Secure Your Investment: Hard Money Lenders Florida

- Published on

- 12 min read

-

Sam Dadofalza Associate EditorClose

Sam Dadofalza Associate Editor

Sam Dadofalza Associate EditorClose

Sam Dadofalza Associate EditorSam Dadofalza is an associate editor at HomeLight, where she crafts insightful stories to guide homebuyers and sellers through the intricacies of real estate transactions. She has previously contributed to digital marketing firms and online business publications, honing her skills in creating engaging and informative content.

Are you looking to jumpstart your next real estate project in the Sunshine State with a hard money loan? From renovating a historic home in St. Augustine to securing an investment property in Orlando, hard money lenders in Florida can provide the financial flexibility you need. For individuals with tight deadlines, limited budgets, or less-than-perfect credit, these loans offer a practical alternative to traditional financing.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Meanwhile, if you’re a homeowner who needs to bridge the timing gap between buying and selling a home, we’ll discuss alternatives to help leverage your home’s equity. This guide will cover the essentials of hard money loans in Florida, giving you the know-how to decide if this financial option aligns with your real estate goals.

What is a hard money lender?

A hard money lender in Florida is a private individual or company that provides short-term loans secured by real estate. They usually look at the property’s potential when evaluating applications, unlike traditional lenders who focus on your credit score and income history. They often accommodate house flippers and rental property investors who need quick access to cash and flexible loan terms.

To determine loan amounts, hard money lenders use after-repair value (ARV), the estimated value of a property after renovations. They lend a percentage of that ARV to ensure the investment’s security and profitability.

Interest rates for hard money loans range from 8% to 15% or more, with repayment periods between 6 to 24 months. Costs can include origination fees, closing costs, and points. Failure to repay can result in the lender seizing the property to recover their investment.

How does a hard money loan work?

If you’re investing in Florida real estate and need fast, flexible financing, going with a hard money lender could be a smart move. Here’s a quick rundown of how hard money loans work:

- Short-term loan: These loans typically have a repayment period of six to 24 months, unlike the 15- or 30-year terms of conventional mortgages. Some lenders might extend the term up to 36 months if needed.

- Faster funding: Hard money loans can be approved within days, compared to the 40 to 50 days typical for a mortgage loan. This makes them ideal for quick transactions.

- Less focus on creditworthiness: Approval relies less on your credit score or income history and more on the property’s value. This can be beneficial for those with imperfect credit.

- Greater scrutiny on collateral: These loans require collateral, such as a home, and are based on the loan-to-value ratio of the property. The property’s potential after-repair value (ARV) is crucial.

- Non-traditional lenders: Individual investors or private lending companies usually provide hard money loans, not traditional banks. This can result in more personalized lending terms.

- Loan denial: These loans are often used by those with poor credit who have been denied a mortgage but possess significant home equity. It offers an alternative route to financing.

- Higher interest rates: Due to higher risk, these loans have higher interest rates than traditional mortgages. Borrowers should be prepared for this increased cost.

- Larger down payments: Borrowers may need to provide a larger down payment, sometimes up to 20% to 30%, depending on the property’s value and loan specifics.

- More flexibility: With less government regulation, hard money lenders in Florida can set flexible credit scores and debt-to-income (DTI) criteria.

- Potential for interest-only payments: Unlike traditional mortgages, hard money loans may allow for interest-only or deferred payments initially. This can help manage cash flow during a project’s early stages.

What are hard money loans used for?

Hard money loans are great for specific financing needs in Florida’s real estate market. They’re especially popular with investors who need fast cash or can’t get a traditional bank loan. Here’s a look at some common ways people use them:

Flipping a house: If you plan to flip homes, hard money loans provide quick access to funds for buying and renovating properties. They help flippers quickly acquire homes, make necessary repairs, and sell them for profit in a short period.

Buying an investment rental property: If you’re looking to purchase rental properties, use hard money loans to secure properties quickly, especially those needing urgent repairs. Compared to traditional loans, hard money loans allow you to complete renovations and start generating rental income sooner.

Purchasing commercial real estate: In commercial real estate, hard money loans are popular because they’re flexible and close fast. They’re perfect if you need to move quickly to grab a valuable property and don’t have time to wait on a traditional loan.

Looking for alternatives to traditional loans: If you have substantial home equity but poor credit, a hard money lender can provide the solution you’re looking for. These loans focus on your property’s value rather than your credit score, giving you a way to secure financing when traditional loans aren’t an option.

Facing foreclosure: If you’re at risk of foreclosure, use hard money loans to refinance your debts or buy time to sell your property. This option can help avoid foreclosure and the negative impact it has on credit reports.

How much do hard money loans cost?

The cost of hard money loans is generally higher than traditional loans due to the increased risk and quick, less restrictive funding. Here are some typical costs:

- Interest rates: These can range from 8% to 15%, depending on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount as an origination fee.

- Closing costs: Additional fees at closing can include legal fees, appraisal fees, and other administrative fees.

- Points: Lenders might charge points (a percentage of the loan amount) upfront, adding to the initial cost of obtaining a loan.

There are many online hard money loan calculators available to help estimate these costs.

Alternatives to working with hard money lenders

Let’s say you’re not an investor, but a Florida homeowner looking to leverage your current home’s equity. Here are a few options you might want to consider:

Take out a second mortgage: If you have a significant amount of equity, a home equity loan or home equity line of credit (HELOC) could provide the necessary funds at a lower interest rate compared to a hard money loan.

Cash-out refinance your home: This option allows you to refinance an existing property, withdrawing cash to fund your new investment. It usually comes with lower interest rates than hard money loans.

Borrow from family or friends: A personal loan from family or friends can offer flexible repayment terms and potentially lower or no interest rates, making it a more cost-effective option.

Use a government-backed loan program: Programs offered by the FHA, VA, or USDA can assist in purchasing homes with lower down payments and reduced interest rates.

Consider a peer-to-peer loan: These loans are put forward by individual investors through lending platforms like LendingClub or Prosper, functioning similarly to hard money loans but often with different terms.

Explore specialized loan programs: Consider specialized loans for fixer-uppers or investment property refinancing if you already have a hard money loan and want to replace it.

Request a seller financing option: In select cases, sellers may agree to finance the purchase themselves, which can result in lower closing costs and less stringent eligibility requirements.

How to buy before you sell

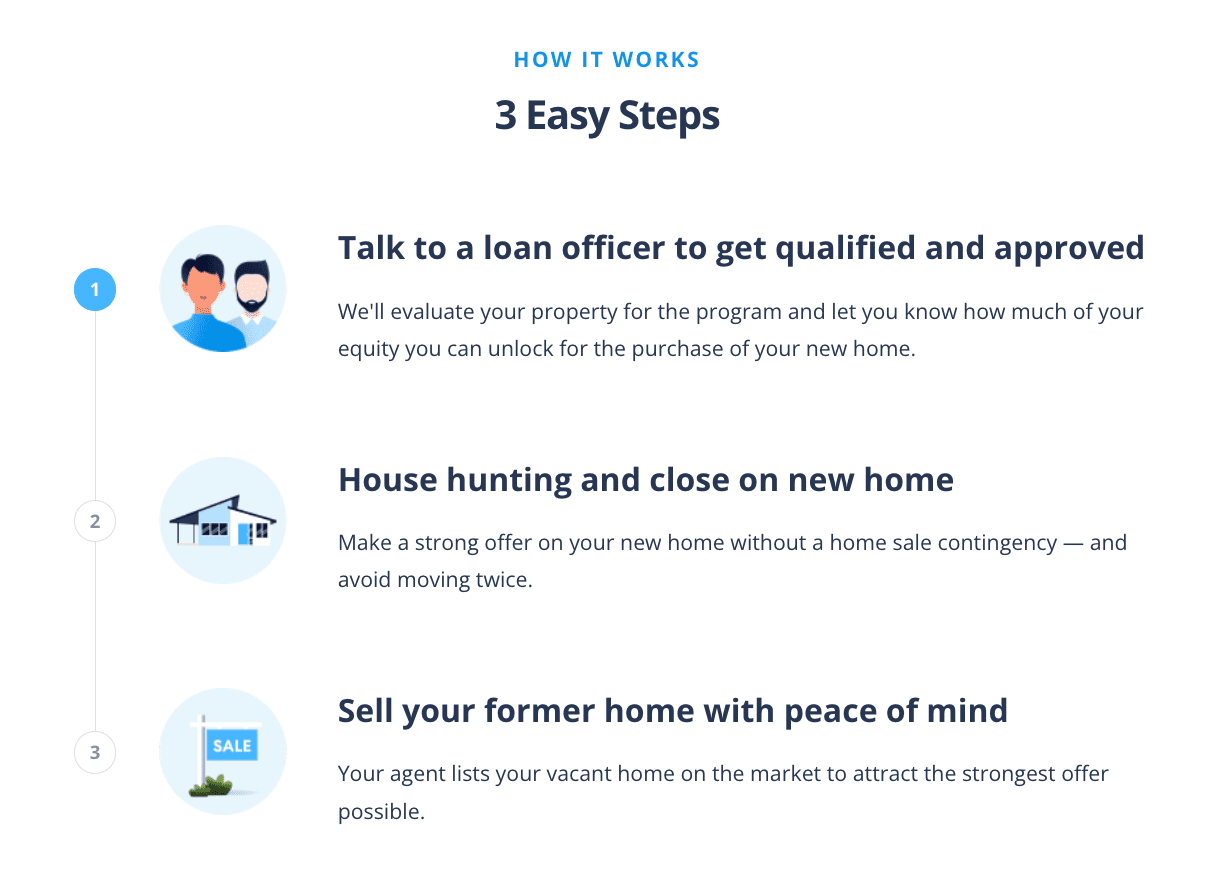

Imagine finding the perfect home just when you least expect it — a cozy bungalow in a sought-after neighborhood or a sleek downtown condo. For Florida homeowners wanting to buy a new home before selling their current one, HomeLight’s Buy Before You Sell (BBYS) is an ideal solution.

This program allows you to unlock the equity in your existing home to make a competitive, non-contingent offer on a new property. If your home qualifies, you can receive approval for your equity unlock amount in 24 hours or less, with no upfront costs or obligations. This enables you to purchase your next home confidently, sell your current one after you move, and avoid the stress of moving twice.

Here’s how HomeLight Buy Before You Sell works:

The program charges a flat fee based on your current home’s sale price, but its benefits tend to outweigh this cost. Savings on moving expenses, temporary housing, and the potential to secure a better deal on your new home are just a few advantages. Plus, HomeLight’s BBYS fees are typically lower than the interest rates on bridge loans in Florida, which currently range from 9.5% to 12%.

3 top hard money lenders in Florida

Finding the right hard money lender can make all the difference when investing in Florida real estate. The right lender helps you move quickly on deals, secure funding for renovations, and maximize your returns. Here are three top hard money lenders in Florida to consider for your next project.

A to Z Capital Lending

A to Z Capital Lending, based in Boca Raton, is a full-service lender and broker that provides comprehensive mortgage solutions. The firm specializes in hard money loans for real estate investors, offering financing from $50,000 to over $3 million. Loans typically close within seven to ten days, allowing investors to act quickly on opportunities.

With no minimum credit score requirements, their financing is accessible to a broad range of borrowers. Backed by extensive market expertise, A to Z Capital supports both residential and commercial real estate investments across Florida.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Up to 75% LTV

Receiving the highest praises from past clients, A to Z Capital Lending earned a 4.9-star rating on Google. According to reviews, the company is a trusted partner for real estate financing, as the team consistently delivers excellent rates and favorable terms.

Some highlight the company representatives’ professionalism, expertise, and dedication to making deals happen smoothly. Other investors consider them as the go-to choice for reliable, efficient financing solutions.

Website: atozcapitallending.com

Phone number: 561-609-6699

Hard Money Loan Solutions

Based in Delray Beach, Hard Money Loan Solutions delivers a comprehensive suite of private hard money financing options tailored for real estate investors, including rehab, fix-and-flip, bridge, and commercial loans. The company serves a wide range of project sizes, offering loan amounts from $100,000 to more than $100 million.

With flexible terms ranging from one to five years, the firm is positioned to accommodate both short-term opportunities and longer investment horizons. Their streamlined process allows borrowers to secure funding quickly, often closing within just one to two weeks.

Lending clientele: Residential and commercial real estate investors, as well as homeowners and foreign nationals

Loan criteria: Up to 65% of the as-is value or purchase price

Hard Money Loan Solutions boasts a 5-star rating on Google, with many commending the employees for their professionalism, prompt responses, and excellent customer service. Reviewers say the staff is committed to making the lending process smooth from start to finish.

Many highlight how clearly the team explains each step, adding confidence to their investment decisions. With consistent praise for reliability and expertise, clients strongly recommend giving the company an opportunity when seeking a hard money loan for their properties.

Website: hardmoneyloansolutions.com

Phone number: 561-707-1753

Capital Funding

Located in Boca Raton, Capital Funding offers a robust range of private lending solutions designed to support residential and commercial real estate projects of varying scales. The company provides loan sizes from $250,000 up to $25 million, giving investors the flexibility to pursue both modest renovations and large development opportunities.

With terms spanning 12 to 24 months, borrowers can tailor their financing to the specific needs and timelines of their investments. Capital Funding is known for its efficiency, often closing deals within 3 to 14 days from deposit.

Lending clientele: Residential and commercial real estate investors, plus homeowners and foreign nationals

Loan criteria: Up to 65% LTV

Capital Funding earned 4.7 stars on Google, with many reviewers praising them for their professionalism, knowledge, and a genuine desire to help their investors succeed. Some note how representatives took the time to walk them through each step of the loan process with clarity and professionalism.

Others emphasize that the proposals offered were more than fair and reflected a genuine desire to help clients succeed. Overall, clients express deep appreciation for the support and guidance they received from the Capital Funding team.

Website: capitalfundingfinancial.com

Phone number: 866-999-2011

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in Florida?

The decision to use a hard money lender in Florida should be based on your unique circumstances and real estate investment goals. This type of financing is best suited for real estate investors who need quick access to capital, whether it’s for flipping a property or securing a rental investment.

If you’re comfortable with higher interest rates and shorter repayment terms, hard money loans can offer fast, flexible funding for time-sensitive real estate opportunities in the Florida market.

But if you’re a homeowner looking to leverage your home’s equity without taking on high interest rates, HomeLight’s Buy Before You Sell program is a compelling alternative. The program allows you to make a non-contingent offer on your next home by unlocking your existing home’s equity. It involves a small flat fee, unlike the high costs of hard money loans.

As with any significant financial decision, it’s important to consider your long-term strategy and consult with a financial advisor to make sure your choices align with your overall investment goals. If you’re looking to connect with investor-friendly real estate agents in Florida who have connections to trusted hard money lenders, let HomeLight introduce you to top professionals in your area who fit that criteria.

Header Image Source: (Eric Ardito/ Unsplash)

Editor’s note: This post is for educational purposes only and should not be considered financial advice. HomeLight encourages you to consult your own advisor.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.