Hard Money Lenders NYC: Secure Your Next Deal

- Published on

- 11 min read

-

Kelsey Morrison Former HomeLight EditorClose

Kelsey Morrison Former HomeLight Editor

Kelsey Morrison Former HomeLight EditorClose

Kelsey Morrison Former HomeLight EditorKelsey Morrison worked as an editor for HomeLight's Resource Centers. She has seven years of editorial experience in the real estate and lifestyle spaces. She previously worked as a commerce editor for World of Good Brands (eHow.com and Cuteness.com) and as an associate editor for Livabl.com. Kelsey holds a bachelor’s degree in Journalism from Concordia University in Montreal, Quebec, and lives in a small mountain town in Southern California.

Are you considering funding your next real estate project in New York City with a hard money loan? Whether you’re aiming to renovate a historic brownstone in South Slope or acquire a rental property in the Bronx, hard money lenders in NYC can offer the quick and flexible financing you need. These loans are ideal for those dealing with tight deadlines, limited initial capital, or less-than-perfect credit scores.

For those not investing in real estate but needing to bridge the gap between buying and selling a home, we’ll discuss some alternative options to help you leverage your home’s equity. This article will walk you through the essentials of hard money lending in New York City, helping you determine if this financial solution fits your investment or home-buying plans.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Editor’s note: This post is for educational purposes and is not intended to be construed as financial advice. HomeLight always encourages you to consult your own advisor.

What is a hard money lender?

A hard money lender is a private individual or company that provides short-term loans secured by real estate. Unlike traditional lenders who prioritize a borrower’s credit history and income, hard money lenders focus on the property’s value used as collateral. These lenders usually partner with real estate investors, such as house flippers and those purchasing rental properties, in need of fast funding and flexible terms.

Hard money lenders determine loan amounts based on the after-repair value (ARV) of the property, which is the estimated value after all renovations are completed. Typically, they offer a percentage of the ARV to ensure the loan’s security.

These loans come with higher interest rates, usually between 8% to 15%, and short repayment periods ranging from 6 to 24 months. Additional costs include origination fees, closing costs, and points, a percentage of the loan paid upfront. If the borrower fails to repay the loan, the lender can seize the property to recover their investment.

How does a hard money loan work?

If you’re a real estate investor in NYC and need financing quickly, hard money lenders might be your best option. Here’s a brief overview of how hard money loans work:

- Short-term loan: Hard money loans are usually short-term, with repayment periods ranging from 6 to 24 months, unlike the 15- or 30-year terms common with traditional mortgages.

- Faster funding option: These loans can be approved and funded within a few days, a stark contrast to the 30 to 50 days it often takes for conventional loan processing.

- Less focus on creditworthiness: Hard money lenders place less emphasis on your credit score and income history, focusing instead on the value of the property.

- More focus on property value: These loans are primarily based on the loan-to-value ratio of the property, using it as collateral to secure the loan.

- Not traditional lenders: Hard money loans are usually offered by private individuals or companies, not traditional banking institutions.

- Loan denial option: These loans are a viable choice for those who have been denied traditional mortgages but have substantial home equity.

- Higher interest rates: Due to the increased risk, hard money loans often come with higher interest rates compared to conventional mortgages.

- Might require larger down payments: Borrowers may need to make a sizeable down payment, sometimes as high as 20%–30% of the property value.

- More flexibility: These loans offer flexibility in terms of debt-to-income criteria and can provide solutions for avoiding pre-foreclosure property sale.

- Potential for interest-only payments: Some hard money loans offer interest-only payment options initially, which can be beneficial for managing cash flow early in the project.

What are hard money loans used for?

In New York City’s real estate market, hard money loans address specific financing gaps. They are popular among investors and individuals needing fast access to funds or who face challenges qualifying for traditional loans. Here are some common scenarios where securing a hard money loan coule be beneficial:

Flipping a house: NYC investors focused on flipping homes can benefit from hard money loans due to their rapid funding. These loans allow investors to purchase and renovate properties quickly, enabling them to sell the upgraded homes for profit within a short timeframe.

Buying an investment rental property: Those looking to scoop up rental properties can use hard money loans to act quickly, especially for properties needing immediate repairs. This speed helps landlords complete necessary renovations and start earning rental income faster than traditional financing options.

Purchasing commercial real estate: Commercial real estate transactions can benefit from hard money loans due to their flexible terms and faster closing timelines. This can be advantageous for investors seeking to act quickly on opportunities, compared to the more time-consuming approval processes associated with traditional loans.

Borrowers who can’t qualify for traditional loans: Individuals with considerable home equity but poor credit scores or other issues often turn to hard money lenders. These loans are based more on the asset’s value rather than the borrower’s credit history, offering a practical financing alternative.

Homeowners facing foreclosure: Homeowners at risk of foreclosure may use hard money loans to refinance their debt or buy time to sell their property. This option can help them avoid losing their home or having a foreclosure on their credit report.

How much do hard money loans cost?

The cost of hard money loans is generally higher than traditional loans due to the increased risk and faster funding they offer. Here are the typical costs involved:

- Interest rates: These can range from 8% to 15%, depending on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount as an origination fee.

- Closing costs: Additional fees at closing can include legal fees, appraisal fees, and other administrative expenses.

- Points: Lenders might charge points upfront, which are a percentage of the loan amount, adding to the initial cost.

Online calculators can help estimate these costs.

Alternatives to working with hard money lenders

If you’re a homeowner looking to tap into your home’s equity for financing, here are some alternatives to consider:

Take out a second mortgage: If you have significant equity, a home equity loan or home equity line of credit (HELOC) can provide funds at a lower interest rate than hard money loans.

Cash-out refinance: This option lets you refinance your existing property and withdraw cash for new investments, typically offering lower interest rates compared to hard money loans.

Borrow from family or friends: Personal loans from family or friends can yield flexible repayment terms and potentially lower or no interest rates, making this a cost-effective alternative.

Use a government-backed loan program: Programs such as FHA, VA, or USDA loans assist in home purchases with lower down payments and reduced interest rates.

Peer-to-peer loan: These loans are provided by individual investors through online platforms and can be a viable alternative to hard money loans with different terms.

Specialized loan programs: Look into loans specifically designed for fixer-uppers or for refinancing investment properties if you want to replace an existing hard money loan.

Request a seller financing option: In some cases, sellers may finance the purchase themselves, resulting in lower closing costs and more lenient eligibility requirements.

How to buy before you sell

Sometimes, the perfect listing appears when you least expect it, whether it’s a one-family, detached home in Flushing or a brick-clad loft in Harlem. If you’re a New York City homeowner looking to buy a new home before selling your current one, HomeLight offers a seamless solution with their Buy Before You Sell (BBYS) program.

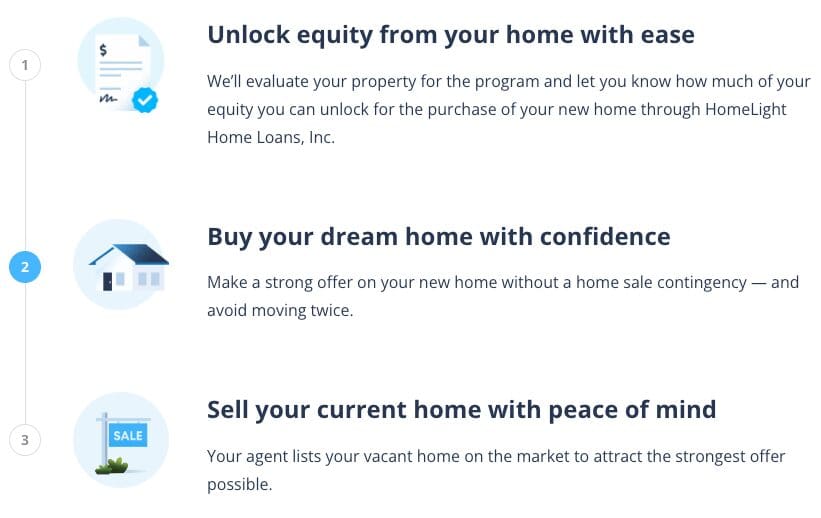

The Buy Before You Sell program enables you to leverage the equity in your current home to make a strong, non-contingent offer on your next property. If your home qualifies, you can get your equity unlock amount approved in as little as 24 hours, with no cost or obligation. Once approved, you can purchase your new home confidently, then sell your current home vacant — avoiding the hassle and expense of moving twice.

Here’s how HomeLight Buy Before You Sell works:

The program charges a flat fee of 2.4% of your current home’s sale price, but the potential savings in other areas can offset this cost. You might save on moving costs, temporary housing, and even secure a better price on your new home. Additionally, HomeLight’s BBYS fees are generally much lower than bridge loan interest rates, which range from 9.5% to 12%.

3 top hard money lenders in NYC

Traditional lenders may not always suit every real estate investment. If you need to move quickly to take advantage of a valuable opportunity, consider partnering with one of these top-rated hard money lenders in NYC.

Manhattan Bridge Capital

Manhattan Bridge Capital, founded by Assaf Ran in 1989 and publicly traded since 1999, offers hard money loans to professional real estate investors. Serving all five NYC boroughs (Brooklyn, Queens, Bronx, Manhattan, and Staten Island), Long Island (Nassau and Suffolk Counties), Hudson Valley, Rockland, and Westchester counties, as well as Florida, MBC typically provides funds within 3–10 business days. They offer fix-and-flip loans, loans for 1- to 3-unit new construction projects, and bridge loans to purchase small, income-generating properties.

Lending clientele: Residential real estate investors

Loan criteria: Up to 65% of the appraised value of asset collateral

Manhattan Bridge Capital has a 5-star rating on Google based on over 40 reviews. Clients praise the employees’ responsiveness, expertise, and short closing timelines. “We have been working with Manhattan Bridge Capital for over 10 years buying and selling properties,” wrote one reviewer. “Great team, friendly customer service, and easy application process. They provided fast funding when we needed it.”

516-444-3400

Hard Money Brooklyn

Hard Money Brooklyn specializes in short-term mortgages, offering hard money loans for non-owner-occupied properties, whether they be residential or commercial. The company lends throughout New York State, including New York City (Bronx, Brooklyn, Manhattan, Queens, Staten Island), and Nassau and Suffolk counties on Long Island. They can close deals in as little as seven business days, and provide loan amounts of $100,000 and up.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Short-term mortgages starting at $100,000

Hard Money Brooklyn holds a 4.5-star Google rating from 30-plus reviews. Clients commend owner Jonathan for his fast turnaround, trustworthiness, and professionalism. “Very honest, communicative and professional service, and overall lowest and most competitive rates and terms!” shared a reviewer. “Highly recommended!”

718-593-4527

West Forest Capital

West Forest Capital, headquartered in NYC, specializes in financing non-owner-occupied real estate. Their hard money loans are ideal for fix-and-flip or fix-and-refinance opportunities. Loans are typically funded within a week and rates start at 10% (interest only). While a one-year term is standard, two-year terms and six-month extensions are available. In addition to NYC, West Forest Capital lends in Long Island, New Jersey, and six other East Coast states.

Lending clientele: Residential, commercial, and development investors

Loan criteria: Up to 75% ARV (hard money loans)

West Forest Capital maintains a 5-star Google rating based on a limited number of reviews. Reviews highlight the company’s willingness to accommodate clients, consistent communication, and competitive rates. “We have a portfolio of properties, and they are our go-to lender for our financing needs,” reads one review. “They’re fast, easy to work with, and have the most friendly terms. A great partner.”

917-267-9523

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in NYC?

Deciding whether a hard money loan is right for you depends on your specific situation and investment goals in New York City. Hard money loans are best suited for real estate investors needing quick access to funds, especially for projects with tight timelines or when traditional financing isn’t available. If you’re equipped to handle higher costs and shorter repayment terms for the benefit of fast, flexible funding, a hard money lender in NYC could be the right choice for your next investment.

For homeowners looking to leverage their equity, consider HomeLight’s Buy Before You Sell program as an alternative. This program allows you to avoid high-interest rates by paying a small flat fee, making it easier to make competitive offers and simplifying the moving process.

As with any major financial decision, it’s important to evaluate your long-term strategy and consult with a financial advisor to ensure it aligns with your overall investment goals. If you need to connect with real estate agents in New York City who have access to reliable hard money lenders, let HomeLight introduce you to top professionals in your neighborhood who meet those criteria.

Header Image Source: (Sam Balye/ Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.