What Contingencies Are Standard and Which to Push Back On? A Seller’s Guide for 2026

- Published on

- 7 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

As a home seller, contingencies in real estate introduce a frustrating level of uncertainty and risk into your transaction. Each clause is a potential exit for your buyer, which can lead to stressful delays, last-minute renegotiations, or the entire sale falling through.

Having a deal collapse forces you to relist your home, losing valuable time and market momentum. In this post, we take a closer look at what contingencies are standard and which ones to challenge (and when).

The Top 5% of Agents Sell Homes for Up to 10% More

HomeLight analyzes over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs. Connect with your top agent matches today at no cost.

What contingencies in real estate impact sellers?

A real estate contingency is a clause in a purchase agreement that specifies a condition that must be met for the contract to remain in force. For buyers, these clauses act as a safety net, allowing them to back out of a deal without penalty if issues like a low appraisal, failed financing, or major inspection problems arise.

As a seller, you should anticipate these common requests and be prepared to negotiate their specific terms. Let’s take a look at the five most common contingencies in real estate that impact home sellers.

Inspection contingency

The inspection contingency allows the buyer a set period to have the home professionally inspected. Based on the inspector’s report, the buyer can request repairs, ask for credits, or terminate the contract if significant issues are discovered. This is one of the most common and often heavily negotiated contingencies.

Appraisal contingency

An appraisal contingency protects the buyer if the home’s appraised value comes in lower than the agreed-upon sale price. Since a lender won’t finance a home for more than it is worth, this clause gives the buyer the ability to renegotiate the price or walk away if an “appraisal gap” exists.

Financing contingency

This contingency, also known as a mortgage contingency, gives the buyer an out if they are unable to secure a mortgage to purchase the home. Even with pre-approval, a buyer’s loan can be denied for various reasons. This is a standard clause that protects the buyer’s earnest money if their financing falls through.

Home sale contingency

A home sale contingency makes the purchase of your home dependent on the buyer successfully selling their own property. This is a particularly risky clause for sellers, as it ties your transaction to the success of another sale over which you have no control.

Title contingency

The title contingency is a standard clause that ensures the property title is free of liens or ownership disputes before the sale is finalized. A title search confirms you have the legal right to sell the property, protecting the buyer from future legal challenges. This is generally non-negotiable protection for all parties.

When to push back on contingencies based on market conditions

As a home seller, the strategy you use to negotiate contingencies depends on market conditions. Your leverage to resist or modify a buyer’s requests is directly tied to local supply and demand. Below is a snapshot of the markets you may encounter and what you can expect.

Hot (seller’s) market

In a seller’s market, you have significant leverage due to high demand and low inventory. This is the best time to push back on non-essential requests or counter with shorter contingency periods. Buyers may even waive certain contingencies to make their offers more competitive.

Balanced market

In a balanced market, a give-and-take approach is necessary. You will likely need to accept standard contingencies, but you can stand firm on requests for extensive repairs or unusually long timelines. The goal is to find a fair middle ground in your negotiations.

Cool (buyer’s) market

In a buyer’s market, you’ll need to be more flexible. Buyers have more options, so you have less leverage. Being accommodating of reasonable requests is key to securing a buyer and keeping a deal together. While some buyers in hot markets may waive protections, this is far less common when conditions cool.

Your most valuable resource is a top local agent who understands the specific dynamics of your market and can advise on the most effective ways to negotiate or tighten contingency terms.

With market context in mind, let’s look at how sellers can handle specific contingencies, starting with inspections.

Inspection contingency: how sellers can negotiate and push back

If you take a proactive approach, you can often prevent inspection-related headaches. Before listing, address any small, obvious repairs. You might even consider a pre-listing home inspection. And don’t let minor cosmetic items (such as a scuffed wall) cloud the negotiations. You have more power to refuse requests for cosmetic fixes.

However, significant material defects (like a failing roof) will need to be addressed. When a legitimate problem is found, your negotiation playbook should be flexible. You can offer to make the repair, provide a seller credit to the buyer, reduce the sale price, or refuse the request and risk the buyer walking away.

A simple script for a counteroffer could be: “In lieu of making the requested repairs, the seller offers a credit of $X,XXX at closing for the buyer to use as they see fit.” Always insist on clear deadlines for the inspection period to keep the process on track.

In many cases, offering a credit is the best solution, as it keeps the deal moving and removes your liability for the repair work. In other situations, fixes may be necessary after a home inspection if you wish to proceed with the sale.

Appraisal and financing contingencies: How to handle valuation gaps and loan approvals

An appraisal contingency protects the buyer if the home is valued for less than the offer price, creating an “appraisal gap.” If this happens, you have options:

- The buyer can pay the difference in cash

- You can lower the price to the appraised value

- You can negotiate a price in the middle

- You can challenge the appraisal with supporting data

The financing contingency protects the buyer if their loan is denied. To minimize this risk, prioritize offers from buyers with a strong pre-approval letter from a reputable lender, which shows their finances have already been vetted.

When these issues arise, clear communication and a decisive strategy developed with your agent are critical to saving the deal. This is often where a full-service Realtor can outperform a discount broker or agent.

HomeLight solution: Reducing contingency risk and gaining certainty

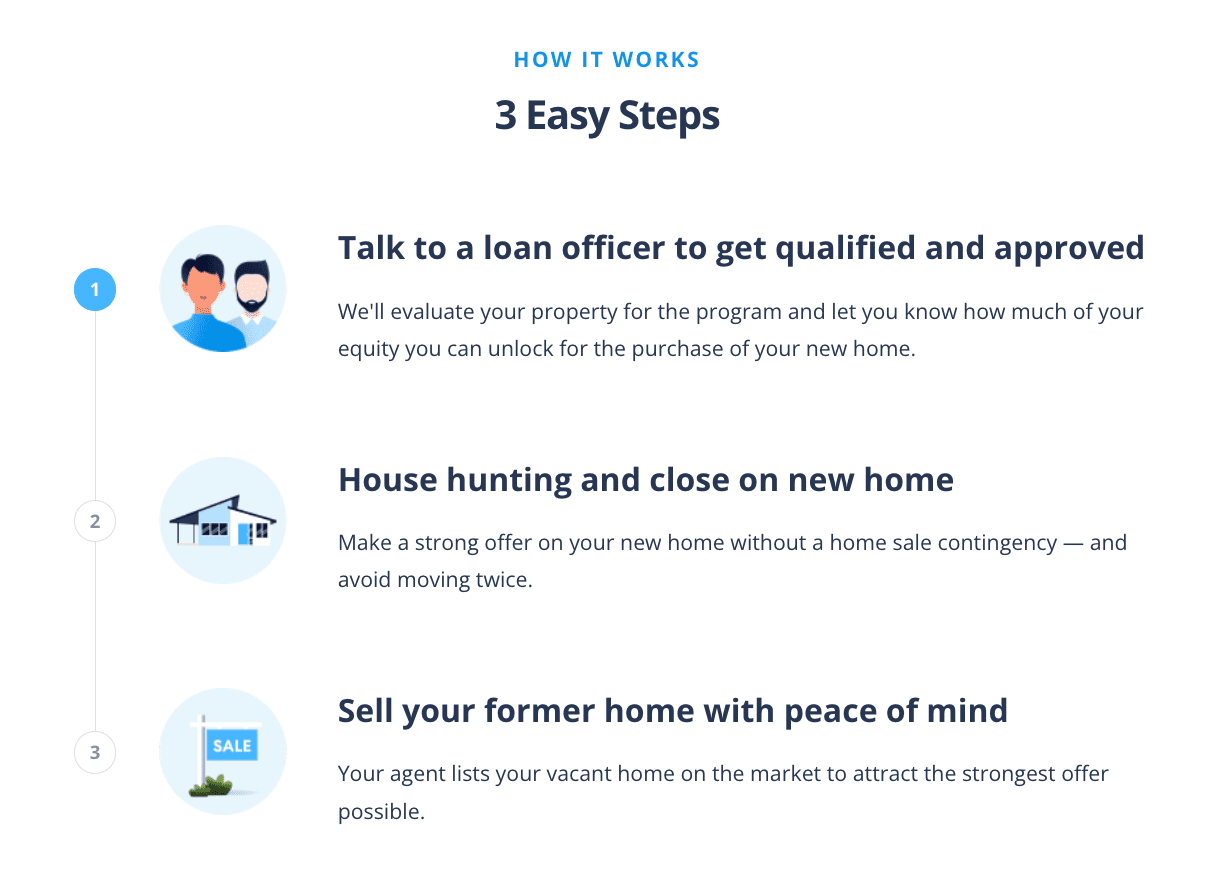

HomeLight’s Buy Before You Sell program provides an innovative solution for sellers who are also buyers. This modern program helps you to purchase a new home before selling your current one. It allows you to remove uncertainties on both the buying and selling sides, including your desire to make a non-contingent offer for your next home purchase.

Here’s how HomeLight Buy Before You Sell works:

With Buy Before You Sell, you only need to move once. Plus, you’ll have peace of mind with HomeLight’s Home Sale Guarantee, a backup cash offer for your old property, providing a safety net if it doesn’t sell quickly on the open market.

HomeLight also offers a free Agent Match platform, which connects you with a top-performing, trusted agent in your market. We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs.

Connect With a Top Agent For Successful Negotiations

Top agents sell homes faster and for more than average agents and are in their clients’ corner. They also come with an array of skills and experiences, including in negotiation.

Non-negotiable contingencies: When to prioritize protection over profit

Some contingencies are fundamental protections that should not be negotiated away. The title contingency is non-negotiable. It ensures the buyer receives a clean title, free from claims or liens, which protects you from future legal issues.

Similarly, mandatory seller disclosures are legally required in most states. Complying with laws that require you to disclose known issues with the property’s condition protects you from future lawsuits. An offer that waives too many critical protections might seem appealing, but it can be a red flag for a high-risk buyer or a deal destined to collapse.

Crafting counteroffers and setting clear contingency deadlines

Crafting a strong counteroffer involves using precise language to define terms and setting firm, reasonable deadlines for each contingency. This approach creates a clear timeline, holds buyers accountable, and prevents them from unnecessarily delaying the process. All negotiated terms should be documented in writing to avoid future disputes.

If you must accept a home sale contingency, insist on a kick-out clause. This allows you to continue marketing your home and accept a better offer if one comes along, after giving the original buyer a set time to remove their contingency.

Always work with your real estate agent to draft and review contract language to make certain your interests are protected.

FAQs: Common questions about contingency negotiations

Here are answers to some of the most common questions home sellers have about navigating contingency negotiations.

A “clean” offer is attractive, but be cautious. Waiving an inspection can be a plus for you, but waiving a title review is a major red flag. Your agent can help you assess the risks and verify the buyer’s financial ability to close.

Yes. Your power to refuse depends on the market. In a seller’s market, you can often stand firm on minor issues. In a buyer’s market, being more flexible on reasonable requests for major items can keep the deal together.

You can renegotiate the price, the buyer can make up the difference in cash, or the contract can be terminated if an agreement can’t be reached. Sometimes, the appraisal can be successfully challenged with better data.

Timelines are negotiable but often follow local norms. Inspection contingencies typically last 7–10 days, although some states use longer standard periods. For example, California contracts usually allow 17 days to complete inspections and remove contingencies. Financing and appraisal contingencies typically last 21–30 days or more. Home sale contingencies are often set for 30–60 days. The key is clearly defining each deadline in the purchase contract.

Empower your home sale with HomeLight

Successfully selling your home requires a deep understanding of how to manage contingencies. Your strategy should be guided by local market conditions, the strength of the offer, and your personal goals.

Working with an experienced real estate professional is the best way to navigate these complex negotiations and protect your interests. HomeLight provides the tools and connections you need to sell with confidence. To get started, tell us a little about your home and selling timeline.

Find a top agent today who can provide local market insights and guide you through every contingency. Or, check out HomeLight’s Buy Before You Sell program.

You’ll find more helpful tips and guides in HomeLight’s Seller Resource Center.

Additional home-selling tools from HomeLight:

- Seller Closing Cost Calculator

- Best Time To Sell Calculator

- Net Proceeds Calculator

- Agent Commissions Calculator

- Home Value Estimator

Header Image Source: (allihahnsolo / Deposit Photos)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.