Using Your Home Equity for Retirement Income: 5 Options to Explore

- Published on

- 5 min read

-

Christine Bartsch Contributing AuthorClose

Christine Bartsch Contributing Author

Christine Bartsch Contributing AuthorClose

Christine Bartsch Contributing AuthorFormer art and design instructor Christine Bartsch holds an MFA in creative writing from Spalding University. Launching her writing career in 2007, Christine has crafted interior design content for companies including USA Today and Houzz.

As the cost of living rises at the fastest pace in 10 years, facing a future without a steady salary is a scary thought for retirees.

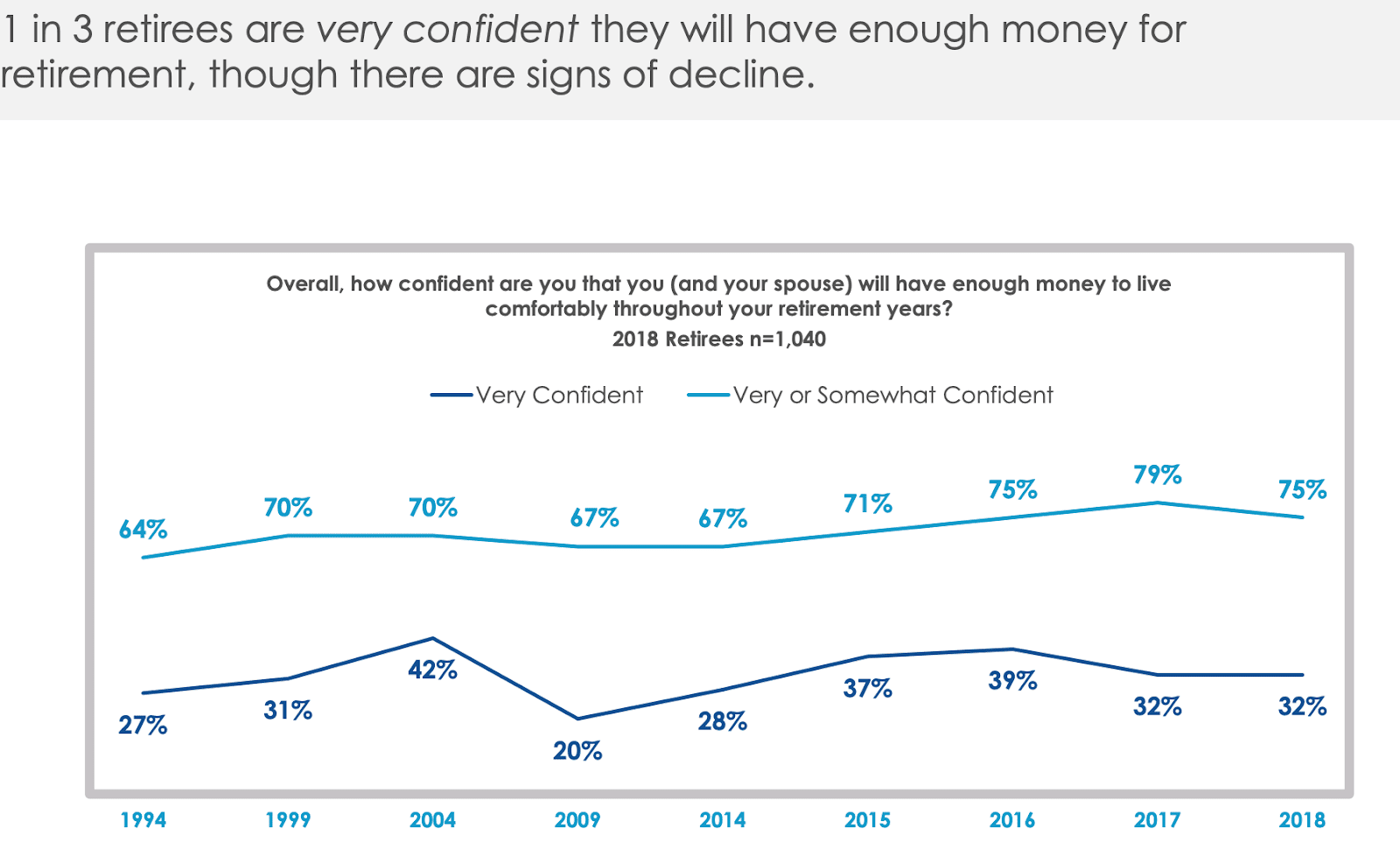

What’s more, a 2018 Retirement Confidence Survey by the Employee Benefit Research Institute found that only 1 in 3 retirees are “very confident” that they have enough money to live comfortably throughout their retirement.

Using your home equity for retirement income is one way to help secure financial post-career stability, but liquidating that wealth isn’t as simple as taking out cash from an ATM.

Tough decisions start with knowing your options, so here we’ll walk you through the most popular routes and help you weigh the pros and cons of each one, including:

- Taking out a reverse mortgage

- Tapping into a HELOC (home equity line of credit)

- Refinancing your mortgage

- Downsizing your home

- Selling your home and renting

Option A: Keep your home and…

Whether you’re renting or own your own home—it’s common knowledge that paying for a place to live is your biggest bill each month. Recent statistics show that the majority of Americans spend close to one-fourth of their annual income on shelter.

Once you’ve paid off your mortgage, though, your monthly housing costs drop dramatically. Sure, you’ll still need to pay for utilities, property insurance, home maintenance, and have some savings stashed away for home repairs. But overall—when you own your home outright, you’ll need less money to cover living expenses.

That’s why many retirees choose to keep their homes and age in place.

Even though you don’t have a mortgage, though, you’ll still have to cover those other housing costs and other necessities like food, medical needs, and transportation.

If your Social Security benefits and dividends from other retirement assets aren’t enough to cover your monthly expenses, there are ways that your home equity can help—without having to sell your house.

1. Take out a reverse mortgage

A reverse mortgage converts your home equity into cash while allowing you to continue living in the house. Essentially, you’re selling your home equity to the bank bit by bit.

There are a number of reverse mortgage types available from a variety of lenders.

However, it’s important to note that the Home Equity Conversion Mortgage (HECM) is the only reverse mortgage insured by the U.S. Federal Government.

In the right conditions, a reverse mortgage offers the best of both worlds. But there’s good reason why some financial planners say reverse mortgages are a last resort option.

Pro: Access to equity and no monthly mortgage payment

A reverse mortgage is one of only a handful of ways to access the cash value of your home equity without selling it.

And unlike a traditional mortgage, a reverse mortgage doesn’t require a monthly mortgage payment. Instead, the bank gives you a check monthly, based on the value of the home.

Con: The whole loan comes due when you leave the home

As great as it sounds that you don’t have to pay monthly on a reverse mortgage, don’t ever forget that it is a loan.

The minute the home is no longer your primary residence, your reverse mortgage comes due immediately—whether you decide to downsize, transition into assisted living, or pass away.

Pro: The title remains in your name

“Many people still assume that they have to sign the house over to the bank when they do a reverse mortgage,” says Matthew Stewart, a Certified Financial Planner with 20 years of industry experience, Chartered Financial Consultant, and president of Forestview Financial Partners, LLC. “This isn’t true. The homeowners still own the house the entire time.”

The title remains in your name, so it is possible to sell the home even if you have a reverse mortgage.

Con: A reverse mortgage hurts your ability to sell your house later

If you ever do want or need to sell your home, the reverse mortgage can complicate the process.

“We’ve had clients who wanted to downsize, and it creates an additional difficulty because obviously that reverse mortgage has to be paid off. That can be difficult to afford, depending on how far the reverse mortgage has gone,” says Ken Carpenter, who ranks in the top 1% of sellers’ agents in Plymouth, Minnesota.

“In one case we ended up doing a short sale, and the lender had to agree to take a loss on the sale of the home.”

Pro: You won’t owe more than your home is worth

If you’ve obtained an FHA-insured HECM, that’s a non-recourse loan. This means that you are not at risk of having to pay more than what you get from the sale of your home (as long as the home sells for 95% of its appraised value).

Stewart advises, “One difference with reverse mortgages over traditional mortgages is that if the loan balance is greater than the value of the home at pay-back time, then the debt amount over the home value is forgiven.”

But this is only good news if you’ve already used up all of your home’s equity—which is a distinct possibility with a reverse mortgage.

Con: You’re spending down your home equity

With a traditional mortgage, you’re slowly paying of the debt you owe on your house. With a reverse mortgage, you’re adding to your debt each month. The longer you have a reverse mortgage the less equity you have left in your house.

2. Use a home equity line of credit to purchase a rental property

A home equity line of credit (HELOC) is a revolving credit line that uses your house as collateral. Unlike a reverse mortgage, you’ll need to make a minimum payment toward the principal loan amount and the interest each month.

Since a HELOC actually increases your monthly bills and your overall debt, it’s never advisable to rely on it as a cash supplement to your retirement income.

The only practical way to use a HELOC to generate additional retirement income is to use it as a down payment towards a rental property investment.

Pro: A rental property is a tangible asset

Investors with free and clear cash have a choice to make between investing in real estate or the stock market. Both come with risks and benefits, making it a personal preference decision.

However, when your investment capital is coming out of your primary residence via a HELOC, purchasing a rental property is the clear choice.

“A lot of people are looking at rental properties as additional income for those retirement years. It’s a physical asset, so it’s certainly more stable,” says Carpenter.

Since land is an appreciating asset, in the long run your investment will continue to grow—unlike a risky investment in a volatile stock market, where your investment could lose value.

Con: It takes time to liquidate a rental property

For many retirees, home equity serves as their “in case of emergency” funds, available to pay off large, unexpected expenses like a new roof or medical bills. But if you’ve already used a HELOC as a down payment on a rental property, you may not have enough equity left in reserve.

You can sell off that rental property to cover emergency expenses, however that’ll take some time. A recent report says that homes spent an average of 48 days on market before selling. And selling a rental home with an existing tenant can further complicate and delay the sale.

Pro: An investment property guarantees a monthly rental income

If you’ve found the right investment property for you, the dividends from rent will allow you to pay back the HELOC, cover expenses for the rental property, and to supplement your monthly income.

“The stock market has been very unstable this year. So if you had a $300,000 investment in the stock market, there’s probably been no return this year,” advises Carpenter. “But had you purchased a rental property for $300,000, you would have had an income of approximately $24,000, which is about a 7 or 8% return.”

Con: You’re increasing your monthly housing expenses

Owning a house costs money. Owning two houses costs more. Property taxes, maintenance, and other fees add up.

Plus, you’ll want to hire a property manager to find and communicate with tenants, collect the rent, and make minor repairs. This will cost around $80 to $90 a month or more.

3. Refinance your mortgage

If you haven’t fully paid off your home yet, and you’re still carrying a mortgage from years ago when interests rates were 7-8% or higher, refinancing may be a smart way to access some of your home equity.

Pro: You can pull out some equity when you refinance

Today’s mortgage rates are hovering around 4-5%. So you could pull out a lump sum of your equity when you refinance your home and still be paying less than you are now.

Con: Refinancing interest rates are typically higher

Don’t let those low mortgage rates fool you. If you’re refinancing instead of buying new, those rates are often slightly higher, depending on the loan type and how you structure the loan.

Every mortgage lender determines its own rates, which is why experts recommend that you get quotes from multiple lenders and brokers.

Con: Refinancing will cost you

Refinancing isn’t cheap. First off, you’re going to have closing costs and lender fees which are typically 3% to 6% of your outstanding principal on your existing mortgage. You may also be on the hook to pay a prepayment penalty to your original lender.

You’re probably extending the life of your mortgage, too. The shortest term for most mortgages is 15 years.

If you do manage to find a lender to give you a 5-year, fixed rate mortgage, the monthly payment may wind up being more than you’re paying now, depending on how much equity you pull out of your house.

Option B: Sell your home, liquidate your equity and…

How much is your home worth? It depends. You can’t always count on your home being worth as much tomorrow as it is today.

Until you sell, your home’s value is just a number on a piece of paper. That number can change as the real estate market shifts between buyer’s, seller’s, and balanced market conditions.

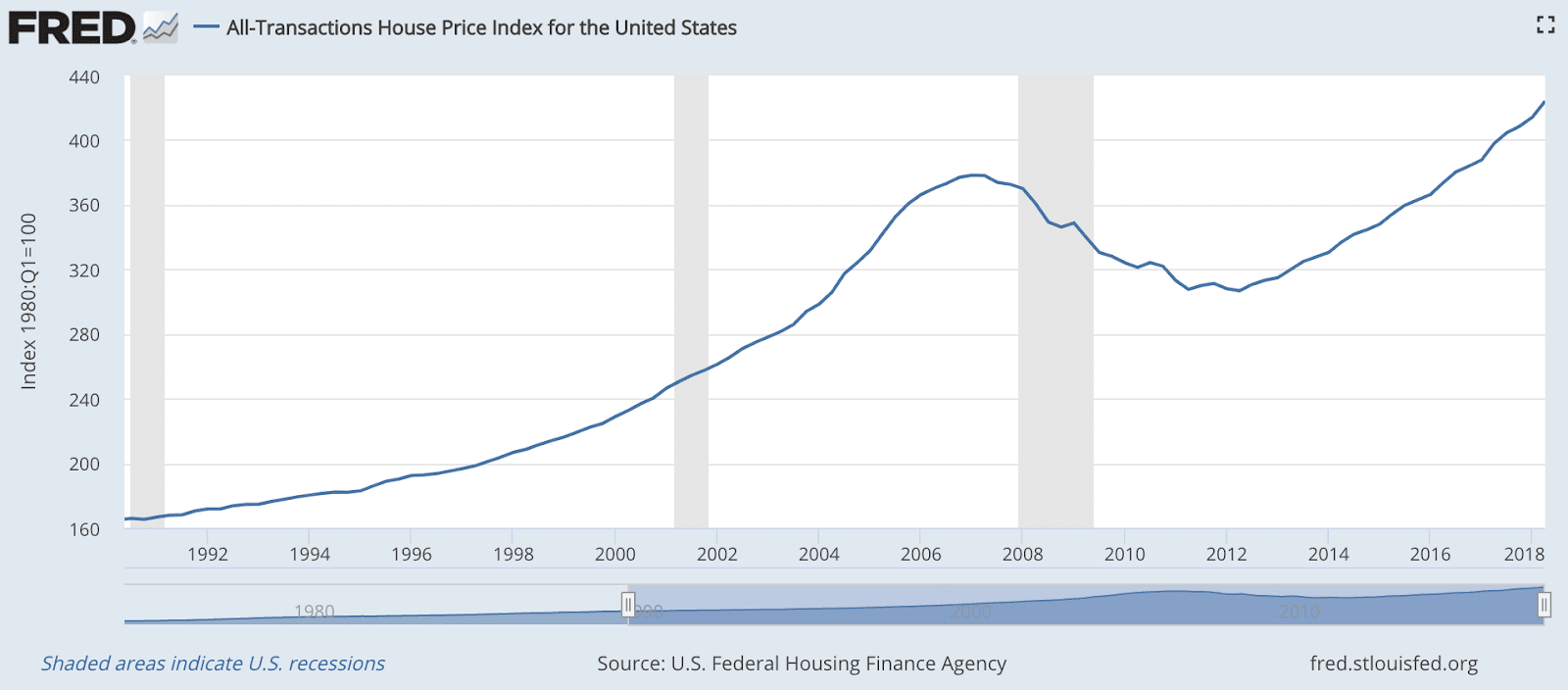

During the notorious 2008 financial crisis and the subsequent housing market crash, home values fell fast. Luckily, as the economy recovered, so did home values—and they’ve recently surpassed peak values set in 2006.

Plus, there’s been significant financial regulatory reform to stave off such a dramatic economic crisis in the future. So, while your home’s value may fluctuate, it’s unlikely to take a dramatic dive.

However, there are signs that home values are leveling off, and may even be falling slightly in some areas. Some economists are even advising that if you’re considering selling your house, you should sell before 2020.

So, if you’re happy with your home’s current market value, and you want to access every last cent of that equity, the only way to do it is to sell it.

Selling the home where you’ve raised your kids and made precious memories is a heart-wrenching decision—but the financial freedom that comes with unloading your now too-big home makes the process easier.

The question is: “What do I do now that I’ve sold my home?”

4. Downsize into a smaller home

Now that the kids have moved out, you can get by with a cozy one- or two-bedroom house. Perhaps you’ll find one in a retirement community, or buy a place closer to your family, or even purchase a property in a warmer, Southern, retirement-friendly state.

Once you’ve sold your larger, more expensive house, you can use the proceeds to make an all-cash purchase of a smaller, more accessible home. With no mortgage to pay, and the excess home equity to use as a nest egg, you’ll have more time and money to enjoy your retirement.

Pro: Downsizing into a more accessible home means aging in place longer

While you may be the picture of health right now, you need to think long-term when choosing your next home.

Because downsizing isn’t just about going smaller, it’s about buying a smaller home that’s outfitted with features that’ll allow you to age in place longer.

For example, bypass any tiny houses that include stairs (two-story or raised foundations). Instead, opt for a ranch-style home so you’ll have fewer issues if mobility ever becomes an issue.

Other senior living features to consider: wheelchair accessibility, showers with built-in seating, and easy-open lever door handles instead of hard-to-turn knobs.

Con: You’ll have to get used to the reduced square footage

Sure, you knew that moving into a smaller home meant paring down your stuff, but you may be shocked by just how much you need to purge.

Not only do you need to cut back on the clutter, but your tiny home may not even have room enough for your existing furniture. Instead of your 8-person dining set, you may only have space for a table for two. Same goes for your massive, sectional sofa and your California King mattress.

Entertaining can be an issue, too. It’s hard to host a formal dinner at a dainty café table. Luckily, there are ways to maximize your small space with creative multi-use furnishings.

Pro: A smaller home helps you cut back on housing costs

Aside from accessibility, one of the key reasons retirees downsize is to cut costs.

In most cases, smaller homes have lower utility costs, lower homeowner’s insurance expenses, and lower property taxes (assuming you’ve stayed within the same neighborhood or moved to an area with equitable cost of living expenses).

If you purchase a property in a 55+ community, many of these expenses may be included in your monthly dues—along with landscaping and exterior maintenance.

Con: Smaller, cheaper homes offer less equity

One simple fact downsizers often overlook is: a house that costs less, is worth less. This means that you’ll have less home equity to access in an emergency situation.

Once you sell, that home equity you spent years accumulating will go to cover closing costs, moving expenses, and the price of the new house. If you use what’s left of your converted-to-cash equity to supplement your retirement income, you’ll slowly be spending away your nest egg.

Plus, downsizing may cost more than you’re anticipating, leaving you less of a nest egg to begin with.

5. Become a renter

Let’s face it—being a homeowner can be a hassle. It takes a lot of work to clean and maintain a 2,000+ square-foot home, not to mention all the yard work.

And when you’re the owner, you’re on the hook if things go wrong, like termites or storm damage to your roof.

When you become a renter, you’re free of that responsibility.

Plus, in some regions, it’s actually cheaper to rent—at least in the short term. It all comes down to running the numbers.

Pro: Home maintenance is no longer your problem

A major reason that many retirees sell their homes to live large off of the proceeds—so that home maintenance becomes someone else’s problem.

Your roof’s leaking? Call your landlord. Grass needs trimming? Call your landlord. Kitchen faucet keeps leaking? Call your landlord.

You get the picture.

And, since you’re no longer tied to a house, if you don’t like where you’re living you can move as soon as your lease is up.

Con: You no longer own an appreciating asset (and rents can rise)

All of those years you spent paying off your mortgage you were investing that money into an asset that you own. And that equity acted as a safety net to cover unexpected expenses, like home repairs and medical care.

When you rent, all of that money goes into someone else’s pocket. Essentially, you’ll be spending down your home’s equity to finance in your twilight years.

And you may run through that money faster than you’d expect.

Experts say that you’ll spend upwards of one-third of your annual income on rent. And rents aren’t locked in like mortgage payments are—so over time, you’ll l wind up spending more than you expect to on housing costs.

So, what is the best way to access home equity in retirement?

Unfortunately, there’s no easy answer to this question. Factors like your retirement income, the condition of your home, and your financial needs all play a role in helping you make this deeply personal decision.

The good news is that, as a homeowner, you’re living in a substantial asset that offers you significant financial security, no matter how you decide to access it.

And if you decide that selling is the right move for you, make sure you hire a real estate agent who’s worked with retirees and can guide you through the next steps with ease.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.