Rise, Fall, or Stay Level: What Happens to House Prices in a Recession?

- Published on

- 5 min read

-

Melissa Rudy Contributing AuthorClose

Melissa Rudy Contributing Author

Melissa Rudy Contributing AuthorClose

Melissa Rudy Contributing AuthorMelissa Rudy is a seasoned digital journalist with 15 years of experience writing web copy, blog posts and articles for a broad range of companies. When she can’t buy or sell homes, she settles for the next-best thing: researching and writing about all things real estate-related.

A looming recession, such as the one we’re facing now on the heels of COVID-19, brings a great deal of worry and no shortage of questions. You might be wondering about the stability of your job, the state of your investments and — if you’re a homeowner — the impact on the value and price of your property. That’s especially true if you’ve been considering selling your home anytime soon.

By definition, a recession is a “significant decline in general economic activity in a designated region,” marked by a drop in employment, income, retail sales, production and the gross national product (GDP) — and so it seems like a given that home prices would naturally drop in response.

“In a recession, more people are unemployed and cannot pay their mortgages,” says Tenpao Lee, Ph.D., a professor of economics at Niagara University. “Therefore, in a recession, the demand for a home will decline and the supply for a home will increase. Home prices will inevitably decline.”

But the reality is that every recession is different and every homeowner’s situation is unique — which means the effects on home prices can vary widely across markets.

How past recessions impacted housing prices

Every recession has unique variables that make it different from the last one, notes Owen Dashner, a real estate investor and partner with Red Ladder Property Solutions. Prior to the current “pandemic recession” we’re approaching (or already in the midst of), the most recent economic contraction was the Great Recession, which lasted from December of 2007 until June of 2009.

Great Recession pummeled prices

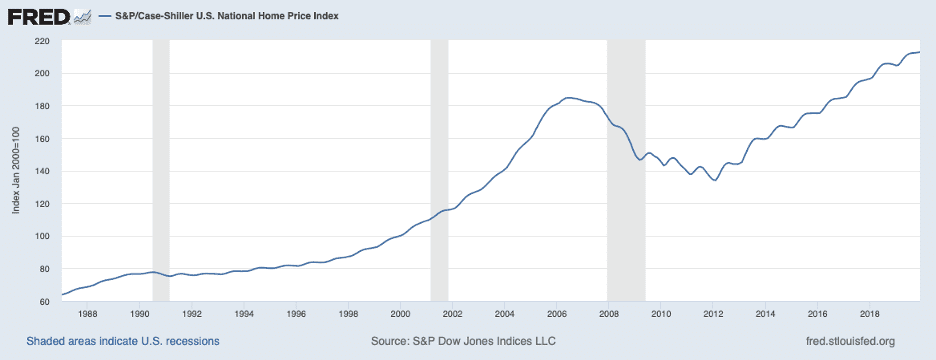

After a decade of steadily rising home prices — from the average price of $207,000 in 2000 to $314,000 in 2007 — the housing bubble finally burst in 2007. The inflated home prices and spike in subprime mortgages combined to trigger the biggest housing market crash in modern history. Unemployment spiked to 10% as of October 2009, and the GDP (gross national product) fell by more than 5%.

“In The Great Recession, the subprime mortgage market had a big hand in bringing the economy and the housing market to its knees,” says Dashner. “In the aftermath, many home builders were crushed. Over the past decade, the pause in home building led to an undersupply of housing, especially starter homes, which has in turn led to high demand and increased pricing that we’ve maintained until this year.”

Mike Graf, a top real estate agent in Cedar Rapids, Iowa, was selling homes during the Great Recession, and remembers the impact well. “It had a substantial effect on the market — we saw home prices drop by 10-12%,” he recalls. “It took 10 years for the market to recover.”

Prices fared better in shorter recessions

But it’s important to remember that the Great Recession was centered in the real estate market, and not every economic decline has such a dramatic impact on home prices. Max Kimmel, owner of One Shot Finance, points out that during the two mini-recessions in the 1980s, housing prices actually increased — and the 2001 recession saw similar trends.

In fact, according to data from ATTOM Data Solutions, throughout all five of the recessions that have occurred since 1980, there were only two instances when home prices decreased, in 1990 and 2008.

“The Great Depression [of the 1930s] saw a 25% average decrease in home prices, but that was mostly due to the large number of foreclosures — and with much stronger regulations nowadays, that isn’t likely to happen again,” Kimmel says.

Dennis Shirshikov, a senior economic analyst for FitSmallBusiness.com, agrees that not all economic declines will leave the housing market battered and bruised. “Other recessions saw home prices decline significantly at the highest price points, but left most homes declining at a moderate amount of under 10%,” he says.

Most of the real estate agents and finance experts we spoke with agree that the current COVID-19-triggered recession isn’t likely to have the same devastating impact on the housing market as the Great Recession.

“Damage to housing will probably not be as bad as the Great Recession, as the pandemic is a non-economic factor and the economy is fundamentally healthy,” notes Lee.

Are some housing markets more vulnerable to recessions?

The short answer is yes. Here’s how a recession impacts different types of housing markets — and different types of properties — in unique ways.

Low vs. high price points

Generally speaking, upper-end property values are more affected by economic dips, says Curt Stinson, a real estate agent based in Tucson, Arizona. That’s because higher-net-worth homeowners are much more portfolio-sensitive.

“When the stock market and investment portfolios drop drastically, that affects the upper end more,” Stinson says. “On the other hand, homeowners on the lower end are more interest rate-sensitive.”

Graf agrees that higher-priced listings are harder-hit. In his Iowa market, he sees the greatest impact on properties priced at $400,000 and up. He says that during the COVID-19 economic crisis, homes in the $250,000 range remain a hot commodity.

“That’s partly because the higher-priced homes have a more limited audience,” he explains. “The lower-priced homes appeal to first-time homeowners who are eager to take advantage of the lower interest rates.”

Metro vs. rural areas

As with most elements of real estate, it’s all about location, says Lee. “Luxurious houses in over-developed areas will be hurt more, such as New York City and San Francisco,” he points out.

“Already depressed cities will be hurt less, such as Detroit and Cleveland. Some inland states will also be hurt less, such as Wyoming and North Dakota.”

Shirshikov notes that recession-triggered home price declines are typically limited to metropolitan areas. “Historically, following a disaster, home prices in major cities decline, and more rural and suburban homes outside the city see price increases. This is due to individuals leaving cities and entering markets that are safer in comparison,” he explains.

Impacts by industry

Isack Kohn, CPL, an oil and gas professional with over 15 years of experience in land acquisitions and financial modeling, says the housing markets most vulnerable to a recession are those in cities that support the energy industry. In his Texas market, that’s mainly Houston, Midland, and Dallas. “The least vulnerable markets are those revolving around the production of economic staples,” he says. “That’s not to say they won’t feel the pain — just less so.”

New vs. existing homes

As far as property types, Kohn says newer developments are more at risk, because developers or homebuilders could potentially go out of business and leave unfinished homes or empty lots. Neighborhoods that are already built out and well-established tend to better weather the storm.

Tips for pricing a home in a recession

If you’ve decided to list your home during a recession, pricing is everything. Keep these expert tips in mind to help maximize your sale price:

Don’t overprice:

“During a recession, you’re not in a position where you can overprice a home and count on negotiating back,” Graf warns. “If you’re overpriced, agents will be less likely to show your home.”

Shirshikov agrees that sellers should under-price homes and wait for multiple buyers to start bidding, which gives the seller leverage.

“Sellers who price like nothing is happening will end up with their house on the market for a long time and will have much lower interest, even if they eventually cave and lower their asking prices,” he warns.

Take a cue from the comps:

Stinson typically sets prices at 3% to 5% above comps, but in a recession, he looks at pricing 3% to 5% percent below the comps.

Have your home ready when you list:

In an economic decline, buyers tend to have less extra cash to spend on improvements, and will gravitate to homes that are well-maintained, updated and move-in ready.

“If two homes are in the same neighborhood with the same square footage and are very similar, but one shows better than the other, that one will ultimately sell at a higher price,” Graf predicts.

Have a strong marketing plan:

That’s where a trusted real estate agent comes in. Talk to your agent about how he or she plans to promote your property and boost visibility.

Know what to expect:

When setting a sale price, use a calculator to determine how much you’re likely to make when your home sells, based on its value, location, agent commission, and remaining mortgage.

Consider renting out your property:

If you’re not in a position to lower your price to accommodate a down market, Kohn says it might make more sense to rent out your property for the time being.

“As long as your tenants maintain the property, it can become a passive income stream instead of a financial loss,” he explains. “Once the market recovers, you can then put the home back on the market.”

Header Image Source: (Martin Widenka / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.