The Case for Buying That Retirement Home Before You Retire

- Published on

- 6-7 min read

-

Christine Bartsch Contributing AuthorClose

Christine Bartsch Contributing Author

Christine Bartsch Contributing AuthorClose

Christine Bartsch Contributing AuthorFormer art and design instructor Christine Bartsch holds an MFA in creative writing from Spalding University. Launching her writing career in 2007, Christine has crafted interior design content for companies including USA Today and Houzz.

Over a third of pre-retirees plan to change residences in their golden years, but what they may not realize is there are a number of benefits to purchasing a retirement house long before you’ve left the workforce.

“Deciding on whether to buy a retirement home before you retire depends on what your goals are, and what your finances look like,” advises Raylene Lewis, a retirement specialist with over 18 years of experience who ranks in the top 5% of agents in College Station, Texas.

“There are a lot of things that you have to think through, but if you’re financially able to purchase your retirement property before you retire, do it.”

Ultimately the decision will be up to you and you can time the purchase as you please—though you’d be wise to review these four reasons that make a strong case for snagging that retirement property sooner rather than later.

1. It’s easier to qualify for a mortgage while you’re still working

Thanks to the Equal Credit Opportunity Act it’s illegal for lenders to deny you for a mortgage simply because you’ve retired, but that doesn’t mean the banks will make it easy.

While lenders can’t discriminate based on your life expectancy, they can and do take your income into account.

“It’s usually easier to qualify for a mortgage while you’re still working,” advises Lewis.

“Your income is higher when you’re pre-retirement, so your debt-to-income ratio is more favorable. If you wait to buy after you retire, you may be limited to a smaller mortgage amount because you’re living off of your retirement savings.”

When you apply for a mortgage after you retire, distributions from retirement accounts, like your 401(k) and IRA, can be counted toward your monthly income totals, but only if you can access these funds without penalty. And even then, lenders can only calculate your expected distribution amount based on 70% of the total value.

If you buy before you retire, you’ll have your pay stubs and W-2s to verify your income, and then your retirement accounts can be counted as assets to determine your mortgage eligibility.

2. You’ll have more spending money to spruce up your retirement property

No matter how hard you look, you’ll never find a house that’s exactly what you want.

Maybe your dream retirement home needs a major renovation, like a kitchen makeover or a roof replacement. Or perhaps you’ve got a handful of smaller projects in mind, like installing chic new light fixtures throughout, or putting up a gazebo out back to create the ultimate retirement relaxation experience.

In short, if you want to turn that house into a home, you’re going to need to make a few tweaks to the property—and that takes money.

If you buy a retirement property before you retire, you have more flexibility and extra cash to do a little bit of remodeling to add your personal touch to the home.

An age-in-place property also needs more than just personal, cosmetic improvements. You may have to invest in accessibility features to accommodate any health and mobility issues you could face down the road.

Having trouble visualizing what your housing needs might be should your health fail?

The Americans with Disabilities Act (ADA) provides extensive guidelines to help you meet accessibility standards.

“I’ve had quite a few clients who remodel their retirement properties to be ADA-compatible, such as installing accessible sinks or adding grab bars for safety,” says Lewis.

Not only will you have more money to invest in your forever home if you buy before you retire—you’ll have your current good health to invest in it, too.

Home repair and renovation expenses add up when you pile labor costs on top of project supplies and materials. If you purchase your forever home before you retire, you’ll be in good enough shape to tackle some of the home improvements yourself.

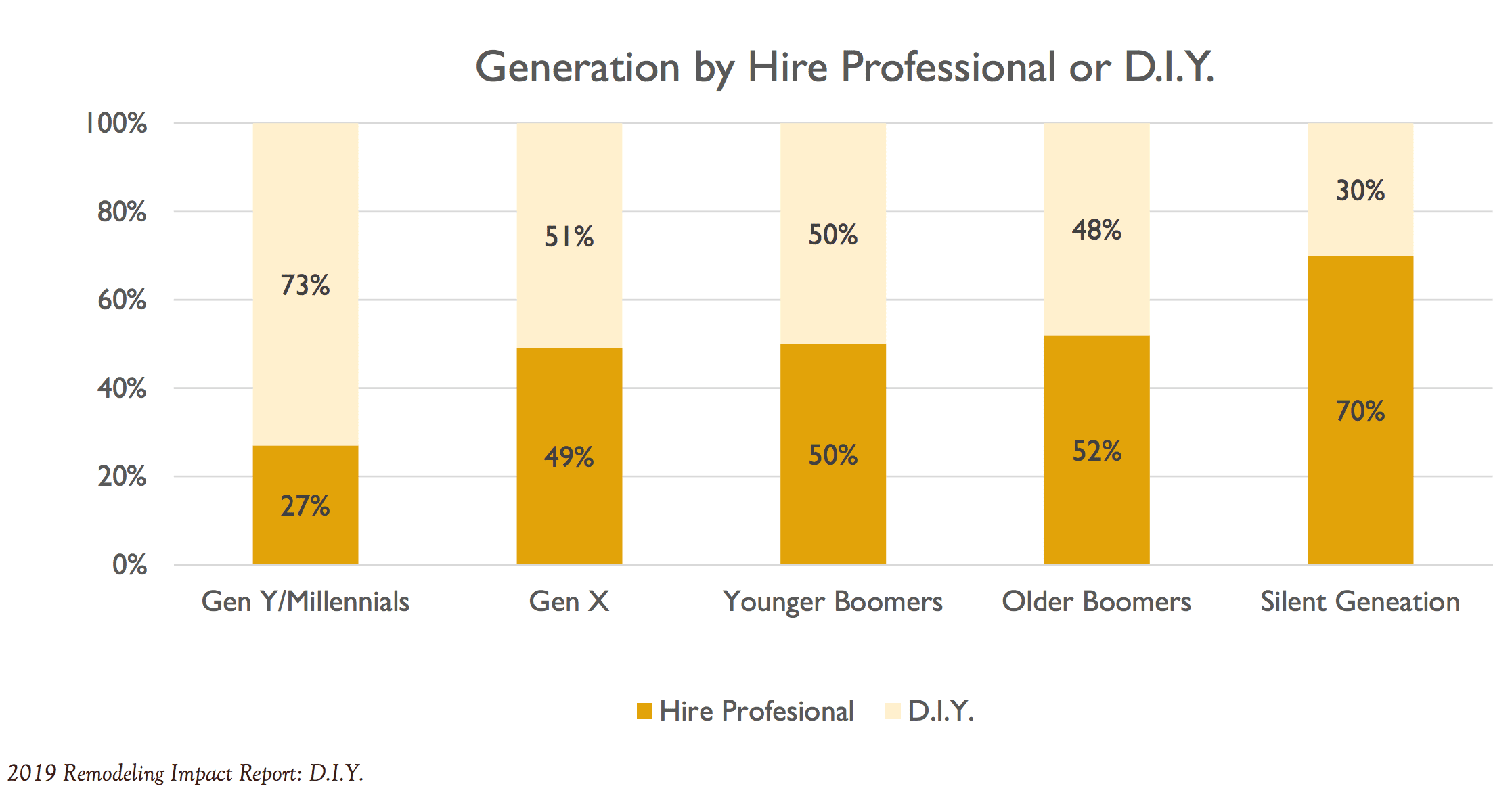

However, the older you get, the less likely you’ll be able to take on home repairs and improvements. Statistics show that 70% of homeowners over age 70 have to hire professionals to make those home repairs.

3. You have greater financial resources to handle unplanned expenses

The longer you live in a house, the better you get to know its creaks, quirks and requirements. You’ll grow to know how soon your home will need a new roof, or a replacement water heater—and you can budget accordingly.

However, pricey problems are known to crop up unexpectedly within the first few years that you own a property. Those high dollar expenses may force you to dip into your retirement savings—and replacing those funds may be difficult if you’re no longer earning a salary.

“There’s always going to be unanticipated expenses whenever you buy a property, even if it’s new construction. It’s easier to handle unanticipated costs that come up when you purchase a property while you’re still working,” says Lewis.

These unforeseen financial burdens can also arise during the sale of your existing home. For example, while most seller closing costs are laid out up front, you could be on the hook to make repairs mandated by your buyer’s lender before they’ll approve the loan.

4. Knowing your housing expenses helps you plan your retirement finances

One of the biggest benefits to buying your retirement home now is that you’ll be locking your monthly mortgage payment and interest rate in place—a smart move to make while interest rates are low.

Knowing the hard number for your housing costs, likely your biggest monthly expense, puts you in a better position to calculate your retirement budget so you’re not stuck with a mortgage payment you can’t afford on a fixed income.

Buying while you’re still receiving a salary also lets you build up equity in your retirement house that provides you with a financial safety net in case any unexpected expenses arise.

Let’s say you’ve still got a year or two until you can access your retirement accounts without penalty. Disaster strikes and you’re now facing a huge medical bill that your accessible savings can’t cover.

Option one is paying the penalty to cover the bill with your retirement savings. Option two is taking out a home equity line of credit (HELOC) on your current home—the one you intended to sell after you retire.

If you do take out a HELOC, that’ll need to be repaid at the time of the sale, tying up that home equity you spent years building up. However, if you already own the home you intend to spend your retirement years in, then you can repay that HELOC in your own time.

Buying sooner rather than later also lets you cash in on your state’s property tax benefits for retirees.

Almost all states have a homestead exemption program that allows qualifying retirees to exempt part of their home’s value from their property tax calculations. A handful of states offer even better benefits.

The assessment freeze program available in ten states limits how high your property’s appraised value can go for taxation purposes. Six states offer a property tax freeze that simply locks your current property taxes in place.

These laws are in place to prevent property taxes from rising too high for retirees to pay with a limited income. So the sooner you own your age-in-place home, the sooner you can take advantage of these programs.

Buying retirement housing? Avoid making these 3 mistakes

Picking the right retirement house to buy while you’re still pre-retirement is even more challenging than buying your first house. Without a workplace to tie you down, your retirement lifestyle housing situation is wide open.

You could downsize to finance world traveling, or relocate to be near family, or move into a 55+ community. While there are many tantalizing options to choose from, you’re also at a greater risk of making the wrong buy.

Take care not to make these mistakes:

1. Don’t get lured by your dream location

Have you painted yourself an idyllic picture of your retirement life? Maybe you see yourself lounging on the porch of a tropical beachside bungalow, or tending the gardens of a quaint little historic farmhouse in the countryside.

If you buy one of these dream homes without ever experiencing the lifestyle it provides, you may find a nightmare waiting for you instead.

“I had a client who wanted to retire on a lot of on acreage out in the country where they could just relax by themselves. But buying that dream property didn’t live up to their expectations,” says Lewis.

“My clients found that they didn’t enjoy paying the massive water bill or spending one full day a week on a riding lawn mower. Plus, they didn’t want to be tied to maintaining all that acreage when they could spend that time traveling.”

2. Don’t cash strap yourself

One major financial danger is buying a place with a monthly mortgage payment that won’t be sustainable once you retire.

Maybe it’s the beautiful kitchen, or the perfect location. Whatever the reason, it’s easy to talk yourself into buying a higher-priced home to retire in if you buy while you’ve got that extra security of a salary flowing in.

That’s why you need to calculate your affordable housing costs before you go house hunting. You can do this by basing your calculations on your projected retirement income, rather than your current employed income.

You need to do this even if you’re buying pre-retirement so that your current income can help you get a better loan. That way you’ll know that you can afford the mortgage payment on a fixed income.

3. Don’t fail to make a priority list

Figuring out where you want to live and how much you can afford to pay for housing after you retire all comes down to creating a list of your priorities.

“You definitely need to figure out what your retirement lifestyle is going to be before you buy your retirement house. Otherwise, you may find that the house you’ve always wanted won’t offer what you need,” says Lewis.

Location and affordability may top the list, but they’re not the only factors to consider. As you create your list, ask yourself questions like these:

- Do I want to relocate closer to family?

- Do I need space to babysit my grandkids?

- Do I want to downsize and travel?

- Do I need extra bedrooms for house-visiting family?

- Do I want to do my own yard work or let an HOA community handle landscaping?

- Do I need special accessibility features, like lower sinks or wheelchair-width hallways?

Of course, sometimes you won’t be able to answer those questions until you actually retire. But if you don’t try to answer them know, you’re more likely to wind up needing to sell the home you intended to retire into.

I’m buying before I retire: Should I sell my current house, too?

Just because you’re buying your forever home doesn’t mean you automatically need to sell your current house. In some cases it’s not even an option, such as if you’re relocating to a different city or state after you retire.

If you do intend to hang on to both houses, you first need to figure out if your retirement house can be considered a second home or if it needs to be treated as an investment property.

“Some people will buy their retirement home and then lease it out until they’re ready to move into it. This can be a very successful option, but it can also be frustrating if you have trouble dealing with your tenants,” advises Lewis.

“On the other hand, if you can declare your retirement home as a second home, you can get a lower interest rate than if you declared it as an income property.”

The IRS has strict regulations for second home properties if you want to receive tax benefits like deducting the mortgage interest and property taxes. For example, the second home needs to be over 50 miles away from your current home, and your ability to rent it out is limited.

Selling your current house to buy a retirement home offers up several benefits worth considering:

- You won’t need to juggle two mortgages

- You’ll be moving into your retirement home while you’re still young and able

- You can use the proceeds of your home sale to fund the purchase of your retirement property

Using the proceeds from your current home sale to fund the purchase of your retirement house is one of the strongest arguments for selling.

Instead of holding on to two houses, that built-up equity can grant you access to the benefits of making a large down payment. By putting down 20% or more on the new house, you can:

- Significantly lower your monthly payment for the lifetime of the loan

- Avoid paying for private mortgage insurance

- Pay less in interest for the lifetime of the loan

- Have more lenders eager to offer you the lowest interest rates

The benefits of buying your retirement house now

Buying your retirement home when you’re still several years out from leaving the workforce seems counterintuitive. But when you think about the advantages, like securing a mortgage while you’re still fully employed, having the extra income to make renovations, and boosting your savings by turning your second home into an investment property, you may find that it’s a financial strategy well worth considering.

Header Image Source: (StacieStauffSmith Photos/ Shutterstock)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.