Dividing Your Home in a Divorce: Do You Need an Appraisal?

- Published on

- 13 min read

-

Jacob Burdis, Contributing AuthorClose

Jacob Burdis Contributing Author

Jacob Burdis, Contributing AuthorClose

Jacob Burdis Contributing AuthorJacob Burdis, PhD is a professional dabbler with experience in entrepreneurship, educational technology, digital language learning, product management, and real estate investing.

-

Richard Haddad, Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

Going through a divorce is difficult and taxing. Not only are you feeling the emotional loss as you grieve the ending of what was once a strong relationship, but the logistical and legal hurdles may sometimes feel like more than you can bear. Even in the most amicable situations, splitting up real estate assets can create distrust and resentment.

You aren’t a failure, and you don’t have to go through the process alone. Many people have gone through what you’re going through, and there are professionals who specialize in helping divorcing couples sort through the financial divisions equitably.

In this guide, we’ll help you answer questions about whether getting a home appraisal is the right step for you, how you can go about getting one, and how to prepare for it.

We’ve interviewed top real estate agent Edward Kaminsky, who has completed more than 1,580 transactions in Los Angeles County and has 39 years of experience, and Marco Brown from Brown Family Law: Utah Divorce Attorneys, who specializes in helping divorcing couples navigate the process fairly.

Enter a few details about your home, and we’ll provide you with a preliminary estimate of value in less than two minutes. This won’t replace a home appraisal, but it can be a helpful starting point.![]()

Start With a Free Home Value Estimate

What happens to your home when you get a divorce?

Getting a divorce means taking the assets you’ve shared together and dividing them, so that you and your ex-spouse can go your separate ways. When you own a home together, timely decisions need to be made.

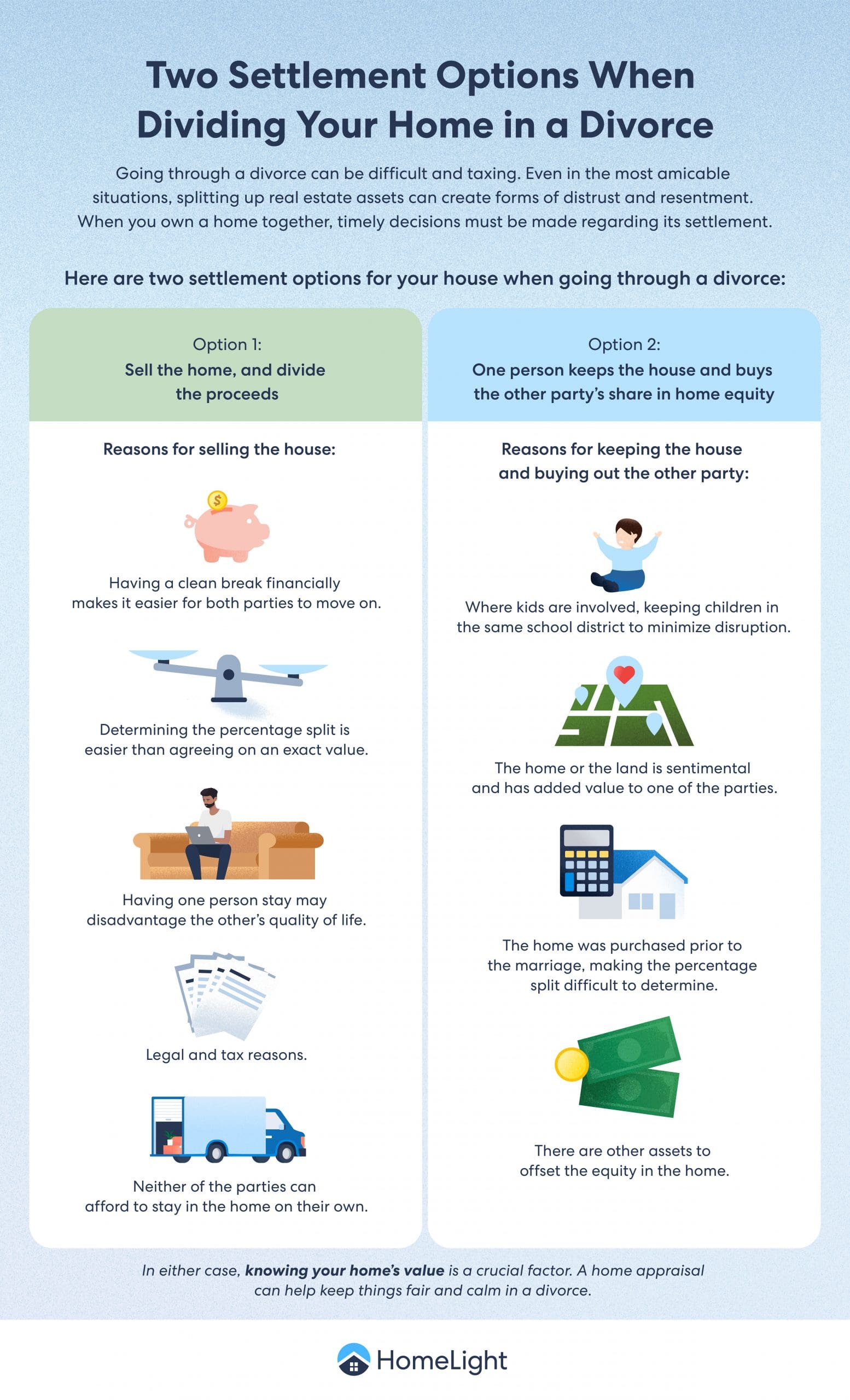

For the most part, there are two options:

- You both move out, sell the home, and divide the proceeds

- One person stays and buys out the other for their share of the home’s equity

According to Brown, “Selling a house which was purchased during the marriage and splitting the equity 50/50 happens in 95% of cases. In 5% of cases, someone keeps the home and refinances it in their name.”

How do you decide if it’s best to sell the home or keep it?

Several factors must be considered when deciding whether to sell the home and divide the equity or have one of the divorcing parties keep the home and buy the other out.

Typically, according to the experts, the most straightforward and cleanest solution is to sell the home and divide the proceeds. “You don’t want to have to work with your ex after the divorce,” states Brown, who has seen some situations turn nasty because of prolonged real estate entanglements.

Reasons for selling the house:

- Having a clean break financially makes it easier for both parties to move on.

- Determining the percentage split is easier than agreeing on an exact value.

- Having one person stay may disadvantage the other’s quality of life.

- Legal and tax reasons, such as the divorce judge mandating that the home be sold.

- Neither of the parties can afford to stay in the home on their own.

For the most part, the cases where one partner wants to stay and buy out the other are a bit more complicated. These include situations where the home was purchased prior to the marriage or if the parties have multiple real estate investments as assets. However, they can also include sentimental or other family-related reasons for keeping the home.

According to Kaminsky, “Sometimes couples factor in the disruption to kids caused by changing schools, putting them through an even more challenging situation because the home is being sold.”

Reasons for keeping the house and buying out the other party:

- Where kids are involved, keeping children in the same school district to minimize disruption.

- The home or the land is sentimental and has added value to one of the parties.

- The home was purchased prior to the marriage, making the percentage split difficult to determine.

- There are enough other assets to offset the equity in the home, such as a 401k or other property.

In either case, knowing your home’s value is an important factor in determining the right option.

But do you need to hire an appraiser at this stage? It depends on your situation. Using other methods to determine the ballpark value might be enough for some circumstances, and depending on which option you choose, an appraisal may be the right step down the road.

Let’s take a closer look at your options.

If you are selling the home in a divorce, what’s next?

The first thing you should do when selling the home is to determine each party’s percentage of homeownership. What happens next depends on when the home was purchased.

The home was purchased during the marriage

If the home was purchased during the marriage, then in most cases, any proceeds will be split 50/50 between the parties. This point is sometimes misunderstood when comparing common law states vs. community property states. While common law allows for one married individual to hold separate property that is only in their name, in the case of a marital home, equitable distribution usually applies, mandating that the property should be distributed equally.

Of course, there are exceptions to this, and you should consider hiring a divorce attorney to make sure your situation is covered without any hiccups.

The home was purchased by one party before the marriage

If the home was purchased by one party prior to the marriage, determining the percentage of ownership is a lot trickier. According to Brown, “Most people don’t know how to divide real estate that was purchased with pre-marital money. You need a professional who understands the law and how to calculate the ownership.”

Next, you’ll need to hire an agent who is experienced with selling property due to divorce.

Because you’ve already determined the percentage split of the proceeds, both parties should be incentivized to sell the home for as much as possible, which makes the fiduciary job of an agent representing both parties much easier.

It is always challenging as a real estate professional to represent the fiduciary duties to both parties, but is easier when both parties agree.

Ed Kaminsky Real Estate AgentCloseEd Kaminsky Real Estate Agent at The Kaminsky Real Estate Group Currently accepting new clients

Ed Kaminsky Real Estate AgentCloseEd Kaminsky Real Estate Agent at The Kaminsky Real Estate Group Currently accepting new clients

- Years of Experience 39

- Transactions 1589

- Average Price Point $2m

- Single Family Homes 1043

During the course of a normal home sale, your real estate agent performs a comparative market analysis (CMA), which looks at comparable home sales in your area to provide an estimated value for your home.

In most cases, where the percentage split is agreed upon before selling the home, a CMA is probably enough of an estimate of value to determine the list price and sell the home. In this situation, you may not need to get a home appraisal.

If one person in a divorce wants to keep the home, what’s next?

If one person decides to stay in the home, the most common option is for the person to do a cash-out refinance to use the current equity to pay cash to buy out the other party.

The person doing the refinance will typically end up with a much larger payment for the home and needs to make sure they can afford it. According to Brown, this could cause residual resentment because “you are basically mortgaging your ex’s payout over the next 30 years.”

Another option is for the person who wishes to stay in the home to offset the value through other assets. “You could use other assets to offset the home equity, such as investment accounts and 401ks, other investment properties, or even gifts from wealthy family members,” Brown says.

You need to determine the value of the home to make either of these options work, which can be difficult, especially in volatile and rapidly changing markets. In this case, getting a home appraisal is an essential part of the process.

What should you expect to happen during the appraisal process?

Appraisers go through extensive training to develop the expertise required to assess the value of a home and must get a professional license. Along with visiting your home, a licensed appraiser will compare your house to other houses that have sold recently, looking at factors such as the home’s condition, location, and size, to determine its comparative value.

An appraisal typically costs between $300 and $500, but it’s one of the costs you should expect to pay during the course of a divorce that involves joint property. The appraisal report typically comes back in less than a week. The appraisal results can take longer if the home is unusual, unique, or a high-end property.

Using an upfront appraisal to price your home is not to be confused with the appraisal that happens on behalf of the buyer of the home after a house goes under contract.

To be clear, an appraisal paid for by the sellers before listing the home does not negate the need for the buyer’s appraisal later in the transaction. For a mortgage-backed purchase, the lender will still require a separate appraisal (covered by the buyer) to make sure they aren’t financing a loan for more than the home is worth.

What happens when the divorcing couple can’t agree on the appraisal?

Kaminsky has seen problems between divorcing couples sprout up from the start when they can’t agree on a real estate agent or an appraiser, not to mention what repairs need to be done prior to the sale, and the list price.

“The biggest friction point with home values and divorcees is getting to an agreement on the appraisal value. If one party doesn’t agree, you can get a second appraisal, and then you can compare and see how close they are. If there still isn’t agreement, then you’ll need to put it before a mediator or a judge,” Kaminsky says.

Common options for parties that don’t agree on the appraisal value:

- Each party hires its own appraiser and takes the average of the two values.

- The parties hire a third-party mediator to come to a mutual decision on value based on the appraisals.

- The parties take the issue of the home’s value to court and let a judge make a determination, which may even result in conducting a third court-appointed appraisal.

Finding the right professional to perform the home appraisal may be easier than you think, and it’s always best to get a referral. Your real estate agent and attorney should have lists of trusted appraisers available in your area.

How can I prepare the home before an appraisal?

In the case of a buyout, keep in mind that both parties aren’t equally invested in getting the home appraised for the highest amount. The party that is staying in the home will prefer a lower appraisal so that the buyout amount is lower, while the party leaving will want a higher amount.

If you’re the party receiving the buyout, here are some helpful tips for how you can prepare the home to get the highest appraised value:

- Prepare a home fact sheet, including details such as the type of materials, information about schools, and any recent upgrades.

- Make minor repairs so that the appraiser doesn’t notice any patterns of neglect.

- Secure your pets to make sure they don’t interrupt the process or annoy the appraiser.

- Spruce up your curb appeal by mowing the lawn and tidying up the landscape.

At what point during the process should we get the appraisal?

According to Brown, the division of assets due to divorce happens at the time that the divorce decree is executed (signed) and made official. But anyone who has gone through a divorce knows that it often takes months and sometimes years to come to an agreement on the final terms before the decree can be finalized.

This is problematic when dealing with the value of real estate because the market is always changing. According to Kaminsky, “We’ve had to re-appraise houses due to market volatility. If things get postponed for three or four months, we have to go revalue because, in that short time, values may have changed significantly.”

Experts agree that in situations where an appraisal is needed, getting it as close to mediation or the court date is important. In some situations, it is even possible to choose the appraiser beforehand and have the appraisal happen once the divorce is official in order to ensure the value is as up-to-date as possible.

How can a cash offer be a good option to sell your home during a divorce?

If you’ve decided to sell your home as part of the divorce, you may consider seeking a cash offer to make the process simple. In today’s market, it’s becoming more and more likely to get a cash offer on your home.

In some cases, you may want to move faster than a typical sale and avoid the potential hassles of working together to list the home. A platform like HomeLight’s Simple Sale can help you receive a cash offer in as few as 24 hours and avoid conflicts that can arise when trying to coordinate a traditional home sale during a divorce.

The benefits of an all-cash offer:

- Less time you have to work with your soon-to-be ex to sell your home.

- Removes the need to agree upon and organize cleaning and home repairs prior to listing.

- Removes the hassle of coordinating showings or open houses.

- Makes the whole process more private (no “for sale” signs or public listings).

- Removes extra out-of-pocket costs such as appraisal, attorney, and financial advisor fees.

A no-obligation Simple Sale cash offer can help you keep the home sale process fast and convenient.

Need to Sell Your Home in a Divorce?

Going through a divorce or separation can be a difficult time. If you’re selling your home, explore the possibility of requesting a no-obligation cash offer through our Simple Sale platform. No staging, no repeated showings, no open houses.

A home appraisal can help keep things fair and calm in a divorce

The need for a home appraisal depends on whether you’re selling the home prior to the divorce or if one person is planning on keeping the home. If you are selling the home, coming to an agreement on each party’s equity percentage is most important.

In this case, partner with a top agent who has experience selling a home due to divorce. HomeLight can connect you with highly rated agents in your market based on their actual performance history. From there, you get to pick the best one to meet your individual needs.

If one party is planning on staying in the home, getting an appraisal is typically the best way to keep things civil and fair.

If you’re curious about what your home might be worth right now, try HomeLight’s Home Value Estimator. This free online tool can provide a ballpark estimate of your home’s worth in less than two minutes.

Editor’s note: This article is for educational purposes only, not financial, tax, or legal advice. HomeLight always encourages you to reach out to an advisor regarding your own situation.

Header Image Source: (Karolina Grabowska / pexels)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.