Who Keeps the Earnest Money Deposit if a Home Sale Falls Through?

- Published on

- 8 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

According to transaction data, home sales are falling through at a higher rate than in recent years. When a sale falls apart, one of the first questions sellers and buyers ask is: Who keeps the earnest money deposit?

The answer depends on why the deal fell through and what the purchase agreement says. If the buyer backs out for a reason protected by a contract contingency, they usually receive their earnest money back. If the buyer cancels without a valid contingency, the seller may be entitled to keep the deposit.

In this guide, we’ll explain how earnest money works, when buyers get it back, and when sellers may legally keep it.

A Top Agent Can Weed Out Bad Offers

Use HomeLight’s free Agent Match platform to find a top-rated listing agent who knows how to attract qualified buyers and get you the highest proceeds possible. We analyze over 27 million transactions and thousands of reviews to take the guesswork out of finding a great agent.

What is an earnest money deposit?

Earnest money is a good-faith payment that shows the buyer is serious about purchasing your home. Buyers typically submit these funds shortly after their offer is accepted. The money is then held by a neutral third party until the transaction closes or the contract is canceled.

The deposit provides the seller with financial protection if the buyer backs out without justification.

If the transaction closes successfully, the earnest money is credited toward the buyer’s down payment or closing costs.

Linda Quinn, a top real estate agent in Portland, Oregon, with 50 years of experience, explains that the earnest money deposit is often considered an important element reinforcing a legally binding home purchase agreement.

“There are four necessary things to actually have a legal contract: the start and stop dates, the parties to the transaction, and then the compensation,” she says. “Without the deposit, it is unlikely that it would have the legal definition of a contract between a buyer and a seller.”

How much is a typical earnest money deposit?

The amount of earnest money your buyer offers will vary depending on the market and the price of your home. Common ranges include:

- 1% to 3% of the purchase price in many markets

- Higher deposits in competitive markets to strengthen an offer

- Smaller deposits, such as $1,000–$2,000, in slower markets or lower-priced transactions

For example, on a $500,000 home, a typical deposit might range from $5,000 to $15,000.

Try our earnest money calculator

To get an idea of what you can expect, check out the earnest money calculator below:

Who keeps the earnest money if the deal falls through?

As the seller, you can keep the earnest money if your buyer breaches the contract or backs out without a valid contingency reason. If the sale falls through due to a valid, unmet contingency, such as a failed inspection, appraisal, or loan denial, the buyer usually gets the deposit back.

When the seller keeps it:

Sellers typically receive the earnest money only if the buyer breaches the contract without a valid contingency. Some situations:

- The buyer simply changes their mind

- The buyer misses contract deadlines

- The buyer refuses to close despite meeting all contingencies

- The buyer cannot complete the purchase for reasons not covered in the contract

In these situations, the deposit can serve as compensation to the seller for lost time and opportunity. It can be frustrating to have taken your home off the market and stopped accepting offers, and then have the buyer walk away from the deal.

When the buyer gets it back:

If the cancellation occurs within the contractually allowed “due diligence” period or because of a failed contingency (for example, financing falls through or the inspection reveals major issues).

If the parties cannot agree on who receives the money, the funds typically remain in a neutral third-party account until a court order or signed release determines how the deposit will be distributed. In some cases, both parties agree to cancel the contract and return the funds.

“All of the earnest monies that we’re working with go to a neutral party, which is escrow,” Quinn explains. “In some states, there are trust funds set up by the real estate companies, and they will hold the earnest money deposit for the buyer.”

Next, let’s look at the most common contingency clauses that determine whether a buyer keeps their earnest money if a deal is canceled.

How contingencies protect the buyer’s earnest money

Most home purchase contracts include contingencies, which are specific conditions that must be satisfied before the sale can proceed. If one of these conditions fails, the buyer can typically cancel the deal and receive their earnest money back.

Common contingencies include:

- Inspection contingency: If a home inspection reveals significant problems, the buyer may renegotiate repairs or cancel the contract and recover their deposit.

- Appraisal contingency: If the home appraises for less than the agreed purchase price and the buyer and seller cannot renegotiate, the buyer can walk away without losing the deposit.

- Financing contingency: If the buyer cannot secure a mortgage despite making a good-faith effort, the contract may allow them to cancel and receive their earnest money back.

- Home sale contingency: Some buyers include a clause allowing them to cancel if they cannot sell their current home first.

Quinn notes that buyers often have several built-in opportunities to exit a contract while protecting their deposit.

“The interesting thing is the buyers really have a lot of the control,” she says. For example, buyers may receive a short window to review the seller’s property disclosure and withdraw if they’re uncomfortable with what they learn. “They can get out for almost any reason after the receipt of that paperwork.”

Inspection and financing contingencies can also extend close to the closing date. Quinn notes that a financing contingency is also known as a mortgage contingency. “That means if they don’t qualify for financing or they lose their job, they get their money back.”

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

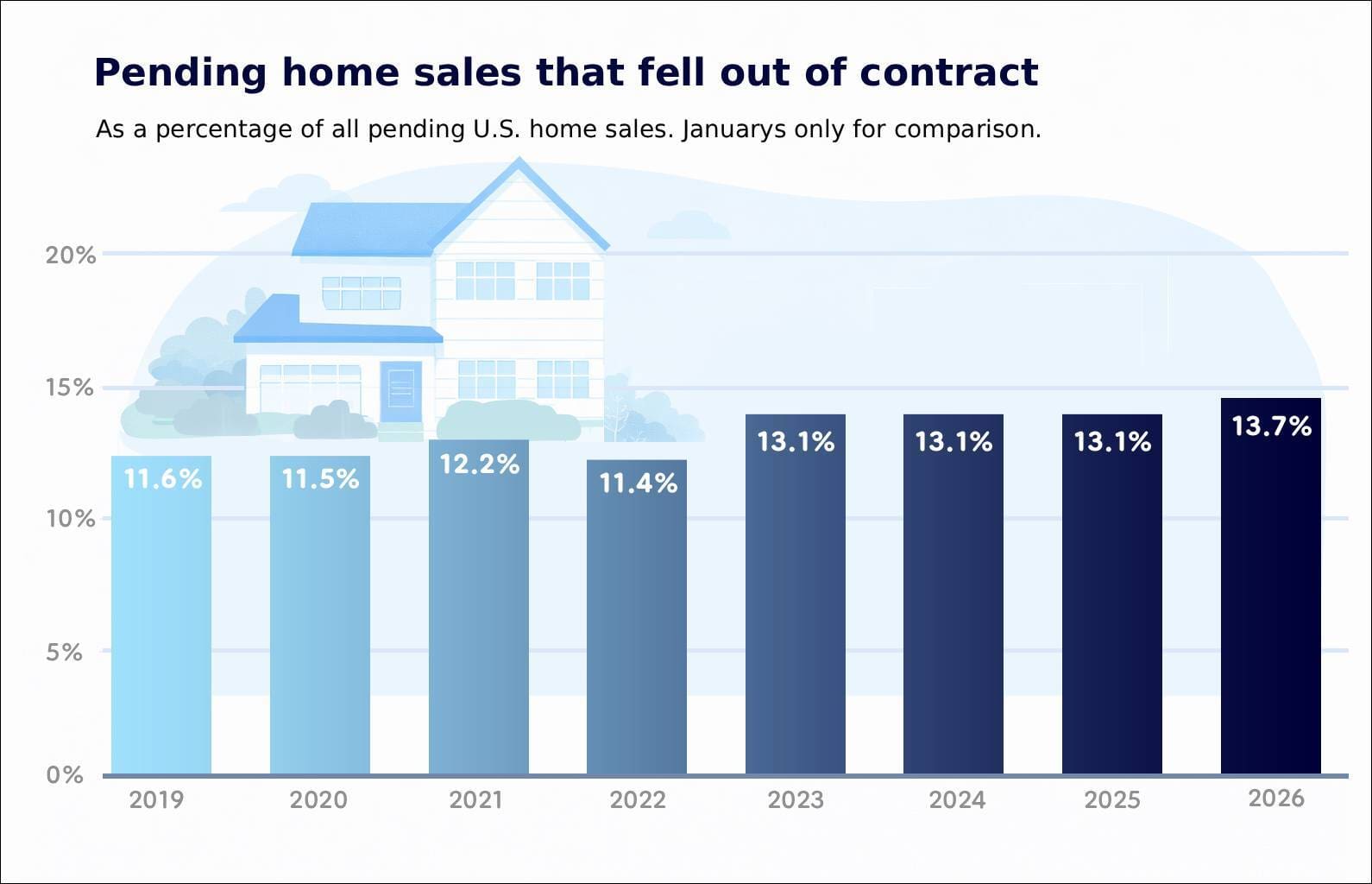

How often are pending home sales canceled?

On average, about 10%–16% of pending home sales fall through each month in the U.S. The percentage of sales falling through has increased in recent years.

According to a recent Redfin report, 13.7% of U.S. home purchase agreements were canceled in January 2026, the highest January rate since the company began tracking the data in 2017. That’s roughly 1 in 7 pending sales, or about 40,000 deals that fell out of contract in a single month.

The report notes that cancellation rates tend to be seasonal, with the lowest share typically occurring during the spring homebuying season. Conversely, cancellations often spike at the end of the year and into January. For example, in December 2025, the cancellation rate was roughly 16.3%.

Market conditions also matter: Cancellations are often lowest when inventory is tight, and competition is high, forcing buyers to stick with contracts, whereas higher cancellation rates occur when buyers have more choices, leading some to back out during inspections in favor of better options.

How sellers can reduce the risk of a canceled deal

While earnest money offers some protection, most sellers would still prefer the deal to close rather than collect the deposit. To reduce the risk of a contract falling apart, here are some things Quinn suggests you can do:

- Review buyer financing carefully

- Ask for a stronger earnest money deposit

- Limit certain contingencies in competitive markets

- Work with an experienced real estate agent

In a strong seller’s market with multiple offers, some buyers may even waive contingencies to make their offer more attractive. There are also modern ways buyers can make a non-contingent offer on a home, such as buy–before–you–sell programs.

If you’re selling and buying at the same time, check out HomeLight’s innovative Buy Before You Sell program. This buy-sell solution unlocks the equity in your current home, simplifying the entire process. You can make a stronger, non-contingent offer on your new home and only move once. Watch the short video below to learn more.

The bottom line on who keeps earnest money deposits

Earnest money deposits help reinforce commitment between buyers and sellers like you during a home transaction. If your home sale falls through, who keeps the deposit depends largely on the contract and the reason for the cancellation.

In most cases:

- The buyer gets the earnest money back if the deal falls through due to a valid contract contingency, such as financing, appraisal, or inspection issues.

- The seller keeps the deposit if the buyer cancels the contract without a protected reason or misses the required deadlines.

- If there’s a dispute, escrow holds the funds until both parties agree or a court decides.

Because rules and timelines can vary by state and contract terms, both sellers and buyers should carefully review their agreement and consult a knowledgeable real estate professional to protect their interests.

HomeLight’s free Agent Match platform can connect you with a trusted, top-rated local agent with a track record for navigating buyer contingencies and finding a qualified buyer so you can close your sale and move on.

Writer Lauren Vella contributed to this post.

Header Image Source: (Curtis Adams/ Pexels)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.