Your Ultimate Guide to Buying a Home in Connecticut in 14 Steps

- Published on

- 18-19 min read

-

Jody Ellis, Contributing AuthorClose

Jody Ellis Contributing Author

Jody Ellis, Contributing AuthorClose

Jody Ellis Contributing AuthorJody Ellis is a freelance writer with more than 15 years of experience in the writing industry. Her work includes copywriting and content marketing for real estate professionals, stories covering real estate trends and housing markets, and varied articles on decor and design. In addition to buying and selling several homes herself, she's also owned and managed rental properties, and previously worked in mortgage lending.

-

Fran Metz, Contributing EditorClose

Fran Metz Contributing Editor

Fran Metz is a freelance content writer, editor, blogger and traveler based in Las Vegas, Nevada. She has seven years of experience in print journalism, working at newspapers from coast to coast. She has a BA in Mass Communications from Fort Lewis College in Durango, Colorado, and lived in Arvada for 15 years, where she gained her experience with the ever-changing real estate market. In her free time, she enjoys 4-wheeling, fishing, and creating digital art.

If you’re considering buying a home in Connecticut, you’re in for a treat. Despite being the third smallest state, Connecticut offers a rich blend of history, culture, and a high quality of life. Residents enjoy the state’s four distinct seasons, stunning coastal shores, mountain ranges, and a mix of urban and rural living. Its proximity to New York makes it a popular choice for commuters looking for a more affordable housing option while still being close enough for weekend trips.

For those planning to purchase a home in Connecticut, we’ve teamed up with top agent David Landau, who handles 68% more single-family homes than the average agent in Newtown, Connecticut. This ultimate guide covers 14 steps to follow, including everything from saving for your down payment to choosing the right loan programs, as well as tips for finding a great agent.

Find a Buyer's Agent in Connecticut

Looking to buy your dream home in the Constitution state? Use HomeLight’s agent matching tool to find an agent in less than two minutes.

Steps to buying a home in Connecticut

While the median price of a home in Connecticut is $432,611, housing prices can vary greatly, and those seeking to buy in some of the more sought-after areas might find themselves paying well over $1 million for their dream home. And with so many options, determining which county is best, what you can afford, and how to go about the process can seem overwhelming.

So let’s dive straight into the steps of buying a house in Connecticut:

1. Assess your readiness

Before beginning your home search in Connecticut, take a moment to consider whether you’re truly ready to make the leap into homeownership. Reflect on how long you intend to stay in the area, whether your job situation is stable, and if you’ve saved not only for a down payment but also for additional costs. There are extra expenses like closing costs, property taxes, and ongoing maintenance to consider.

Closing costs: When buying a home in Connecticut, understanding closing costs is key to budgeting effectively. With the state’s median home price at about $432,000, buyers should expect closing costs ranging from 2% to 5% of the purchase price. This means you could be looking at anywhere between $8,640 and $21,600 in fees, depending on the specifics of your transaction. These costs typically include lender fees, title insurance, appraisal costs, and prepaid items like property taxes and homeowners insurance.

Sellers in Connecticut face losing expenses, averaging between 6% and 10% of the home’s sale price. For a property selling at the median price of $432,000, sellers could pay anywhere from $25,920 to $43,200. The most significant cost for sellers is usually the real estate agent’s commission, which traditionally has been 6%, but may now be closer to 3% following recent Realtor fee rule changes. Transfer taxes and attorney fees also add a substantial amount.

Overall, these percentages highlight the importance of preparing for additional financial commitments beyond the down payment. Buyers and sellers alike should plan carefully and consider negotiating some costs or exploring local programs that assist with closing expenses to make the transaction more manageable.

Credit score: During this time, review your credit score and determine if it’s considered excellent, good, fair, or poor. Typically, the higher your credit score, the lower your interest rate will be, which saves you money over the life of the loan. You may want to pay off any collection accounts, dispute errors on your credit report, and pay down your credit card balances before you start shopping for a home.

According to Landau, these are all things that should be in order before you start the house-hunting process, and buyers should always consider how much house they can really afford. “I talk to my clients about the importance of working within their budget, and not ending up house poor,” he says.

2. Saving for your down payment

The amount you need to save for a home purchase depends on several key factors, such as the home’s price, closing costs, and additional expenses like attorney fees (which we’ll cover in more detail shortly). Many lenders also prefer buyers to maintain a financial cushion after the purchase to ensure you’re not draining your savings entirely. This way, you’ll have funds set aside for any unexpected costs or emergencies that may arise after you become a homeowner.

Different loan programs come with varying down payment requirements, and thankfully, you don’t always need to put 20% down to buy a home. Data from the 2024 Profile of Home Buyers and Sellers released by the National Association of Realtors (NAR), shows that first-time homebuyers typically put down a median of 9%, with repeat buyers contributing about 23%. The overall median down payment across all buyers was 18%. This highlights how down payment expectations can vary widely depending on the buyer’s experience and financial circumstances.

Some buyers also may qualify for one of Connecticut’s down payment assistance programs, which, based on certain criteria, can cover part or all of your down payment. These programs include:

Connecticut Housing Finance Authority (CHFA): The Connecticut Housing Finance Authority offers down payment assistance to first-time buyers in the form of a second mortgage called a DAP loan. Both the down payment and closing costs can be financed up to $15,000, with an interest rate equal to either the first mortgage interest rate in effect or 5% (5.10%-5.50% APR), whichever is less. Homebuyers must already be prequalified through a CHFA approved lender, and are required to attend a homebuyer education class prior to closing.

SmartMove Connecticut: Connecticut’s Housing Development Fund (HDF) SmartMove program allows first-time homebuyers the opportunity to purchase a home with as little as 1% down, by way of a low interest (3%) second mortgage for up to 25% of the home’s purchase price. To qualify, buyers cannot have owned a home in the past three years, and must meet certain income limits, which vary between counties within the state. Buyers must also prequalify for their first mortgage through an HDF approved lender.

HDF Live Where You Work: To help families reduce commute costs and improve their work-life balance, The Housing Development Fund created the “Live Where You Work” program, which allows first-time homebuyers to purchase a house in the same town where they work. Qualified buyers can get up to $25,000 in down payment assistance, which is repaid as a zero-interest second mortgage. Eligibility requirements include income levels below 80% of the area’s AMI (area median income), and buyers cannot have owned a home in the past three years.

3. Get preapproved for a mortgage

Getting preapproved for a mortgage will help you determine how much you can afford, which will then inform your home search. It’s always smart to shop around for the best rates and terms, so be sure to research a few lenders during this process.

Landau recommends that buyers consider local lenders first when shopping for a mortgage. “We always suggest getting preapproved with a local lender who knows the area, especially if you’re competing against other offers,” he says. “With the current shifting market, financing is heavily looked at, and there’s a preference for a local lender that understands the process here.”

You can also ask family, friends, your buyer’s agent, and attorneys for mortgage lender recommendations. When choosing a mortgage lender, ask for a detailed cost breakdown, review the terms you are being offered, and compare loan types.

According to the US Consumer Financial Protection Bureau (CFPB), there are three general categories of mortgage:

Conventional

There are two types of conventional loans — conforming and non-conforming. A conforming conventional loan will meet or exceed the guidelines set by Fannie Mae and Freddie Mac, which are government-sponsored enterprises (GSEs) that purchase conventional loans. Guidelines for a non-conforming loan will vary more widely depending on the lender.

Typical requirements for a conventional loan may include:

- Minimum credit score of at least 620

- Maximum debt-to-income (DTI) ratio of 43%

- Minimum down payment of 5%, though some programs allow for a 3% down payment

- Maximum loan amount of $766,550 in most counties; as much as $1,149,825 in high-cost counties

- Typically requires private mortgage insurance (PMI) if the down payment is less than 20%

Non-conforming loans are designed for borrowers whose financial profiles don’t meet the guidelines set by Fannie Mae and Freddie Mac. These loans can’t be purchased by these entities. A common type of non-conforming loan is a jumbo loan, which is for loan amounts that exceed the maximum limits established by Fannie Mae and Freddie Mac. Since jumbo loans involve larger amounts, they often come with stricter requirements, like higher credit scores and larger down payments, to compensate for the increased risk.

FHA loans

An FHA loan is insured by the Federal Housing Administration and can be obtained through FHA-approved lenders. One unique aspect of FHA loans is that borrowers can use down payment assistance programs for the entire down payment. Here are the typical qualifications for an FHA loan:

- Minimum credit score:

- A score of 580 allows for a minimum down payment of 3.5%.

- A score between 500 and 579 requires a higher down payment of 10%.

- Mortgage insurance premiums (MIP):

- Borrowers must pay an upfront MIP and a monthly MIP for the life of the loan.

- Debt-to-income (DTI) ratio: Typically must be 43% or lower.

- Primary residence: The property must be the borrower’s primary residence.

- Loan limits for FHA loans in Connecticut vary significantly depending on the county. In high-cost areas like Fairfield County, the maximum loan amount for a single-family home reaches $1,149,825. In contrast, in New Haven-Milford County, the loan limit is lower, set at $515,750. These differences reflect regional variations in home prices and are designed to align with the local real estate market.

Special loan programs

Veterans Affairs (VA) Loans: Designed for veterans, active service members, and eligible surviving spouses, VA loans are backed by the Department of Veterans Affairs and offer the advantage of 0% down payments for those who qualify. While lender-specific requirements may vary, VA-backed loans are notable for not having a universal cap on debt-to-income (DTI) ratios. However, many lenders prefer to see a DTI of about 41% or may allow higher ratios based on compensating factors.

USDA Loans: Backed by the Department of Agriculture, USDA loans provide an opportunity for lower-income borrowers to purchase homes in designated “rural areas” with no down payment. To check if a property is eligible, you can use the USDA’s interactive eligibility map. These loans require that the home be used as a primary residence and typically have income limitations and specific DTI guidelines, though exceptions may be made depending on financial factors. These loans also offer 0% down for qualified borrowers.

4. Research the market and choose your ideal location

Once you have a clearer picture of what’s needed to buy a home and understand the down payment options, the next step is pinpointing where you want to put down roots. Think about whether you want to be close to family and friends or if starting fresh in a different city excites you. Would you prefer the calming waves of the coast, or does the charm of a rural area sound more appealing? Factor in practical considerations like your work commute, the average home prices in your preferred neighborhoods, and the local amenities. Take time to explore the lifestyle each area offers, from recreational activities to community vibe, so you can find a place that truly feels like home.

Some great places to consider when buying a house in Connecticut include:

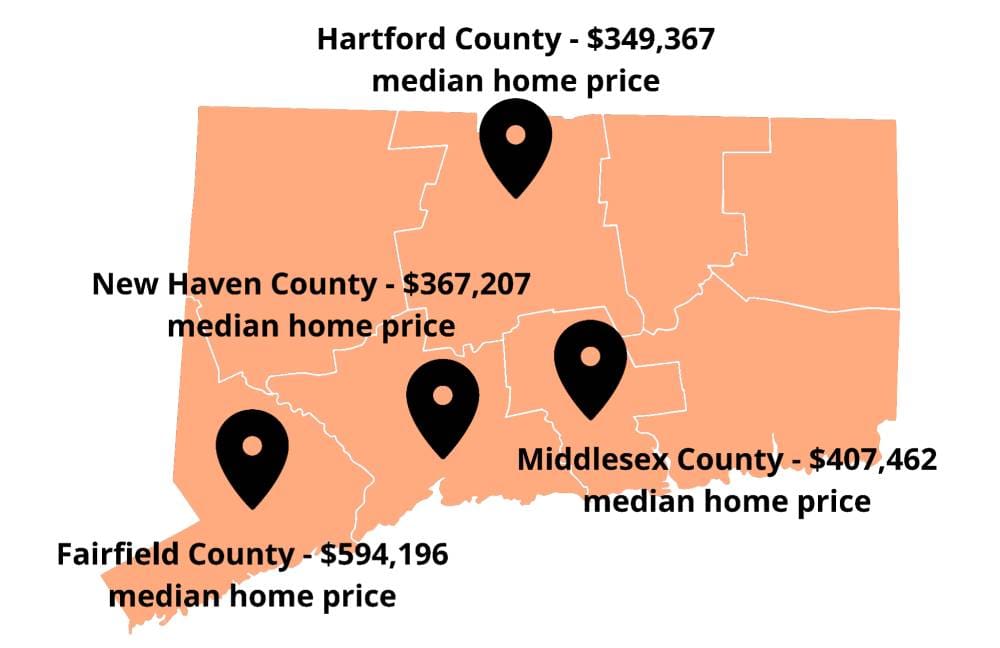

Fairfield County: With its close proximity to New York City (60 to 70 miles away), Fairfield County is often the first choice for young professionals in Connecticut. The median home price here is c urrently $594,196 as of October 2024, and it’s been ranked as the best county to live in in the state. Residents of Fairfield County not only have easy access to the bright lights of New York, but also top schools, plenty of shops and restaurants, and a relaxed, suburban vibe.

Hartford County: Hartford County includes the cities of Glastonbury, West Hartford, and South Windsor, which are the Connecticut Chamber of Commerce’s top picks for best cities to live in Connecticut. All of these towns are rich in history, have some of the state’s best school districts, and plenty of options for recreational activities. Hartford County is also home to Connecticut’s capital city of Hartford, where residents enjoy an abundance of museums, performing arts, and family-friendly parks. The median home price in the county as of October 2024 was $349,367, although you might find higher prices in cities such as Glastonbury or West Hartford.

New Haven County: New Haven County is Connecticut’s third most populous, not to mention one of the most popular places to live! The median home price here is $367,207, and its location on the Long Island Sound makes it very sought after. New Haven County is home to Yale University, and living here not only provides access to arts and culture, but also outdoor fun that includes hiking, biking, and water sports.

Middlesex County: Middlesex County gets high marks for its school system, earning a top four ranking for “Counties with the Best Public Schools in Connecticut.” The median home price is $407,462, and major towns within the county include Cromwell, a suburb of nearby Hartford, and Middletown, which sits on the Connecticut River and is home to Wesleyan University.

5. Find a local Connecticut agent

Real estate agents love when clients kick off their home search with a mortgage preapproval in hand. It signals that you’re serious, ready to make offers, and have a clear understanding of your budget. When choosing an agent, look for someone experienced and well-versed in the neighborhoods you’re interested in, especially someone who specializes in representing buyers. A knowledgeable local expert can make all the difference in finding the perfect home and navigating the market efficiently.

Your buyer’s agent will assist you in setting up viewings, share insights about neighborhood trends, negotiate the best deal on your behalf, and connect you with essential professionals like title companies, insurance agents, and home inspectors. Real estate agents are experts in the homebuying process and provide invaluable guidance to keep everything on track, ensuring a smooth path to closing.

6. Start shopping for homes in Connecticut

Once you’re preapproved for your loan and line up a knowledgeable agent to work with, the fun part of the house-hunting process really begins! Depending on your budget and location preferences, Connecticut home styles range from historic Saltbox and Colonial houses, beach bungalows, modern ranch homes, or townhomes, commonly called “row houses.”

The summer months often are the busiest for Connecticut’s housing market, and Landau says house hunting in winter means less competition and a higher chance of being able to negotiate. “Sellers who have their property listed at this time are motivated and more likely to deal,” he says.

Landau says he always cautions buyers to be aware of potentially big-ticket repair items, like roofs or HVAC replacement, when looking at homes. It’s easy to get caught up when you love a location or floor plan, but you also don’t want to get into a house and then end up with a bunch of expensive repairs right after closing. “Especially for first-time buyers, who might not be aware of these kinds of things,” Landau says, “We don’t want to get them into a house just to find out they can’t afford to live in it.”

7. Make a strong offer

Creating a strong, competitive offer with your agent can feel overwhelming, but it’s important in today’s market. In 2024’s competitive landscape, cash offers are often the most attractive to sellers, especially when multiple bids are on the table. However, while it’s generally not advisable to waive all contingencies, you can stay competitive by limiting them to key ones, like the inspection and financing contingencies.

Get strategic and think outside the box. You could increase your earnest money deposit, propose a quicker closing timeline, or even offer the seller a rent-back arrangement for a specific period. These creative touches can help your offer stand out from the rest.

Connecticut’s real estate market continues to be dynamic, with limited housing inventory keeping prices elevated. Competition remains significant, especially for highly desirable properties. Buyers should expect to present competitive offers, and cash offers may hold an advantage. However, there’s also room for negotiation, particularly with properties that are less sought-after or need renovation.

Properties in prime areas may still receive multiple offers, but overpricing has become more noticeable. As a result, having a skilled real estate agent is more valuable than ever. They can help you navigate fluctuating market trends, negotiate effectively, and make well-informed decisions. “Prices have leveled off,” Landau says, adding that finding a balance between standing out and protecting your interests is key, which highlights the importance of an experienced, market-savvy agent.

When making an offer on a home in Connecticut, several key components need to be included:

- Purchase price: This is the amount you are willing to pay for the property. Your offer should be competitive based on current market conditions and the home’s value.

- Closing date: The proposed date on which you’d like to close the deal. Sellers may prefer a quicker closing, but flexibility can make your offer more appealing, especially if you’re able to accommodate the seller’s timeline.

- Earnest money deposit: This is the deposit you put down to show your commitment to the sale. It is usually 1% to 2% of the offer price, but can vary. The higher the deposit, the stronger the offer may seem.

- Contingencies: These are conditions that must be met for the sale to proceed. Common contingencies include:

- Financing contingency: This ensures that you can secure a mortgage loan.

- Home inspection contingency: Allows you to back out or renegotiate based on the results of the inspection.

- Appraisal contingency: Protects you if the home appraisal comes in lower than your offer.

- Closing cost stipulations: This includes specifying who will cover closing costs (the buyer or the seller). Buyers sometimes ask for seller credits to cover closing costs, particularly if the home price is on the higher end.

- Home warranty: Some buyers request a home warranty to cover the cost of repairs for appliances or major systems in the home for the first year after purchase.

- Personal property: Buyers can negotiate for additional personal property to be included in the sale, such as appliances, furniture, or fixtures.

Each component should be carefully considered based on your goals and the seller’s circumstances, especially in today’s more balanced market. A well-structured offer will increase your chances of securing the home you want.

8. Send your earnest money deposit

Your earnest money deposit, also known as a “good faith deposit,” is an amount of money you agree to pay the seller to indicate that you are serious about purchasing the home. This is usually between 1% and 3% of the purchase price. However, a higher deposit can be more attractive to sellers and make your offer stand out in competitive markets.

Whether or not you get your earnest money back when backing out of a home purchase depends on the terms outlined in your contract. Typically, if you back out for reasons that are not covered by contingencies in the agreement, you may forfeit the earnest deposit. However, if you back out due to contingencies like a failed home inspection or appraisal, or if financing falls through, you could likely get your earnest money refunded.

It’s essential to carefully review the contract with your real estate agent and attorney to understand the specific conditions under which your earnest deposit could be refunded or lost. A clear understanding of these terms can help prevent surprises if you decide not to move forward with the purchase.

9. Order a title search

It’s advisable to order a title search as soon as possible after your offer is accepted. While you can technically order it at any point in the process, it may take a couple of weeks to receive the results, especially if the title company is experiencing delays or a heavy workload. The title search is crucial for identifying any legal issues with the property, such as liens or disputes over ownership, and it’s better to uncover these early.

Who chooses the title company can vary depending on the state or county, but in many cases, it’s the buyer’s responsibility. If you’re unsure, your real estate agent or mortgage lender typically can recommend a reliable title company. They can guide you to a company that suits your needs and ensure the process runs smoothly.

The title company will issue a preliminary title report that will be reviewed by all parties, including your lender, and will include items such as property tax information, easements, CC&Rs, deed restrictions, liens, and any judgments against the title of the home. Any liens, encumbrances, or judgments against the property will need to be removed before the buyer can close on the property.

Connecticut can sometimes have unique title issues that you might not find in other states, especially when it comes to older properties. “Some of these properties have been here since the 1700’s,” Landau says. “Sometimes properties changed title a long time ago and it wasn’t documented. There were also no land surveys back then, so property line issues can be another common problem.” Landau says these are usually minor and easily resolved, but it is something buyers in Connecticut should consider when looking at homes.

10. Shop for homeowners and specialty hazard insurances

Homeowners insurance is always recommended and it is almost always required if you’re financing your home with a mortgage. The average yearly cost of homeowners insurance in Connecticut is $2,165 per year.

Landau adds that in some regions, it’s common for lenders to require additional specialty insurance for flooding. “Connecticut has a lot of coastal areas, as well as many lakes and rivers,” he says. If you buy a house that sits in a flood zone, it’s likely you’ll be required to get that extra coverage, which averages about $1,500 a year.

11. Order inspections and appraisal

When applying for a mortgage, your lender typically will order the appraisal, which you’ll be responsible for paying. The appraisal is essential for confirming the property’s value and ensuring it meets the lender’s requirements.You are also responsible for arranging and covering the cost of your own inspections, such as a home inspection. Your buyer’s agent can help by recommending licensed professionals for these services.

The home inspection will be scheduled directly by the inspector, and depending on the size of the property, it may take a few hours. Having a thorough inspection done helps identify potential issues with the home before finalizing the purchase, and can give you leverage for negotiations or make you aware of repairs that may be needed.

Some common issues in homes in Connecticut that merit a separate, more specialized inspection, include:

Well and septic: In Connecticut, many homes, especially those in more rural areas, rely on well water and septic systems. If either of these systems hasn’t been properly maintained, it could lead to serious issues, such as leaks, contamination, or other harmful problems. To ensure that both the well and septic systems are in good condition, buyers should schedule separate inspections for each. A well inspection will verify that the water is safe for consumption and free of contaminants, while a septic inspection ensures the system is functioning properly and won’t pose future issues. Ensuring these systems are in good shape is essential for both the safety and value of the property.

Radon gas: According to Landau, many homes in Connecticut may have radon gas, a naturally occurring radioactive gas that can seep into homes through cracks in the foundation. While radon isn’t always a significant issue, it can pose health risks if levels are high. Therefore, it’s highly recommended that buyers arrange for a separate radon inspection to ensure the air quality is safe. If elevated levels are found, radon mitigation systems can often be installed to reduce the concentration of the gas. Addressing radon concerns before moving in helps protect the health and well-being of you and your family, and it’s better to handle the issue early rather than after the purchase is final.

Until recently, it was common for sellers to refuse to do any repairs, but as the market has softened, that has changed. You can still negotiate for repairs, but I do recommend sticking to health and safety issues in order to keep things moving forward.

David Landau Real Estate AgentCloseDavid Landau Real Estate Agent at RE/MAX Right Choice

David Landau Real Estate AgentCloseDavid Landau Real Estate Agent at RE/MAX Right Choice

- Years of Experience 13

- Transactions 289

- Average Price Point $355k

- Single Family Homes 215

12. Negotiate repairs

Remember, almost everything is negotiable when buying a home, including issues that arise from inspections. If your inspection report reveals significant problems, such as costly repairs, it’s time to reassess and negotiate with the seller. Your buyer’s agent will be your ally in this process, helping you decide the best course of action.

For instance, if you discover a leaky roof or other major issues, you’ll need to decide whether you’d prefer the seller to make repairs before closing, or if you’d rather receive a credit for repairs so you can handle them yourself.

Focus on major issues that require immediate attention, such as structural repairs, electrical work, or plumbing fixes, and try not to get bogged down in minor cosmetic concerns. Home inspectors are thorough, and while they may find a lot of small issues, negotiating on the big-ticket repairs will help ensure you’re not burdened with substantial costs after the purchase.

“Until recently, it was common for sellers to refuse to do any repairs, but as the market has softened, that has changed,” Landau says. “You can still negotiate for repairs, but I do recommend sticking to health and safety issues in order to keep things moving forward.”

13. Final walkthrough

This is to verify that agreed-upon repairs have been completed and the condition of the home is satisfactory. The final walkthrough is usually done a day or two before the closing date.

With the help of your agent, check that all plumbing, electrical, and HVAC units are on and working. If personal items such as the dining room chandelier and the washer and dryer were included in the contract, make sure they’re still in the house.

It’s important for buyers to have their agent present during the final walkthrough, along with a copy of the repair addendum from the purchase agreement. Your agent can help ensure that all repairs are completed as agreed and keep you focused on verifying the details. Having the repair list handy will also make it easier to ensure nothing is overlooked before closing.

If you find that the necessary repairs were not made, or that there were damages left behind by the seller, notify your agent immediately so they can rectify the situation before closing.

14. Closing time!

In Connecticut, it typically takes about 75 days to sell a home on the market using an agent. That includes an average of 31 days on the market plus the typical 44 days a buyer needs to close on a purchase loan. “Because most buyers still finance their home purchase, we have to order appraisals, get inspections, negotiate and complete any repairs, all of which can take at least 30 days,” Landau says.

Connecticut is an “attorney state,” which means that a real estate attorney is required to handle the closing process, as opposed to a title company. This process is common in several states and is designed to ensure that buyers fully understand the legal aspects of their transaction. It may feel like an extra step, but many buyers appreciate the added assurance that comes with legal oversight. After closing, it typically takes a day or two for the title to be recorded, and once that’s complete, you’ll receive the keys to your new home.

Buying a home in Connecticut’s still-competitive market can feel a little challenging, which is why pairing with an agent who knows the best areas to live, best times to buy, and the best ways to navigate your purchase is so important. They’ll be able to assist you in finding the perfect home, from the moment you decide to buy to holding those keys in your hand and knowing you’re officially a Connecticut homeowner!

Writer Madeline Sheen contributed to this post.

Header Image Source: (Juliette Dickens / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.