How Long Does Closing Take on a House From Start to Finish?

- Published on

- 14 min read

-

Jedda Fernandez Associate EditorClose

Jedda Fernandez Associate Editor

Jedda Fernandez Associate EditorClose

Jedda Fernandez Associate EditorJedda Fernandez is an associate editor for HomeLight's Resource Centers with more than five years of editorial experience in the real estate industry.

You’ve accepted an offer on your house and both you and the buyer have signed the purchase contract. How long does closing take from here?

Next steps include the home inspection, appraisal, and final paperwork. But the time required to process and underwrite the loan will be in large part what dictates the length of your closing.

Selling your house soon? Connect with a top agent near you to get an expert opinion on how much your house will sell for, what to fix before listing, and the latest local housing market trends.![]()

Step one: Talk to an expert!

How long does it take to close on a house?

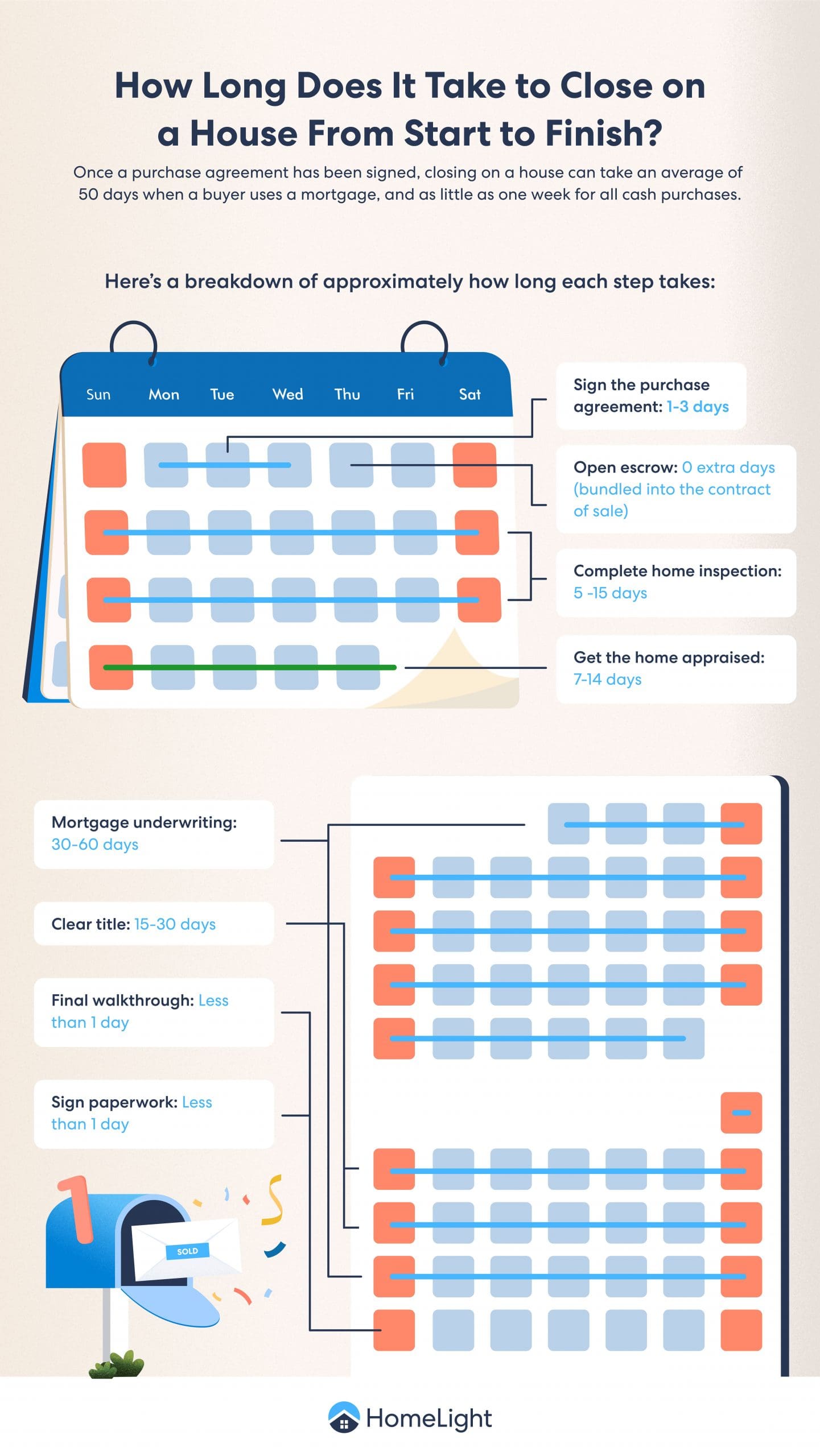

Once the purchase agreement has been signed, closing on a house can take an average of 43 days when a buyer is using a mortgage. For example, if you list your home on Jan. 1 and accept an offer on Jan. 24, you can expect to close on the sale of your home somewhere between the end of February to mid-March.

For all cash purchases, closing can take as little as 1 week.

The buyer will sign the brunt of the paperwork, especially if they are securing a mortgage. The seller’s portion of closing day usually takes one to two hours, according to Sherry Wiggs, a top real estate agent in Westchester County, New York. And in some scenarios, the seller won’t be required to attend in-person if they pre-sign the deed and other documents.

However, a holdup could push out your projected closing date. Let’s take a look at how long each step of closing takes, so you have a better idea of what to expect and what you can do to help prevent delays.

Does cash speed up closing?

You need extra cash now, you’re relocating for a job, or a family member had a change in health — some scenarios such as these require sellers to move more nimbly than a 43-day closing timeline allows. If you are concerned about the process taking too long, consider the alternative of requesting a cash offer for your home.

A cash sale can usually be turned over in a week to two weeks, as it allows you to skip the mortgage process and the appraisal, which are typically the two most time-consuming steps in the process.

HomeLight’s Simple Sale platform provides cash offers for homes in almost any condition across the country. To get started, complete a brief questionnaire about your property and your selling goals, and we’ll provide an all-cash offer for your home within 24 hours with the ability to close in as little as 7 days.

Get a no-obligation all-cash offer through HomeLight’s Simple Sale. Cash offers can reduce the time it takes to close from months to weeks (or even days) and eliminate the risk of a sale falling through due to your buyer’s financing. You can skip repairs and sell without paying commission or additional fees. You’ll also see an estimate of what a top agent might get for your home.![]()

Get to Closing Day Faster With a Cash Offer

How long each closing step takes

There’s a lot that has to happen in that 43-day window of time between offer and closing. Stephen Donaldson, a real estate attorney and founder of The Donaldson Law Firm in New York, breaks down approximately how long each step takes along the way.

Signing the purchase agreement: 1-3 days

Once the parties reach an accepted offer, Donaldson says that signing a purchase agreement or contract of sale can usually be accomplished within 1-3 days, assuming no one’s on vacation or otherwise unavailable.

However, if the sale involves contingencies for repairs, post-closing possession, or anything the parties negotiated specific to the sale, that can add a day or two if the parties or their attorneys get particular about the language addressing those contingencies.

In addition to price, the purchase and sale agreement details other points of negotiation, such as who gets to keep the fridge, the buyer’s inspection period, how much the buyer will put down in earnest money — and your closing date. Each step from here on out will be scheduled based on that date, the final deadline on your home sale (which can be renegotiated in the event of delays or surprises).

Open escrow: 0 extra days (bundled into contract of sale)

Donaldson says that in New York, it’s customary for the seller’s attorney to hold the earnest money deposit in an escrow account with the attorney escrowee’s obligations and rights spelled out in a lengthy paragraph in the contract of sale. “This usually does not add any time to the closing process, as it’s pretty standard,” he notes.

Home inspection and negotiation: 5-15 days

The buyer typically has 5-15 business days to complete the inspection after they sign the contract. Once it’s on the schedule, the inspection itself should take only a few hours to perform, and the written report is usually ready to review the day after the inspection. (Generally, only buyers will receive the full inspection results).

Donaldson notes that repairs are usually not required to be completed until at or near closing.

“Ideally, inspections are completed before the closing process begins so the seller is aware of any obligations to make repairs prior to closing,” he says. “Usually, a seller will provide a buyer with receipts to show that any agreed-upon repairs were affected, preferably by licensed, insured, and experienced professionals.”

Get the home appraised: 7-14 days

After you accept an offer and the home has been inspected, it’s time for the house to be appraised. An appraiser’s onsite visit of the home will take around one to three hours. Due to high appraisal demand, it may be up to two weeks before you receive the appraisal report, which will detail the appraiser’s analysis of recent comparable sales and opinion of value for the property.

If the appraisal comes in under contract value, the buyer can bring extra funds to close the gap, you can reduce the price of the home, or you can meet somewhere in the middle. Otherwise, if the buyer added a home appraisal contingency to the contract, they can walk away from the deal with their earnest money if you’re unable to come to an agreement.

Mortgage underwriting: 30-60 days

The amount of time underwriting requires is usually between three and four weeks, but it can be lender-specific, Donaldson says.

“Large, risk-averse lenders such as Chase Bank and Bank of America will require significantly more time before they issue a final ‘clear to close,’” he explained. Big banks typically have a lot more internal red tape to deal with before they’re able to fund a loan and write a check.

On the other hand, smaller local lenders often have shorter closing times because they tend to be nimbler and more adept at navigating the quirks of their local market.

“Underwriting is going to take into account many factors, including the buyer’s credit score, buyer’s income, the appraisal, and many other factors,” says Eli Goodman, the owner of a house-buying company in Illinois.

“It’s important to work with a high-quality company that can get everything done fast and on time,” Goodman adds. “We have had many closings that have dragged on for months because the mortgage company was not organized. It’s also imperative that the buyer provides everything as requested.”

Clear title: 15-30 days

Donaldson estimates a two- to four-week wait to receive a title report or abstract of title after the contract of sale is fully signed, depending on the location.

For instance, the parties may receive a title report two weeks after entering into the contract if the property is in the Bronx.

However, if the property is in Westchester (one county immediately north), a title report may not be produced until four weeks after the contract is signed, as the local building departments are much slower in Westchester compared to New York City. Further, “clearing” the title could take weeks, if not months, depending on whether title claims are discovered.

“Typically, when we are clearing title, we will need all the parties on the title to have signed the purchase agreement, mortgage payoff, and any other payoff, such as liens or HOA, that may have been put on the property over the years,” says Goodman.

“Sometimes if there was a death, inheritance, or a lienholder that is not responding, clearing the title can take a long time, but it’s usually done well before you are ready to close.”

Final walkthrough: Less than 1 day

The final walkthrough, which should occur shortly before closing, should only take 30 minutes or so.

“This is where the buyer makes sure nothing has been damaged since they last saw the house, that the owner has cleaned out all their possessions, and that everything the seller agreed would come with the house is there,” says Goodman.

Sign paperwork: Less than 1 day

For an all-cash deal, Donaldson says the closing itself can be finished in 30 minutes. He recently closed a small commercial office space in Nassau County in just 25 minutes, where the buyer client paid all cash.

If the purchase is being financed with a loan, he estimates that the closing will take around 60-90 minutes because of the small mountain of paperwork the buyer will need to sign. However, a seller can usually skip the closing by either pre-signing the documents in advance or giving their attorney a power of attorney to sign on their behalf.

Common causes of closing delays

With any home purchase, there is always the potential for roadblocks to delay or derail the path to closing. According to the National Association of Realtors®, 14% of closings get delayed but eventually go to settlement — only 5% of contracts die before the deal closes.

Below are some of the most common holdups:

Buyer financing

Andrina Valdes, CEO of Alta Home Lending, estimates that a little over a fifth of closings are delayed because buyers experience holdups in getting their loan approved. As a key precautionary measure, the seller can request a preapproval letter prior to accepting a buyer’s offer.

A preapproval usually indicates that a lender has performed a preliminary credit check, reviewed the buyer’s debt to income (DTI) ratio, and looked at their finances to determine how expensive of a home they can afford.

“Beyond that, financing approval is almost entirely beyond a seller’s control, because the buyer has no obligation to provide anything to the seller other than a mortgage commitment letter by a certain date after the contract of sale is signed,” Donaldson says.

A preapproval helps to qualify a buyer, but it still isn’t a guarantee to lend. If a buyer makes a large purchase before closing, such as a car, that could shift their DTI outside of the limits set by the lender.

While less common, Donaldson says that 30-60 days can easily be added to the closing process if there was a material change to the buyer’s credit score from the time they received a pre-approval to when they submit their loan application.

Title issues (~11% of delays)

The discovery of a title issue can create a delay. This may include conflicts over property surveys, heirs laying claim to the property, or renovations made to the property without first obtaining a permit from the local building department.

To avoid title issues jeopardizing the deal, the seller can get a preliminary title report to determine any existing issues, such as tax debts or unpaid contractors (known in some states as “mechanic’s liens.”)

Another potential issue is if the seller made renovations without a permit. In that case, Donaldson says they should either clear up the issue proactively before going to market, or explain to a buyer that there is no certificate of occupancy or compliance for whatever work was done and that the house is being sold as-is.

Appraisal

As a condition of offering a mortgage, lenders will require that an independent appraisal is performed. If the house doesn’t appraise for at least the negotiated purchase price, it could put the deal in jeopardy or cause delays.

To help prevent this setback, Donaldson says the seller could invest in an independent appraisal prior to listing.

Another recommendation is to use a tool such as HomeLight’s Home Value Estimator to get an instant idea of what a property is worth on the open market. An online home value estimate won’t replace the appraisal, and could fail to account for details such as recent upgrades. However, it is a good starting point and helpful reference when selling a home.

Inspection issues

Although inspections can sometimes result in a list of issues that need to be addressed, Donaldson says they rarely cause delays to the closing process, because they are usually performed before the parties reach an accepted offer.

“However, a seller can get ahead of any possible issues by investing in an inspection before putting the property up for sale and providing their Realtor with a copy of the report, so they can then offer it to potential buyers,” he suggests. This could save time during closing, but the seller is required to disclose everything in the pre-inspection report (at least in most states), and pay for the pre-inspection with their own money.

Valdes adds that it can also be helpful for the seller to work with the inspector to find out what they need to perform a smooth inspection. This might mean clearing out attics and crawl spaces or being prepared to make any necessary repairs.

Final walkthrough surprises (small sliver)

In a vast majority of cases, Donaldson says there aren’t any unwelcome walkthrough surprises as long as the seller has maintained that the property is in good working order before closing.

“And even if something does happen, the easiest way to deal with it is to patch things up at the closing by way of extending a credit to the buyer for anything that isn’t working that should’ve been,” he adds.

Valdes offers this bit of advice to sellers to prevent unwelcome walkthrough surprises: “Leave your home empty and clean, review your contract to make sure all contingencies are met, and lean on your Realtor for closing day guidance.”

In closing…

Every real estate transaction is different — but if your buyer is using a mortgage, there will be a waiting period between signing the purchase contract and receiving your sale proceeds. This period averages around 43 days in today’s market.

The length of that wait can vary based on the buyer’s loan type, the volume of loans and refinances a lender is managing at that time, as well as issues that can occur with the inspection, appraisal, and title search.

If you’re selling to a buyer who is working with a lender, the 43-day average is likely a safe expectation. But if you’ve received an all-cash offer, you could close in as little as 7 days.

As a seller, the best ways to minimize the wait is to make sure there are no issues with the title, require that the buyer gets preapproved before entering into a contract, and consider getting a preliminary inspection to identify any issues that may need to be addressed before the sale.

Oftentimes, the shortest path to closing is to request a cash offer and cut out the loan underwriting process from the start. A service like HomeLight’s Simple Sale can provide you with an all-cash offer within 24 hours, without the need to prep, stage, or show your home.

Header Image Source: (fizkes/ Shutterstock)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.