What Makes Mortgage Rates Go Down?

- Published on

- 8 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

You’ve probably noticed how mortgage rates change all the time, leaving homebuyers scratching their heads. One month they’re “low,” the next they’re creeping up, and it seems like no one can predict them. Between news about the economy, the Fed, and your own credit score, it’s easy to feel lost. But if you’ve ever wondered what drives those numbers, here’s the truth: what makes mortgage rates go down is a mix of economic forces and personal factors you can actually understand and keep an eye on.

Knowing them can help you time your move and maybe save thousands on your loan. In this post, we’ll break down the key elements that influence mortgage rates and show you what to watch for.

How Much Is Your Home Worth Now?

Home values have rapidly increased in recent years. How much is your current home worth now? Get a ballpark estimate from HomeLight’s free Home Value Estimator.

1. Slower economic growth

When the economy slows down, mortgage rates often take a dip too. Slower growth usually means less inflation and lower demand for borrowing, which can prompt lenders to drop rates to get people back in the market. For homebuyers, that’s good news, as you could get a lower rate and save big over time. Sellers benefit too: lower rates can attract more buyers, meaning your home might sell faster than you expected.

2. Favorable government policy changes

Government policy can have a big impact on mortgage rates. When the Federal Reserve or other central banks lower the federal funds rate to encourage borrowing, mortgage rates often follow. That means mortgage loans can become more affordable, which is helpful if you’re looking to buy.

Watching for changes in government policy can give you an idea of when rates might dip. Timing your purchase or sale around these shifts could lead to meaningful savings.

3. Decreasing inflation rate

Inflation reduces the value of money over time, and when it’s high, lenders often raise mortgage rates to protect their returns. But when inflation starts to ease, it can point to lower borrowing costs.

As inflation drops, interest rates usually follow, making it a smart time to lock in a mortgage. Lower inflation can also make homes more affordable, which is good news for both buyers and sellers. Keeping an eye on inflation trends can give you a better sense of where mortgage rates might be headed.

4. High borrower credit score

Your credit score is a major factor in determining your mortgage rate. Borrowers with higher credit scores are seen as lower risk, so they often qualify for lower interest rates.

If you’re aiming to secure the best possible rate, improving your credit score should be a priority. Pay down debt, avoid late payments, and check your credit report for errors. A strong credit score not only helps you get a better rate but also broadens your mortgage options.

5. Shorter loan term options

Choosing a shorter loan term can help reduce your mortgage rate. Lenders typically offer lower interest rates on 15-year mortgages compared to 30-year mortgages, as the shorter term means less risk for the lender.

If you can afford the higher monthly payments of a shorter loan, you’ll pay less in interest over the life of the loan. This option may appeal to buyers who want to build equity faster or sellers who are looking to finance their next home with minimal long-term interest.

6. Opting for adjustable-rate loans

Adjustable-rate mortgages (ARMs) often come with lower initial interest rates compared to fixed-rate loans. For buyers who anticipate selling or refinancing before the rate adjusts, this can be a way to secure lower payments in the short term.

However, ARMs carry the risk of rate increases later on. If you’re considering this option, make sure you understand the terms and are prepared for any future rate changes.

7. Increased housing supply and reduced demand

When more homes are available on the market and demand is lower, mortgage rates can drop. A larger housing supply gives buyers more negotiating power, which can push prices and mortgage rates down.

If you’re selling, this might not be the ideal scenario, but for buyers, it could be an opportunity to get a better rate and more favorable terms. Staying informed about housing market inventory trends can help you time your purchase or sale to your advantage.

8. Low investor confidence

Investor confidence also plays a role in mortgage rates. When investors are uncertain about the economy, they tend to shift their money into safer assets, like bonds, which can push bond yields down and, in turn, lower mortgage rates.

As a buyer, this could mean an opportunity to secure a lower rate when the market is turbulent. Sellers may also benefit, as lower rates could draw more buyers into the market.

No mortgage rate guarantees: It should be noted that lower interest rates aren’t guaranteed during times of recession or periods of weak investor confidence. Even when the Fed makes progress in taming inflation and guiding the market to the desired “soft landing,” a situation where the economy slows without tipping into a full-blown recession, interest rates can be volatile and change quickly.

Buying or Selling? Start With a Top Agent

Connect with a top-rated local real estate agent for an expert opinion and to get the ball rolling. HomeLight analyzes over 27 million transactions and thousands of reviews to help you find the best agent for your needs.

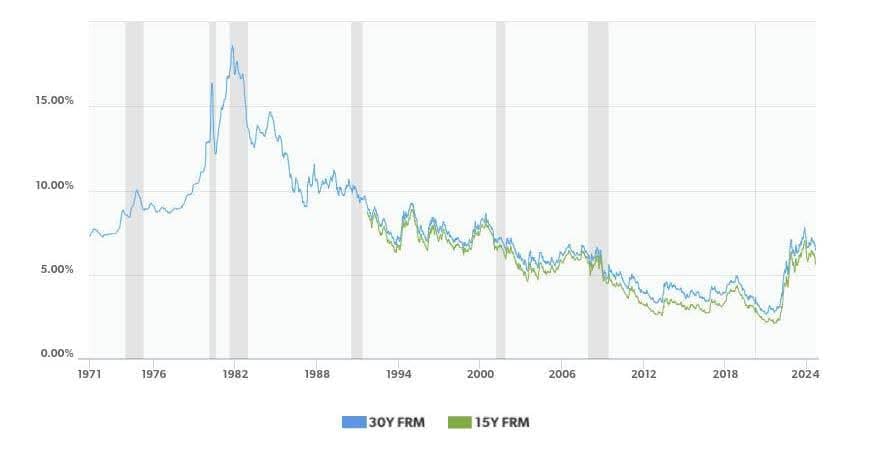

How do today’s rates compare with history?

Watching mortgage rates go up these past few years, it might seem like it was always cheaper for your parents or grandparents to buy a house. However, looking back through the decades, you can see that this assumption may not always hold true. Even the recent mortgage rate peak of 7.79% in October 2023 was considerably lower than the peak of 18.63% in October 1981.

Here’s a look at the 30-year fixed mortgage rates in the U.S. since 1974:

Home mortgage interest rates from 1974 to 2024

| Year | Average 30-year rate | Year | Average 30-year rate | Year | Average 30-year rate | Year | Average 30-year rate |

| 1974 | 9.19% | 1987 | 10.21% | 2000 | 8.05% | 2013 | 3.98% |

| 1975 | 9.05% | 1988 | 10.34% | 2001 | 6.97% | 2014 | 4.17% |

| 1976 | 8.87% | 1989 | 10.32% | 2002 | 6.54% | 2015 | 3.85% |

| 1977 | 8.85% | 1990 | 10.13% | 2003 | 5.83% | 2016 | 3.65% |

| 1978 | 9.64% | 1991 | 9.25% | 2004 | 5.84% | 2017 | 3.99% |

| 1979 | 11.20% | 1992 | 8.39% | 2005 | 5.87% | 2018 | 4.54% |

| 1980 | 13.74% | 1993 | 7.31% | 2006 | 6.41% | 2019 | 3.94% |

| 1981 | 16.63% | 1994 | 8.38% | 2007 | 6.34% | 2020 | 3.10% |

| 1982 | 16.04% | 1995 | 7.93% | 2008 | 6.03% | 2021 | 2.96% |

| 1983 | 13.24% | 1996 | 7.81% | 2009 | 5.04% | 2022 | 5.34% |

| 1984 | 13.88% | 1997 | 7.60% | 2010 | 4.69% | 2023 | 6.81% |

| 1985 | 12.43% | 1998 | 6.94% | 2011 | 4.45% | 2024 | 6.72% |

| 1986 | 10.19% | 1999 | 7.44% | 2012 | 3.66% | 2025 | 6.47% |

Source: Freddie Mac

Monthly payment comparison: As mentioned earlier, in 1981, mortgage interest rates peaked at 18.63%. This significantly impacted house payments. For example, a $300,000 mortgage at 18.63% would require a monthly payment of $4,676. That same loan at a pandemic-era rate of 2.65% would only require a $1,209 monthly payment.

Here’s how the past 53 years of mortgage rates history look on a chart:

How buyers can secure a lower mortgage rate

Now that you understand the key factors that influence mortgage rates, like the economy, inflation, and government policy, you might be wondering how you can use that knowledge to your advantage. While you can’t control the broader market, there are practical steps buyers can take to improve their personal rate. By planning ahead and making strategic moves, you can put yourself in a stronger position when it’s time to apply.

Here are some tips to help you lock in a better rate:

- Improve your credit before applying: Higher credit scores often qualify for lower rates, so check your score and fix any errors ahead of time.

- Shop multiple lenders: Comparing offers can reveal significant differences in rates, fees, and loan terms.

- Buy discount points: Paying upfront to reduce your interest rate can save money over the long run.

- Choose shorter loan terms: 15- or 20-year loans often carry lower rates than 30-year loans.

- Lock rates strategically: Rate locks can protect you from increases while your loan is processing.

- Reduce your debt-to-income (DTI) ratio: DTI is the percentage of your monthly income that goes toward paying debts, helping lenders gauge how much mortgage you can afford. Paying down debts before applying for a mortgage can improve your loan terms and rate.

In the same way, you should make sure you can comfortably afford your mortgage payments while taking advantage of lower rates. Even if you secure a great interest rate, overextending yourself can lead to financial stress and limit your lifestyle.

Here are some strategies to help you budget wisely and avoid becoming house poor.

- Get pre-approved for a mortgage: Having a pre-approved mortgage loan shows sellers you’re serious and helps define your budget.

- Save a larger down payment: With a larger down payment, you’ll pay less interest over time. Plus, it makes your offer more attractive to sellers. HomeLight’s down payment calculator can assist you with planning.

- Consider an adjustable-rate mortgage (ARM): If you don’t plan on staying long, this can help you secure a lower initial rate.

- Shop within your budget: Avoid overextending yourself by buying at the top of your price range. To shop with more confidence, try HomeLight’s Home Affordability Calculator.

Meanwhile, if you’re juggling buying and selling at the same time, HomeLight’s Buy Before You Sell program can give you a big advantage. By tapping into the equity in your current home, you can move more strategically, without rushing your sale or dipping into savings.

This flexibility lets you time your purchase to take advantage of lower mortgage rates, make a stronger, non-contingent offer, and move just once. With less financial pressure and more control over your timeline, you can position yourself to lock in the best rate possible.

Watch the video below to know how HomeLight Buy Before You Sell works:

Get started with a top agent

Understanding what makes mortgage rates go down can help you time your next real estate move, whether you’re buying or selling. Factors like declining economic growth, favorable government policies, and lower inflation all contribute to potential rate drops.

Additionally, your own financial standing, such as a high credit score, can lead to securing a better mortgage rate.

If you’re ready to make a move, you’ll get the best results when you partner with an expert. HomeLight’s free Agent Match platform connects you with top agents in your area who can guide you through the process.

Whether you’re looking to lock in a lower rate for a home purchase or sell your property at the right time, having the right agent by your side can make all the difference.

HomeLight partners with top-rated real estate agents across the country. We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs.

Header Image Source: (Curtis Adams/ Pexels)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.