Hard Money Lenders Boston: Fast Funding Options

- Published on

- 15 min read

-

Kelsey Morrison Former HomeLight EditorClose

Kelsey Morrison Former HomeLight Editor

Kelsey Morrison Former HomeLight EditorClose

Kelsey Morrison Former HomeLight EditorKelsey Morrison worked as an editor for HomeLight's Resource Centers. She has seven years of editorial experience in the real estate and lifestyle spaces. She previously worked as a commerce editor for World of Good Brands (eHow.com and Cuteness.com) and as an associate editor for Livabl.com. Kelsey holds a bachelor’s degree in Journalism from Concordia University in Montreal, Quebec, and lives in a small mountain town in Southern California.

Are you thinking about funding your next real estate project in Boston with a hard money loan? Whether you’re planning to renovate a brick townhouse in Dorchester or purchase a rental property in Southie, hard money lenders in Boston offer the speed and flexibility you need. Hard money lenders in Boston provide a viable alternative to conventional loans, which are especially convenient for those with tight project timelines, limited initial capital, or less-than-perfect credit.

Start Making Offers Without Waiting to Sell Your Home

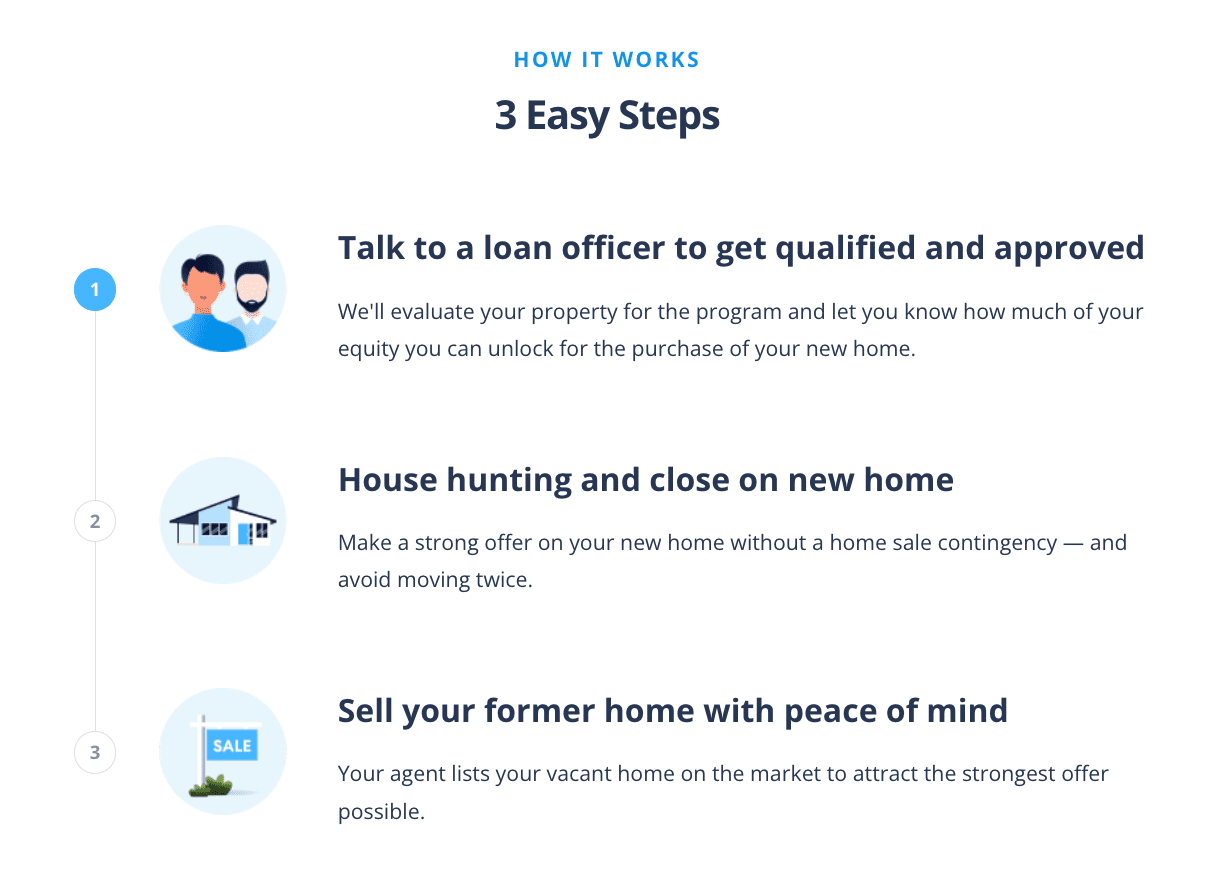

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

If you’re not an investor but need to bridge the gap between buying and selling a home, we have some alternatives to help you leverage your home’s equity. This article will guide you through the essentials of hard money lending in Boston, helping you determine whether this financial tool fits your real estate investment or home-buying objectives.

What is a hard money lender?

A hard money lender is a private individual or institution that offers hard money loans, which are named after the “hard” assets used as collateral, typically real estate. Instead of relying heavily on a borrower’s credit or income, these loans are approved based on the property’s value. These firms usually accommodate real estate investors like house flippers and rental property buyers.

To determine loan amounts, hard money lenders consider the after-repair value (ARV) or the estimated value of a property after all renovations and repairs are completed. They typically lend a percentage of the ARV to ensure a profitable investment and minimize risk.

These loans come with higher interest rates, ranging from 8% to 15% or more, and additional costs like origination fees, closing costs, and points. If a borrower fails to repay the loan, the lender can take possession of the property to recover their investment.

How does a hard money loan work?

If you’re a real estate investor in Boston seeking fast and flexible financing, working with hard money lenders could be the solution. Here’s a quick rundown of how hard money loans work in Boston:

- Short-term loan: These loans typically have a repayment period of six to 24 months, unlike the 15- or 30-year terms of conventional mortgages. Some lenders might offer extensions of up to 36 months if needed.

- Faster funding: When a quick deal is essential, hard money loans can be approved within days, compared to the 40 to 50 days usually required for a mortgage loan.

- Less focus on creditworthiness: Approval is less dependent on your credit score or income history and more on the property’s value.

- Greater scrutiny on the collateral: These loans require collateral, like a home, and are based on the loan-to-value ratio of the property.

- Non-traditional lenders: Hard money loans are typically provided by private investors or lending companies, not traditional banks.

- Traditional loan denial: They are sometimes used by those with poor credit who have been denied a mortgage but have significant home equity.

- Higher interest rates: Due to higher risk, these loans come with higher interest rates than traditional mortgages.

- Larger down payments: Depending on the property’s value and loan terms, borrowers may need to fork over a larger down payment, sometimes up to 20% to 30%.

- More flexibility: With fewer regulations, hard money lenders can set flexible credit scores and debt-to-income criteria. These loans can also help homeowners avoid foreclosure.

- Interest-only payments: Unlike traditional mortgages, hard money loans may allow for interest-only or deferred payments at first.

What are hard money loans used for?

Hard money loans are a go-to option for Boston real estate investors who need fast funding or might not qualify for a traditional bank loan. They’re flexible and can cover a range of situations. Let’s take a look at some of the most common ways people use them:

Flipping a house: For Boston-area house flippers, hard money loans provide quick access to cash for purchasing and renovating properties. These short-term loans enable investors to acquire properties in competitive markets, make necessary renovations, and resell them for a profit as soon as possible.

Buying an investment rental property: Investors seeking rental properties can use hard money loans to acquire them quickly, especially those in need of immediate repairs. Compared to traditional loans, hard money loans allow landlords to complete renovations and start renting out their units sooner.

Purchasing commercial real estate: Hard money loans are popular in commercial real estate transactions due to their flexibility and quick closing times. They are particularly useful when timing is crucial, making the difference between securing a valuable investment and missing out.

Looking for alternatives to traditional loans: Individuals with substantial home equity but poor credit or other disqualifying factors sometimes turn to hard money lenders. With these loans, qualification is based more on the asset’s value than the borrower’s credit score.

Facing foreclosure: Homeowners nearing foreclosure may use hard money loans to refinance their debts or buy time to sell the property. This can provide a temporary solution to avoid losing their home or receiving a foreclosure mark on their credit report.

How much do hard money loans cost?

The cost of hard money loans is typically higher than traditional loans due to the increased risk and convenience of quick funding. Here are some common costs associated with hard money loans:

- Interest rates: These can range from 8% to 15% or higher, based on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount as an origination fee.

- Closing costs: Additional fees at closing can include legal fees, appraisal fees, and other administrative costs.

- Points: Lenders might charge points (a percentage of the loan amount) upfront, adding to the initial cost.

You can use online hard money loan calculators to estimate your hard money loan costs.

Alternatives to working with hard money lenders

If you’re a Boston homeowner looking to leverage your home’s equity, here are some alternatives to hard money loans to consider:

Take out a second mortgage: A home equity loan or a home equity line of credit (HELOC) allows you to borrow against your home’s equity, often with lower interest rates compared to hard money loans.

Cash-out refinance your home: This option lets you refinance your existing mortgage and take out cash, typically at lower rates than hard money loans.

Borrow from family or friends: Loans from family or friends can offer flexible terms and potentially no interest, making it a cost-effective option.

Use a government-backed loan program: Programs from the FHA, VA, or USDA provide low down payments and reduced interest rates for eligible buyers.

Consider peer-to-peer loans: Peer-to-peer lending platforms connect you with individual investors offering loans, often with terms differing from traditional hard money loans.

Explore specialized loan programs: Look into loans tailored for fixer-uppers or investment property refinancing, which can replace an existing hard money loan.

Request a seller financing option: Some sellers may finance the sale themselves, offering lower closing costs and more lenient eligibility requirements.

How to buy before you sell

Sometimes, the perfect listing appears when you’re not even looking. Maybe it’s a single-family home in Allston with a spacious backyard or a two-bedroom condo in East Boston with picturesque harbor views. If you’re a Boston homeowner aiming to buy a new home before selling your current one, HomeLight offers an innovative solution to make the process smoother.

The Buy Before You Sell (BBYS) program allows you to leverage the equity in your current home to make a stronger, non-contingent offer on a new property. With this program, you can get your equity unlock amount approved within 24 hours, with no cost or obligation. This allows you to purchase your next home confidently and then sell your current one vacant, avoiding the inconvenience of moving twice.

Here’s how HomeLight Buy Before You Sell works:

While there is a flat fee based on the current home’s sold price, the potential savings in other areas can outweigh this cost. You might save on moving expenses, temporary housing, and even the purchase price of your new home. Moreover, HomeLight’s BBYS fees are generally lower than the interest rates on bridge loans, which currently range from 9.5% to 12%.

3 top hard money lenders in Boston

Boston’s real estate market moves fast, and having the right lender can make all the difference. Whether you’re flipping a property, funding a renovation, or need to close quickly, hard money loans offer speed and flexibility that traditional banks often can’t. Below, we’ve rounded up three of the top hard money lenders in Boston to help you find the right fit for your next deal.

TMD Capital

TMD Capital is a direct private lender specializing in financing non-owner-occupied residential and commercial properties. Established in 2019, the firm operates in 46 states, including Massachusetts, offering a diverse range of loan programs, including fix-and-flip, long-term rental, multi-family, new construction, and bridge financing.

With a focus on efficiency and investor needs, TMD Capital can close loans in as little as seven days. Their comprehensive approach combines speed, flexibility, and market expertise to support a wide range of real estate investment strategies.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Varies by loan program

TMD Capital has earned a 4.7-star rating on Google, with several clients praising the team for delivering strong value through competitive pricing and reliable service. Reviewers highlight a smooth loan process and appreciate that the staff executes exactly what is promised.

Many note the friendly, easy-to-work-with approach that makes transactions straightforward. Overall, clients recommend TMD Capital for dependable financing and a hassle-free experience.

Website: tmd-capital.com

Phone number: 800-571-7405

New Silver

New Silver, founded in 2018, helps real estate investors get fast, flexible funding while supporting local communities. Their data-driven platform, FlipScout, gives investors the insights they need to make smarter decisions.

Loans can go up to $15 million, and funding is typically available within five days, covering a wide range of projects. With a focus on speed and simplicity, New Silver makes it easier for investors to move quickly and get deals done.

Lending clientele: Residential real estate investors

Loan criteria: Up to 75% ARV

New Silver scored 4 out of 5 stars on Google from over 30 reviews. Clients’ experiences with this company appear to be mixed. Some reviewers praise the team for efficiency, innovative products, and a focus on client success, noting that they return for multiple deals and feel supported throughout the process.

Others, however, report frustrations with slow communication, repeated requests for documentation, and difficulty reaching the team. Overall, while some clients find the company reliable and forward-thinking, others caution that inconsistent service and responsiveness can create challenges.

Website: newsilver.com

Phone number: 855-844-5626

Raymond C. Green Companies

Raymond C. Green Companies, based in Boston, provides short-term financing to real estate and construction professionals across New England. As a regional direct lender with over 50 years of experience, the firm offers loan amounts ranging from $100,000 to $10 million, with maturities of up to two years.

Borrowers can request pre-approval letters, and closings are typically completed within three to seven business days. Payment structures are flexible, including interest-only options or payments built into the loan.

Lending clientele: Builders, developers, and real estate investors

Loan criteria: Up to 75% LTV

The Raymond C. Green Companies boasts a 4.9-star rating on Google from nearly 50 reviews. Clients praise their exceptional customer service, deep knowledge of the construction industry, and responsiveness to inquiries.

Many highlight the team’s reliability and integrity, noting that they felt confident and supported throughout the process. Others describe working with the company as smooth and positive, and highly recommend them for anyone seeking reliable real estate financing.

Website: raygreen.com

Phone number: 617-947-8070

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in Boston?

Deciding whether a hard money loan is right for you depends on your specific circumstances and real estate investment objectives. This type of financing is best suited for Boston real estate investors who need quick access to capital for projects with fast turnarounds or when traditional financing just isn’t feasible.

If you can handle the higher costs and shorter repayment terms, this type of funding can provide the flexibility needed to take advantage of lucrative opportunities in the Boston real estate market.

For homeowners looking to leverage their equity without the burden of high interest rates, consider HomeLight’s Buy Before You Sell program. This alternative allows you to make a competitive, non-contingent offer on a new home while paying a small flat fee, simplifying your move and potentially saving you money.

As with any major financial decision, it’s important to consider your long-term strategy and consult with a financial advisor to ensure it aligns with your overall investment goals. If you’re looking to connect with investor-friendly real estate professionals in Boston who have access to trusted hard money lenders, let HomeLight introduce you to top agents in your area who meet these criteria.

Header Image Source: (f11photo/DepositPhotos)

Editor’s note: This post is for educational purposes only and should not be considered financial advice. HomeLight encourages you to consult your own advisor.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.