Hard Money Lenders Cincinnati: Alternative Financing Options

- Published on

- 10 min read

-

Joseph Gordon EditorClose

Joseph Gordon Editor

Joseph Gordon EditorClose

Joseph Gordon EditorJoseph Gordon is an Editor with HomeLight. He has several years of experience reporting on the commercial real estate and insurance industries.

Cincinnati’s real estate market offers plenty of opportunities for investors. Whether targeting a rehab project in Over-the-Rhine or looking at commercial spaces downtown, finding the right financing is key. This is where hard money loans come in, offering a faster, more flexible solution than traditional lending options.

Hard money loans are favored by Cincinnati investors who need quick access to capital. These loans are typically secured by the property’s value rather than the borrower’s credit score, making them a practical choice for those looking to capitalize on the city’s vibrant real estate opportunities.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Editor’s note: This post is for educational purposes and is not intended to be construed as financial advice. HomeLight always encourages you to consult your own advisor.

What is a hard money lender?

A hard money lender provides short-term loans secured by real estate, catering primarily to investors such as house flippers and those purchasing rental properties. Unlike traditional lenders, hard money lenders focus on the property’s after-repair value (ARV)—the estimated property value after renovations. ARV is crucial in determining the loan amount, with the lender often offering a percentage of this value.

Interest rates for hard money loans are higher than conventional loans, reflecting the increased risk. If a borrower fails to repay the loan, the lender can foreclose on the property, which serves as collateral. This risk makes hard money loans a tool for experienced investors who understand the potential rewards and pitfalls.

How does a hard money loan work?

In Cincinnati, hard money loans offer a unique and flexible way to finance real estate investments. Here’s how these loans typically work:

- Short-term loan: Hard money loans are designed as short-term financing solutions, typically ranging from 6 months to a few years, depending on the lender and the project.

- Faster funding option: Unlike traditional mortgages, which can take 30 to 50 days to close, hard money loans can often be funded within days, making them ideal for time-sensitive deals.

- Less focus on creditworthiness: Hard money lenders are less concerned with your credit score and more focused on the property’s value, which makes it easier for some borrowers to qualify.

- More focus on property value: The loan amount is typically based on a percentage of the property’s after-repair value (ARV), ensuring the lender has sufficient collateral.

- Not traditional lenders: Hard money lenders are private individuals or companies, not banks or financial institutions, offering more flexibility in terms and conditions.

- Loan denial option: If the property doesn’t meet the lender’s criteria or the project seems too risky, the loan may be denied, regardless of your financial standing.

- Higher interest rates: Interest rates for hard money loans are higher than conventional loans, typically ranging from 8% to 15%, due to the increased risk taken by the lender.

- Might require larger down payments: Borrowers may need to put down 20%–30% of the loan amount upfront, depending on the lender’s requirements and the project’s risk profile.

- More flexibility: These loans often come with more flexible terms, allowing you to structure payments, repayment schedules, and even the overall loan amount to fit your project needs.

- Potential for interest-only payments: Some lenders offer interest-only payment options during the loan term, with the principal due at the end of the loan period.

What are hard money loans used for?

Hard money loans in Cincinnati are often utilized for a variety of real estate investment purposes. Here’s how they might be used:

- Flipping a house: For flipping homes, where speed is crucial, hard money loans offer quick access to funds, allowing investors to purchase, renovate, and resell a property quickly.

- Buying an investment rental property: Investors looking to buy rental properties can use hard money loans to quickly secure a property, particularly in competitive markets where traditional financing might take too long.

- Purchasing commercial real estate: Hard money loans can be a solution for acquiring commercial properties that need significant renovations or are not currently generating income, which might disqualify them from traditional financing.

- Borrowers who can’t qualify for traditional loans: Hard money loans can help those who don’t meet traditional lenders’ stringent requirements due to issues like a low credit score or high debt-to-income ratio.

- Homeowners facing foreclosure: For homeowners at risk of pre-foreclosure property sale, hard money loans can provide the necessary funds to pay off existing debts and avoid losing their property.

How much do hard money loans cost?

Hard money loans generally cost more than traditional loans due to the higher risk for lenders and the convenience of quick, flexible funding. Typical costs include:

- Interest rates: 8% to 15% or higher, based on risk assessment.

- Origination fees: 1% to 5% of the loan amount.

- Closing costs: Legal, appraisal, and administrative fees.

- Points: A percentage of the loan amount charged upfront.

Online calculators can help estimate these costs.

Alternatives to working with hard money lenders

If you’re a homeowner, rather than an investor, who is looking for a way to leverage your current home’s equity, here are a few options to consider:

- Take out a second mortgage: If you have substantial equity in your home, a home equity loan or home equity line of credit (HELOC) can provide the needed funds at a lower interest rate compared to a hard money loan.

- Cash-out refinance: This option allows you to refinance an existing property, pulling out cash to finance your new investment. It often comes with lower interest rates than hard money loans.

- Borrow from family or friends: A personal loan from family or friends can offer flexible repayment terms and potentially lower or no interest rates, making it a more affordable option.

- Use a government-backed loan program: Programs offered by the FHA, VA, or USDA can assist in purchasing homes with lower down payments and reduced interest rates.

- Peer-to-peer loan: These loans are provided by individual investors through lending platforms like Funding Circle, functioning similarly to hard money loans but often with different terms.

- Specialized loan programs: Consider specialized loans for fixer-uppers or investment property refinancing if you already have a hard money loan and seek to replace it.

- Request a seller financing option: In some cases, sellers may agree to finance the purchase themselves, which can result in lower closing costs and less stringent eligibility requirements.

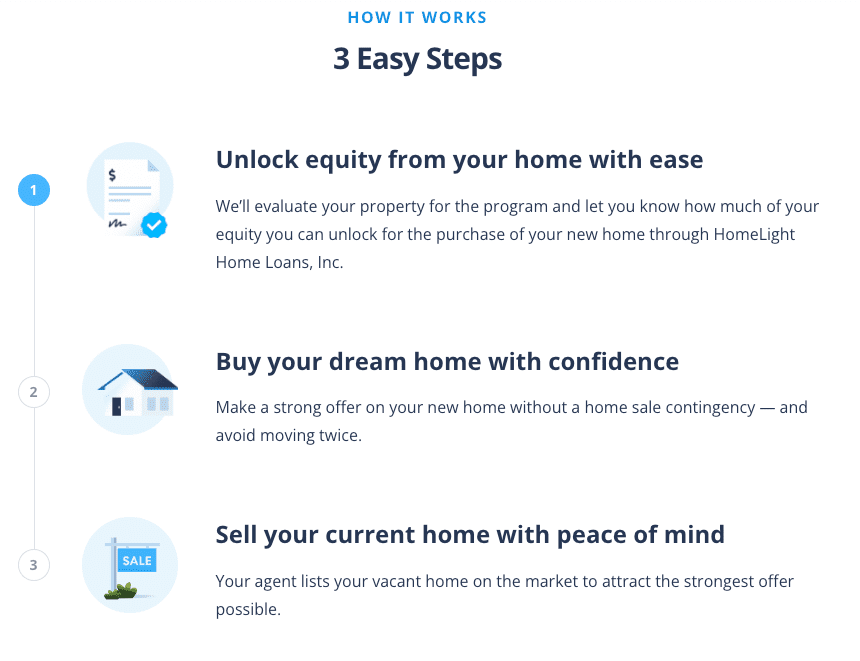

How to buy before you sell

HomeLight’s Buy Before You Sell program offers a unique solution for homeowners who want to buy a new home before selling their current one. This program provides a bridge loan that covers the cost of your new home, allowing you to move in without the stress of selling first.

The Buy Before You Sell (BBYS) program allows you to leverage the equity in your existing home to make a stronger, non-contingent offer on a new property. If your home qualifies, you can get your equity unlock amount approved in 24 hours or less, with no cost or commitment required. Once approved, you can confidently purchase your next home and then sell your current one vacant, avoiding the hassle of moving twice.

Here’s how HomeLight Buy Before You Sell works:

Although there’s a flat fee of 2.4% of your current home’s sold price, the potential savings you could see in other areas might outweigh the cost. For example, you might save on moving expenses, temporary housing, and even the final purchase price of your new home. On top of that, HomeLight’s BBYS fees are typically much lower than the interest rates on bridge loans, which currently range from 9.5% to 12%.

3 top hard money lenders in Cincinnati

Traditional lenders might not be the solution for every real estate investment. If you’re looking to move quickly and capitalize on an opportunity, explore the hard money lending options available in Cincinnati.

Dayton Capital Partners

Dayton Capital Partners, founded by seasoned real estate investors Darrin Carey and Joe Davidson, is located in Dayton, Ohio. The company offers private money for rehab loans, hard money loans, and transactional funding, specializing in 1-4 family and multifamily properties.

Lending clientele: Real estate investors

Loan criteria: 70% Loan-to-Value (LTV)

Dayton Capital Partners has a Google rating of 4.0 based on more than 20 reviews.

937-240-1805

Secure Lending, Inc.

Secure Lending, Inc. offers competitive rates for home purchase loans and refinancing options. They boast fast funding, often within 30 days, and provide tools for rate comparison, property evaluation, and pre-approval to help clients make informed decisions.

Lending clientele: Homebuyers and real estate investors

Loan criteria: Up to 90% LTV

Secure Lending, Inc. boasts a Google rating of 4.5 with over 100 reviews.

800-705-4308

Tidal Loans

Texas-based Tidal Loans services 45 states, including Ohio. It offers a variety of residential hard money loan options, including fix-and-flip, new construction, rental property, multi-family, commercial, and vacation rental.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Up to 70% of the ARV

Tidal Loans holds a 4.9-star Google rating with over 70 reviews.

832-757-1262

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in Cincinnati?

Working with a hard money lender in Cincinnati can be a smart choice for investors who need fast, flexible financing. These loans are beneficial for those involved in property flips, rental investments, or commercial real estate projects that might not qualify for traditional loans.

Since hard money loans are based on property value rather than credit history, they offer a way to secure funding quickly, allowing you to capitalize on opportunities in Cincinnati’s real estate market.

However, if you’re a homeowner looking to tap into your home’s equity without the higher interest rates and shorter terms that come with hard money loans, HomeLight’s Buy Before You Sell program might be a better fit. This program allows you to purchase your next home before selling your current one, making the transition smoother and less stressful. Carefully consider your financial situation and real estate goals to decide which option best meets your needs.

Header Image Source: (Jp Valery / Unsplash)

- "What is ARV and how is it calculated?," Rehab Financial Group (June 2023)

- "A Comprehensive Guide to Common Terms Used in Hard Money Lending," LinkedIn, Joseph Walker (September 2023)

- "Why Do Hard Money Lenders Require A Down Payment?," RCN Capital (April 2024)

- "What Are The Costs Involved In A Hard Money Loan?," NorthWest Private Lending (March 2024)

- "What are the Closing Costs of a Hard Money Loans?," Marquee Funding Group (January 2022)

- "What are Points on a Hard Money Loan?," LinkedIn, Blaise Brewer (December 2021)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.