How Much Mortgage Can You Afford? 16 Line Items to Consider

- Published on

- 7 min read

-

Mark Henricks Contributing AuthorClose

Mark Henricks Contributing Author

Mark Henricks Contributing AuthorClose

Mark Henricks Contributing AuthorMark Henricks writes about real estate, homeownership and other topics from Austin, Texas. His byline has appeared in many leading publications. He has authored, co-authored or ghostwritten a dozen published non-fiction books. For relaxation he reads omnivorously, performs as a guitarist and singer, trains for sprint triathlons and disappears whenever possible on whitewater kayaking and wilderness backpacking expeditions.

If you’ve never bought a house before, then you might (understandably) be spending a lot of time daydreaming about whether you can afford a midcentury modern or a restored Victorian in your area. A much less interesting question to ask is how much mortgage you can afford … but it’s going to be a critical question to answer before you can start the fun part of the process — shopping for a place to live.

Four factors are most important when determining how much house or mortgage you can afford: your income, your existing debts, your credit score, and your down payment.

Savvy buyers deciding how much to spend will also consider things like the interest rate and length (or term) of the loan, and taxes and maintenance after the purchase. But those first four are the main controlling influences.

16 factors that determine how much mortgage you can afford

Here are details on the four primary concerns, as well as a dozen more to keep in mind.

1. Income

Your gross monthly income is one of the first things lenders look at when deciding how much you can borrow.

That’s understandable. Without adequate income, it will be tough for a borrower to pay back the loan.

There’s no real minimum to the income you need to buy a home. It all depends on how much a house costs in your market and whether your earnings will cover the monthly payments.

If your income is coming up short, working more overtime or taking on a second job aren’t your only options. “Applying with a partner or non-occupying co-borrower, someone who’s not going to live in the home but will be on that loan, can help you qualify,” suggests Marcus Rittman, HomeLight Home Loans’ director of mortgage operations.

Of course, you still need to be able to afford the mortgage payments and all your other housing expenses each month, so make sure you get that sorted before going this route.

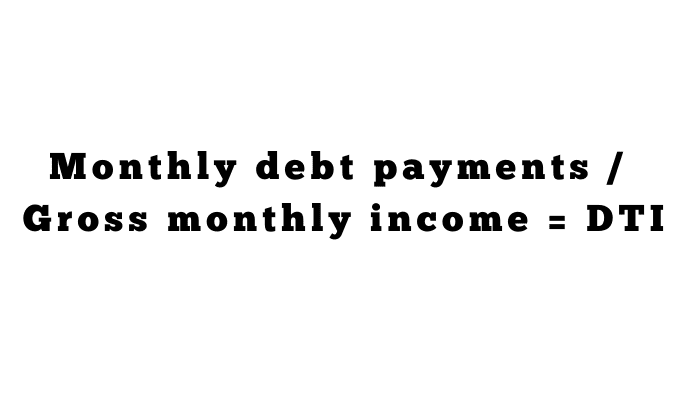

2. Monthly debts

The next major consideration is the amount you have to pay every month to service other debts. This includes car payments, student loan payments, and credit card minimum payments. Lenders will also include court-ordered child support and alimony payments, but they don’t consider utility bills, insurance premiums, and the like.

Add up these monthly debt payment amounts and divide that number by your gross monthly income to get your debt-to-income (DTI) ratio.

Lenders look at DTI to estimate your ability to pay back your mortgage loan. Most look for a DTI ratio of around 43% or lower, including your new mortgage payment, but this varies from lender to lender.

This means that one way to increase the amount you can spend on a home is to focus on debt reduction. Rittman says your lender can help you with the calculations and strategizing.

“The loan officer can look through your debts and make recommendations to pay off some of your debts, which might help boost the maximum amount you can get approved for,” he says.

3. Credit score

You don’t need a perfect 850 credit score to buy a house, but the further you are from the theoretical bottom score of 350 or so, the better.

Here are the credit score categories:

- Excellent (720-850)

- Good (690-719)

- Average (630-689)

- Poor (350-629)

If your score is lower than 580, then you may have trouble borrowing money to buy a home. If your score is 740 or better, you probably will get your lender’s best offer (provided the rest of your financials check out).

If you’re somewhere in between, you’ll likely qualify for a loan, but you may not get the best possible rate.

Start by taking a look at your credit report. You are entitled to get a free copy of your credit report each year from each of the major credit bureaus. You can request a copy by checking AnnualCreditReport.com.

When you get the report, look for errors and write to the appropriate credit bureau to correct any mistakes you find.

You may also consider paying down any credit balances, which will help improve your score.

Avoiding applications for new credit can also help your score. Whatever you can do to improve your credit score can help, says Rittman.

“The credit score is a factor. It does have an effect. If your credit score is better, it’s going to affect affordability.”

4. Down payment amount

The down payment is the last of the four major influences on how much mortgage you can afford. Simply put, a bigger down payment lets you consider more expensive homes.

Putting 20% down can get you the best possible interest rate and also help you avoid extra expenses, such as mortgage insurance.

But buyers usually put down less than 20% of the home’s purchase price. Here are the minimum down payments for different types of loans:

- FHA loans can get approved with as little as 3.5% down.

- Conventional loans, such Fannie Mae’s HomeReady program, can be made with as little as 3% down.

- VA loans allow eligible service veterans to borrow money to buy a house with zero down.

- USDA loans featuring zero money down are also available, mostly in rural areas.

5. Savings

Lenders will also look at your personal savings in addition to the amount you can put down. They like to see borrowers with three months’ worth of savings, including the mortgage payment, as well as enough to cover expenses, such as moving costs and utility bills.

Now is a good time to consider re-ordering your priorities to emphasize savings, says Janet Anderson, a real estate agent who works with 86% more single-family homes than the average agent in Tracy, California. “The first time I purchased a home, I stopped going out to eat and saved money and paid off debt so when I went to purchase, I was ready,” she says.

6. Mortgage insurance

Whether or not you’ll pay mortgage insurance also helps determine how much you can afford.

Generally, if you put less than 20% down, you’ll have to pay the premiums for this insurance, protecting lenders against the risk of a loan default. It can add hundreds of dollars a month to the mortgage payment, and that can have a big effect on your DTI ratio — and, of course, how much house you can afford.

7. Mortgage rate

With interest rates at the bottom of historic ranges, your mortgage rate has less impact than in a more typical interest rate environment.

When interest rates are low, “there’s a lot more affordability,” Anderson says. “I have clients say, ‘This is my price range.’ But for an extra $10,000, they can get a lot more house and their payment might have gone up only $40 a month.”

Still, you can reduce your rate and increase the amount you can spend by, among other things, making a larger down payment.

8. Loan term

The length of your loan has a major impact on the house you can afford, and it’s also something you can control.

Most loans are issued for 30 years, but 15-year mortgages are also popular, in part because they allow buyers to build up equity faster and save on total interest over the life of the loan. But a 15-year mortgage has a significantly larger monthly payment and that can limit the amount you can borrow.

Choosing a 30-year mortgage, with its lower payment, can put a more expensive house in your affordability range.

9. Type of interest

Whether the loan charges a fixed interest rate or an adjustable rate can also have an effect on payment size.

Most loans are fixed-rate, meaning they will carry the same interest rate throughout the life of the loan.

An adjustable-rate mortgage, or ARM, typically has a lower rate for the first few years, and after that, it adjusts periodically to follow the market. When current rates are high, this may mean having a lower monthly payment when it recasts after the initial fixed period if rates are lower.

But in an environment like 2020, when rates have little room to go down, an adjustable-rate mortgage payment is likely to simply adjust higher in the future. That said, the lower start rate of an ARM loan may make your home more affordable for the first 5 to 10 years. While lenders will likely qualify you at the “fully indexed rate” (a calculated rate that approximates the maximum amount you would pay when the loan recasts after the initial fixed period), to ensure you can truly afford the loan, your actual monthly payment will be lower with an ARM, giving you extra wiggle room each month.

10. Property type

Different types of properties cost more or less to own so that can affect how much you can spend.

An older home may have more repairs and deferred maintenance than a newer one. A condominium apartment may have lower utility bills than a standalone single-family home.

11. Property taxes

Property taxes assessed to pay for local schools and government vary widely across the country.

In some places, property taxes can represent a large share of the cost of ownership, and they don’t go away when the mortgage is paid off.

You can pay property taxes annually or have them included in your monthly payment, but either way, this is a non-optional cost to consider.

12. Homeowners insurance

To protect them against loss, lenders require paid-up hazard insurance on any property with a mortgage.

Costs for this insurance depend on your location among other things, but it’s a cost you’ll have to put into your affordability budget.

13. HOA fees

Most homes are not part of a homeowner’s association (HOA), but if yours is, you’ll be assessed membership fees to cover association functions, such as landscaping common areas.

These can range from as little as $100 to as much as $1,000 a month, so it’s vital to determine whether your home is part of an association when evaluating whether or not you can afford it.

14. Other insurance

The most common type of insurance you might need in addition to a regular homeowner’s hazard policy is flood insurance.

Mortgage lenders require properties in designated flood-prone areas to have this insurance. The cost depends on how risky your location is, and it can be as low as about $100 a year, but typically averages more than $600 a year.

15. Other expenses

Maintenance, repairs, and utilities can add significantly to the cost of owning a home and should be kept in mind when considering affordability.

Is it an older home with appliances that will need frequent service calls? Is there a big yard that consumes lots of water in a dry climate? Situations like these could make a house unaffordable.

Occasional major repairs, such as a new air conditioning system, can also put a major strain on a homeowner’s budget.

16. Your long-term goals

No matter what your lender thinks you can afford, the final decision of what to spend is up to you.

Having a large mortgage payment can make it hard to achieve long-term financial goals, such as paying off student loans and taking nice annual vacations. Not everyone likes the idea of giving up some luxuries to buy a nicer house. That may be what’s called for if you borrow up to your limit.

“Are you okay with spending a little more on the mortgage and housing expense and sacrificing going out to dinner?” Rittman asks. “It’s a good thing to not get a shock.”

One way to figure out how much you can afford is to ask yourself what you can comfortably devote to mortgage payments and other costs, and then work backward.

Don’t forget to leave yourself some reserve cash to cover unexpected expenses. That may serve you well if, for instance, you need to increase your bid in a competitive situation.

Financial advisors often use the 28/36 benchmark to help determine affordability. According to this guideline, your mortgage payment should be no more than 28% of your gross monthly income. Your housing costs, including all the items listed above, should be no more than 36% of your gross.

While this isn’t a hard-and-fast rule, it can help suggest a reasonable total housing cost.

Home affordability calculator

Home affordability calculators like this one from HomeLight can also help. By answering a few questions about your location, pre-tax annual income, down payment, other debts, and credit score, you can instantly get valuable additional insight into this crucial question.

“That’s a great tool and will give you a nice idea,” Anderson says.

“Definitely with technology today, there’s a lot at our fingertips. That will give you a general idea of what you can afford.”

A final question about affordability is: When? At what point in the process should you try to determine your price range?

The answer is: When you start.

Before looking at any properties, sit down with a loan officer and get pre-approved for a loan amount. While a preapproval letter isn’t a guarantee that you’ll get a loan, it will give you confidence, reassure sellers that you can do the deal, and reduce chances you’ll fall in love with a property you can’t afford. Ultimately, there’s no substitute for this.

“Doing research on your own, you can get an idea,” Rittman says “But talking to a professional is your best bet.”

Header Image Source: (Elle Aon / ShutterStock)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.