memories. If you need expert insights about selling your home while managing a job transition, talk to a top-performing real estate agent today.

Header Image Source: (VGstockstudio/ Shutterstock)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.