Seller vs. Buyer: Who Pays for What When Closing on a Home?

- Published on

- 7 min read

-

Caroline Feeney Former Executive EditorClose

Caroline Feeney Former Executive Editor

Caroline Feeney Former Executive EditorClose

Caroline Feeney Former Executive EditorCaroline Feeney was previously HomeLight's Executive Editor / Director of Content. With 7 years of real estate reporting and editing experience, she previously managed content for Inman News and co-authored a book on real estate leadership. The Midwest native holds a master's from the Missouri School of Journalism and was formerly a real estate contributor for Forbes.

Have you ever wrapped up a delicious meal with friends and had someone reach for the check, a gesture indicating they plan to cover the bill for everyone? Well, dividing fees in a real estate deal is usually nothing like that.

For the buyer, a few thousand dollars saved could mean the ability to furnish their new living room. While they dream of Restoration Hardware, you as the seller have a target for how much you’d like to net at the end of the day. Each additional fee in the “debit” column of your closing statement raises your blood pressure!

But when selling a house, who pays for what largely depends on how negotiations go and whether you have a position of leverage in the current market. That said, market norms and regulations often create a default framework for real estate transaction fees in a given area.

For example, in many areas it’s customary for buyers to cover the lender’s title insurance policy, while sellers cover the buyer’s policy. Another common compromise is that buyers and sellers split escrow fees 50/50.

But wait! It gets a little more complex. Some fees that would seem to fall firmly in one camp can flip-flop if one party has power, like a seller who offers to cover a portion of a buyer’s mortgage fees in a down market.

As the seller, you’re looking to save where you can and to maximize the value of this transaction. Though this list is not entirely comprehensive, here’s a breakdown of common fees encountered in a home sale — and who typically pays for what.

| Cost item | Typical cost or percent of sale | Who usually pays for it? |

| Home prep and staging | $5,000-$6,000 | Seller |

| Pre-listing inspection | $340 | Seller |

| Agent commission | 5.8% | Seller |

| Transfer taxes | 0.1%-2.2% | Negotiable, though often the seller pays |

| General and specialized inspections | $340 and $100 per specialized inspection | Buyer |

| Loan application and origination fees | 1%-3% of loan amount | Buyer |

| Appraisal fees | $450-$550 | Buyer |

| Settlement fees | 1% | Split between buyer and seller |

| Title fees | 0.5%-1% of sale price | Split between buyer (lender’s policy) and seller (owner’s policy) |

| Property taxes | Varies | Buyer and seller pay for taxes accrued during the time they own the property |

| Home warranty | $900-$1,000 for a year’s worth of coverage | Seller may offer as incentive or in lieu of replacing older items in the home |

References consulted in our table of “Who Pays for What in a Home Sale?”: HomeLight Agent Commissions Calculator; HomeLight Ebook: How to Save Up for Your Dream House; HomeLight Net Proceeds / Easy Home Sale Calculator; HomeLight study: The Average Cost to Sell a Home in 2021; HomeAdvisor: 2021 Home Inspection Costs; HomeAdvisor: 2021 Land Survey Costs

Costs usually covered by the seller

Some of the major costs in the seller’s camp include any pre-listing work done to the home, the real estate agent commission, and in some states — transfer taxes. Let’s review what’s commonly on your tab.

Home prep and staging ($5,000-$6,000):

According to data from HomeAdvisor’s True Cost Guide using data collected from thousands of consumers, common projects sellers do to prep their house for sale total an average of $5,478. This includes 2021 estimates for:

- Dumpster rental: $381

- Deep clean: $168

- Paint interior: $1,886

- Replace carpet: $1,651

- Basic lawn care: $131

- Home staging: $1,261

Your costs will vary based on the projects your home needs as well as your location. For example, it costs nearly $10,000 to prepare a home for the market in San Francisco due to the area’s high cost of goods, materials, and services, according to HomeLight’s analysis of selling costs.

A buyer isn’t going to help you cover any of these costs — but how much work you put in will depend on market conditions and your desired price point. When in doubt, chat with a top real estate agent about improvements for your home that will be worth the investment.

Pre-listing inspection ($340):

It’s not required to inspect your home before you sell it. But you can voluntarily opt to get a pre-listing inspection as a strategic move. A pre-listing inspection follows the same procedures as a general inspection; the difference is that it’s paid for by the seller and done prior to the house going on the market. A pre-listing inspection can surface any issues that could later raise red flags with the buyer and cause a closing delay.

With knowledge about your home’s condition, you can decide whether to preemptively fix problems to maximize your resale value, or adjust your price accordingly. Keep in mind that you’ll likely be required to disclose the results of that inspection with buyers, so talk to your real estate agent about whether it makes sense to get one.

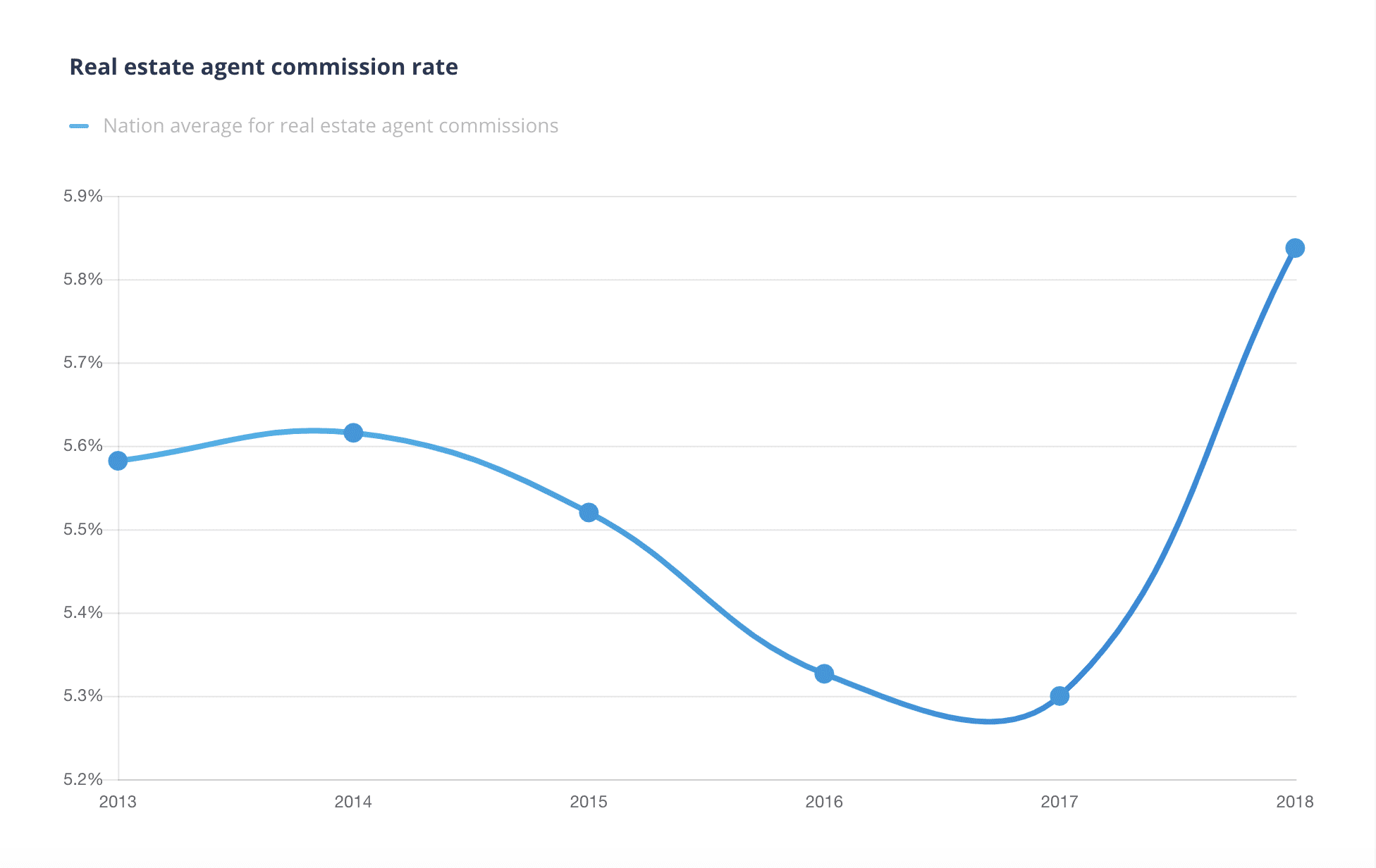

Agent commission (5%-6%):

In exchange for a real estate agent’s time, services, and expertise, sellers agree to offer a commission fee as a certain percentage of the sale at closing. According to HomeLight’s Commission Calculator, which uses real estate transaction data from thousands of home sales each year, the national average agent commission rate is 5.8%. On the sale of a median-priced $363,300 home, that amounts to $21,071. The exact commission rate you’re responsible to pay will be documented in your listing agreement.

It’s standard practice for the seller to cover this commission charge in its entirety. The payout is then usually split 50/50 with the buyer’s agent as a credit for bringing a buyer to the sale. In addition, it’s common for a listing agent to give their broker anywhere from 30%-50% of the commission (for a 50/50 or 70/30 split) depending on the agent’s experience, the market size, and their brokerage agreement.

Concerned about paying too much in commission? Thankfully, a great agent’s expertise can add significant value and help maximize your sale price. Researchers at leading real estate data company Collateral Analytics, now owned by Black Knight, found that FSBO (For Sale By Owner) sales sell for 5.5% less — and in some cases, nearly 6% less — than agent-assisted sales, indicating that the expertise real estate agents contribute immense value to the listing process.

That said, it’s critical that you work with a quality agent with a proven track record to get the outcome you desire. At HomeLight, we’ve found that the top 5% of real estate agents sell homes for as much as 10% more than the average real estate agent. Top agents will offer a detailed comparative market analysis (CMA), professional photography, postings of your property to all the major listing sites, exclusive home previews to other brokers, open houses, among other services as part of their commission fee.

Transfer taxes (0.1%-2.2%):

Local governments collect transfer taxes when property changes hands between seller and buyer. The purpose of these taxes is to generate revenue for the services provided by your city, county, or state (and sometimes all three). In many states, the responsibility to pay the transfer tax on the sale falls on the seller. However, in other states it’s negotiable or common for buyer and seller to split the expense.

While transfer taxes vary by locale, a study from the George Washington Institute of Public Policy reported that state transfer tax rates range on average from 0.1%-2.2%. But your transfer tax charge could look different. Thirteen states do not charge transfer taxes at all; meanwhile, these taxes can go up to 3%-4% for homes over a million dollars in some states. Review HomeLight’s state-by-state guide to real estate transfer taxes for further details.

Costs usually covered by the buyer

On the flip side, the buyer will generally be in charge of paying for any inspections they order to evaluate the home, the fees related to their mortgage, and the lender-ordered appraisal among other purchase expenses. Let’s review!

General and specialized inspections ($340 for general, an additional $100 for specialized):

Most buyers will write a home inspection contingency into the purchase agreement, giving them the right to order a professional evaluation of the property before closing. The costs to obtain the general inspection — as well as any specialized inspections to check for pests, radon, or lead-based paint, for example — will be the responsibility of the buyer to cover.

Loan application and origination fees (1%-3% of loan amount):

Any fees charged by the lender for services like processing the new loan request, credit checks, or evaluating and preparing the mortgage will default to the buyer’s list of expenses. If the buyer asks for a closing cost credit from the seller to cover all or a portion of these fees, that would be an explicit negotiation.

If you do decide to help the buyer with closing costs, know that Fannie Mae does set limits on financing concessions. For example, a seller can only offer a maximum 3% seller concession to a buyer with a conventional loan who puts down less than 10%. In that event, any additional amount offered would need to result in a reduction in the purchase price, dollar for dollar.

Appraisal fees ($450-$550):

If the buyer is purchasing the home using a mortgage, the lender involved will require an appraisal before closing. Although the lender selects the appraiser who will assign a value to the home, the cost of the appraisal will be charged to the borrower. The seller would only pay for an appraisal in the event they elect to getting a home appraisal to help price the home before it hits the market. However, usually the seller uses the CMA from their agent to complete this task instead.

Costs that can be split or may go either way

Sometimes real estate transaction fees don’t fall squarely on the buyer or seller. Some expenses may be split, while others can be negotiated one way or another.

Settlement fees (1%):

The title company, escrow company, or attorney that orchestrates the closing will also charge what are called settlement or escrow fees for handling the final paperwork and distributing funds to the appropriate parties.

As an impartial facilitator, the closing agent will make sure you get your money from the sale, that the buyer’s purchase goes down in the books, and whoever else is owed money gets paid. (This may include the real estate agents and any repair contractors involved in the sale.)

The settlement fees are generally divided between the buyer and seller depending on what the purpose of the specific settlement fee is and what is customary in the market where the property is located, but who pays these fees can be a matter for negotiation in many instances.

Title fees (0.5%-1%):

Title fees go toward covering insurance policies that offer protection to both the lender and buyer if a costly title issue crops up with a home after it’s purchased. A title search prior to closing is meant to surface problems, but instances of forgeries or filing errors do rarely crop up and create problems for an owner down the road. Title fees are typically negotiable in a real estate transaction, though most commonly the seller covers the new owner’s title policy, while the buyer covers their lender’s policy. These policies together usually cost around 0.5% and 1% of the purchase price, according to the American Land Title Association.

Property taxes (varies):

During closing, you and the buyer will also settle up on property taxes. The seller will pay for any taxes owed through their final day of ownership. And likewise, the buyer will be responsible for paying any taxes accrued starting from the day they take possession. Some municipalities pay taxes in arrears — i.e., when the bill comes, you’re actually paying for the previous six or 12 months of taxes owed.

It often goes something like this: Let’s say you close May 15, and the tax bill for January through the end of May is due June 1st. In that case, the seller would need to pay out their taxes from January through May 15 at closing. The buyer would cover May 16 through June 1, as well as the property taxes associated with the home moving forward.

Home warranty ($900-$1,000 for yearlong coverage):

A home warranty is designed to cover you when the refrigerator, HVAC, oven/range, dishwasher, water heater, or other major home system or appliance breaks down. A seller may offer a home warranty as an incentive to buyers at an average cost of $957 for a year’s worth of coverage.

A warranty can serve as a compromise if the buyer is concerned about the lifespan of an older system in the home, and the seller doesn’t want to replace it because it’s still functioning. Alternatively, a buyer may elect to purchase their own home warranty policy regardless of what a seller offers. This is one of those costs that could really go either away depending on market conditions and who has more leverage.

Double-check that you’re paying for the right fees

Don’t stress too much about who pays what when selling a home. Negotiations over this or that fee may arise, and if that happens, lean on your real estate agent to determine the best play. At the end of the sale, be sure to review your settlement statement for a line-by-line breakdown of your charges and final take-home pay. If anything looks off, flag it to your agent or the settlement company. Hopefully you’re walking away with a tidy sum to either put toward your next home or boost your savings!

Header Image Source: (Rumay Strauss / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.