Negative Amortization Loans: How They Work And When to Consider One

- Published on

- 5 min read

-

Amna Shamim Contributing AuthorClose

Amna Shamim Contributing Author

Amna Shamim Contributing AuthorClose

Amna Shamim Contributing AuthorAmna Shamim is a writer and digital marketing consultant who works with local and e-commerce businesses, ensuring they are easily findable online to and trusted by their clients. Her words have been featured in Glamour Magazine, Business Insider, Entrepreneur, Huff Post, Thrive Global, BUST, Paste, and other publications.

Amortization isn’t something you’re likely to think about every day. But how you handle your mortgage has a huge impact on everything from your day-to-day finances to what your life looks like in 5, 15, or even 30 years.

Spend wisely and you could be headed for financial security and freedom. Make careless mistakes and you could lose your home. Avoiding the worst-case scenario requires understanding the different types of loans you’re being offered and the benefits or drawbacks of each. So what are negative amortization loans and how can they impact your finances, right now and in the future?

We spoke with experts, ranging from experienced mortgage sales professionals to financial advisors, looked into what the Consumer Finance Protection Bureau and other resources advise, and broke it all down for you so you can make the decisions that are right for you and that put you on your path to financial freedom.

What is amortization?

Amortization is the process of paying off a loan in equal payments over a period of time —part of each payment goes toward the loan’s principal and the other part goes toward interest.

Mortgage loans are typically set up so that paying interest is prioritized. So that means you’ll pay more toward interest than principal at the start of the loan and then as you pay down the loan, you’ll put more toward principal.

For example, let’s say you take out a 30-year fixed mortgage for $250,000 at a rate of 4.5%. Your monthly payments remain at $1,266.71 throughout the entire life of the loan. On your first $1,266.71 payment, $970.50 goes toward interest, while $329.21 goes toward paying down the principal.

Gradually, over the course of the loan, the amount you pay toward the loan principal will overtake the amount you pay toward interest. Toward the end of paying off the loan, you’ll pay mostly principal and very little interest.

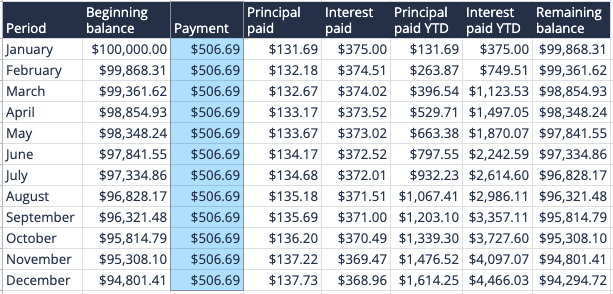

Here’s a typical amortization schedule for the first year of a loan.

- Amount of loan: $100,000

- Interest rate: 4.50%

- Months: 360

- Years: 30

- Payment amount: $506.69

Year 1 schedule:

Mortgages and car loan payments are two of the most common loans that use amortization. With a 30-year mortgage, you can expect to spend the first few years focusing on paying down the interest, and the remaining years paying down the loan principal. This is part of why paying off a mortgage quickly can save you so much money in interest payments.

What is negative amortization?

Negative amortization is when the borrower isn’t making sufficient interest payments to exceed the amount of interest accrued on the principal in a given period. These payments are usually lower than amortization payments but will not result in the loan being paid off in full by the end of the original agreed-upon payment schedule.

How does negative amortization work?

There are pros and cons to negative amortization, but there are definitely some facts you need to keep in mind.

When making negative amortization payments, you aren’t avoiding paying the interest; you’re just delaying it.

Interest is still accruing on the loan — but you, the borrower, aren’t paying it off as it accrues. Instead, it’s increasing the principal loan balance and will come due at some future point.

This is different from an interest-only loan, where the principal balance remains the same and the interest is paid in full.

If your mortgage is $100,000 and your fully-amortized payment is $1,000, with $600 going to interest and $400 toward the principal, the following month you’ll have $99,600 left of your principal balance. But with negative amortization, you may be paying only about $500 toward the principal and nothing toward the interest, resulting in $100,500 of debt the following month because you’ve accrued interest on the debt.

Instead of decreasing, with negative amortization, your debt increases every month because you aren’t paying enough to cover the interest and chip away at the principal.

Negative amortization payments can’t be a permanent situation as your debt is increasing, rather than decreasing; eventually, your loan will have to get recalculated.

Richie Helali, mortgage sales leader at HomeLight Loans, does not advise people to use negative amortization loans without a plan, clarifying:

“A negative amortization loan is not really intended for long-term personal use; it’s intended for somebody who’s going to own a home temporarily or for a short period of time. Most likely this is an investor who wants to do a fix and flip, so they can just have low monthly payments.”

What types of loans feature negative amortization?

While mortgages aren’t the only loans that might offer negative amortization, they are some of the most common. Two types of mortgages often feature negative amortization.

Payment option adjustable-rate mortgages are loans where the interest rate varies over the duration of the loan and you can choose to make a payment that is lower than the fully amortized payment.

With these mortgages, the interest rate is typically locked in for an initial period of three, five, or seven years, and then adjusts periodically thereafter (usually every six to 12 months). The initial interest rate is often lower than the current average interest rate for a fixed-rate loan.

With the loans, borrowers are allowed to decide how much of the interest portion they want to pay each month, and any interest that they don’t pay is simply added to the loan balance.

Graduated payment mortgages are a type of fixed-rate mortgages where the payments increase gradually over time from an initially low base rate to a higher final interest rate. The payments will typically increase by between 7% and 12% annually from their initial base payment until they reach the full monthly payment amount.

Not every state allows negative amortization mortgage options, especially since the subprime mortgage meltdown of 2008.

Why would you consider a negative amortization loan?

Although unpredictable or increasing interest rates and mortgage payments may sound unappealing upfront, there are some situations where they can be a good financial choice.

If you have short-term expenses that you need to cover and as a result don’t have as much ready cash during the next few years, negative amortization could make sense. In this case, with negative amortization, your principal payments will drop initially, buying you some breathing room while you cover the other expenses, but you should have a plan to refinance that loan before the high principal balance comes due.

Helali explains: “A negative amortization loan is not designed to say, ‘let me pay off my house’. It’s designed to say, ‘let me use my equity to allow me to stay in this home at a lower monthly payment for a short period of time.’”

Another situation where negative amortization may make sense is if you’re an investor who is flipping a house or a similar scenario where you know you won’t be in the house long. Rather than tie up your cash reserves in an asset you won’t be paying off fully, you can keep the liquidity to invest in improvements (resulting in a higher sales price) or in other investments.

The last case where negative amortization loans might make sense is when you earn a lot of money — but not in a steady manner. A negative amortization loan may make sense in a situation where it is being used as a method of cash flow management rather than a crutch of affordability, resulting in a home you can’t really afford.

Greg McBride, senior vice president and chief financial analyst at Bankrate.com, would recommend a negative amortization loan to “high-net-worth borrowers with sufficient income and assets and a large down payment. An entertainer or entrepreneur who sees the bulk of their income at one time of year or at very irregular intervals can use the loan to preserve cash flow in the months without income, and then make a significant payment against the principal in the months when income is rolling in.”

What are the drawbacks — why might you pass?

One of the reasons many people pass on negative amortization loans is because you’ll end up paying more (sometimes a lot more) on your house overall.

The ability to delay paying down the mortgage could more quickly lead to a scenario where you’re underwater on your loan. This can occur due to unforeseen circumstances impacting your cash flow or overall liquidity. It can also occur if the average interest rate outpaces your cost of living increases.

Some people make the mistake of being optimistic about their future earning potential and buying more house than they end up being able to afford in the future.

The Consumer Finance Protection Bureau recommends you pay off all the interest on your loans as soon as possible to avoid paying interest on your interest.

In a market where house prices are skyrocketing, McBride advises that “buyers should be more averse to employing any negative amortization loan because a plunge in home prices could be significant enough to offset even a healthy down payment. There just isn’t the margin of error in an inflated housing market that there is when home prices have languished for a while.”

How much more might you pay with a negative amortization loan?

Some borrowers are surprised by how much more they end up paying with a negative amortization loan. However, if you look at how quickly the unpaid interest and principal over just the first year, you can see how it quickly increases.

We’ll use the same numbers of $100,000 mortgage, 30 year loan term, and 4.5% interest rate as the example above so you can easily compare the numbers for the first year. You can also see how over just a few years, negative amortization loans can snowball into you owing $117,241.11 by the end of Year 7 on a $100,000 initial mortgage, despite having paid $8,400 already.

If you do decide to go with a negative amortization loan, they may not be easy to find. Since the subprime mortgage meltdown of 2008, very few lenders offer them and only to borrowers that meet certain criteria.

Header Image Source: (Lukasz Radziejewski / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.