From Charlotte to the Outer Banks: Here is How to Buy a House in North Carolina

- Published on

- 18-19 min read

-

Syndie Eardly, Contributing AuthorClose

Syndie Eardly Contributing Author

Syndie Eardly, Contributing AuthorClose

Syndie Eardly Contributing AuthorSyndie Eardly is a veteran journalist and legal reporter with more than 20 years’ experience, writing for the real estate, mortgage and title insurance industries. She has helped launch several online publications, including DoddFrankUpdate.com, which was launched after the Great Recession to cover the many legislative efforts that followed. Syndie resides in Cleveland, Ohio, where she enjoys the lively restaurant scene, spending meditative time on the beautiful shores of Lake Erie, and hiking in the Emerald Necklace and Cuyahoga Valley National Park.

-

Madeline Sheen, Contributing AuthorClose

Madeline Sheen Contributing Author

Madeline Sheen, Contributing AuthorClose

Madeline Sheen Contributing AuthorMadeline Sheen is a passionate writer and editor with experience in real estate, personal finance, and mortgage content. Along with serving as an associate editor for HomeLight, she’s worked in the mortgage industry since 2019 and holds a BA in Communications from California State University, Monterey Bay.

If you are considering a home purchase in North Carolina, you are in luck. This beautiful southern state offers a wealth of diverse communities to satisfy every possible personal preference.

Whether you are building a career in the heart of the state’s business mecca, seeking the quiet of a mountain town, or relishing the excitement of the coastal region, North Carolina measures up well in every aspect of homeownership with a moderate cost of living, reasonable tax rate, and wide variety of housing styles and prices.

To learn the best way to approach homebuying in North Carolina, we spoke with top real estate agent Mechelle Kuld, who completes 13% more sales than the average agent in Salisbury, North Carolina. Kuld, who has successfully represented homebuyers and sellers in more than 200 transactions in the heart of the state, says there are several logical steps you can take to successfully acquire a home in her state.

Let’s dive into the steps of buying a house in North Carolina:

1. Assess your readiness

Before you start looking for homes in North Carolina, you want to determine if you’re ready to purchase one. Consider factors such as how long you plan to be in the area, if you have steady employment, and if you have enough money saved for not just the down payment, but for closing costs, maintenance, property taxes, and more. Homebuyers in North Carolina pay $2,766 on average in closing costs when purchasing a home.

During this time, review your credit score and determine if it’s considered excellent, good, fair, or poor. Typically, the higher your credit score, the lower your interest rate will be, which saves you money over the life of the loan. You may want to pay off any collection’s accounts, dispute errors on your credit report, and pay down your credit card balances before you start shopping for a home.

Kuld notes that with mortgage interest rates creeping up in recent months, buyers have to be more focused than ever on the health of their credit to make sure they are able to meet the more stringent lending standards they will face.

2. Saving for your down payment

The median home price in North Carolina is $343,370, as of August 2022. So, expect to spend somewhere around that number depending on what part of the state you’re purchasing in, the home’s age and condition, and the size of the property, among other factors.

Different loan programs will require different down payment amounts, but you do not always need to put 20% down when buying a home. A survey completed by the National Association of Realtors found that first-time homebuyers put just 7% down on average in 2021.

Kuld says down payment requirements vary by loan program, but notes that North Carolina has great down payment assistance programs through the North Carolina Housing Finance Agency, which homebuyers should check out early in the process.

Here are a few of the programs they offer:

- The NC Home Advantage Mortgage offers down payment assistance up to 3% of the loan amount that can help first-time and as well as buyers looking to sell and buy up to get into a new home.

- NC 1st Home Advantage Down Payment gives eligible first-time buyers and military veterans $8,000 in down payment help, which may provide a better option than the NC Home Advantage Mortgage.

- Buyers may also qualify for the NC Home Advantage Tax Credit, which can save them up to $2,000 in federal taxes each year, but buyers must be approved prior to their home purchase.

- There are also Community Home Buying Programs, where the NCHFA works with local nonprofits and government agencies through community loan pools and self-help loan pools to offer down payment funds as well as reduced interest rates to buyers who qualify.

3. Get preapproved for a mortgage

Getting preapproved for a mortgage will help you determine how much you can afford, which will then inform your home search. It’s always smart to shop around for the best rates and terms, so be sure to research a few different lenders during this process.

You can also ask family, friends, your buyer’s agent, and attorneys for mortgage lender recommendations. When choosing a mortgage lender, ask for a detailed cost breakdown, review the terms you are being offered, and compare loan types.

According to the US Consumer Financial Protection Bureau (CFPB), there are three general categories of mortgage:

Conventional

There are two types of conventional loans — conforming and non-conforming. A conforming conventional loan will meet or exceed the guidelines set by Fannie Mae and Freddie Mac which are government-sponsored enterprises (GSEs) that purchase conventional loans. Guidelines for a non-conforming loan will vary more widely depending on the lender.

Typical requirements for a conventional loan may include:

- Minimum credit score of at least 620

- Maximum debt-to-income (DTI) ratio of 43%

- Minimum down payment of 5%, though some programs allow for a 3% down payment

- Maximum loan amount of $647,200 in most counties; $970,800 in high-cost counties

- Typically requires private mortgage insurance (PMI) if the down payment is less than 20%

Non-conforming loans are for borrowers who do not fit into the guidelines set by Fannie and Freddie and are not eligible to be purchased by them — jumbo loans are an example of this because they offer loan amounts above the limits set by Fannie and Freddie.

FHA loans

An FHA loan is insured by the Federal Housing Administration and available from FHA-approved lenders. An FHA loan is unique in that borrowers are able to use a down payment assistance program for the entire down payment. Requirements to qualify for an FHA loan may include:

- Minimum credit score dependent on down payment amount:

- 580 = 3.5% down payment

- 500-579 = 10% down payment

- An upfront mortgage insurance premium

- Mortgage insurance premium (MIP) paid monthly for the life of the loan

- DTI of 43% or lower

- Must be borrower’s primary residence

Similar to conventional conforming loans in this way, FHA loans have loan limits that vary from county to county. For example, in Mecklenburg County, North Carolina the maximum loan amount is $420,680 for a single unit home.

Special programs

VA loans: For veterans, service members, and surviving spouses. Loans backed by the VA offer 0% down payments for those who qualify. Different lenders will have different requirements; however, VA-backed loans do not have a universal maximum DTI requirement.

USDA loans: These loans are backed by the United States Department of Agriculture and are for lower income borrowers in “rural areas.” To determine if the area you are purchasing in is eligible for a USDA home loan, use this eligibility map. These loans also offer 0% down for qualified borrowers.

4. Research the market and determine where you would like to buy

Now that you know more about preparing to purchase a house and down payments, it’s time to decide where you want to live. Do you want to live near family and friends, start over in a new city, live on the coast, or in a more rural area? Consider work commute times, average house prices, and things to do in each area that you’re thinking about living in.

Some wonderful places to consider when buying a house in North Carolina include:

Western Mountain Towns

The charming mountain communities at the western end of North Carolina, such as Asheville and Boone, offer unique community amenities in a small-town atmosphere.

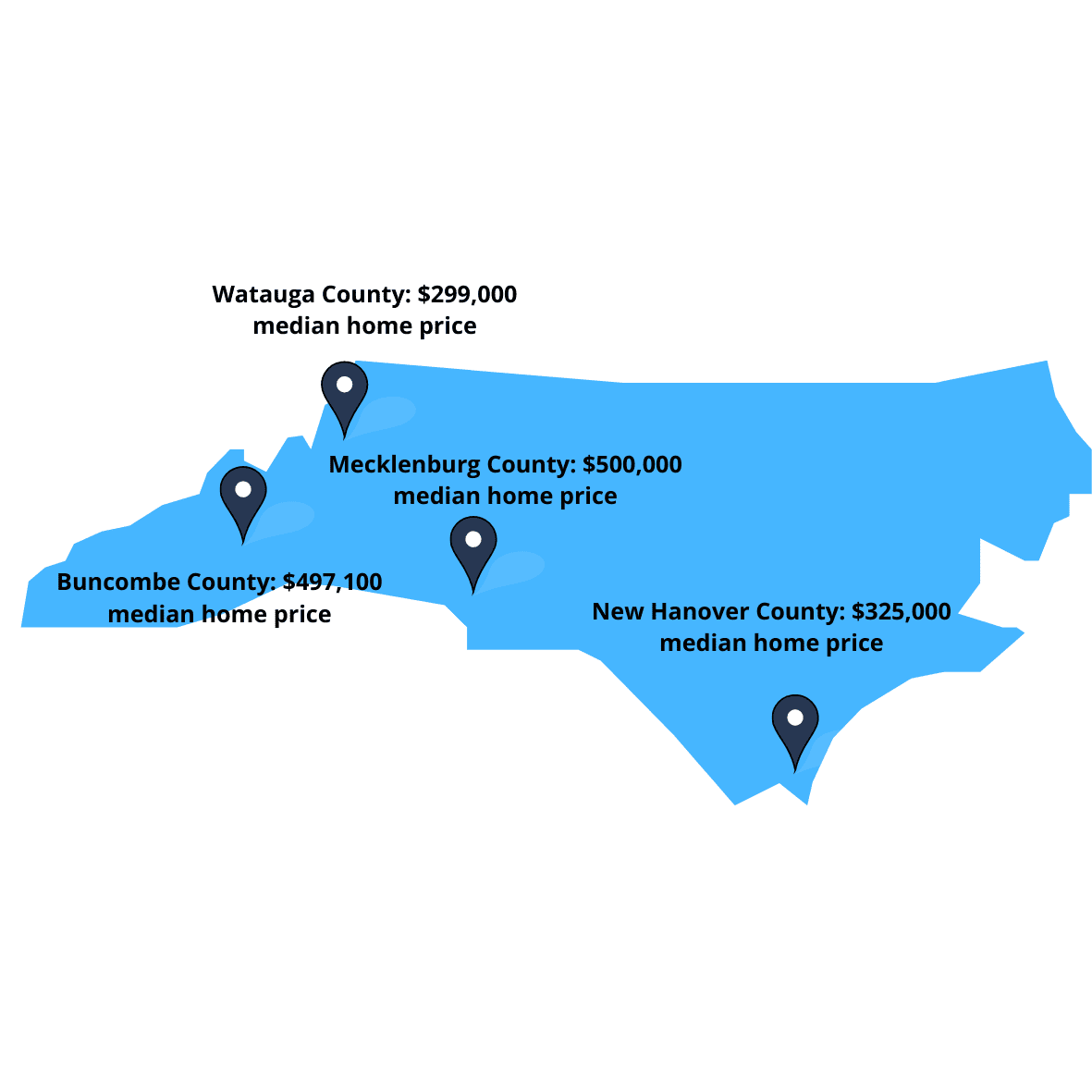

Located in the foothills of the Blue Ridge Mountains in Buncombe County, Asheville is the largest of the mountain towns with a population nearing 100,000. The city has long been a tourism destination due to its cooler mountain climate, its extensive art and music communities, and its brewpub and culinary scene. Its location near Pisgah National Forest and the Biltmore Estate have also contributed to its popularity as a prime vacation destination. However, there is also a wealth of industry and business in Asheville, making it a very livable and workable city year-round.

The median home price in Asheville is $480,000 as of August 2022, and sellers usually receive 2-3 offers, so it is moderately competitive for buyers. The good news for homebuyers is that home prices have moderated a bit as the market cooled slightly in early 2022.

Boone is also a Blue Ridge Mountain community and features homes similar in price to Asheville, selling on average for $423,000.

Located in the northwest corner of North Carolina in Watauga County, Boone is named for pioneer and explorer Daniel Boone. This charming town is home to Appalachian State University, giving it that wonderful laid-back university ambiance that characterizes so many of the smaller college towns across the country. The city is also known for its bluegrass musicians and Appalachian storytellers and is home to the Junaluska community, the only remaining African American community in Watauga county.

Central Economic Centers

Central North Carolina boasts the economic heart of the state, from the banking hub of the south in Charlotte, to the research triangle of Chapel Hill, Durham, and Raleigh, and finally to The Triad region – Greensboro, High Point, and Winston-Salem – known historically for its strong industrial and manufacturing base, in recent years bolstered by the addition of technology and biotechnology into the mix.

Charlotte has a wide range of homes and has experienced tremendous population growth with a commensurate housing boom over the past decade. Overall, North Carolina’s population grew by 9.5% from 2010 to 2020, adding over 900,000 citizens to its counties, with nearly 200,000 of those settling in Charlotte’s Mecklenburg County alone.

As you can imagine, that kind of influx has made the Charlotte housing market incredibly competitive. Homes generally sell for about 2% over list price, with the average median sale price of single-family homes currently at $429,000, up 17.2% year over year. Even as interest rates rise, the market continues to be a seller’s market and houses generally go under contract in under 24 days.

For young workers looking to take advantage of the robust jobs market in Charlotte, the downtown area is surrounded by a wide range of neighborhoods and housing price points, served by the

Charlotte Area Transit System (CATS), which operates light rail and bus lines throughout the city and surrounding area.

If you are looking for a lower price point, typically you will want to check out the bedroom communities of North Carolina’s largest cities or the in-between communities strung along I-77 running north and south through the state, or I-85 that connects Charlotte to Raleigh. Work-from-home opportunities have provided young professionals with the opportunity to consider moving farther out from the cities to take advantage of lower-cost properties.

Kuld, who lives in Rowan, 40 miles north of Charlotte, says that stretch along I-85, including Salisbury and Lexington in Davidson County, is a homebuyer’s best bet when trying to shop for more affordable housing.

“Just north of me in Davidson County is probably the most affordable,” Kuld advises. “I have buyers who start out looking in Rowan County but find if they go a little further north, they can get a whole lot more property. Charlotte, Mooresville, and the Lake Norman area are the areas that are generally less affordable.”

Kuld says the central area of North Carolina also provides a good mix of different style homes, from traditional older properties, to ranch style homes, to plenty of newer builds offering a broader range of architectural designs.

Eastern Coastal Towns

And finally, you can’t talk about North Carolina real estate and not take a look at its famous coastal plains region, featuring a retirement and vacation mecca that attracts retirees and vacation home ownership from around the country and the world.

At the heart of this gorgeous 100-mile coastline known as the Outer Banks, is Wilmington, the county seat of New Hanover County. With a population of 117,643, Wilmington is best known for its nearly 2- mile long river walk along the Cape Fear River.

The real estate market in Wilmington is currently highly competitive, with the median price of single-family homes jumping nearly 13% year over year to $424,000 while the price of all dwellings, including condominiums, coops, and townhomes, jumped 27% to $399,000.

5. Find a local North Carolina agent

Real estate agents appreciate it when their clients come to them to start home shopping after getting preapproved for a mortgage. This typically means that a buyer is ready to go and can start making offers. Choose a knowledgeable agent that specializes in representing buyers in the area you want to purchase in.

Your buyer’s agent will be able to help you create a wish list, set up viewing appointments for you, tell you more about what’s going on in the neighborhood, negotiate on your behalf, and connect you with other vendors such as a title company, insurance agent, and home inspector. Real estate agents are also incredibly knowledgeable on the homebuying process as a whole and can hold your hand throughout the process to keep closing on track.

Looking to Buy Your Dream Home in Beautiful North Carolina?

North Carolina has all a potential homeowner can dream of, and it’s no wonder why the population has grown so quickly in the last few years. With the help of a top real estate agent, you can find your home in the big city of Charlotte or your beach bungalow in the outer banks. HomeLight can match you with the best agents in your area to get you started.

6. Start shopping for homes in North Carolina

From mountain log houses to coastal plain beach homes, North Carolina offers a stunning array of architectural styles. Some of the most classically beautiful designs include colonial homes modeled after the old plantations, as well as the traditional Federal and Georgian styles. And of course, bungalow, modern, and contemporary designs are also ubiquitous among the developments that have sprung up in every region during the recent construction boom.

But within every architectural style, you will often find characteristics most typical of houses built in southern climates, including:

- Columns, supporting deep roof overhangs to protect from the heat in summer or snow in the mountain areas in winter

- Long and deep porches, wrapping around the sides of the home

- Massive trees, particularly oaks, which provide much needed shade in the summer

- Breezeways

In North Carolina’s humid summers, all of these features can be helpful in escaping the heat of the day and homebuyers should be on the lookout for these amenities when considering the purchase of a home there.

7. Make a strong offer

Working with your buyer’s agent to craft a winning offer can sound overwhelming. In competitive markets, cash offers could be more likely to be accepted by sellers with multiple interested buyers. While it is not always recommended to completely waive contingencies to impress a seller, you might consider pairing down to just the inspection contingency and financing contingency to remain competitive. Get creative with your offer — you may want to offer a larger earnest money deposit, schedule a quick closing, or even consider letting the seller rent the house back from you for a certain period of time.

Components of an offer when buying a house in North Carolina include:

- Purchase price

- Closing date

- Earnest money deposit amount

- Due diligence fee

- Contingencies: Financing, home inspection, and appraisal

- Closing cost stipulations: Who pays for what, and if you’re asking the seller for a credit to use toward closing costs

- Home warranty

- Personal property: Such as appliances or furniture

Because it is a seller’s market, Kuld says she is seeing fewer contingencies, since sellers are not interested in accepting the risk of the deal not going through, and buyers are less likely to ask for contingencies for fear of losing their due diligence money.

Sellers are still in the driver’s seat in North Carolina and looking for the highest offer. And they are asking for the highest due diligence. Years ago, due diligence was very affordable, very minimal, but the state of the market now has driven that fee up thousands of dollars. The purpose of the nonrefundable deposit is to make sure that the buyer has skin in the game, the more money the seller can get on the front end, the more likely the buyer will follow through on the purchase.

Mechelle Kuld Real Estate AgentCloseMechelle Kuld Real Estate Agent at TMR Realty Inc. Currently accepting new clients

Mechelle Kuld Real Estate AgentCloseMechelle Kuld Real Estate Agent at TMR Realty Inc. Currently accepting new clients

- Years of Experience 12

- Transactions 316

- Average Price Point $193k

- Single Family Homes 307

8. Send your earnest money deposit and due diligence fee

Your earnest money deposit, also known as a “good faith deposit,” is an amount of money you agree to pay the seller to indicate that you are serious about purchasing the home. This is usually between 1% and 3% of the purchase price. However, a higher deposit can be more attractive to sellers and make your offer stand out in competitive markets.

Whether or not you get your earnest deposit money back if you decide to back out of the sale depends on the contract. If you decide to back out of the purchase for any reason not specified in the contract, you could forfeit your earnest money. Be sure to review the contract with your real estate agent and attorney before making any decisions.

In addition to the earnest money deposit, the custom and practice in North Carolina is for the buyer to submit a nonrefundable due diligence fee, which holds the property for the buyer while they are conducting their inspections.

“Sellers are still in the driver’s seat in North Carolina and looking for the highest offer,” Kuld says. “And they are asking for the highest due diligence. Years ago, due diligence was very affordable, very minimal, but the state of the market now has driven that fee up thousands of dollars. The purpose of the nonrefundable deposit is to make sure that the buyer has skin in the game, the more money the seller can get on the front end, the more likely the buyer will follow through on the purchase.”

Kuld says there is no set amount for the due diligence fee, and she has not seen a particular trend. The amount is always negotiated with the seller. But she notes that it could be as high as 1% of the purchase price of the house.

9. Order a title search

Ordering a title search can be done any time after your offer is accepted, but it’s a good idea to do it as soon as possible because it may take a couple of weeks for the title search to come back.

In North Carolina, a real estate attorney handles the title search, examination, and closing, while the title insurance company issues the policy based on the findings of the attorney.

Who customarily chooses the real estate attorney can vary by county — but if it is the buyer’s choice, your real estate agent or mortgage lender will have a recommendation.

The real estate attorney’s preliminary title report will be reviewed by all parties including your lender and will include items such as property tax information, easements, CC&Rs, deed restrictions, liens, and any judgments against the title of the home. Any liens, encumbrances, or judgments against the property will need to be removed before the buyer can close on the property.

10. Shop for homeowners and specialty hazard insurances

Homeowners insurance is always recommended, and it is almost always required if you’re financing your home with a mortgage. The average yearly cost of homeowners insurance in North Carolina is $1,800 annually, according to Value Penguin.

North Carolina experiences regular threats from hurricanes and tropical storms, as well as hailstorms and tornadoes. While homeowners inland may not be as concerned about being in the path of a hurricane, the residual torrential rains from a hurricane can quickly create flood events throughout the state. Homebuyers in North Carolina should discuss coverages for all these potential threats with their insurance provider when choosing a policy for their new home.

11. Order inspections and appraisal

If you’re applying for a mortgage, your lender will most likely order the appraisal and you will pay for it. You will be responsible for ordering your own inspections with the help of your buyer’s agent, again, at your own cost. Your agent can recommend a licensed home inspection company if you don’t have one. The home inspector will schedule a date and time to inspect the house and depending on its size, it may take a couple of hours to complete.

12. Negotiate repairs

Remember that everything is negotiable. If you have an inspection contingency in your contract, and the inspection report comes back with tens of thousands of dollars of necessary repairs, it’s time to negotiate.

Talk to your buyer’s agent and come up with a plan for what to ask for during negotiations. Do you want a credit for the leaky roof or would you rather a licensed contractor repair it prior to settlement? If the house needs two new toilets, are you willing to walk away if the seller refuses to budge during negotiations? Keep the bottom line in mind, but don’t nitpick. Home inspectors are meant to be thorough. Focus on major repairs that need to be done ASAP and are going to be costly.

“Unfortunately for buyers, negotiation for repairs is becoming less common in North Carolina because sellers are in control,” Kuld notes. “If you are on the hook for a high due diligence payment, the seller feels like they have the power to move forward without addressing needed repairs.”

13. Final walkthrough

This is to verify that agreed-upon repairs have been completed and the condition of the home is satisfactory. The final walkthrough is usually done a day or two before the closing date. With the help of your agent, check that all plumbing, electrical, and HVAC units are on and working. If personal items such as the dining room chandelier and the washer and dryer were included in the contract, make sure they’re still in the house.

If you find that the necessary repairs were not made, or that there were damages left behind by the seller, notify your agent immediately so they can rectify the situation before closing.

14. Closing time!

North Carolina is what is known as an attorney state, when it comes to real estate transactions. Therefore, closings are always conducted in an attorney’s office, with the seller signing their documents first, and buyer signing afterwards.

“Once the deed is recorded, the homebuyer will get their keys,” Kuld explains. “That could happen the same day unless it is a late closing. If it is a late closing, the attorney would be unable to record the deed until the next morning. In that case, the homebuyer would get their keys the next day.”

An experienced real estate agent can be especially helpful in pointing you in the right direction to meet your particular budget and lifestyle. Ask lots of questions when you are hunting in North Carolina. There are gems everywhere in this great southern state, and plenty of opportunities to find the home of your dreams.

Header Image Source: (Gene Gallin / Unsplash)

- "ClosingCorp Reports Average Closing Cost Data for Refinances In 2020," Business Wire (March 2021)

- "Tackling Home Financing and Down Payment Misconceptions," National Association of Realtors (January 2022)

- "Adult population drives NC growth," Carolina Demography (August 2021)

- "Due Diligence Fees: When Are They Refunded?," North Carolina Real Estate Commission (May 2017)

- "Best Cheap Home Insurance Companies in North Carolina," ValuePenguin (August 2022)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.