Is Paying Off the Mortgage Before Retirement a Smart Move?

- Published on

- 6 min read

-

Christine Bartsch, Contributing AuthorClose

Christine Bartsch Contributing Author

Christine Bartsch, Contributing AuthorClose

Christine Bartsch Contributing AuthorFormer art and design instructor Christine Bartsch holds an MFA in creative writing from Spalding University. Launching her writing career in 2007, Christine has crafted interior design content for companies including USA Today and Houzz.

-

Jedda Fernandez, Associate EditorClose

Jedda Fernandez Associate Editor

Jedda Fernandez, Associate EditorClose

Jedda Fernandez Associate EditorJedda Fernandez is an associate editor for HomeLight's Resource Centers with more than five years of editorial experience in the real estate industry.

Should you pay off the mortgage before retirement? Unfortunately, there’s no one-size-fits-all answer to this question. Your finances and goals are so unique that the path toward the retirement of your dreams will be just as tailored.

For some, paying off the mortgage while they’re still earning income is a “must-do” to preserve limited funds once the paychecks stop flowing. However, leaving no cushion in your savings to eliminate mortgage debt could leave you financially strapped and unprepared for any unexpected expenses down the road.

A Quick (And Free) Way to Check Your Home Value

Get a preliminary home value estimate in as little as two minutes. Our tool uses information from multiple sources to give you a range of value based on current market trends.

Should you pay off mortgage before retirement: A comparison table

This table summarizes when it might make sense to pay off mortgage before retirement versus when you might consider retaining the mortgage even as you reach retirement age.

| Scenario | Pay off mortgage before retirement if… | You don’t have to pay off mortgage early if… |

|---|---|---|

| Cash Flow & Stability | You want significantly lower monthly expenses in retirement to live on a fixed/limited income (e.g., Social Security). | You have a substantial, well-diversified retirement portfolio that comfortably covers the mortgage payment and living expenses. |

| Savings & Liquidity | Paying off the mortgage does not deplete your emergency fund or necessary liquid assets (e.g., you still have 6-12 months of expenses saved). | Paying off the mortgage would exhaust your emergency fund or force you to liquidate investments at a loss. |

| Investment Returns | The after-tax interest rate on your mortgage is higher than the expected after-tax return on a low-risk investment (e.g., Treasury bonds). | Your non-mortgage investments (e.g., diversified stock market portfolio) are reliably generating a higher after-tax return than your mortgage’s interest rate. |

| Tax Situation | You no longer benefit substantially from the mortgage interest tax deduction (e.g., due to lower income or taking the standard deduction in retirement). | You are in a high-enough tax bracket and have enough other itemized deductions that the mortgage interest deduction provides a significant financial benefit. |

| Risk Tolerance | You prioritize the psychological benefit and financial security of being completely debt-free. | You prefer maximizing wealth accumulation and are comfortable with the calculated risk of maintaining debt if the investment returns outweigh the interest cost. |

| Age/Time Horizon | You are planning for retirement within the next 10-15 years and want to systematically eliminate the debt before your income stops. | You have options like refinancing to a lower rate, using a reverse mortgage to eliminate payments, or downsizing the home. |

To find the best solution for your personal financial situation, let’s turn to the experts for answers to all the unknowns related to this complex dilemma.

What are the benefits of paying off my mortgage before retirement?

This most common mortgage payoff-related question is one of the easiest to answer.

“The financial security of not having the burden of a house payment during retirement is the biggest benefit,” says top-selling agent Kevin Shaw, who’s sold over 83% more single-family homes in Johnstown, Colorado, than the average agent. “If you’re on a limited income every month, like say social security, now that can go towards living expenses rather than funding your home.”

While paying off the mortgage before retiring means lowering your monthly housing expenses by a considerable amount, it doesn’t eliminate them completely. You’ll still need to plan on paying for things like property taxes, homeowners insurance, maintenance expenses, and utilities.

Other benefits come with freeing up your monthly cash flow. You’ll be reducing the amount of interest you’ll pay over the lifetime of the loan by paying it off early. You’ll also have the financial security of a debt-free asset whose cash value you can access with a home equity line of credit.

“It’s a good idea to plan your retirement around when that mortgage is paid off,” advises Tim Kennedy, a retirement mortgage professional. “Once you retire, you’re not making income anymore. So every mortgage payment you make, you’re withdrawing money from your retirement portfolio that you may need some time down road.”

Since paying off your mortgage before retiring is the smart financial move for most people, you’d think most people would be doing it. Research from Fannie Mae shows that 58% of retirees aged 60+ in 2024 owned their homes outright, but 56% wished they had saved more for retirement.

One big reason homeowners carry a mortgage into their retirement is simply that they cannot afford to pay it off by the time they’re ready to retire — at least, not without dipping substantially into their savings.

Should I use my savings to pay off mortgage before retirement?

The lure of living mortgage-free is so attractive to some seniors that they’re willing to spend some, most, or all of their retirement savings to completely pay off their home loan. This can be a financially crippling move for some, especially these days.

In the survey, 61% of homeowners aged 60+ admit to wishing they had saved more for retirement when they were younger.

That’s why some experts advise clients against depleting their savings to pay off the mortgage.

“I would not feel comfortable, as a professional, advising retirees to deplete all of their liquid assets and savings to pay off the mortgage. I think that would be a bad idea,” warns Shaw.

“You need to have a certain amount of liquid cash on hand in retirement. If you use your savings to pay off your mortgage, you run the risk of not having enough cash to take care of emergencies that come up.”

However, it’s not always a bad idea to dip into your savings to eliminate your mortgage.

In a case study for the Center for Retirement Research at Boston College, economist Anthony Webb found that the majority of homeowners are better off financially by paying off their mortgage before retirement — even if they need to use pull funds out of retirement accounts.

Doing the math, Webb discovered that most retirees would pay more in interest on their mortgage than they would make on the interest by leaving their savings in a low-risk investment, such as a treasury bond.

Only the small minority of homeowners who have all or almost all of their assets invested in the stock market (who need the mortgage interest tax deduction) reap any benefit from hanging on to their home loan.

However, you may be able to save some money with a short-term delay on repaying that mortgage.

Webb notes in his study that, “It is optimal to delay repaying the mortgage for one year if the after-tax interest rate on the household’s short-term deposits exceeds the aftertax cost of the mortgage.”

How can I pay off mortgage before retirement?

The biggest mistake retirees make is deciding to pay off their mortgages too late. That’s why so many are faced with the difficult “dip into my savings, or not to dip into my savings” dilemma.

If you don’t want to face that tough decision, you need to start paying that house debt down at least a decade before you’re ready to retire.

A more recent study by the Center for Retirement Research at Boston College found that older sellers see lower returns on their home sale.

“People should plan to pay off their mortgage 10 to 15 years prior to retirement rather than a lump sum when you’re about to retire, advises Shaw. Some options to pay off mortgage before retirement include:

- Refinancing to a shorter term

- Making extra mortgage payments

- Using tax refunds towards extra house payments

Does making one extra mortgage payment a year really help?

Making one extra payment a year or paying your tax refund toward your mortgage may not sound like much, but it adds up over time. These extra payments work to reduce the interest you’ll pay to the bank because the entire amount is going toward paying down the principal balance.

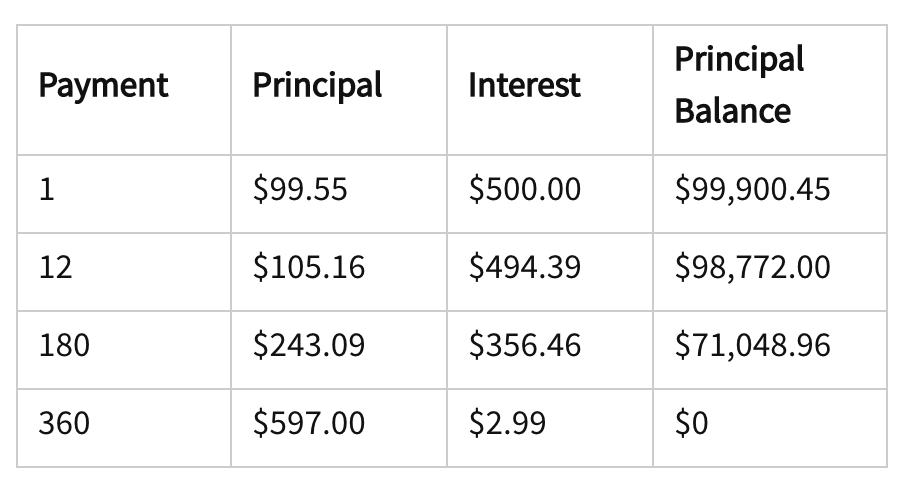

Believe it or not, the majority of the mortgage payment you make every month isn’t going toward the principal; it’s going toward the interest. For example, if you have a 30-year mortgage for $100,000, less than $100 of your $600 payment goes toward paying down the debt itself.

This rate improves with every payment made, but even when you’re halfway through your installments at payment number 180, only $250 of that $600 is going toward your balance.

So every lump sum payment you make toward your principal balance reduces the amount of interest you’ll be charged on that debt, which means each subsequent payment you make will pay towards the principal at a better rate.

How can downsizing help cut down on mortgage debt?

Aside from just paying off your existing loan, there are other ways to eliminate your monthly mortgage payment, such as downsizing.

Downsizing uses the equity you’ve built up in your current house to finance a smaller, less expensive home. That smaller price tag means you’ll only need a small loan, or you may even be able to purchase the property outright with your home sale proceeds.

“Downsizing to eliminate your mortgage payment or to get into a smaller mortgage so the home loan doesn’t deplete your retirement portfolio is not a bad idea if the market conditions are right,” says Kennedy. When home values are high, it would be a great time to “sell my home if I want to get top dollar for it.”

If you make smart downsizing decisions, you’ll not only significantly reduce or eliminate your monthly mortgage payment, you’ll also lower other housing expenses, including utilities, home insurance, home maintenance, and property taxes.

But buying a smaller house doesn’t guarantee that you’ll be saving money. If you’re not careful, you might wind up buying a smaller home in a more expensive area that’ll have higher utility prices and higher taxes. Plus, the overall expenses of downsizing may add up to too much money.

“You have to sit down with pen and paper to figure out what you’re spending on principal and interest each month,” advises Kennedy. “We’d look at the terms of the new 15 or 20-year term loan, add the closing costs, and see if it’s feasible to save you any money on a monthly basis.”

When is a reverse mortgage the better financial decision than paying off my mortgage?

For those who want to eliminate their monthly mortgage payment without the stress of moving or concern over depleting your savings, one option is taking out a reverse mortgage.

“A reverse mortgage may be a viable option for a lot of people rather than paying off their mortgage,” says Shaw. “With a reverse mortgage, you’re not making a mortgage payment — so the interest is adding rather than coming off every month. When you die, you may owe more for your home than you did, but you haven’t had to make a mortgage payment for 20 years.”

The trouble is, reverse mortgages come with risks. Horror stories have circulated of little old ladies being thrown into the streets, and rumors spread about seniors with reverse mortgages losing their homes to the banks piece by piece.

The truth is, as long as you continue living in the property as your primary residence, the title remains in your (the homeowner’s) name. And those “out on their ear” circumstances often occurred because those senior homeowners stopped making payments on other housing expenses, like the utilities or property taxes.

Reverse mortgages were once highly unregulated. “It was really the Wild, Wild West. So in 2015, the federal government developed financial assessments and other mechanisms to protect the consumer,” explains Kennedy.

With these protections in place, today’s reverse mortgages function in a similar fashion to a Home Equity Line of Credit, where a bank lends you cash using your home’s equity as collateral. Those funds are then available to you as a lump sum, a line of credit, or in monthly installments paid to you.

You can even use a reverse mortgage to help you downsize using a home equity conversion mortgage (HECM).

“With an HECM for purchase, or a reverse for purchase, seniors are able to keep the bulk of the money from the sale of their primary residence to buy another property without having the burden of another monthly payment,” explains Kennedy.

“For example, let’s say you have $500,000 in the bank from the sale of your home that you owned free and clear. Instead of taking $300,000 of that money to purchase another house outright, you would make a down payment of $150,000 and finance the rest with an HECM, which doesn’t require monthly mortgage payments. That leaves $350,000 in the bank for your long term goals. With more money in the bank and less money owed in monthly bills, that benefits your strategic retirement plan.”

Is it ever better to refinance instead of paying off my existing mortgage?

If all of the options for eliminating your home loan are out of the question, but you’re still unhappy with your existing mortgage, it may be wise to refinance.

How does refinancing work? Essentially, you’re paying off your existing mortgage and replacing it with a new loan that has better terms and interest rates. Since you’re getting a new mortgage, you will need to qualify for a new loan.

However, deciding whether or not refinancing is “better” for you depends on your financial situation and the terms of your existing mortgage.

Let’s say you’ve still got 20 years left on your mortgage. You may be able to refinance with a 15-year mortgage so you can pay it off faster and get a lower interest rate. While there’s a chance that you’ll pay a higher mortgage payment with a shorter-term loan, more of your monthly payment is going toward the principal balance rather than toward interest with a shorter loan.

The trick is finding a mortgage company offering better interest rates than those on your current loan. Every mortgage lender determines its own rates, which is why experts recommend that you get quotes from multiple lenders and brokers.

So not only do you need to find a lender offering a lower rate, you need to make sure that lower rate applies to the loan type and time period you want.

For example, the same lender may charge 4.88% interest on a 15-year, fixed-rate mortgage for a new purchase home, while charging 5.59% interest on a 30-year fixed rate mortgage.

How to figure out the right retirement plan

Experts agree that paying off your mortgage before you retire is the smart financial move for most people (all but those select few who need the tax break that a mortgage provides).

Figuring out the right financial plan to reduce or eliminate your mortgage is the tricky part. A certified financial planner can help you determine if, when, and how to pay off your mortgage before you retire.

Step one: Talk to an expert!

Selling your house soon? Connect with a top agent near you to get an expert opinion on how much your house will sell for, what to fix before listing, and the latest local housing market trends.

Key takeaways

- Financial security is the primary benefit: For the majority of homeowners, paying off the mortgage before retiring is a smart financial move that lowers living expenses and is crucial for those who will rely on fixed incomes like Social Security.

- Liquidity is non-negotiable: Do not deplete essential liquid savings or your emergency fund (aim for 6–12 months of expenses) to pay off the mortgage. Sacrificing liquidity can be financially crippling if unexpected emergencies arise.

- Investment vs. debt: Most retirees benefit more from eliminating mortgage interest than they would gain from leaving equivalent funds in low-risk investments (like Treasury bonds), according to financial research.

- Start early: Plan to systematically pay down the debt 10 to 15 years before retirement using strategies like refinancing to a shorter term or making extra principal payments.

- Alternatives exist: There are alternatives to early payoff, such as downsizing or reverse mortgage (HECM).

- Tax deduction value decreases: The benefit of the mortgage interest tax deduction often diminishes in retirement due to lower income levels or opting for the standard deduction.

- Seek professional guidance: A certified financial planner can provide tailored advice on whether, when, and how to structure your plan for mortgage reduction or elimination based on your specific financial portfolio and goals.

If downsizing is the right financial plan to eliminate your mortgage payment, be sure to enlist the help of a top tier agent who can get you top dollar on your home sale and find you the best deal on a smaller house.

Header Image Source: (Matthew Bennett / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.