7 Tips to Use (Not Abuse) the Home Office Tax Deduction as WFH Rises

- Published on

- 5 min read

-

Melissa Rudy Contributing AuthorClose

Melissa Rudy Contributing Author

Melissa Rudy Contributing AuthorClose

Melissa Rudy Contributing AuthorMelissa Rudy is a seasoned digital journalist with 15 years of experience writing web copy, blog posts and articles for a broad range of companies. When she can’t buy or sell homes, she settles for the next-best thing: researching and writing about all things real estate-related.

Disclaimer: This blog post is meant to be used as a helpful guide and for educational purposes only. It is not to be taken as legal or tax advice. If you have a question about your taxes, please consult a skilled tax professional for guidance.

A massive transition to remote work in the U.S. has elevated intrigue around the home office tax deduction. Many people are wondering if their new pandemic WFH setups make them qualified for certain write-offs. However, most of the folks who packed up their desk plants and bobbleheads back in March won’t be able to claim the deduction — unless they are or have become self-employed.

In addition, the home office deduction is somewhat of an “honor system” write-off and one you’ll want to have good records for in the event of an audit. That said, if you qualify under current tax code, you should by all means claim it if doing so makes financial sense. Here are what some seasoned CPAs say are the main points of confusion about this popular deduction and what you should know.

1. Company employees need not apply.

Prior to the sweeping tax reform passed in 2017, W2 or “paycheck” employees were able to take the home office deduction to some extent if they used the space for their company’s convenience and claimed the deduction as an unreimbursed job expense. However, the Tax Cuts and Jobs Act (TCJA), which went into effect Jan. 1, 2018, suspended the home office deduction for employees at least through 2025.

As of this writing, the home office deduction is limited to what the IRS calls “self-employed taxpayers, independent contractors, and those working in the gig economy.” It’s aimed at people, say, running a small consulting business out of their home or freelancers who plant themselves in the same chair every day for their writing business. The fact that you’re telecommuting alone doesn’t qualify you for the deduction. You also must be self-employed.

If you find that you’re spending a good chunk of your own money on items you need to work from home, it couldn’t hurt to ask your employer about reimbursement.

2. Make sure your business meets the ‘PEP’ requirements.

If you’re self-employed or run a home-based business, there are three more conditions that must be met in order to cash in on the home office deduction, per the IRS.

Deltrease Hart-Anderson, EA, who has provided income tax services for small businesses in South Carolina for more than 20 years, calls it the “PEP” rule (Principal place of business, Exclusive use, and Profits).

Hart-Anderson helps us break it down:

Principal place of business

This rule requires you to prove that your home serves as your principal place of business. That might mean holding meetings with clients or customers (in person or virtually), doing computer work, answering emails, taking phone calls, creating and shipping products, or any other activities required to do your job. That’s not to say you can’t duck out every now and then to work at Starbucks, but the IRS is looking for substantial and regular use.

“The business space you deduct must be used strictly for business purposes, and it usually will not work if you are renting an office elsewhere,” says Gail Rosen, CPA, PC, who runs a boutique CPA firm that has been providing tax services for individuals and small business owners in New Jersey for over 35 years. “The home office cannot be for your convenience.”

Exclusive use

The second condition is that you must use your designated home workspace solely to perform your business duties. If you’ve converted a spare bedroom, dining room, garage, or even just a corner of a room into a place to work, you can generally take the home office deduction.

“Exclusivity is key,”” explains Hart-Anderson. “This space can’t double as your kids’ play space when you’re not doing business. Regular can mean essential and frequent. If you sporadically use your office in your home, then this is not a deduction for you.”

Profitable (or Profit-Seeking)

To qualify for the home office tax deduction, you must have a business that is profitable in the year for which you’re filing. If your business doesn’t qualify due to lack of profit in one year, you can carry over the deduction to the next year. “Hobbies are not profit-seeking endeavors and do not qualify for office use in home tax deductions,” says Hart-Anderson.

3. Pick a route: actual expenses or simplified method.

The IRS gives you two options for calculating the home office tax deduction: using your actual expenses or the “simplified method.”

Actual expenses

This method is based on your actual expenses associated with working from home, and is the more complicated method of the two. Hart-Anderson breaks it down for us:

Step 1:

Determine the square footage of the portion of the home you’re using for business, then divide that number by the total square footage of the entire home. This becomes your usage percentage. For example, if your home office is 300 square feet and your total home is 2,500 square feet, then your usage percentage is 12% (300 divided by 2,500).

Step 2:

Next, you’ll determine your actual home expenses, based on what is used directly for business and what is used for both business and personal purposes. If an expense is used 100% for business — such as a new desk for your office — then you’ll deduct 100% for the business. If an expense is used both for business and personally—such as a housekeeping service that also cleans other rooms— then you can only deduct 12% of that expense for business. The same goes for expenses that apply to the entire house. For example, if your mortgage interest is $15,000, then you will have a business deduction of $1,800 ($15,000 x 12%).

Simplified method

Keeping track of your home office expenses can be tedious and requires a lot of recordkeeping. So some taxpayers may instead opt for the simplified method. With the simplified method, you can deduct up to 300 square feet at $5 per square foot of space used in your home office, for a maximum home office deduction of $1,500.

Hart-Anderson offers an example: If you have a 200-square-foot home office, then your deduction would be $1,000 (200 x $5). If you have a 300-square-foot home office, then your deduction would be $1,500 (300 x $5). However if you have a 600-square-foot home office, then your deduction under this method would still be $1,500, the maximum allowed by law.

Your accountant or tax professional can help you crunch the numbers to determine which option will let you recoup the biggest deduction.

4. Understand which expenses qualify — and which ones won’t.

If you’ve decided to use the simplified method and take the $5 per square foot of office space, the process is simpler. You won’t need to worry about combing through all of your expenses and figuring out which ones are deductible, and will just deduct a single, flat amount. But if you think the actual expenses method will get you a bigger tax break, you’ll have to itemize your individual work-related expenses.

When figuring out your actual expenses, there will be two categories that are deductible: direct and indirect.

Direct expenses

These are expenses that are only for the part of the home where you work, and are 100% deductible. Some examples of direct expenses include:

- Painting your home office

- Repairing a water leak in the ceiling of the office

- Home office furniture, monitor, printer, etc.

Indirect expenses

These expenses are those that partly apply to your home office, but also apply to the remainder of the home. You can deduct these, but only at the percentage of the home taken up by your office or workspace. Some examples of indirect expenses include:

- Repairing your furnace or air conditioner (which impacts the whole house and not just your office)

- Real estate property taxes (note: If you’re also itemizing deductions on Schedule A, you can only deduct this once)

- Mortgage interest (note: If you’re also itemizing deductions on Schedule A, you can only deduct this once)

- Homeowner’s insurance

- Internet access

- Utilities (gas and electric, trash collection, water, cleaning services, a dedicated business phone line)

- Security system

- Depreciation (allowance for the wear and tear put on your home office)

What’s not covered?

Any expense related to an area of the home outside of the office isn’t deductible. For instance, you won’t be able to write off any portion of your master bath remodel, lawn care services, new patio, or kitchen repair.

Also, if you only worked in your home office for part of the year, you can only deduct your expenses for that time period. So if you didn’t start your business until June, you’ll only be able to deduct expenses for seven months of the year.

5. Know the exceptions for daycare facilities.

If you use your home to provide childcare services or to care for an adult over 65 years of age, you may be able to claim a deduction on the part of your home used to provide that service. The catch is the IRS requires you to have a “license, certification, registration, or approval as a daycare center or as a family or group daycare home under state law.”

Unlike a traditional home office, it’s likely that the areas of the home where you provide daycare services are also used by other people, both during and after your working hours. For that reason, you can only deduct your expenses for the amount of time that those spaces are used solely for your business.

6. Hang onto your receipts.

If you’re using the actual expenses method and itemizing your individual expenses, it’s a good practice to keep all of your receipts in case you’re ever audited by the IRS. “As with all business deductions, I recommend keeping all receipts for at least seven years,” says Hart-Anderson.

7. Use the correct forms.

If you’re self-employed or a business owner who qualifies for the home office deduction, don’t miss the chance to cash in on the tax savings.

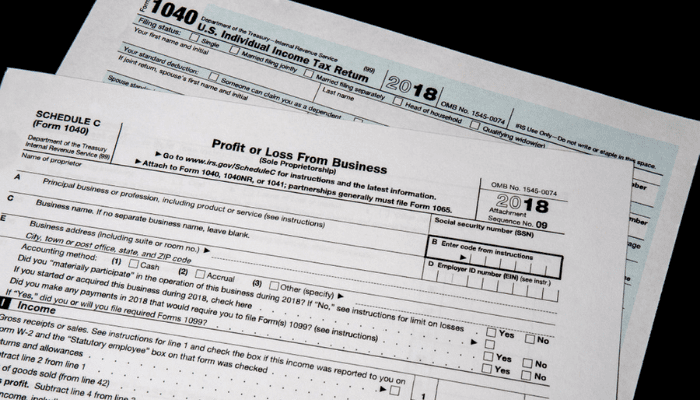

If you’ve opted to use the simplified method, you’ll take the flat-rate deduction on Schedule C (Form 1040), which reports profit or loss from a business.

If it’s worth the extra time and hassle to itemize your actual expenses, you’ll need to submit Form 8829 to calculate the total deduction, and then report that amount when you file your Schedule C.

Header Image Source: (Gian Paolo Aliatis / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.