Hard Money Lenders Idaho: What You Need to Know

- Published on

- 12 min read

-

Joseph Gordon, EditorClose

Joseph Gordon Editor

Joseph Gordon, EditorClose

Joseph Gordon EditorJoseph Gordon is an Editor with HomeLight. He has several years of experience reporting on the commercial real estate and insurance industries.

-

Sam Dadofalza, Associate EditorClose

Sam Dadofalza Associate Editor

Sam Dadofalza is an associate editor at HomeLight, where she crafts insightful stories to guide homebuyers and sellers through the intricacies of real estate transactions. She has previously contributed to digital marketing firms and online business publications, honing her skills in creating engaging and informative content.

Finding quick real estate financing in Idaho can be challenging, especially when traditional loans are not an option. This is where hard money loans come into play. This type of financing offers a quicker, more flexible alternative for those looking to invest in properties without the lengthy approval processes of conventional lenders.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

This guide will explore the ins and outs of hard money loans in Idaho. From what hard money lenders do to the specifics of loan costs and alternative funding options, we’ve got you covered, whether you’re an investor or a homeowner looking for a new profitable venture.

What is a hard money lender?

A hard money lender provides short-term, asset-based loans, primarily to real estate investors, like house flippers and rental property owners. Unlike traditional lenders in Idaho, hard money lenders focus more on the property’s value rather than the borrower’s credit score. They determine loan amounts based on after-repair value (ARV), the property’s estimated value after renovations.

Interest rates for hard money loans are typically higher than traditional loans, ranging from 8% to 15%, with additional fees and costs. If the borrower can’t pay the loan back, the lender can take the property, which is why it’s important to have a solid plan for how to pay it off. Hard money loans in Idaho offer a fast, flexible financing solution but come with higher risks and costs.

How does a hard money loan work?

Hard money loans in Idaho offer a flexible financing option for real estate investors. Here’s how they typically work:

- Short-term loan: These loans usually have a term of 12 months, much shorter than a standard 30-year mortgage.

- Faster funding option: Approval and funding can take as little as a few days, compared to the typical 30 to 50 days for conventional loans.

- Less focus on creditworthiness: Unlike traditional loans, hard money lending places far less weight on the borrower’s credit score.

- Greater emphasis on collateral’s value: The primary consideration is the property’s loan-to-value ratio and its potential after-repair value.

- Non-bank lenders: These loans come from private investors or companies, not banks or credit unions.

- Loan denial: If the property doesn’t meet the lender’s criteria, the loan can be denied, regardless of the borrower’s financial status.

- Higher interest rates: Interest rates can range from 8% to 15%, reflecting the higher risk involved.

- Larger down payments: Borrowers may need to put down 20% to 30% of the property’s value.

- More flexibility: Terms can be more negotiable than those of traditional loans, allowing for customized solutions.

- Interest-only payments: Some hard money loans allow for interest-only payments during the loan term, with the principal due at the end.

What are hard money loans used for?

Hard money loans in Idaho can be used in a variety of real estate scenarios. Here are some of the most common uses:

- Flipping a house: Ideal for flipping homes, where quick funding is important to buy, renovate, and sell properties for a profit

- Buying an investment rental property: Useful for purchasing rental properties, allowing investors to secure and rehab the property swiftly

- Purchasing commercial real estate: Helpful when buying commercial properties needing renovations or quick turnarounds

- Exploring alternative financing: Beneficial for those with low home equity or poor credit who need financing options other than traditional loans

- Facing foreclosure: Ideal for those who want to avoid foreclosure by refinancing or catching up on payments

How much do hard money loans cost?

The cost of hard money loans in Idaho is typically higher than traditional loans. Here are some typical costs associated with hard money loans:

- Interest rates: These can range from 8% to 15% or higher, depending on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount as an origination fee.

- Closing costs: Additional fees at closing can include legal fees, appraisal fees, and other administrative costs.

- Points: Lenders might charge points or a percentage of the loan amount upfront, which can add to the initial cost of obtaining a loan.

Use online hard money loan calculators to estimate your costs.

Alternatives to working with hard money lenders

If you’re an Idaho homeowner looking for a way to leverage your current equity, here are a few options to consider:

- Take out a second mortgage: A home equity loan or line of credit can provide the needed funds at a lower interest rate than a hard money loan.

- Cash-out refinance your home: This option allows you to refinance an existing property, pulling out cash to finance your new investment.

- Borrow from family or friends: A personal loan from family or friends can offer flexible repayment terms and potentially lower or no interest rates.

- Use a government-backed loan program: FHA, VA, or USDA programs can help buyers purchase homes with lower down payments and reduced interest rates.

- Apply for a peer-to-peer loan: These loans are provided by individual investors through lending platforms. They function like hard money loans but often have different terms.

- Explore specialized loan programs: If you already have a hard money loan and want to replace it, consider specialized loans for fixer-uppers or investment property refinancing.

- Request a seller financing option: Sometimes, sellers may agree to finance the purchase, resulting in lower closing costs and less stringent eligibility requirements.

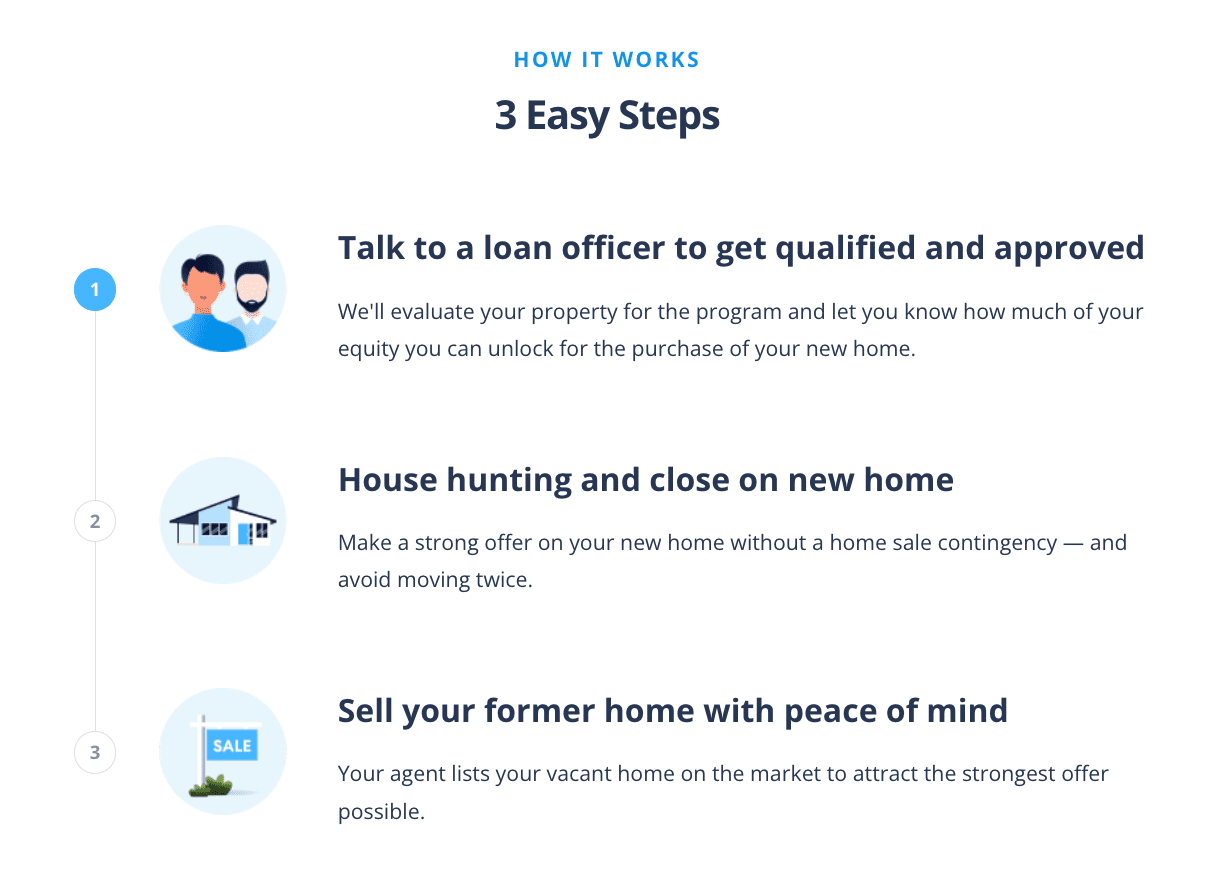

How to buy before you sell

HomeLight’s Buy Before You Sell program offers a seamless way to buy a new Idaho home before selling your current one. It provides the funds needed to purchase your new home, allowing you to move without the pressure of selling first.

The process involves securing a short-term loan to cover your new home’s down payment and closing costs. Once you’ve moved, you can focus on selling your old Idaho house at the best possible price.

The program facilitates a seamless buy-sell transaction, avoiding the need to get temporary housing and helping you fetch a better price for your old home, as it’s cleaned and staged properly. The costs are competitive, with rates that typically range from 9.5% to 12%.

With HomeLight’s program, you can confidently buy a new home before selling your current one, making the transition smoother and more efficient. Here’s how HomeLight Buy Before You Sell works:

3 top hard money lenders in Idaho

Traditional lenders might not be the solution for every real estate investment. If you want to move quickly and capitalize on an opportunity, explore the hard money lending options available in Idaho.

Northwest Private Lending

Northwest Private Lending helps real estate investors in Idaho with flexible, equity-based lending solutions. It specializes in hard money loans that make it possible to buy cash-only properties or deals that traditional lenders won’t finance. Its services cover everything from fix-and-flip and bridge loans to construction financing and cash-out refinances, making it easier for investors to get deals done.

Lending clientele: Residential and commercial real estate investors

Loan criteria:

- 80% max LTV for the purchase price on a fix and flip

- 75% or lower LTV for the purchase of an investment property

- 70% or lower LTV for the refinance of an investment property

- 50% LTV for the purchase or refinance of bare land

- 100% LTV loans available with additional collateral / cross-collateralization of other investment properties.

Northwest Private Lending has been accredited with the Better Business Bureau (BBB) since 2018 and earned a high A+ rating. It achieved a perfect 5-star rating on Google, as clients commend its professional services.

According to online reviews, the company is a trusted partner for experienced house flippers. Clients highlight not only the competitive rates but, more importantly, the company’s ability to close deals quickly, an essential factor in a fast-moving market. They appreciate how the team consistently exceeds expectations, making them a go-to choice for reliable, efficient private lending.

Website: nwprivatelending.com

Contact number: 503-941-5473

Payette Financial Services

Payette Financial is a hard money lender that specializes in providing financing solutions for complex transactions often declined by traditional lenders. Serving the western U.S., they provide fast funding to borrowers in Idaho, Arizona, Colorado, Montana, Nevada, New Mexico, Oregon, Utah, Washington, Wyoming, and beyond.

They can deliver cash in as little as 10 days and lend on nearly any commercial property, whether it’s undeveloped or developed land, industrial, retail, mixed-use, warehouses, self-storage, shopping centers, hotels, office buildings, or multifamily units with five or more residences.

Lending clientele: Commercial real estate investors

Loan criteria: Loans from $25,000 to $2.5 million with interest rates ranging from 8% to 13%, depending on collateral and terms.

With limited reviews, Payette Financial Services earned a 4.2-star rating on Google. Some commend the consistently positive experience they received from the company. They praise the team’s smooth and efficient funding process, clear communication, and attentiveness to project details.

Even with more complicated deals, clients note that Payette listens carefully, asks thoughtful questions, and provides the approvals needed to move forward. Investors rely on the company for fast, dependable closings and professional guidance every step of the way.

Website: payettefinancial.com

Phone number: 208-333-2040

Alpha Lending

Alpha Lending focuses on single-family rehab financing in Boise, targeting properties with untapped equity that traditional lenders often avoid. By funding fast renovations, they help investors close deals, boost property values, and recycle capital quickly.

Neighborhoods benefit from refreshed, energy-efficient homes, while first-time buyers gain access to move-in-ready options. With 80% of capital dedicated to this niche and additional construction and bridge loan solutions available, the company supports a more accessible Boise housing market.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Loan criteria are not listed online.

Alpha Lending reflects a 4-star rating on Google Reviews. Some clients share that the company delivers reliable and attentive service. They highlight the team’s dedication to taking care of clients and providing support whenever needed. Many praise the staff for their professionalism and responsiveness, making the team a trusted choice for anyone seeking assistance with property deals.

Website: alphalendingllc.com

Phone number: 208-854-1122

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in Idaho?

Hard money loans are best suited for real estate investors who need quick, flexible project funding options. This type of financing is ideal for flipping houses, buying rental properties, or purchasing commercial real estate.

However, if you’re a homeowner looking to leverage your equity, HomeLight’s Buy Before You Sell program might be a better fit. This program offers a smooth transition to your new home without the rush of selling your current one first. You can determine the best financing solution for your real estate goals in Idaho by exploring your options.

Header Image Source: (knowlesgallery/ Deposit Photos)

Editor’s note: This post is for educational purposes only and should not be considered financial advice. HomeLight encourages you to consult your own advisor.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.