How to Buy a House Before You Sell Yours (Without the Hassle!)

- Published on

- 12 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

You’re downsizing, upsizing, or want a much-needed change of scenery. While browsing for a home, you’re awestruck by a beautiful abode. Between the modern upgrades and spacious rooms bathed in natural light, it checks all your boxes.

You’re ready to make an offer, but there’s a big caveat: You already own a house, and you need the equity from it to afford your dream upgrade. How do you buy a house before you sell yours — and is it possible to make this work?

Yes, You Can Buy Before You Sell. Why Move Twice?

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

The buy-sell conundrum

Now that you’ve graduated into repeat buyer status, the equity you’ve built in your current house over time can be a springboard for your next purchase.

Homeowners are equity-rich

According to property analytics company Cotality, the average U.S. homeowner has $299,000 in equity in the third quarter of 2025. While it’s a significant financial asset, it’s also not always easy to access when you need it.

Many people can’t buy without it

Many repeat buyers need to use equity from their existing homes to buy the new ones they want. That equity is taken into account when a lender looks at the amount of funds they’re willing to provide. It can also make putting money down a whole lot easier or even enable you to buy your next place with all cash.

Selling first has its own risks

Since you can’t pry open your roof and extract that equity with a crowbar, it can be hard to get the money you need when you need it, let alone time everything right. Some people choose to sell their place first and hope they can find a new house quickly thereafter — but that, too, can feel risky, especially in a market where there aren’t many houses for sale.

You do have options if you want to buy before you sell to remove the stress of moving twice. Here’s a step-by-step guide on how to do it.

Step 1: Assess your financial position

1. Estimate home equity

Using the median home price of around $405,000 and assuming you have an outstanding mortgage of $280,000, this formula will help determine your available equity:

Current home value – outstanding mortgage = available equity

Example:

$405,000 − $280,000 = $125,000 equity

2. Calculate required down payment

Assuming your lender requires the standard 20% down payment, your new home purchase of a median-priced home would require:

0.20 × $405,000 = $81,000 needed

3. Determine your total cash shortfall

Down payment − available equity = cash gap

Example:

$81,000 – $125,000 = –$44,000

Step 2: Explore ways to buy a house before you sell yours

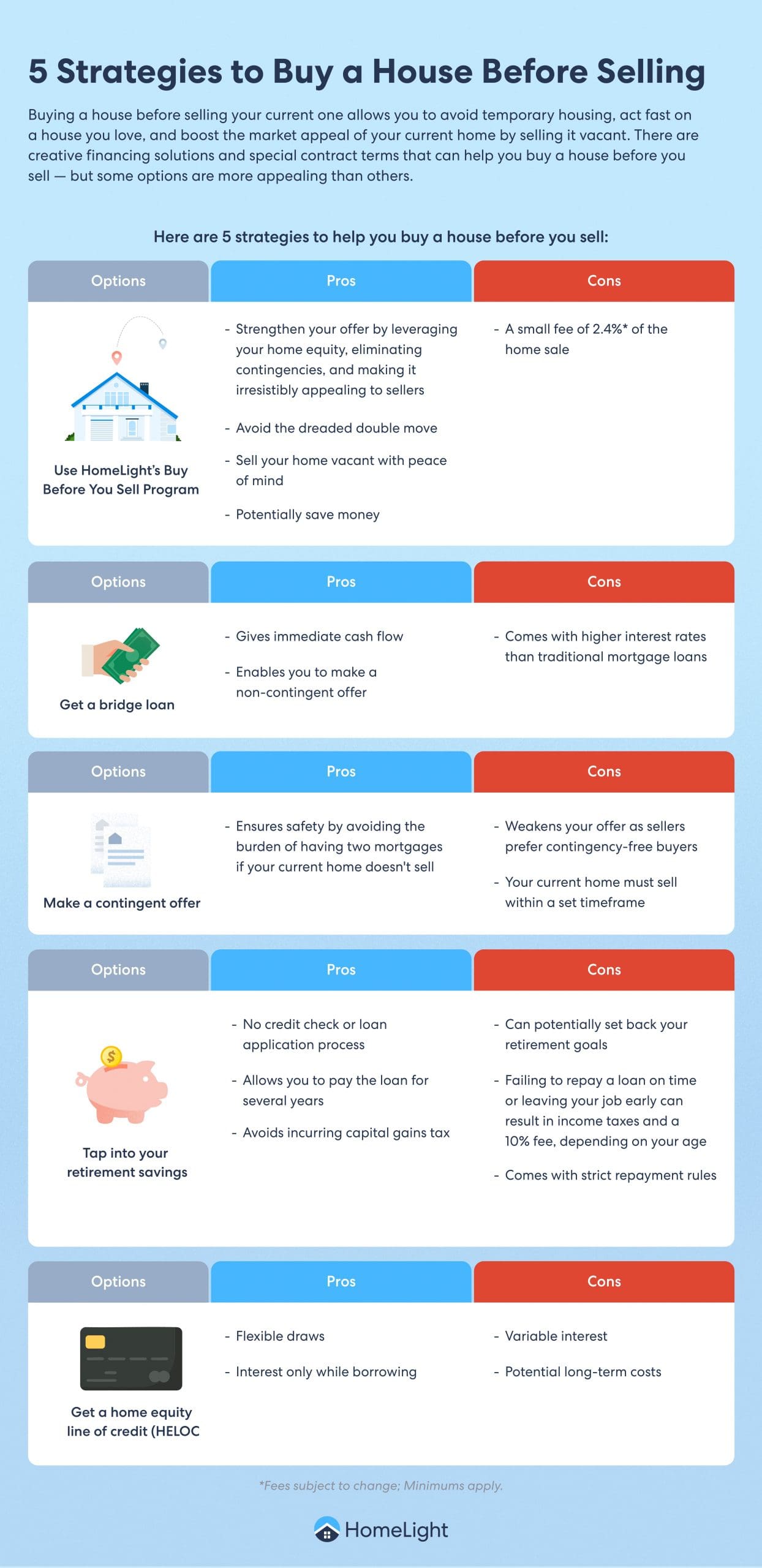

Creative financing solutions and special contract terms can help you buy a house before you sell yours, but some options are more appealing than others.

1. Use HomeLight’s Buy Before You Sell program

Highlights:

- Fronts up to ~80% home equity

- Flat fee ~2.4% of sale price

- Avoids multiple mortgages and bridge-loan interest

It can be tricky to time the sale of your current home with the purchase of another one. Historically, the options available to buyers in this scenario have left a lot to be desired.

However, innovative solutions like HomeLight’s Buy Before You Sell (BBYS) program are specifically designed to make the process much, much easier. Here’s a short video illustrating how this modern program works:

Here’s what you can expect to happen when you use Buy Before You Sell:

- Unlock your equity: Tell us a little bit about your situation, and we’ll help you unlock a portion of your equity as quickly as a few hours later. We’ll tell you how much you can access, based on factors like your home value, outstanding loans, and your financials.

- Use your funds: You can put that equity toward the down payment on your next home, moving expenses, closing expenses, or property repairs.

- Make a strong offer: Now, you’re ready to make a non-contingent offer on your dream home. In competitive markets, this can be a game changer.

- Sell your existing home: Work with your agent to list your vacant home on the market to attract the strongest offer possible. Having already moved out, you won’t have to worry about selling a house that you’re still trying to live in.

Pros

HomeLight’s Buy Before You Sell program, in many ways, is the ideal solution for a variety of scenarios, whether you’re upgrading your home or downsizing to a smaller place.

If you have little ones and furry friends, it can be a lifesaver. We’ve also found it helpful for those in the challenging situation of going through a divorce who want to act fast and simplify their move.

BBYS allows you to:

- Make a stronger offer: A home sale contingency is kryptonite for a real estate deal. BBYS allows you to tap into a portion of your home equity as quickly as the same day and make that beautifully simple, non-contingent offer sellers love to see.

- Avoid the dreaded double move: Move once, and let us handle it from there. There’s no need to hire multiple movers, put your stuff in storage, or find a couch to crash on.

- Sell your home vacant, with peace of mind: Forget having to coordinate showings around your kids’ schedules, late-night clean-up, and worrying about dog care. You’ll work with a top agent to boost the value of your existing home with professional staging touches.

- Potentially save money: Agents estimate that removing the home sale contingency from a contract can help a buyer save significantly on a home’s sale price.

Cons

A (small) fee! BBYS is free to get started and see how much equity you can unlock. If you decide to use the program, there is a flat fee of 2.4% of the departing residence home sale.

However, these costs are potentially more than offset by the savings you’ll make on moving expenses, lodging, and the price of your new home when using BBYS.

In addition, the fees for HomeLight’s BBYS are typically much lower than the interest rates associated with bridge loans, which vary anywhere from 8%-10%.

2. Get a bridge loan

Highlights:

- Interest rate: Around 8%–10% APR

- Example:

- Loan = $100,000

- Term = 6 months

- Total interest ≈ $4,000 ($100K × 8% ÷ 2)

- Monthly cost ≈ $666

A bridge loan is a type of short-term loan typically lasting six or 12 months. It allows you to borrow against the equity of your current home, giving you the funds you need to finance your next property.

Pros

Bridge loans give you immediate cash flow, allowing you to move quickly when you find your dream home. Depending on the amount of funds you qualify for, getting a bridge loan often means you only need to move once, avoiding the hassle of temporary housing. It can also enable you to make a non-contingent offer.

Cons

Since bridge loans are short-term and more risky for lenders, they tend to have higher interest rates than traditional mortgage loans. Bridge loan rates often reflect the prime rate or up to the prime rate plus two percentage points.

3. Make a contingent offer

Highlights:

- No additional financing

- Likely requires competitive pricing or concessions

In your purchase contract, you can include a clause that the purchase of the new home is contingent on the sale of your current one. If the seller accepts your offer, the sale of their home is conditional upon you selling your current house within a certain timeframe.

If you can’t sell your current home within that period (which can range from a few weeks to several months, the contract allows you to back out of the purchase). You’ll typically get your earnest money deposit back.

Pros

This strategy provides safety in that you won’t end up with two mortgages if your current home doesn’t sell. You also won’t pay fees for a short-term loan.

Cons

A home sale contingency generally weakens your offer, especially in competitive markets, as sellers prefer buyers who can move forward without contingencies. To make the offer more attractive, you might have to increase your price. Also, your current home must sell within a set timeframe, which can be stressful.

4. Tap into your retirement savings

Highlights:

- Borrow up to 50% of vested balance (max $50k)

- Interest paid back into your account

Tapping into your retirement savings to finance the purchase of a new home is another option available to some buyers. Many retirement accounts, such as 401(k) plans, allow you to borrow against the funds you’ve accumulated over the years.

When you borrow from your retirement account to purchase a new home, you’re essentially taking out a loan against your future self. You’ll be required to repay the amount you borrowed, typically with interest, over a specified period. Depending on the rules of your retirement plan, you may be able to borrow up to half of your vested balance or a maximum of $50,000, whichever is lower.

Pros

Since you’re borrowing from your own savings, there’s often no need to go through a credit check or loan application process. This can be especially helpful if you have less-than-stellar credit or need to access funds quickly.

Many retirement plans offer flexible repayment terms, allowing you to repay the loan over several years. Additionally, the interest you pay on the loan goes back into your retirement account, essentially paying yourself back.

If you were to sell investments to finance your new home purchase, you might incur capital gains tax. By borrowing from your retirement savings, you can avoid this tax.

Cons

By borrowing from your retirement account, you’re reducing the amount of money you have working for you in the market. This can potentially set back your retirement goals, especially if you don’t repay the loan promptly.

If you fail to repay the loan within the specified timeframe or leave your job before repaying the loan, the borrowed amount may be considered an early distribution. This could result in income taxes and a 10% early withdrawal penalty, depending on your age.

Retirement account loans also come with strict repayment rules. If you miss a payment or can’t repay the loan within the specified period, you could face tax consequences and penalties.

5. Get a home equity line of credit (HELOC)

Highlights:

- Rate: Often variable, say prime + 1% ≈ 8%.

- Example:

- Draw = $140,000

- Annual interest ≈ $11,200

- Monthly = ~$933

A home equity line of credit (HELOC) allows you to borrow against the equity in your current home, typically through a revolving line of credit. You can draw funds as needed — similar to a credit card — and pay interest only on the amount used. This flexibility makes it a popular option for buyers who need access to cash before selling their existing home.

Pros

- Flexible draw schedule

- Interest-only payments during the draw period

- Typically lower rates than personal loans or credit cards

Cons

- Variable interest rates can rise over time

- Requires strong credit and sufficient equity

- Risk of owing on two properties if your home doesn’t sell quickly

Monthly cost comparison of buy-before-you-sell financing options

Given the options listed above, let’s take a look at what your monthly payment might look like for a $140,000 loan amount:

|

Financing option |

Loan amount | Rate | Term | Estimated monthly payment |

Notes |

| HomeLight BBYS | $140,000 | Flat | Upon resale | N/A | One-time fee of $10,080 (2.4% of $420K) |

| Bridge loan | $140,000 | 8% | 6 months | ~$933 | Total interest ≈ $5,600 (based on $140K loan) |

| 401(k) loan | $40,000 | 4% | 5 years | ~$737 | Paid back into retirement account; Might need additional financing to cover the remaining amount |

| HELOC | $140,000 | 8% | Revolving | ~$933 (interest only) | Variable rate, interest-only initially |

Step 3: Compare pros and cons by strategy

All the program options have different structures and terms that might confuse a homeowner who just wants to secure a new house before selling their current home.

Here’s a handy comparison table of the pros and cons to guide you:

|

Financing option |

Pros |

Cons |

| HomeLight Buy Before You Sell | Fast equity access, one-time flat fee, strong non-contingent offer | Flat fee (2.4%), must later repay via sale |

| Bridge loan | Fast, non-contingent offer, helps avoid double move | High interest (8%–10%), monthly payments on two homes |

| Contingent offer | No extra financing, fewer fees | Weaker offer, risk of losing house, may require concessions |

| Retirement account loan | No lender credit approval, interest paid to yourself | Reduces retirement savings, has penalties if not repaid on time |

| HELOC | Flexible draws, interest only while borrowing | Variable interest, potential long-term costs |

Step 4: Choose the right strategy

Now that you understand the available financing options, it’s time to match one with your financial situation and comfort level. Use this step to narrow down your approach based on what fits best.

- Decide required funds by calculating down payment gap

- Weigh monthly costs vs. one-time fees

- Consider market competitiveness and your risk tolerance

- Consult a lender or agent to get pre-approval or run program comparisons

Step 5: Execute the plan

With your strategy chosen and financing lined up, you’re ready to take action. This step outlines the order of operations to buy your new home and sell your current one smoothly.

- Get pre-approved based on your chosen financing

- Make offer (non-contingent if possible)

- Close and move into your new home

- Sell existing home when ready — list vacant for faster sale

- Repay short-term funding from sale proceeds

Can you buy a house without selling yours first?

Yes, buying a house before you sell yours is possible, but it can be challenging.

The process traditionally requires you to make a contingent offer on your new home, which stipulates that the purchase depends on the sale of your current residence. But this can put you at a disadvantage against other buyers who can make clean offers with less perceived risk for the seller.

“I think that contingencies are really tough right now,” says Aleana McMurray, a top real estate agent in Seattle. “If you have a home that is for sale in a less desirable area, it may sit for longer, so a seller is less likely to accept a contingent offer, and it’s nearly impossible in a competitive offer situation.”

Alternatively, some people use a bridge loan or tap into their savings to buy first. Yet, these options can make anyone nervous and strain their finances.

In recent years, a number of creative financing solutions have cropped up to address these obstacles to buying a house before you sell. HomeLight’s Buy Before You Sell program is one of them.

What are the benefits of buying a house first?

Now that we answered the pressing question, “Can you buy a house before selling yours?” let’s consider the advantages of choosing this route. In the complex process of moving and managing multiple real estate transactions, buying your next home before selling can offer these benefits:

1. You can avoid costly rentals (or your friend’s couch).

When you sell a house before you buy a new one, it frees up any equity you’ve gained (after accounting for selling fees) and is likely to boost your buying power. But doing things in this order can also leave you without a place to live.

People typically spend an average of 10 weeks searching for a home. There’s no guarantee you’ll find something you like right away. Until you do, you’ll have to figure out a temporary place to stay and where to put all your stuff.

When you buy a house first, you avoid having to move twice. A one-and-done move can be a godsend for anyone who hates moving (okay, so everyone), especially parents who know that if you disrupt the kids’ schedules, there will be hell to pay.

2. You can act fast on your dream home.

It takes two to three months to sell a home, and sometimes longer. If you find a house you want to buy but wait to sell yours to make a move, there’s a good chance it’ll be long gone by the time you put in an offer.

“Any houses that come on the market that are move-in ready and are up to date with the latest trends are very competitive and are not lasting long at all,” says Jacobe Kendrick, an agent with over 11 years of experience serving the Midland, Texas area.

While your financial circumstances must allow you to buy first, doing so lets you move much quicker and reduces the risk of losing your dream home to another buyer.

3. You won’t have to sell your house while living there.

Clutter, dirty dishes, unmade beds — these are the realities of a lived-in home. With kids and pets around, the mess can pile up even faster.

Trying to sell your house and maintain the appearance of perfection to buyers can be exhausting. However, you can often sidestep that living nightmare when you buy a house first, enabling you (or you plus the fam) to get settled in your new residence while selling your previous home from a safe distance.

Your daily life won’t be disrupted, and your house will look like a million bucks (or at least like the top range of its market value!). For real though, a vacant, well-staged home can sell for more.

Are there any challenges to buying a house before selling?

While buying a house before selling your current one can be advantageous, it’s not without challenges.

1. How will you afford it?

If you want to buy before you sell, you’ll need to figure out how to afford it. For most people, the obvious answer is using equity from their existing home. But until your current home sells or you get a special loan, these funds can remain out of reach, potentially complicating your ability to secure a down payment for your new home and meet lenders’ approval criteria.

2. How long will it take to sell?

Uncertainty about the time your previous home will sell can also be stressful. Until your old home sells, you’ll be responsible for managing the costs for both properties. This includes not only mortgage payments, but also taxes, utilities, insurance, and maintenance. These additional financial responsibilities can add up quickly.

3. Will your offer be competitive enough?

While buying a home before selling your current one allows you to quickly act on a property you love, it can make your offer less attractive. Sellers may favor buyers who are not contingent on selling their own home, considering them less risky. This situation can potentially put you at a disadvantage in competitive markets.

If you need to buy first, let us help!

In the past, there haven’t been a ton of great options to buy a house before you sell your current one. You either had to make a contingent offer, take out an expensive bridge loan, or dip into savings you’re counting on for later in life.

However, it’s our mission at HomeLight to remove these obstacles. With our Buy Before You Sell Program, you can unlock your equity upfront, avoid a double move, and sell your current house with peace of mind. If you’ve already found a home you love and want to learn more details, we’d love to connect with you.

Writers Stephanie Mickelson and Caroline Feeney contributed to this post.

Header Image Source: (Spacejoy / Unsplash)

FAQs about buying before you sell

Yes, it is possible to buy a house before selling your current one, but it can be challenging. You can make a contingent offer on the new home, use a bridge loan, or tap into savings.

However, these options can strain personal finances or make your offer less appealing to sellers. HomeLight’s Buy Before You Sell program is a great alternative solution, allowing you to tap into your home equity quickly for a non-contingent offer, potentially saving you money and avoiding the hassle of moving twice.

Buying a house before selling your current one allows you to avoid temporary housing, act fast on a house you love, and boost the market appeal of your current home by selling it vacant.

Several challenges can arise when buying a house before selling your current one, including the difficulty in accessing home equity, which is often needed for the new purchase. There’s also the uncertainty of not knowing when your current home will sell, during which time you’ll have to bear the costs of both properties.

Additionally, your offers might be perceived as weaker, especially if they’re contingent on the sale of your current home or if you face financial limitations. HomeLight’s Buy Before You Sell program solves these challenges.

HomeLight’s Buy Before You Sell program allows you to tap into your home equity quickly and use the funds for a down payment on your next home, moving expenses, closing expenses, or property repairs. You can then make a non-contingent offer on your dream home and list your existing home on the market without worrying about living in it during the sale process.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.