Thinking About Buying a House? How to Get a Free Credit Report

- Published on

- 5-6 min read

-

Dena Landon Contributing AuthorClose

Dena Landon Contributing Author

Dena Landon Contributing AuthorClose

Dena Landon Contributing AuthorDena Landon is a writer with over 10 years of experience and has had bylines appear in The Washington Post, Salon, Good Housekeeping and more. A homeowner and real estate investor herself, Dena's bought and sold four homes, worked in property management for other investors, and has written over 200 articles on real estate.

When you’re applying for a mortgage, one of the first things your banker will do is pull your credit report. When the loan officer in charge of approving or denying your loan application sees your credit report, do you know what yours will say? Or could you be in for an unpleasant surprise?

Chris Austin, a Kansas City, Missouri, agent who sells 83% more single-family homes than other agents in his area, has new clients start working with a lender right away. The lender can “look at their situation and give them specific advice to get to a place where they can buy in a short amount of time,” he says.

A big part of what the lender does is go over your credit report and identify areas of improvement. But if you want to know where you stand before talking to a banker or real estate agent, here’s how to get a free credit report and start working on your credit yourself.

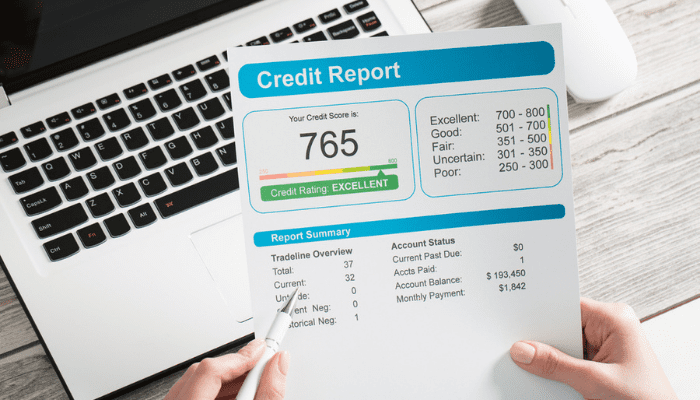

What is a credit report?

A credit report is a snapshot of your financial history. Employers can use it when conducting background checks, and banks will use it when deciding whether or not to let you open a new credit card. Your overall credit score influences the rates you pay to borrow money and your repayment terms.

Credit reports show personal information (your name and past addresses), phone numbers, and current and former employers. Any delinquent or outstanding accounts, missed payments, and bills in collections will also appear if the creditor has reported them to the credit bureaus.

A credit report also includes a list of accounts in good standing, including how long you’ve had them, and how much credit you can draw from them. The length of time you’ve had accounts open also factors into your overall score.

Credit utilization describes the ratio of the amount drawn on your credit to the amount available. In other words, how much money have you borrowed compared to what’s available to you? A high credit utilization ratio tells lenders that you’re relying on credit heavily, so you should try to keep your outstanding balances below 50% of your available credit.

Finally, a credit report shows inquiries — who’s asking about your credit. If a mortgage lender sees that you’ve been inquiring about opening a lot of new forms of credit, they could view it as a warning sign.

How do you get a free credit report?

Three different agencies — Equifax, Experian, and TransUnion — maintain credit reports. By law, they’re each required to give you one free credit report a year.

You can request your report by email, online, or over the phone.

When you apply for a new credit card or loan, you often have the option to request that the lender send you a copy of the credit report they use when making their decision. Typically, they’ll mail it to you during the application process. It’s another great way to get a free copy if you’ve already gone through the credit bureau.

Why would you want a free credit report?

Knowing what’s on your credit report tells you what lenders are looking at when you apply for a credit card or loan. It could give you a rough idea of the interest rates you might qualify for, and insight into why they might turn you down if that’s the result of your application.

Another reason to look at your credit report, even if you’re not currently applying for a mortgage, is to identify and fix any mistakes. According to one study, one in five consumers has an error on their credit report. Errors could be as minor as including the wrong address or phone number, or more serious, such as showing an account in collections when you’ve paid it in full.

It’s also important to monitor your credit for fraud issues. If someone has stolen your identity and is using it to open credit in your name, your credit report can help you discover what’s happening. You may have to reach out to both the creditor, such as the credit card company, and the credit bureaus to get fraud issues resolved.

The process of closing fraudulent accounts and clearing up errors can take time. If you plan on buying a house sometime in the next year, take action now.

Marcus Rittman, the director of mortgage operations at HomeLight Home Loans, recommends that you start checking your report — the “sooner the better. It gives you time to start working on a path to improve your credit.”

How often can you request a free credit report?

You can get one free report a year from each of the three agencies, for a total of three reports every year.

You can also request a free report under other special circumstances:

- You’re unemployed and you intend to apply for unemployment

- You think your file reflects fraud, and you want to check it

- You receive public welfare assistance

What about those free credit reporting agencies? Rittman cautions that while they’re “good as a guideline for buyers, don’t take those scores and think that’s exactly what you’ll get with a lender.”

Lenders perform a tri-merge credit report, combining the reports from all three bureaus, and it’s scored a lot differently than the free credit services.

Those reports can, however, be great for telling you in general if your score is improving or weakening.

Should you ask for a credit report from just one reporting company, or all three?

Does it make sense to order them all at once, or one at a time? That depends on your goals.

If you’re intending to track your score over a year while planning for a home purchase, try spacing out your requests. Request a free report every few months from a different agency to see if efforts to improve your score are paying off.

But if you’ve never checked your credit before, definitely order all three at once. They’ll each have slightly different information, and one could contain a mistake that doesn’t appear on another.

After you’ve pulled and compared them all, and had any errors fixed, a good rule of thumb is to pull one report every four months, just to keep tabs on your credit report’s accuracy.

Who can request your credit report?

Anyone who wants to pull your credit report needs your permission. You’ll have to provide them with details, such as your full name, Social Security number, and address, and you’ll have to sign a form authorizing the requester to access the report.

Who typically requests a credit report? Employers commonly pull your credit report to determine your trustworthiness. When you rent a house, sometimes the landlord will ask permission to do a credit inquiry. And, of course, when you apply for a new form of credit (such as when you’re buying a house), the lender will pull your report to determine your credit-worthiness.

What about when a company sends you an unsolicited credit card offer in the mail? In that case, they performed a “soft pull.”

With a soft pull, the company inquires about your credit with a bureau on their own. Existing credit card companies and lenders may periodically perform a soft pull just to check that you’re still a good borrower.

Soft pulls don’t impact your credit score. Why? Because you didn’t apply for access to more credit, which would indicate possible money issues.

Whenever possible, ask an employer or landlord to do a soft pull if they want to check your credit.

How long will it take to get your credit report?

Your credit report should be processed and mailed within 15 days of receiving the request. The only website authorized to provide a free report is annualcreditreport.com, and you can get a digital copy faster through the website.

If you want your report from a specific bureau immediately, you can set up an online account with them. (Be careful that you don’t accidentally subscribe to their credit monitoring service or any fee-based service when you sign up.)

OK, you have the report. How do you read it?

Once you have a copy of your report, you’ll need to read and interpret it.

Have you actually lived at all of the addresses listed? If a report pulls an address where you’ve never lived — for example, that of an ex-spouse — you could get collection calls for residents at that address. Check basic information like this first, then dig into the details.

Is the list of open and closed accounts correct? Your available credit impacts your credit utilization ratio, so even if you’re not carrying a balance on an open credit card, you’ll probably want the card to appear on your report. Also, look for any accounts that you don’t recognize, which can be a red flag to help identify possible fraud.

What if you’ve paid off a credit card? Should you close it? Not necessarily.

Rittman advises that you keep it open and continue using it, just “don’t go over 30% of the maximum you can borrow, and keep making payments on time.” This demonstrates you know how to properly use credit.

Account balances will probably be averages, rather than exact and down to the minute. But they definitely shouldn’t be wildly different from what you’ve typically charged to the account. A large spike for purchases you don’t recognize could indicate a fraudulent charge.

Austin recommends talking with an expert lender when trying to interpret your report, especially if you’re just under the threshold to qualify for a mortgage and trying to make plans. They can tell you to “pay off this credit card and in two months, you’ll be able to raise your score,” and help you reach your financial goals.

What happens if you find an inaccuracy and want to dispute it?

The dispute resolution process depends on both the type of error and the credit bureau. For example, a simple mistake at Equifax — such as a wrong address — can be resolved entirely online through the company’s online portal. For more serious errors, you might have to send a formal letter or make a phone call.

If the inaccurate information came from a creditor who reported to the agency, it could take more work to get it resolved. You’ll likely have to call or send a certified letter to the creditor explaining the situation and asking them to fix it. They could ask for proof that you’ve paid a balance in full, such as a canceled check, or request other documentation before resolving the error.

Once you’ve convinced them that the error is real, they then have to report it to the credit bureau to get it cleared off your report. They’re required to notify all three credit bureaus of any mistake they find.

What happens if the information provider or credit reporting company doesn’t correct a disputed mistake? You’ll have to contact the credit bureaus directly. Prepare to provide all documentation again, send letters, and make plenty of phone calls.

And if you still can’t get the error removed, ask that a copy of the dispute be included in your file and with any future reports.

How do you keep tabs on your credit?

Order your free credit report once every year; it’s smart to order from all three reporting companies. Put a reminder in your calendar.

If something adverse happens (for example, you’re denied credit, insurance, or employment) because of your credit, you can request a free report within 60 days of receiving notice of the denial.

If you’re concerned about fraud, consider a credit freeze. With a credit freeze, no one can access or view your credit report. This would also prevent a thief from opening a credit card in your name (because the company couldn’t pull your report and verify your score).

What if you’re applying for a mortgage but have a credit freeze in place? Rittman does think a credit freeze is a good idea in cases of possible identity theft, but cautions that “you’ll have to step in and unfreeze each or all of the bureaus that are frozen when applying for a mortgage.” This could take a few days, so build this time into your homebuying plans.

It’s not hard to get a free credit report. But don’t forget: Your credit report can affect everything from a mortgage to getting a new job, so you should make it a habit to keep an eye on your score.

Header Image Source: (Vlada Karpovich / Pexels)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.