Hard Money Lenders Indiana: What You Need To Know

- Published on

- 12 min read

-

Kelsey Morrison Former HomeLight EditorClose

Kelsey Morrison Former HomeLight Editor

Kelsey Morrison Former HomeLight EditorClose

Kelsey Morrison Former HomeLight EditorKelsey Morrison worked as an editor for HomeLight's Resource Centers. She has seven years of editorial experience in the real estate and lifestyle spaces. She previously worked as a commerce editor for World of Good Brands (eHow.com and Cuteness.com) and as an associate editor for Livabl.com. Kelsey holds a bachelor’s degree in Journalism from Concordia University in Montreal, Quebec, and lives in a small mountain town in Southern California.

Are you considering a real estate investment in Indiana and wondering about hard money loans? Whether you’re eyeing a fixer-upper in Gary or planning to expand your rental portfolio in Indianapolis, hard money lenders in Indiana offer a unique financing option. Hard money loans are known for their flexibility and speed, making them ideal for investors with tight project timelines or those who may not qualify for traditional financing.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

For those new to the concept, this guide will walk you through the essentials of hard money lending in Indiana. We’ll cover how these loans work, what they’re used for, and how much they cost. We’ll also explore alternative financing options for homeowners who need to buy a new home before selling their current one. By the end, you’ll be able to make an informed decision about whether working with a hard money lender in Indiana is right for you.

What is a hard money lender?

A hard money lender is a private individual or institution that offers hard money loans, which are named after the “hard” assets used as collateral, typically real estate. Instead of relying heavily on a borrower’s credit or income, these loans are approved based on the property’s value. These firms usually accommodate real estate investors like house flippers and rental property buyers.

To determine loan amounts, hard money lenders consider the after-repair value (ARV) or the estimated value of a property after all repairs and renovations are complete. Typically, they lend a percentage of the ARV, ensuring that the investment remains profitable and secure.

These loans often come with higher interest rates, ranging from 8% to 15%, and shorter repayment periods, usually between six and 24 months. Borrowers should also expect additional costs like origination fees, closing costs, and points. If a borrower fails to repay the loan, the lender can seize the property to recover their investment.

How does a hard money loan work?

Hard money loans follow a straightforward process built for speed and flexibility. Compared to traditional financing, there’s less paperwork and fewer hoops to jump through, so things move faster. Here’s a closer look at the typical steps and what to expect along the way:

- Short-term loan: These loans typically have a repayment period of six to 24 months, unlike the 15- to 30-year terms of conventional mortgages. Some lenders may offer extensions of up to 36 months if necessary.

- Faster funding: When time is of the essence, hard money loans can be approved within days, unlike the typical 40 to 50 days for a conventional mortgage.

- Less focus on creditworthiness: Approval is less dependent on your credit score and income history and more on the property’s value.

- Greater scrutiny on the collateral: This type of financing focuses on the property’s loan-to-value ratio, placing more emphasis on the asset’s value.

- Non-traditional lenders: Hard money loans come from individual investors or private lending companies, not traditional banks.

- Traditional loan denial: Most people who turn to this type of financing are those with poor credit who have been denied a mortgage but have significant home equity.

- Higher interest rates: Due to the higher risk, these loans come with higher interest rates than traditional mortgages.

- Larger down payments: Depending on the property’s value and loan specifics, borrowers may need to provide a larger down payment, sometimes up to 20% to 30%.

- More flexibility: With less regulation, hard money lenders in Indiana can set flexible terms, helping borrowers avoid foreclosure.

- Interest-only payments: Unlike traditional mortgages, hard money loans may initially allow for interest-only or deferred payments, providing flexibility during the loan term.

What are hard money loans used for?

Hard money loans are a popular option for certain financing needs in Indiana’s real estate market. They’re often used by investors or homeowners who need fast funding or can’t qualify for a traditional bank loan. Here are a few common situations where a hard money loan can make sense:

Flipping a house: For Indiana investors focused on flipping homes, hard money loans provide quick access to funds for purchasing and fixing up properties. These loans allow flippers to acquire properties quickly, complete necessary renovations, and resell them for a profit in a short timeframe.

Buying an investment rental property: Investors looking to acquire rental properties can use hard money loans to quickly purchase properties, especially those needing immediate repairs. Unlike traditional bank loans, hard money loans allow landlords to begin renovations ASAP and start generating rental income faster.

Purchasing commercial real estate: Commercial real estate investors may find hard money loans attractive due to their flexibility and fast closing times. These features can be especially beneficial when timing is crucial, allowing investors to move quickly on desirable properties without waiting for lengthy traditional loan approvals.

Looking for alternatives to traditional loans: Individuals with significant home equity but poor credit or other disqualifying factors often turn to hard money lenders. These loans focus more on the value of the asset than the borrower’s credit score, providing an alternative financing option.

Facing foreclosure: Homeowners nearing foreclosure might use hard money loans to refinance their debts or buy time to sell their property. This can offer a temporary solution to avoid losing their home and prevent a foreclosure mark on their credit report.

How much do hard money loans cost?

The cost of hard money loans is generally higher than traditional loans due to the increased risk and convenience they offer. Typical costs include:

- Interest rates: These can range from 8% to 15%, depending on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount as an origination fee.

- Closing costs: These include various fees such as legal, appraisal, and administrative fees.

- Points: Lenders might charge points (a percentage of the loan amount) upfront, adding to the initial loan cost.

Use online hard money loan calculators to estimate these costs accurately.

Alternatives to working with hard money lenders

If you’re a homeowner looking to leverage your home’s equity, here are some alternatives to consider:

Take out a second mortgage: If you have significant equity, a home equity loan or a home equity line of credit (HELOC) can provide funds at lower interest rates than hard money loans.

Cash-out refinance your home: This option allows you to refinance your existing mortgage, pulling out cash to finance new investments, often with lower interest rates.

Borrow from family or friends: Personal loans from family or friends can offer flexible repayment terms and potentially lower or no interest rates, making them a more affordable option.

Use a government-backed loan program: Programs from the FHA, VA, or USDA can help buyers purchase homes with lower down payments and reduced interest rates.

Consider peer-to-peer loans: Loans from individual investors through platforms like Funding Circle can function similarly to hard money loans but often come with different terms.

Explore specialized loan programs: If you already have a hard money loan and want to replace it, consider specialized loans for fixer-uppers or investment property refinancing.

Request a seller financing option: Some sellers may agree to finance the purchase themselves, resulting in lower closing costs and less stringent eligibility requirements.

How to buy before you sell

Sometimes, the perfect home appears when you least expect it. Whether it’s a charming Victorian in Irvington or a modern loft in downtown Indianapolis, timing is everything. For Indiana homeowners looking to buy a new home before selling their current one, HomeLight offers an innovative solution that simplifies the process.

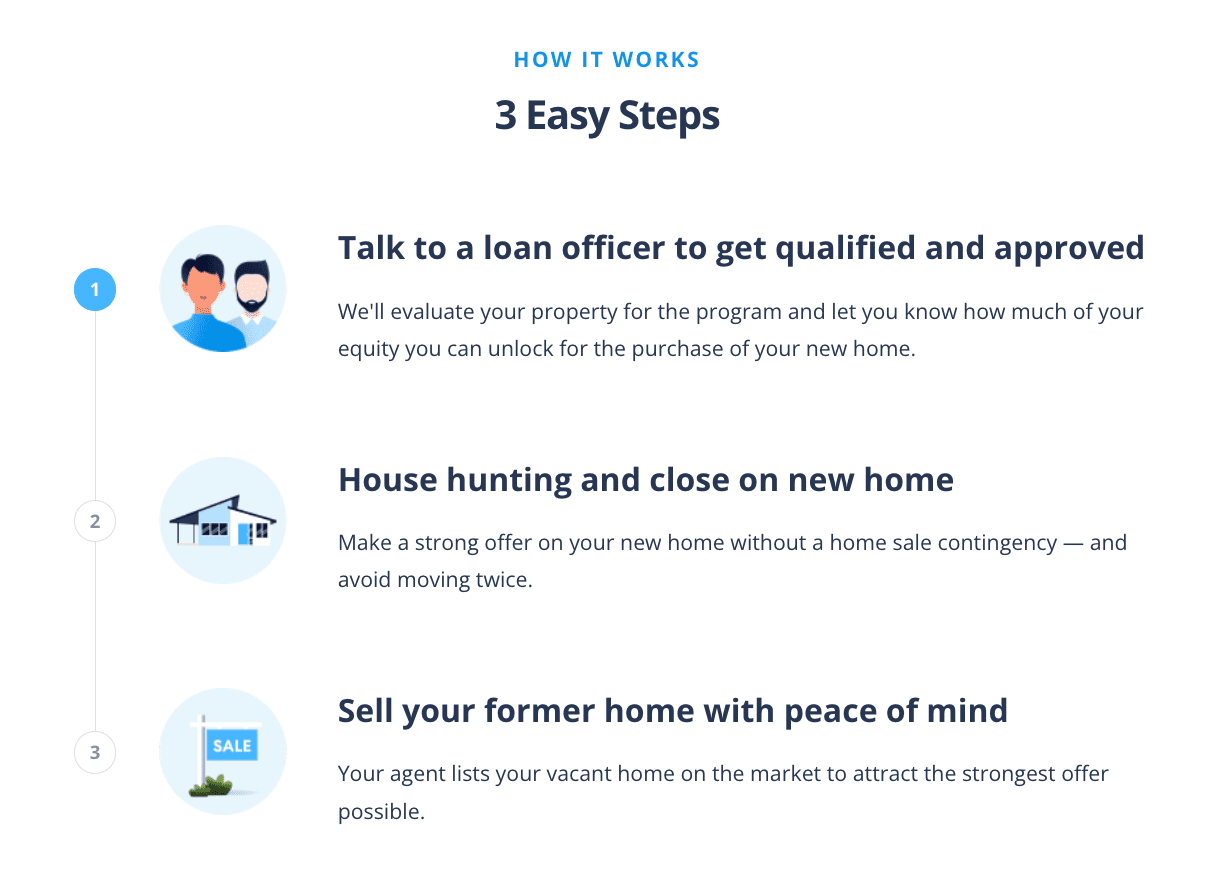

The Buy Before You Sell (BBYS) program allows you to use the equity in your existing home to make a strong, non-contingent offer on a new property. If your home qualifies, you can get your equity unlock amount approved in 24 hours or less, with no cost or commitment required. Once approved, you can confidently purchase your new home and then sell your current one vacant, avoiding the hassle of moving twice.

Here’s how HomeLight Buy Before You Sell works:

While the program carries a flat fee based on your current home’s sold price, the potential savings in other areas can outweigh the cost. You can save on moving expenses and temporary housing, and potentially secure a better purchase price on your new home. Additionally, HomeLight’s BBYS fees are typically much lower than the interest rates on bridge loans, which currently range from 9.5% to 12%.

3 top hard money lenders in Indiana

Indiana’s real estate market moves fast, and having the right lender can make all the difference. Whether you’re flipping a property, funding a renovation, or need to close quickly, hard money loans offer speed and flexibility that traditional banks often can’t. Below, we’ve rounded up three of the top hard money lenders in Indiana to help you find the right fit for your next deal.

RNC Bridge & Private Hard Money

RNC Bridge & Private Hard Money provides flexible financing solutions for real estate investors. The firm offers loan amounts ranging from $100,000 to $10 million, with a streamlined online application process for added convenience.

Competitive interest rates typically range from 7.99% to 12 percent, depending on the deal structure. Loans feature maturity terms of two to three years, with renewal options available, giving borrowers added flexibility as projects evolve.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Up to 70% LTV

RNC Bridge & Private Hard Money earned a perfect 5-star rating on Google. Clients say this team stands out for its care, composure, and client-first approach. They appreciate the clear, reassuring guidance they receive when dealing with complicated or high-stress situations. Many note how the team stepped in when other lenders couldn’t, helping rescue projects and reset deals with smooth refinancing and dependable support.

Website: hardprivatemoneylender.com

Phone number: 888-207-2641

CPL Investments

Based in Carmel, CPL Investments is a hard money lender serving Indianapolis and the surrounding communities. Over its 10-year history, the firm has completed more than 500 real estate deals and funded over $40 million.

CPL Investments provides a range of lending solutions for real estate investors, including fix-and-flip loans, short-term financing, and new construction loans. The company is known for its speed, with loans closing in just a few days and approvals that remain valid for up to 365 days.

Lending clientele: Residential and commercial real estate investors and developers

Loan criteria: Up to 65% of ARV

CPL Investments earned a high A+ grade from the Better Business Bureau (BBB). Its Google Business Profile reflects a 5-star rating, as previous clients praise their customer service, responsiveness, and willingness to make deals work for everyone involved.

Many note that their services help speed up closings and simplify the process, allowing deals to move forward more quickly. Overall, CPL Investments is seen as a dependable partner that supports both smooth transactions and successful real estate investments.

Website: cplinvestments.com

Phone number: 317-836-2807

Total Quality Lending

Total Quality Lending is a mortgage lender that provides hard money loan solutions designed to meet the needs of real estate investors. The company focuses on asset-based lending and streamlined processes to help borrowers move quickly on opportunities. With an emphasis on efficiency and clear communication, it supports various project sizes.

Lending clientele: Residential and commercial real estate investors and homebuyers

Loan criteria: Contact the lender

Total Quality Lending scored 4.9 out of 5 stars on Google, with several reviewers saying that the team delivers a professional and proactive experience for investment property loans. Reviewers note that even when challenges arise, the team responds quickly, communicates clearly, and works diligently to find solutions.

Many appreciate their problem-solving approach and consistent support, which helps keep transactions on track. The smooth closings and attentive service leave clients confident in returning for future deals.

Website: totalqualitylending.com

Phone number: 800-304-1925

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in Indiana?

Deciding whether a hard money loan is right for you depends on your unique situation and real estate investment goals. This type of financing is best suited for Indiana real estate investors who need fast, flexible funding for projects requiring quick turnaround or when traditional financing isn’t an option. If you can manage higher costs and shorter repayment terms, a hard money loan might be the right choice for your next investment.

For homeowners wanting to tap into their home’s equity, HomeLight’s Buy Before You Sell program offers an excellent alternative. Instead of dealing with high-interest rates, you’ll pay a small flat fee while enjoying a more competitive offer and a smoother move. This program allows you to make a stronger offer on a new home by leveraging your current home’s equity, streamlining the entire process.

As with any major financial decision, it’s important to consider your long-term strategy and consult with a financial advisor to ensure it aligns with your overall investment goals. If you’re looking to connect with investor-friendly real estate professionals in Indiana who have access to trusted hard money lenders, let HomeLight introduce you to top agents.

Header Image Source: (Steven Van Elk/ Unsplash)

Editor’s note: This post is for educational purposes only and should not be considered financial advice. HomeLight encourages you to consult your own advisor.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.