Hard Money Lenders San Diego: Quick Financing Options

- Published on

- 12 min read

-

Sam Dadofalza Associate EditorClose

Sam Dadofalza Associate Editor

Sam Dadofalza Associate EditorClose

Sam Dadofalza Associate EditorSam Dadofalza is an associate editor at HomeLight, where she crafts insightful stories to guide homebuyers and sellers through the intricacies of real estate transactions. She has previously contributed to digital marketing firms and online business publications, honing her skills in creating engaging and informative content.

Are you exploring options to fund your next real estate project in San Diego? Whether you’re aiming to flip a craftsman cottage in South Park or acquire an investment property in Pacific Beach, hard money lenders in San Diego can provide the fast and flexible financing you need.

Hard money loans are a popular alternative to conventional financing, especially for those with tight project timelines, limited initial capital, or less-than-perfect credit. If you’re not in real estate investment but need to bridge the gap between buying and selling a home, there are modern solutions that allow you to leverage your home’s equity.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

In this article, we’ll cover the fundamentals of hard money lending in San Diego, guiding you through the process and some alternatives to help you decide if this financial tool is the right fit for your real estate investment or home-buying goals.

What is a hard money lender?

Hard money lenders are institutions that offer hard money loans, which are named after the “hard” assets used as collateral, typically real estate. Instead of relying heavily on a borrower’s credit or income, these loans are approved based on the property’s value.

These lenders in San Diego typically work with clients like house flippers and rental property buyers who need quick access to funds and flexible terms. They use the after-repair value (ARV) or the estimated value of a property after all renovations and repairs are completed to determine the loan amount they are willing to offer. They usually lend a percentage of the ARV to ensure the investment’s profitability and security.

Hard money loans come with higher interest rates, typically ranging from 8% to 15% or more, and shorter repayment periods, usually between six and 24 months. Additional costs can include origination fees, closing costs, and points. If a borrower fails to repay a hard money loan, the lender can seize the property to recover their investment.

How does a hard money loan work?

If you’re a real estate investor in San Diego looking for a financing option that offers speed and flexibility, connecting with hard money lenders could be the right move. Here’s a quick overview of how hard money loans work:

- Short-term loan: These loans usually have a repayment period of six to 24 months, unlike the 15- or 30-year terms of conventional mortgages. Some lenders may extend the term up to 36 months if needed.

- Faster funding: When you need to close a deal quickly, hard money loans can be approved within days, compared to the 30 to 50 days typical for a mortgage loan.

- Less focus on creditworthiness: Approval relies less on your credit score or income history and more on the property’s value.

- Greater scrutiny on collateral: These loans require collateral, such as a home, and are based on the loan-to-value ratio of the property.

- Non-traditional lenders: Individual investors or private lending companies usually provide hard money loans, not traditional banks.

- Traditional loan denial: These loans are often used by those with poor credit who have been denied a mortgage but possess significant home equity.

- Higher interest rates: Due to higher risk, these loans have higher interest rates than traditional mortgages.

- Larger down payments: Borrowers may need to provide a larger down payment, sometimes up to 20% to 30%, depending on the property’s value and loan specifics.

- More flexibility: With less government regulation, hard money lenders in San Diego can set flexible credit scores and debt-to-income (DTI) criteria, and loans can help avoid foreclosure.

- Interest-only payments: Unlike traditional mortgages, hard money loans may allow for interest-only or deferred payments initially.

What are hard money loans used for?

Hard money loans are a great option for specific financing needs in San Diego’s real estate market. They’re popular among investors who need quick cash or struggle to get traditional bank loans. Let’s look at what hard money loans are typically used for:

Flipping a house: For San Diego investors flipping homes, hard money loans provide quick access to funds for purchasing and renovating properties. These loans enable flippers to secure properties in competitive markets, complete necessary updates, and sell them for profit within a short period.

Buying an investment rental property: Investors looking to acquire rental properties can benefit from hard money loans, especially for homes needing immediate repairs. These loans allow landlords to purchase, renovate, and start generating rental income more quickly than traditional bank loans.

Purchasing commercial real estate: Hard money loans are frequently used in commercial real estate due to their flexible terms and rapid closing times. This flexibility is crucial in fast-moving markets, allowing investors to seize opportunities that require quick decisions.

Looking for alternatives to traditional loans: Those with significant home equity but poor credit often turn to hard money lenders for financing. These loans prioritize the asset’s value over the borrower’s credit score, making them accessible to a wider range of borrowers.

Facing foreclosure: Homeowners at risk of foreclosure can use hard money loans to refinance their debt or buy time to sell their property. This option can help prevent the loss of their home and avoid the negative impact of foreclosure on their credit history.

How much do hard money loans cost?

Hard money loans typically come with higher costs due to the increased risk and expedited process. Here are some typical costs associated with hard money loans:

- Interest rates: These can range from 8% to 15% or higher, depending on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount as an origination fee.

- Closing costs: Additional fees at closing can include legal fees, appraisal fees, and other administrative costs.

- Points: Lenders might charge points (a percentage of the loan amount) upfront, adding to the initial cost of obtaining a loan.

Use online hard money loan calculators to help estimate your costs.

Alternatives to working with hard money lenders

If you’re a homeowner, as opposed to an investor, seeking a way to leverage your current home’s equity, here are some options to consider:

Take out a second mortgage: Leveraging the equity in your home through a home equity loan or a home equity line of credit (HELOC) can provide necessary funds at more favorable interest rates than hard money loans.

Cash-out refinance your home: You can borrow cash to fund new investments by refinancing your existing mortgage. This method often offers lower interest rates and longer repayment terms.

Borrow from family or friends: Personal loans from family or friends can be a viable alternative. They often feature flexible repayment plans and minimal or no interest, making them a more cost-effective solution.

Use a government-backed loan program: Federal programs such as those offered by the FHA, VA, or USDA offer lower down payments and reduced interest rates, which can benefit qualifying buyers.

Consider peer-to-peer loans: Online platforms like Funding Circle connect borrowers with individual investors. These loans can serve a similar function to hard money loans but might offer different terms and conditions.

Explore specialized loan programs: Explore specialized financing options designed for specific purposes, such as fixer-upper loans or investment property refinancing, to find a loan that meets your particular needs.

Request a seller financing option: Some sellers may be willing to finance the sale themselves, offering lower closing costs and more lenient qualification criteria. This can be a convenient alternative to traditional financing.

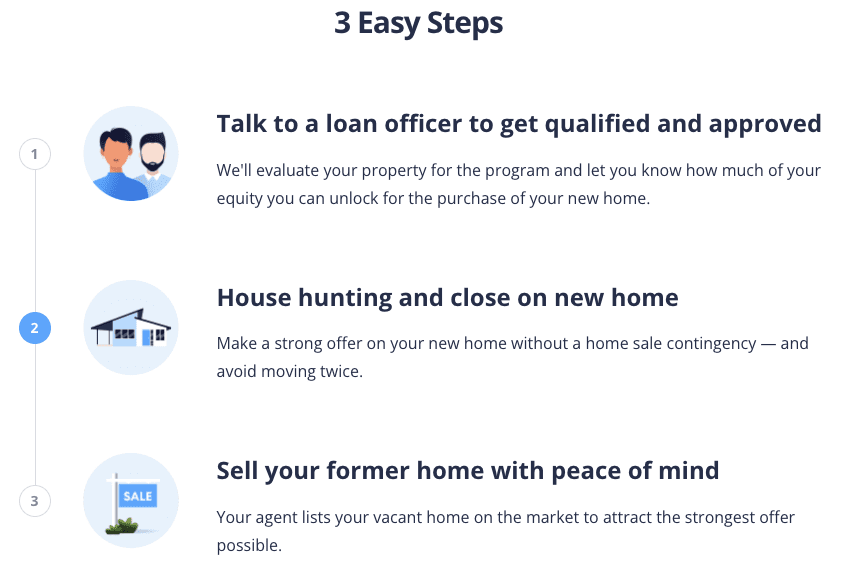

How to buy before you sell

Sometimes, the perfect home comes on the market when you least expect it. Maybe it’s a charming ranch-style home in Point Loma or a modern condo in Little Italy. If you’re a San Diego homeowner who wants to buy a new home before selling your current one, HomeLight offers an innovative solution that simplifies the process.

The Buy Before You Sell (BBYS) program lets you leverage the equity in your existing home to make a stronger, non-contingent offer on a new property. If your home qualifies, you can get your equity unlock amount approved within 24 hours, with no cost or commitment required. Once approved, you can confidently purchase your next home and then sell your current one vacant, avoiding the inconvenience of moving twice.

Here’s how HomeLight Buy Before You Sell works:

The program charges a flat fee based on your current home’s sold price, but the potential savings can outweigh this cost. You might save on moving expenses, temporary housing, and even secure a better deal on your new home. Additionally, HomeLight’s BBYS fees are typically lower than the interest rates on bridge loans, which currently range from 9.5% to 12%.

3 top hard money lenders in San Diego

Finding the right lender can make all the difference in a real estate investment. Here are the top hard money lenders in San Diego known for fast approvals and flexible terms. These lenders are trusted by investors looking to close deals quickly and efficiently.

Source Capital Funding, Inc.

Founded in 2007, Source Capital Funding, Inc. was built to provide financing when traditional lenders would not. The firm has since become a leading direct hard money lender, helping thousands of clients, mortgage brokers, and real estate agents achieve their goals.

To date, Source Capital has funded over $500 million in residential and commercial loans, demonstrating a strong record of reliability and expertise. Committed to client success, the company offers loan approvals in 24 hours and funds within seven to 10 days from initial contact.

Lending clientele: Residential, commercial, and development real estate investors

Loan criteria: Up to 65% LTV

Source Capital Funding, Inc. has been accredited with the Better Business Bureau (BBB) since 2010 and earned an A+ grade. Its Google Business Profile reflects a high 4.9-star rating on Google based on over 300 reviews.

Clients commend the company for its professional service, quick funding process, and clear communication. Some highlight their ability to handle unique or complex properties while providing solid loan terms. Others say the company representatives’ expertise and dedication inspire confidence, encouraging clients to return for future deals.

Website: hardmoneyfirst.com

Phone number: 888-334-6636

Lantzman Lending

For over 50 years, Lantzman Lending has been providing hard money financing to real estate investors in California. Known for speed and reliability, the company structures loan programs to fit each investor’s unique project, offering rates starting at 8% and the ability to close in as little as three days.

The firm supports a wide range of investment types and works with borrowers holding title personally or through entities such as LLCs, corporations, or trusts. As true asset-based lenders, Lantzman Lending streamlines the process with a simple one-page application and delivers loan quotes within 24 hours.

Lending clientele: Residential, commercial, and development real estate investors

Loan criteria: 65% to 70% ARV (flips); otherwise, up to 65% of the current fair market value or finished value

Lantzman Lending touts a 5-star rating on Google, with clients often praising their quick response times, friendly nature, and fair valuations and terms. Some highlight how funding can be completed in under a week, with every staff member providing helpful guidance and support throughout the process. Others appreciate the efficiency and professionalism that make working with the company smooth and straightforward.

Website: lantzmanlending.com

Phone number: 858-720-0229

North Coast Financial, Inc.

Based in Oceanside, North Coast Financial is a direct hard money lender with over 40 years of industry experience. Together with its affiliates, the company has funded over $1 billion in real estate loans. Specializing in financing for real estate investors and property owners, North Coast Financial stands apart from traditional lenders. Most loans can be funded within five days, with same-day approvals available for qualified borrowers.

Lending clientele: Commercial and residential real estate investors and homeowners

Loan criteria: Depends on the loan program; for example, LTVs up to 70%–75% are available for residential real estate investment loans with financing terms up to three years

North Coast Financial, Inc. has been BBB accredited since 2015 and holds an A+ rating. It has a perfect 5-star rating on Google, as clients report that the team delivers seamless and dependable service from start to finish. Reviewers highlight their consistent speed, reliability, and ability to meet commitments without surprises.

Many appreciate how smoothly every stage of the process runs, noting the team’s professionalism and attention to detail. Their efficiency and trustworthiness make clients confident in returning for future projects.

Website: northcoastfinancialinc.com

Phone number: 760-722-2991

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.![]()

Investing in real estate?

Should I partner with a hard money lender in San Diego?

Deciding whether a hard money loan is right for you in San Diego depends on your specific real estate goals and circumstances. This type of financing is best suited for real estate investors who need quick access to funds for projects like flipping houses or purchasing investment properties. They offer flexibility and fast approval times, making them ideal for time-sensitive opportunities in San Diego’s competitive market.

However, if you are a homeowner looking to leverage your home’s equity, HomeLight’s Buy Before You Sell program might be a better fit. This program allows you to make a non-contingent offer on a new home while paying a small flat fee instead of dealing with high interest rates. It also simplifies the process, enabling you to sell your current home after moving into your new one.

As with any major financial decision, consider your long-term strategy and consult with a financial advisor. For those looking to connect with experienced real estate professionals in San Diego who have access to trusted hard money lenders, HomeLight can introduce you to top agents in your area.

Header Image Source: (Leo_Visions/ Unsplash)

Editor’s note: This post is for educational purposes only and should not be considered financial advice. HomeLight encourages you to consult your own advisor.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.

Homelight

619-514-2629

3638 Camino Del Rio N. Ste. 200

San Diego, CA

92018