Is a 50-Year Mortgage Loan a Good Idea?

- Published on

- 8 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

As housing affordability continues to strain buyers across the country, there’s growing discussion around a 50-year mortgage loan. The idea has surfaced as a possible way to lower monthly payments by stretching the loan term well beyond the standard 30 years. But is a 50-year mortgage a good idea?

To help answer this question, HomeLight surveyed hundreds of top real estate agents nationwide and spoke directly with experienced professionals in the field, including Ahkima Bigbee, a Georgia-based agent with nearly two decades of experience. Their insights paint a clear picture of why many housing experts remain cautious about the idea.

Save thousands when buying a home

HomeLight-recommended real estate agents are top-tier negotiators who understand the market data that helps you save as much as possible when buying your dream home.

Is a 50-year mortgage loan a good idea?

For most buyers, top real estate agents say a 50-year mortgage loan is not a good idea. While a longer loan term may lower your monthly payment on paper, agents overwhelmingly warn that it comes with major long-term tradeoffs, including dramatically higher interest costs, slower equity growth, and greater financial risk if your plans change.

In HomeLight’s Top Agent Insights survey, many agents described 50-year mortgages as creating the illusion of affordability rather than solving it. Lower payments may help you qualify for a loan, but they don’t reduce the price of the home, and over five decades, they can significantly increase the total amount you pay.

Bigbee puts it bluntly: “I do not believe in a fifty-year mortgage, I don’t agree with it.”

She explains that while the promise of a lower payment may sound appealing, the math tells a different story. Bigbee provides this example comparison:

- With a 30-year loan, if you purchase a house with a $500,000 mortgage at an interest rate of about 6%, you might pay roughly $580,000 in interest.

- With a 50-year loan, lenders would likely charge a slightly higher interest rate because of the longer term (perhaps 6.5%). With the additional 20 years of borrowing costs, your total interest paid can jump to around $1,190,000.

“Yes, your payment might drop by maybe $200 a month; that would be one of the potential benefits, but the total interest will double,” says Bigbee. “Is it really worth it, especially if you’re a first-time homebuyer in your forties or fifties, paying for your house into retirement, paying your house into your nineties?”

Even if you decide to sell your house in the first five or 10 years, the math will still work against you as far as gaining equity toward your next home.

Test the math on a 50-year mortgage calculator

We’ve placed Bigbee’s $500,000 example mortgage into a 50-year mortgage loan calculator below. The calculator also provides rough estimates for annual property tax and home insurance.

Try adjusting the cost fields to see what a 50-year mortgage loan might look like for your home purchase. If your down payment is less than 20%, the calculator will add private mortgage insurance (PMI) to your monthly payment. You can also modify the interest rate estimates to see how rate changes might affect affordability.

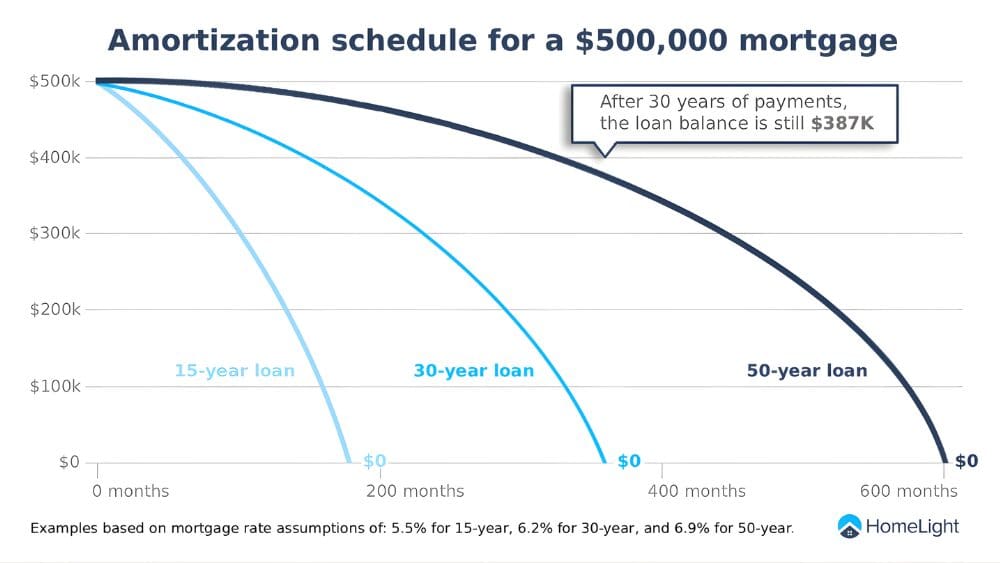

Because mortgage payments are front-loaded with interest, extending the term means you spend far longer paying interest before making meaningful progress on the principal. That’s why many agents worry about how slowly equity builds under a 50-year loan.

The amortization curve chart below illustrates how a 50-year mortgage loan for $500,000 might compare to traditional 15- and 30-year loans.

Bigbee sees this as one of the biggest risks for buyers. “Your payment in the beginning is going to go mostly to interest. Now that you’re in a longer mortgage, it’s more interest you’re paying before you start building equity. You may even be at risk of being underwater.”

For buyers who don’t stay in their homes long (the average homeowner moves after roughly a decade), this slow equity growth can limit flexibility if you need to sell, refinance, or relocate.

How much more interest might you pay?

As our calculator above illustrates, extending a home loan from 30 to 50 years doesn’t just stretch your payments and delay equity growth; it dramatically increases how much you pay in mortgage interest over the life of the loan.

In the table below, assuming a 20% down payment to avoid PMI, you can quickly compare the total interest paid on different loan amounts for a 30-year mortgage at 6% vs. a 50-year mortgage at 6.5% (longer terms have higher rates).

| Mortgage loan amount | 30-year payment | 50-year payment (diff.) | 30-year total interest paid | 50-year total interest paid |

| $200,000 | $1,579 | $1,507 (-$72) | $231,676 | $476,460 |

| $300,000 | $2,272 | $2,164 (-$108) | $347,515 | $714,690 |

| $400,000 | $2,965 | $2,822 (-$143) | $463,353 | $952,921 |

| $500,000 | $3,659 | $3,479 (-$180) | $579,191 | $1,191,151 |

| $600,000 | $4,352 | $4,137 (-$215) | $695,029 | $1,429,381 |

| $700,000 | $5,045 | $4,794 (-$251) | $810,867 | $1,667,611 |

| $800,000 | $5,738 | $5,452 (-$286) | $926,706 | $1,905,841 |

| $900,000 | $6,432 | $6,109 (-$323) | $1,042,544 | $2,144,071 |

| $1,000,000 | $7,125 | $6,767 (-$358) | $1,158,382 | $2,382,301 |

The monthly payment reduction varies by loan size, but the savings are often modest relative to the added long-term cost.

Top agents say a 50-year loan is not a solution

According to HomeLight’s nationwide survey, 43% of agents say that only a small minority of buyers would consider using a 50-year mortgage if it became available. Another 23% predict that “very few or no buyers” would use it. The only consumers who might: first-time buyers struggling with affordability.

Agents did acknowledge that in very limited, short-term scenarios, a longer loan term could align with certain goals — for example, if you plan to sell or refinance within a few years. But as a broad affordability solution, most agents say a 50-year mortgage loan creates more problems than it solves.

Top agents summed up their concerns about 50-year mortgage loans in a few consistent themes:

“Short-term, it may help people get in the door. Long-term, it can create a generation of owners who are house-poor and stuck. Affordability needs structural solutions, not just longer debt.” — Ashley Oakes-Lazosky, Las Vegas, Nevada

“It creates a false sense of affordability. You’re stretching the debt across two generations and barely touching the principal for years. Homeowners deserve clarity, not a payment plan that outlives the roof.” — Carmen Salerno, Melrose Park, Illinois

“A 50-year mortgage stretches debt across generations, traps homeowners in long-term interest costs, and inflates home prices even further. It solves affordability on paper, not in reality.” — Kim Haber, Sarasota, Florida (Darren Dowling Team)

“The monthly payment savings of a 50-year mortgage doesn’t offset the exorbitant amount of interest paid over that loan term.” — Tanya Kerr, Austin, Texas

“With such a long loan term, buyers stay in the ‘interest-heavy’ phase for decades, making it harder to move, refinance, or build wealth through homeownership.” — Lauren Webb, Fort Worth, Texas

“While lower monthly payments may look attractive, homeowners would build equity at a much slower pace, leaving them more exposed if property values flatten or decline.” — Ann Wilson, Arlington, Virginia

“Extended loan terms can artificially prop up home prices by enabling buyers to overextend rather than solving the root issue.” — Kent Rodahaver, St. Petersburg, Florida

“The 50-year mortgage doesn’t fix affordability; it camouflages it.” — Cynthia McKenna, Stony Brook, New York

“Real estate is meant to be a stepping stone, but a 50-year mortgage can easily become an anchor.” — Kip Barnard, San Jose, California

Why the idea sounds appealing to buyers

Despite the drawbacks, it’s easy to see why a 50-year mortgage loan catches your attention, especially if affordability feels just out of reach.

A lower monthly payment can:

- Help you qualify for a higher-priced home

- Reduce immediate cash-flow pressure

- Feel like a workaround when rates and prices remain elevated

Some buyers may also assume they’ll refinance later, treating the longer loan as a temporary bridge. But agents caution against relying on future rate drops or market shifts that may never materialize.

As Bigbee advises her clients: “I always tell people to look at the payment right now. Can you afford it right now? We don’t know when interest rates will drop — or if they will.”

She encourages buyers to compare multiple scenarios side by side — 15-year, 30-year, and longer terms — and to think honestly about how long they plan to stay in the home: “Are you going to be in this house for five years? Ten years? Twenty years? Will you have equity in the next five years? All of those things play a role in whether this really makes sense for you.”

Get a real-world perspective on affordability

From Bigbee’s experience, extending loan terms doesn’t address the root causes of affordability challenges. “The supply type, prices on housing, and building costs are part of the issue. A fifty-year mortgage doesn’t fix those.”

For buyers considering any non-traditional loan term, her advice is simple: “Look at your goals. Get as much information as possible. Educate yourself before you jump into any mortgage loan. Work with a professional real estate agent and lender who are very knowledgeable on these things.”

Bigbee reiterates, “Personally, I’m not for it. It has a lot of drawbacks, and it’s not going to solve affordability issues. Buyers who need lower payments should look into other ways of being able to afford a house.”

Find a trusted agent with HomeLight’s free Agent Match platform. A top agent can provide expert guidance about local downpayment assistance and finance programs, and affordable housing opportunities that fit your budget. We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs. You can also try our home affordability calculator.

So, is a 50-year mortgage loan a good idea?

For most buyers, the answer from top real estate agents is no. While a 50-year mortgage loan may lower your monthly payment, it often does so at the cost of:

- Significantly higher lifetime interest

- Slower equity growth

- Reduced flexibility if your plans change

In limited, short-term situations — especially if you plan to sell or refinance within a few years — a longer loan term might align with your goals. But as a widespread solution to housing affordability, agents overwhelmingly say it falls short.

“If you want to get into a house, save up more so you can put down a down payment and not need a fifty-year mortgage,” Bigbee advises. “The whole goal is to own that house one day, or at least sell it to build equity or leave the house for your next generation.”

If you’re struggling to afford a home, experts recommend focusing instead on:

- Buying within a sustainable price range

- Exploring seller concessions or rate buydowns

- Increasing your down payment when possible

- Working closely with an experienced agent and lender

A 50-year mortgage loan may sound appealing, but when you look beyond the monthly payment, most agents agree it’s rarely the right answer. Longer loan terms may improve cash flow, but not true affordability.

To learn more, visit HomeLight’s Homebuyer Resource Center, where you can search for answers to other homebuying questions.

Header Image Source: (levkro / Deposit Photos)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.