What Happened to Housing in Previous Recessions? A Rundown

- Published on

- 8 min read

-

Chelsea Levinson Contributing AuthorClose

Chelsea Levinson Contributing Author

Chelsea Levinson Contributing AuthorClose

Chelsea Levinson Contributing AuthorChelsea Levinson, JD, is an award-winning content creator and multimedia storyteller with more than a decade of experience. She has created content for some of the world’s most recognizable brands and media companies, including Bank of America, Vox, Comcast, AOL, State Farm Insurance, PBS, Delta Air Lines, Huffington Post, H&R Block and more. She has expertise in mortgage, real estate, personal finance, law and policy.

The coronavirus pandemic has changed life as we know it, and it’s also left a big question on the minds of buyers, sellers, real estate agents, and homeowners alike: Are we facing a housing recession in the coming months?

With so much currently shifting in the world of real estate — from ping-ponging mortgage rates to massive legal restrictions on buying and selling homes — it’s impossible to say with any amount of certainty whether a housing recession is on the horizon.

But one thing we can do is take a look at past recessions, and see if they can give us clues about our present-day situation.

We spoke with top Michigan real estate agent William Frohriep, who boasts an impressive 49 years in the business. Frohriep has seen it all, from the oil crisis of the early ’80s to the Great Recession that hit the nation in 2007.

He walked us through what happened in real estate during past recessions, and what we might be able to expect from the housing market during the coronavirus pandemic. Here’s what you need to know.

Some background on recessions and housing

A recession happens when a country’s GDP (gross domestic product) declines for two or more quarters in a row.

American GDP represents the value of all the goods and services the U.S. produces during a period of time. To economists, it’s one of the most important indicators of economic health.

When Americans produce less and less goods and services over an extended period of time (six months or longer), the country enters a recession. When the country produces more goods and services over the same period of time, it’s called an economic expansion.

Recessions vary in length and severity. The average recession goes on for around 15 months, while the average economic expansion tends to last an average of 48 months.

So what happens with housing during recessions? Typically, housing isn’t hugely affected, and home prices remain relatively steady throughout a recession, give or take a small bump or decline (the one major exception being the Great Recession; more on that later).

That’s because no matter what the economy looks like, people need housing. And, as Frohriep explains, needs dictate most peoples’ real estate decisions more than the state of the economy.

“Usually, most homeowners I talk with have more of a need,” Frohriep shares.

“They need to be closer to work. They need an extra bedroom. They really need some extra space. Those are more the driving factors, I believe.”

Frohriep says that we can see this play out through home sale numbers: The number of homes that sell in a year tends to stay pretty consistent over time.

However, most real estate agents will also tell you there’s no such thing as a national housing market, and local markets tend to be affected by recessions in unique ways.

The two recessions of the early 1980s

The early 1980s got off to a rocky economic start, with two recessions happening back-to-back in the span of just three years.

These recessions were characterized by high inflation, tight Federal fiscal policy meant to control that inflation, and a global oil crisis on top of it all.

These two recessions had a major impact on Americans as they struggled simultaneously with high inflation, high interest rates, high unemployment, and high oil prices.

How housing was affected

So, what happened with real estate during that time?

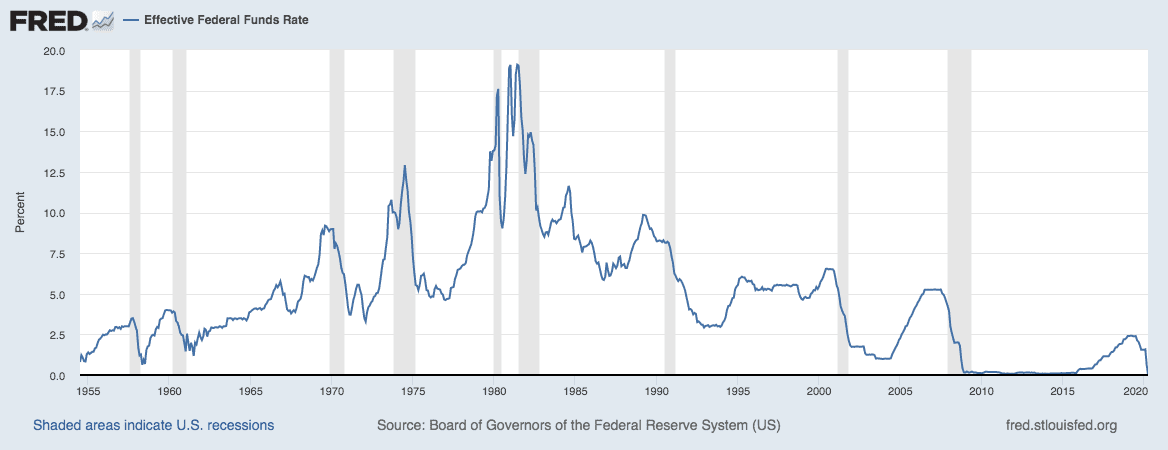

“From December of 1979 to January of 1980, the market changed nearly overnight,” Frohriep explains. “Interest rates were soaring. They hit a peak of about 17% or 18% by the end of 1982.”

And as mortgage rates were going up to numbers unseen before or since, homes were becoming significantly less affordable. Buyers dropped out of the market, no longer able to afford homes at such high rates.

Still, even with buyers dropping out of the market, home prices stayed relatively steady, showing moderate increases over the two periods of recession.

The early 1980s recessions by the numbers:

Recession of 1980 (January 1980 through July 1980):

- GDP: down 2.2%

- Unemployment: 7.8%

- Federal interest rates: ranged from 9% to 14%

- Mortgage rates: ranged from 12% to 16%

- Home prices: up 4.5%

Recession of 1981 to 1983 (July 1981 to November 1982):

- GDP: down 2.7%

- Unemployment: 10.8%

- Federal interest rates: ranged from 9% to 19%

- Mortgage rates: ranged from 14% to 18%

- Home prices: up 1.9%

Recession of the early 1990s

In 1990, another recession kicked off, after several years of the Fed steadily raising rates to once again fight inflation.

The economy slowed down, coinciding with global oil prices more than doubling when Iraq invaded Kuwait in the summer of 1990.

This recession was short, lasting just three-quarters of a year, from July 1990 through March 1991.

How housing was affected

During the early 1990s recession, home prices dropped slightly, by 0.9%. Besides the Great Recession, this is the only recession in modern history where home prices dropped.

However, a drop of less than 1% is pretty minor, and it’s relatively normal for home prices to fluctuate over time.

Overall, this quick recession didn’t impact real estate too significantly.

The early 1990s recession by the numbers

Early 1990s recession (July 1990 through March 1991):

- GDP: down 1.1%

- Unemployment: 7%

- Federal interest rates: ranged from 4% to 6%

- Mortgage rates: ranged from 9% to 10%

- Home prices: down 0.9%

Dot-com recession of 2001

The next recession hit in 2001, when the dot-com bubble burst. Here’s what happened:

At the time, the internet was the hottest new thing around. There was a tech gold rush, with investments pouring in for new internet companies. Tech company values were through the roof, creating an over-inflated stock market.

Then the Nasdaq (one of three major stock indices in the country; the other two are the S&P 500 and Dow Jones) lost over 75% of its value, dissolving a large portion of the massive investments — and investors — behind the companies.

Later in the year, the terrorist attacks of 9/11, coupled with massive accounting scandals at companies like Enron, crashed the stock market.

From 2000 to 2002, the S&P 500 lost 43% of its value. The stock market took more than a decade to fully recover from these events. The Nasdaq didn’t recover its peak 2000 numbers until 2015.

How housing was affected

The early 2000s recession was relatively short, totalling just eight months. Plus, it hit investors a lot harder than it hit most Americans. The GDP suffered a nominal loss of 0.6%.

In fact, as the stock market crashed, home values actually went up, rising 4.8% during the recession. One possible reason is that people began to see housing as a safer bet than buying stocks.

However, not every market fared so well. In San Francisco, the capital of tech, home prices slowed, with many formerly wealthy investors pulling out of the market.

Home sales also experienced a temporary lull in the wake of 9/11.

“I think there was a general fear of the unknown during that time,” Frohriep recalls. “I can tell you that the couple of weeks, even a couple months after September 11, our phones literally stopped ringing. And I think it was just fear and total uncertainty.”

Yet, according to Frohriep, the housing market quickly recovered in the following months and years. All in all, this recession ended up being mostly inconsequential for housing.

The dot-com recession by the numbers

March 2001 through November 2001

- GDP: down 0.6%

- Unemployment: 5.5%

- Federal interest rates: ranged from 6% to 6.5%

- Mortgage rates: 7%

- Home prices: up 4.8%

The Great Recession: 2007 to 2009

The Great Recession was unique because it was actually caused by a housing collapse, rather than housing being affected by other economic factors.

There were two main contributors to the Great Recession:

1. Mortgage lending requirements were too lax

During the lead-up to the Great Recession, many mortgage lenders were issuing risky loans to buyers who ultimately couldn’t afford to pay them back. In some cases, buyers never even had their income verified, yet were still able to get loans.

Mortgages were given to people with poor credit and no down payment, and to offset the risk, lenders charged them higher interest rates (this is known as a subprime mortgage). Many loans started at a super-low or 0% introductory rate, and then gradually, the interest rate would go up until the homeowner could no longer afford to pay.

Meanwhile, lenders were bundling up these mortgages into bonds, and then selling the bonds across global financial markets. When homeowners began to default on the loans they couldn’t afford, those bonds lost their value, and the financial system collapsed.

2. There was a huge flood of home inventory

In months before the Great Recession, homes were being built at a breakneck pace. This created an oversupply of homes, which made homes lose value as markets became much more buyer-centric.

Real estate speculators bought the overflow homes. And since you needed essentially no money down to buy a home (remember those risky loans with zero down?), there was little financial risk for them as they let the homes default.

This contributed to the number of foreclosures, as well as the financial collapse that put the banks in crisis.

How housing was affected

It’s no secret that the Great Recession was extremely hard on homeowners. It dragged on for 18 months and left 10% of Americans unemployed. Millions lost their homes, and home prices dove nearly 14%.

Another effect of the Great Recession? It caused millions of homeowners to go underwater on their homes, meaning they now owed more than the homes were worth. If you wanted to sell your home and were underwater, you had to take a loss to do it.

Further, the relationship between homeowners and mortgage lenders soured. Americans lost trust in the mortgage industry, blaming them for the financial ruin that affected so many people.

After the events of the Great Recession, new laws were passed to reign in the financial practices that caused the collapse, including the Dodd-Frank Wall Street Reform and Consumer Protection Act.

Today, the mortgage industry looks a lot different than it did before the Great Recession. Mortgage companies are stricter with their lending practices. Borrowing has become significantly safer, and regulations are constantly being added to keep lenders accountable.

Some even believe lending has become too constrictive now, locking out qualified buyers with non-traditional finances, such as those who are self-employed, or who might not have a lot of income but who own a lot of equity in their current homes.

All in all, the Great Recession significantly changed the face of lending in America, and made the mortgage industry safer, and more ethical. Although vestiges of mistrust persist between buyers and lenders, the mortgage industry is a far cry from what it used to be.

The Great Recession by the numbers

December 2007 through June 2009

- GDP: down 4.3%

- Unemployment: 10%

- Federal interest rates: ranged from 0% to 4%

- Mortgage rates: ranged from 5% to 6%

- Home prices: down 13.9%

What can we expect from the coronavirus recession?

Prior to the coronavirus pandemic, the U.S. was enjoying one of its longest and largest economic expansions in history.

This steady economic growth of more than a decade caused home prices to appreciate and the demand for homes to skyrocket. Prior to the coronavirus, this spring was gearing up to be extremely competitive for real estate.

There’s no way to know for sure if there will be a coronavirus recession, or what it will look like. Signs point to a likely recession, but it’s too early to tell, without at least two quarters (six months) worth of economic data to look at. This will be a wait-and-see recession.

There’s still so much we don’t know right now about how all of this will play out. However, it’s helpful to look at how this recession is not like the Great Recession, the most recent recession in our economy.

The differences between The Great Recession and the incoming recession

- Lending practices are a lot safer now. Mortgage companies no longer take on risky loans, making it unlikely that millions will fall underwater or lose their homes.

- There are better safeguards in place for homeowners. Early on in the coronavirus pandemic, the CARES Act was passed. It allows homeowners with government-backed loans to go into forbearance for 180 days. That means most people who are financially struggling won’t be foreclosed on. However, the flip side of this is that it’s created the largest surge in mortgage non-payments in history. Approximately 7% of homeowners are currently in forbearance.

- There’s way less inventory now, and higher demand for homes. Inventory of homes remains very low, and buyer demand is high. Of course, unemployment will temporarily disqualify some people from buying a home, but most in the industry believe home prices will remain relatively steady, thanks to low inventory. The bottom line is, there aren’t enough homes to go around. Even with fewer buyers in the market, it will remain a seller’s market unless something drastic happens.

We can’t say there will never be another housing collapse, but we can say that there are a lot more policies in place to prevent another one like we saw in the Great Recession.

What if you want to buy or sell during the coronavirus?

Despite the economic uncertainty during the coronavirus pandemic, now still might be the right time for you to buy or sell a home.

Of course, keep in mind that stay at home orders have changed how real estate deals are done. It’s common to face longer wait times to get a mortgage, and you can probably expect delays on inspections, appraisals, and anything that may require in-person signatures.

Ask your real estate agent to walk you through your state’s current laws and regulations. Agents are keeping up with minute-to-minute law changes and figuring out how to get the deal done, even when everything’s shut down.

Prepare yourself to be patient. These are unprecedented times, and you may be in for frustrations as you navigate a purchase or sale (or both!).

With all of that in mind, we asked Frohriep what buyers and sellers should look out for when making their decision about buying during a recession.

What buyers need to know during the coronavirus recession

“We have unprecedented low interest rates. If you can find a home and buy it, you’re going to have a rate that’s unheard of,” Frohriep says.

Still, he cautions, you have to navigate very low inventory. You may not have a lot of options, and that could mean making compromises on your must-have list.

You also need to make sure buying a new home is a financially sound decision for you right now.

- Do you have steady employment? With the economy on shaky ground, you should make sure your employment is rock-solid before you make such a huge financial decision. You don’t want to buy a home you won’t be able to afford in a few months if you’re laid off.

- Do you have money saved for a down payment? Many mortgage companies are tightening their lending requirements. That means you might have to make a bigger down payment than usual during the coronavirus pandemic, to decrease your lender’s risk.

- Is your credit in tip-top shape? Mortgage lenders are requiring higher credit scores than usual to offset the risk they’re taking on during the coronavirus pandemic. Some are even requiring a score higher than 700. Make sure your credit is in good shape if you want to get a mortgage right now.

Consult a trusted financial advisor and your real estate agent before buying a home in a recession.

What sellers need to know during the coronavirus recession

“The benefit of low inventory is, you can get a good price for your home. And when you’re buying your next home, you have a low interest rate,” Frohriep says.

That means you can potentially get the best of both worlds.

Yet keep in mind that you’ll also have to navigate lower inventory when buying your next home. Though if you’re trading up, you may be in luck, as starter homes are in higher demand than higher-priced homes.

As always, consult your trusted real estate agent before making any big decisions. Your agent is the most qualified person to help you navigate the ever-changing tide of the industry and the local nuances in your area.

Header Image Source: (Tom Rumble / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.