How to Give a House as a Gift to a Family Member

- Published on

- 9 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

Giving a family member a house as a gift can be one of the most generous and life-changing presents you ever give. It can be a way to keep a treasured home in the family or help an adult child get a good start in life.

Whether you’re contemplating this grand gesture for a loved one or planning your estate, we’ll break down the different ways to gift a house, explain the tax implications, and provide a typical house-gifting example scenario.

Home values have rapidly increased in recent years. How much is your current home worth now? Get a ballpark estimate from HomeLight’s free Home Value Estimator.![]()

How Much Is Your Home Worth Now?

What are the top reasons people give a house as a gift?

Here are some of the top reasons people choose to give the gift of a home to a family member:

- Asset transfer for estate planning: Simplifying inheritance by transferring property ahead of time.

- Helping family members financially: Assisting loved ones with housing without the burden of a mortgage.

- Tax benefits: Leveraging potential tax advantages associated with property gifting.

- Celebratory gifts: Marking significant milestones such as weddings, graduations, or retirements with a meaningful asset.

- Family member has poor credit: Offering a stable living situation for those unable to secure a mortgage due to credit issues.

- Reduce assets to qualify for Medicaid: Strategically managing assets to meet eligibility requirements for long-term care assistance through Medicaid.

- Avoiding the real estate market’s unpredictability: Transferring property in a stable manner amidst fluctuating market conditions.

What are the tax implications when you gift a house?

Understanding the tax implications when gifting a house is crucial to ensure both you and your loved one benefit from this generous act without unexpected financial burdens or tax surprises. Here’s what you need to know:

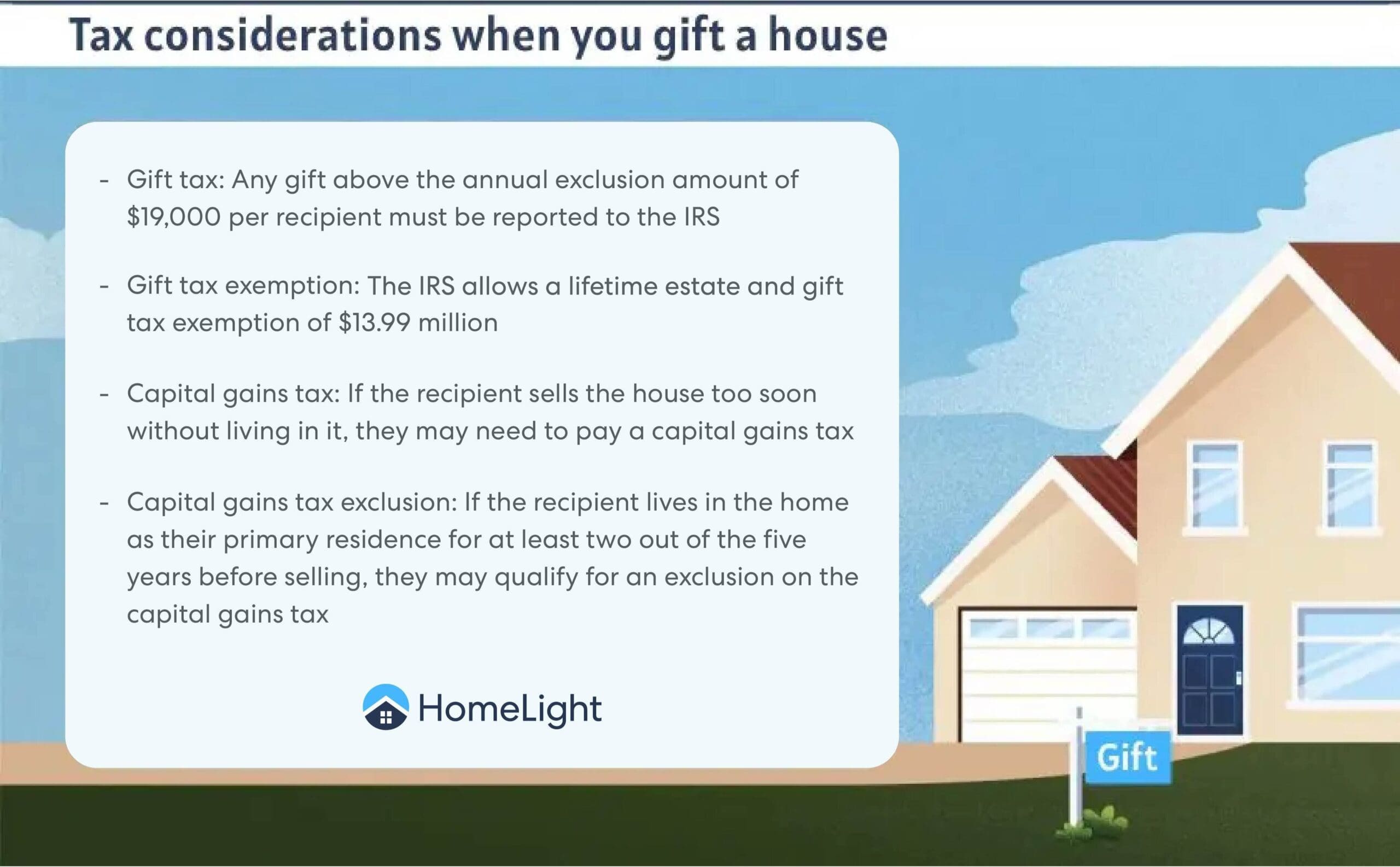

- Gift tax considerations: When you gift a property, it may be subject to the federal gift tax, depending on the home’s value. As of the latest guidelines, any gift above the annual exclusion amount ($18,000 per recipient in 2024; $19,000 in 2025) must be reported to the IRS. However, you can also apply this gift towards your lifetime estate and gift tax exemption of $13.99 million (up from $13.61 million in 2024).

- Capital gains tax: The recipient of your gift takes on the home’s original purchase price as their cost basis. If they sell the house, capital gains tax could apply based on the difference between the sale price and the original purchase price, not the value of the home when gifted.

- Living in the gifted home: If the recipient decides to live in the property as their primary residence for at least two out of the five years before selling, they may qualify for an exclusion on capital gains tax up to a certain limit.

- State taxes: Some states have their own gift tax or inheritance tax. It’s important to check the regulations in your state to understand any additional tax liabilities.

Navigating these tax implications can be complex, and strategies like applying the annual exclusion or lifetime exemption, or even selling the property at a reduced price, can significantly impact your financial situation. Consulting with a tax professional or estate planner can provide personalized advice and help you make the most of your generous gift.

How does giving a house as a gift work?

When it comes to gifting a house to a family member, there are several paths you can take, each with its own set of considerations and procedures. Here’s an overview of the most common options:

- Giving the house as a complete gift: This involves transferring the title of your property to the recipient without receiving any payment in return. This method is straightforward but requires understanding the tax implications, such as the potential for gift taxes if the value exceeds the annual exclusion amount.

- Selling the house at a personal loss: You might choose to sell the house to your family member at a price below market value. While this can still incur gift taxes on the difference between the sale price and the market value, it could be a more manageable way for the recipient to acquire the property.

- Adding the recipient to the home’s deed: This method involves adding the family member’s name to the property’s deed while you remain on it. This is technically creating a new deed and establishing a joint tenancy that includes built-in rights of survivorship. It’s a simpler process but doesn’t avoid taxes and might have implications for your estate because you will no longer have full control over your property.

- Creating a life estate: With a life estate, you gift the property but retain the right to live in it until your death. Afterward, the property automatically passes to the recipient. This option ensures you can use the property for the rest of your life while also planning for its future ownership.

- Use a Qualified Personal Residence Trust (QPRT): A QPRT allows you to transfer your home into a trust for a specific period. You can continue living in the home during this time. Once the term ends, the home passes to the trust beneficiaries, typically at a reduced gift tax cost. This option is complex and requires professional advice to implement correctly.

Each of these options offers a different balance of control, tax implications, and financial considerations. Choosing the best method depends on your personal circumstances and the recipient’s needs.

Scenario: Gifting a family home to a child

In the example scenario below, let’s explore how the process of gifting a house as a “complete gift” might unfold. We’ll highlight the key steps and tax implications involved.

John, a retired teacher, decides to gift his vacation cottage to his daughter, Emily, as a way to pass on a family asset and help her secure her future. The cottage is valued at $300,000, and John owns it free and clear, with no outstanding mortgage.

Step 1: Determining the tax implications

First, John consults with a tax advisor to understand the tax implications of his generous gift. Since the value of the cottage exceeds the annual IRS exclusion amount for gifts ($18,000 per recipient in 2024; $19,000 in 2025), John learns he must file a Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return. However, because the gift also falls under the lifetime estate and gift tax exemption amount ($13.61 million in 2024; $13.99 million in 2025), John won’t have to pay any gift tax, although the value of the gift will reduce his lifetime exemption.

Step 2: Hiring a real estate attorney

To ensure the transfer goes smoothly, John hires a real estate attorney to prepare the necessary paperwork, including a deed that officially transfers ownership of the property from him to Emily. The attorney also advises John on the importance of a title search to ensure there are no issues that could affect the transfer.

Step 3: Filing the gift tax return

Following the attorney’s advice, John files the gift tax return (Form 709) with the IRS, reporting the transfer of the cottage. This step is important for documenting the gift and ensuring compliance with tax laws.

Step 4: Transferring the deed

With the paperwork in order, John and Emily meet with the attorney to sign the deed over. This formalizes the gift, and Emily becomes the new owner of the beachfront cottage. The deed is then recorded in the local county’s land records office, completing the legal transfer of property.

Step 5: Understanding the Tax Basis and future sales

John’s tax advisor explains to Emily that her tax basis in the property is the same as John’s original purchase price, not the current market value. This means if Emily decides to sell the cottage in the future, her capital gains tax will be calculated based on the difference between the sale price and John’s original purchase price. However, if Emily makes the cottage her primary residence and lives there for at least two out of the five years before selling, she may be eligible for an exclusion on capital gains tax up to a certain limit.

In a sale among relatives, an agent creates a safeguard to help prevent familial strain and adds a level of formality and professionalism to an important transaction.![]()

Hire an Agent to Coordinate Your Family Sale

What if the gift house has a mortgage?

Gifting a house that still has a mortgage requires navigating several complexities, including the often-overlooked “due-on-sale clause” found in most mortgage agreements. This clause allows the lender to demand the full repayment of the loan if the property is transferred to someone else. Here are key considerations and steps to take if the house you wish to gift is not yet fully paid off:

- Review the mortgage agreement: Before proceeding with any gift plans, it’s essential to review the mortgage agreement for a due-on-sale or due-on-transfer clause. This will determine whether transferring the property could trigger the requirement to pay off the mortgage in full immediately.

- Assume the mortgage: In some cases, the mortgage lender may allow the recipient of the gift to assume the existing mortgage. This means the recipient takes over the mortgage payments under the same terms. However, not all mortgages are assumable, and lenders typically require the new borrower to qualify for the mortgage, similar to a standard loan application process.

- Pay off the mortgage: If financially feasible, you might choose to pay off the mortgage before gifting the house. This simplifies the transfer process, as the property can be gifted free and clear of any liens or encumbrances.

- Gift the property subject to the mortgage: You can gift the house even if the mortgage is not paid off, but the mortgage remains in your name. This arrangement requires a clear understanding between you and the recipient about who will make the mortgage payments. However, this does not relieve you of the legal obligation to the lender, and any default on payments could impact your credit score.

- Refinance the mortgage: Another option is for the recipient to refinance the mortgage in their own name. This is essentially taking out a new mortgage to pay off the existing one, transferring the debt to the recipient. The recipient will need to qualify for a new loan based on their creditworthiness and financial situation.

- Seller financing: If other options aren’t viable, you might consider seller financing. In this scenario, you act as the lender, and the recipient makes payments to you instead of a traditional mortgage lender. This option requires legal agreements to outline the terms of the loan, including interest rates and repayment schedule.

Consult with experts before giving a house as a gift

Gifting a house to a family member is a profound gesture of generosity that can have significant financial and emotional benefits. However, it’s a process that requires careful consideration of several critical factors, including understanding the tax implications and choosing the most suitable method for transferring ownership.

Given the complexity of tax laws and the potential for significant financial implications, consulting with a qualified real estate advisor, tax professional, or attorney is the best way to navigate the process successfully and make the most of your generous gift.

To learn more about how the Internal Revenue Service handles gift taxes, visit this IRS resource page, “Frequently Asked Questions on Gift Taxes.”

Editor’s note: This post is for educational purposes. If you need assistance navigating the legalities or tax implications of giving a house as a gift, HomeLight encourages you to reach out to a professional advisor.

Header Image Source: (Roger Starnes Sr / Unsplash)

- "What Is the Lifetime Gift Tax Exemption?," SmartAsset, Ben Geier, CEPF® (August 2025)

- "Eligibility Policy," Medicaid

- "How Do I Calculate Cost Basis for Real Estate?," H&R Block (January 2019)

- "Estate and Inheritance Taxes by State, 2024," Tax Foundation (November 2024)

- "IRS releases tax inflation adjustments for tax year 2025," IRS (October 2024)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.