No Credit? No Problem! How to Build Credit for Homebuyers

- Published on

- 5 min read

-

Sally Tunmer Contributing AuthorClose

Sally Tunmer Contributing Author

Sally Tunmer Contributing AuthorClose

Sally Tunmer Contributing AuthorSally Tunmer is a writer and content strategist with 10 years professional experience focusing on real estate, travel and the lifestyle and culture of places. She was the former editor of the official New Orleans tourism blog and is a regular contributor to neighborhoods.com. Sally is currently based in Atlanta where she drinks wine, listens to music and writes about both on her personal blog.

Imagine applying for a credit card or a bank loan with full confidence that you’ll not only get approved, but it will come with a low interest rate. This is the power that comes with a great credit score, which sure beats the dread and doubt associated with a bad one. When you want to buy a house, how can you make sure you’re in the first category? Because unless you’re paying cash, that means you’ll need to get a mortgage.

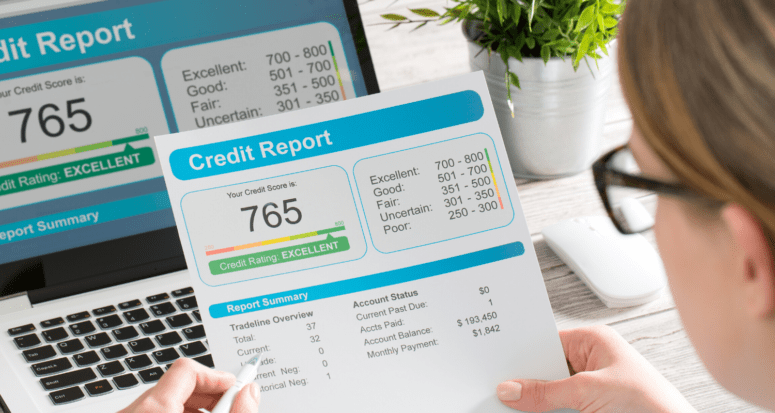

To secure a mortgage, you’re going to need a decent credit score to get a Federal Housing Administration (FHA) government loan, a good credit score to get a conventional mortgage loan with a moderate interest rate, and a great credit score to get a mortgage loan on a range of home values with lower interest rates.

The point being, at the very least, to get a mortgage loan approved at the lowest level by the FHA, buyers need a minimum score of 500. On the other end of the spectrum, a credit score of 740 or higher will offer buyers the most flexibility and the best interest rates available on a mortgage. So, credit scores when buying a house are pretty important and can mean the difference between buying a house you can live with and buying a house you love.

Furthermore, when lending environments are riskier (for example, when a recession is looming), lenders will impose mortgage overlays. This is a way for lenders to decrease their risk by raising the standards required to get a mortgage loan. We saw this happen in 2020, when the minimum credit score to buy a house increased for buyers due to the coronavirus pandemic. Buyers with higher credit scores were more likely to hang onto their loans, but many buyers at the lower end of the credit scale suddenly found themselves out of luck.

If you’re on the lower end of the credit scoreboard but you’re otherwise ready to buy a house, you’re not alone, says Augusta, Georgia-based real estate agent Natalie Poteete, who has a track record of selling 68% more properties than the average agent in her market.

“You’re always going to have people calling who want to buy a house who just don’t have good credit. In that case, you get them to a lender and let the lender take care of it from there.”

Luckily, there are many methods and strategies to up your game. “[The lender] can look everything over and tell you where you’re at and typically put you in a time frame for getting there.”

We’ve anticipated some of these ways to improve your credit. Discover how credit scores are calculated and how to build yours before buying your first house. With industry-expert intel and research, we’ve compiled this how-to guide for the winning score that will bring home the trophy — your new mortgage.

How credit scores work

What’s the purpose of credit scores, how are they determined, and who even are these people giving out scores? We’re so glad you asked!

Credit scores are assigned to individuals so lenders can assess the credibility and risk associated with each person’s ability to make debt payments. With a bad credit score, the likelihood of getting a loan is low — and with a good one, it is high.

FICO (Fair Isaac Corporation) is the national industry standard used for credit scores based on consumer credit history. The three main credit bureaus in the U.S. that supply the reports used for credit scores are Equifax, Experian, and TransUnion. It takes six months of using credit and having a credit account open to get a FICO score.

FICO scores weigh the following credit report components:

Payment history: 35%

Payment history is the most important factor of a credit score. This shows if you can make payments on credit cards, loans, and bills on time.

Credit utilization: 30%

Credit utilization is the amount that is owed on credit cards. Maxing out or using a high percentage of available credit can negatively affect credit scores. The best scores include a low percentage of credit borrowed, ideally below 30%.

Length of credit history: 15%

The length of credit history is how long someone has used credit and how long active accounts have been open. The best way to build credit is to have credit over time — the longer, the better.

New credit: 10%

New credit factors in how many new accounts a user has and how quickly each was opened after the previous account. Having multiple accounts opened in quick succession could indicate risk to a lender, suggesting the credit user may not have their finances under control.

Credit mix: 10%

Credit mix in a credit report shows all the types of loans someone has, including revolving credit card payments, payment installments like student loans and car loans, and retail accounts like store credit cards. A variety of credit that’s properly managed and paid on time proves the user’s experience with making payments on multiple accounts.

Best ways to build credit

The answer to how to build credit fast for anyone who has little to no credit history or bad credit starts with practicing good money habits.

1. Pay your debts on time

Because payment history is the biggest factor of your credit score, making all your payments on time is crucial for building and maintaining good credit.

Make sure you know all the payments you are responsible for and their due dates, including credit card payments, utility bills, rent, car loans, insurance, phone payments, and medical bills. For recurring payments — like phone bills, power bills, insurance bills, car payments, and internet bills — set up automatic withdrawal to avoid any late payments that will damage your credit score.

When evaluating your credit before buying a house, paying off outstanding debts that show up on your report can be a relatively quick fix if there aren’t other major issues. “If you have an old Verizon bill you never paid, and that can typically get paid off, then you can probably buy a house in two to three months,” says Poteete.

2. Prioritize high-interest debt

Hopefully you’re managing your credit well and keeping your credit balances low, but that might not be the case. Also: Life happens. If you have multiple debts with a large payoff amount, attack them with the debt avalanche strategy.

An alternative to the debt snowball strategy created by personal finance guru Dave Ramsey, the debt avalanche tackles the debt with the highest interest rates first while maintaining minimum monthly payments on other accounts. Once the highest-interest debt is paid off, move on to the next and repeat until all your debt is paid off.

3. Be strategic about opening new accounts

Because new credit and credit mix both make up a percentage of your credit score, they should both be considerations when opening credit accounts. It’s a bit of a catch-22 situation, because you need new accounts to have diversified credit… but it’s not in your favor to have too many new accounts opened back to back. So, what’s the best way to proceed?

First of all, you don’t need many different accounts to have a good credit mix. Even just opening one or two additional accounts will benefit your credit score over a year. Only open accounts where it makes sense.

For example, what major type of account are you missing, and which ones do you actually need on top of what you already have? Here are some of the primary credit accounts to consider opening for a good mix of credit:

A secured credit card

Secured credit cards are an easy way to start building credit from scratch before you get a regular, major credit card. With secured credit cards, you put a small deposit down equal to the limit of the credit amount, which will usually be returned at the time the account is closed — as long as the payments were made in full and on time. Pro tip: Find a secure credit card that can roll into a standard credit card with the same company.

A store credit card

Another low-stakes option to build up credit is a credit card with a store. There are pros and cons to store credit cards, the downsides being they have low limits and high interest rates. However, it’s very easy to get approved for one without putting any kind of deposit down, which is good news if your options are limited.

An auto loan

An auto loan, also known as a car payment, is an installment loan — a fixed monthly payment over a set time period — which is good to have in addition to a revolving credit card payment for an improved credit mix. An auto loan, like a credit card, involves the lender making a hard inquiry into the buyer’s credit, which can temporarily reduce your credit score but will greatly improve it over time if managed responsibly.

A joint account with another user

Becoming an authorized user on someone else’s credit card account, like a parent or significant other, is another easy way to build credit. If this route is taken, be sure that the credit company reports authorized user activity to the credit bureaus and that the primary account holder is a responsible credit user with excellent payment history.

4. Finally: Request credit increases

You’ve done all the work and made the necessary moves to build up your credit — great job! Now what? Keep going.

The best next step after earning a solid credit score is to increase your available credit. This will decrease your credit utilization, which makes up one of the largest measures of your credit score. The best way to do this is to ask for a credit increase on your oldest accounts that you’ve consistently paid on time and kept a low balance on.

Sticking to the plan

The only way building your credit successfully will work is if you practice good money management across all your personal finances. To boost your credit score and get to where you want to be in order to buy the house you want, you’ll need to plan accordingly.

Poteete recommends that her clients start with outlining what their expenses are every month. “Knowing how you’re going to spend every month allows you to be able to figure out where you can budget in for your mortgage.”

The next step in managing finances is to set goals. She recommends her clients ask where they see themselves in 20 or 30 years and where they would like to be. Whatever the target for retirement or the next phase of your life is, make a financial plan to achieve it.

“If you want to be in a 20-year mortgage and have your house paid off in 20 years, then what does that look like for you? How much can you realistically afford every month in order for you to get it paid off in 20 years?”

Header Image Source: (REDPIXEL.PL / Shutterstock)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.