How to Find Comps for My House: An Illustrated Guide

- Published on

- 15 min read

-

Dena Landon, Contributing AuthorClose

Dena Landon Contributing Author

Dena Landon, Contributing AuthorClose

Dena Landon Contributing AuthorDena Landon is a writer with over 10 years of experience and has had bylines appear in The Washington Post, Salon, Good Housekeeping and more. A homeowner and real estate investor herself, Dena's bought and sold four homes, worked in property management for other investors, and has written over 200 articles on real estate.

-

Richard Haddad, Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

Once upon a time, the only place you could find property data was the MLS (multiple listing service), a series of private databases real estate professionals use to share listing information among one another and broker deals. Before contacting a real estate agent, you had no idea how much your house was worth or how much you could make in a home sale. If you were making an offer on a house, was the asking price fair?

Today, all you need is a Wi-Fi connection to dig up specs like square footage, bedroom count, and selling prices on nearly any house across the country.

This “how to find comps for my house” crash course will teach you how to find comparable sales and calculate a rough estimate of your home’s value. Then you can decide if you’d like to do it alone or enlist a pro’s help.

Price Your Home Right With a Top Agent

Our agent matching platform takes into account an agent’s specialties and certifications, years of experience, and concentration of transactions in your neighborhood — helping you set an accurate price for your home sale.

What are comps in real estate?

In real estate, the term “comps” — short for comparables — refers to recently sold homes that are similar to your house. To be a comp, the house must have similar characteristics, such as size, school district, and amenities.

Comps give you a range for its “market value,” which you can then add or subtract from based on your home’s unique characteristics and features. For example, if you have a two-car garage and your neighbor has a one-car garage, your home might sell for more.

Once you’ve assembled your pool of similar properties, look at their sold prices. Active listings are not an accurate comparison point for your home’s value until they sell.

Why? Even if the home down the street is listed for $500,000, it hasn’t sold yet — so how do you know if it’s too high or too low?

Comps sold within the last 60 days are preferable because their sale price reflects current market conditions. However, recent sales aren’t always available, so you may have to pull comps from as long as six to 12 months ago.

What factors are used when finding comps?

Agents — and appraisers — use these factors to identify comps. Agents use the same factors as a home appraiser because they know that if your house fails to appraise appropriately, a buyer may not get a mortgage on it, and the sale could fall through.

- Location: Neighborhood, access to major highways or public transportation, how close it is to the school or a public park, all of these influence a home’s price.

- Location features: A home that backs up on a lake might be more valuable than a similar home in the same neighborhood that doesn’t have water access.

- Date of sale: A home sale from three years ago doesn’t reflect market conditions today.

- Home and lot size: A comparable home will have relatively close square footage and the same size yard.

- Number of bedrooms and bathrooms: If your home has three bedrooms and one bath, it’s not comparable to a six-bedroom with three bathrooms.

- Age of the home: A home built a hundred years ago won’t need the same maintenance and upkeep as a home built five years ago. However, some buyers may prefer an older home with character and unique features. An experienced agent would select a home of similar vintage to price your property.

- Condition of the home: Have you been meticulous about having the furnace serviced every year, the air filters changed, and cleaning the gutters? A well-maintained home will price higher than one where the buyer might need to invest in catching up on maintenance.

- Special features or upgrades: A newly remodeled kitchen, a room addition, or a deck could all make one home worth more than another house just down the block.

What is an appraiser going to see when he appraises this house? The listing price needs to stay within earshot of the appraisal because the methodology will be the same federal government guidelines that the buyer’s appraiser will use down the line.

Collier Swecker Real Estate AgentCloseCollier Swecker Real Estate Agent at Mega Agent Real Estate Team at RE/MAX Advantage5.0Currently accepting new clients

Collier Swecker Real Estate AgentCloseCollier Swecker Real Estate Agent at Mega Agent Real Estate Team at RE/MAX Advantage5.0Currently accepting new clients

- Years of Experience 20

- Transactions 832

- Average Price Point $220k

- Single Family Homes 737

How do home sellers use comps?

Comps are a benchmark that will come into play at multiple points in a home sale.

Sellers use comps to determine the market value of their home and correctly price their property for sale. If you’re working with an agent, they’ll typically bring a comparative market analysis (CMA) to your first meeting. This analysis pulls in all similar sold properties, as well as draws on the agent’s market expertise, to come up with a suggested list price.

The right price is crucial in order to attract interested buyers. A buyer’s agent will look at the exact same comparable sales and tell their client if they think your property is accurately priced — and if you’ve gone too high, they might not even bring the buyer to look at your property. They’ll also use these prices when writing up an offer.

But you’re not done with comparables after you’ve accepted an offer. Once it’s under contract, a home appraiser will assess your home’s value on behalf of the mortgage lender financing the home — using a comps analysis of their own. If the appraiser says that your home’s market value is less than the offer price, the buyers can negotiate the price down or back out of the sale.

“What is an appraiser going to see when he appraises this house?” asks top agent Collier Swecker, an investment properties specialist endorsed by Dave Ramsey and Glenn Beck. “The listing price needs to stay within earshot of the appraisal because the methodology will be the same federal government guidelines that the buyer’s appraiser will use down the line.”

How do homebuyers use comps?

When shopping for a home, buyers use comps to help them figure out if a property is reasonably priced and to calculate their offer. While some buyers may be willing to pay over asking price and bring cash to the table to close a deal, not everyone has this option. In some markets, comps can also be used as a negotiating tool if the buyer is armed with proof you might have over-priced your home.

Buyers want to find a place to live, but they don’t want to overpay. And they’re also concerned about a mortgage lender’s appraisal.

“Different loan types have different guidelines and criteria that the appraiser must meet,” says Swecker. “For example, the appraiser may have to find three comps for a VA loan, but for an FHA loan six comps may be needed within a half-mile.”

Get an Estimate on Your Home's Value

It only takes two minutes to answer a few questions. You’ll receive a detailed analysis of your home straight to your inbox immediately. Simply tell us a little bit about your property (the address, type of property, its condition, and the year it was built) and how soon you’re looking to sell.

This won’t replace a comparative market analysis from a top real estate agent, but it can be a helpful starting point.

Who else uses real estate comps?

A number of real estate, financial, and legal professionals use comps.

- Agents use comps to set a listing price.

- Appraisers research comps when they’re appraising a home for a mortgage lender.

- Lenders need comps when they’re underwriting a home for a mortgage loan.

- Divorce attorneys could use comps to help a couple split their assets and divide up equity.

- Estate planners might use comps to help a client plan for retirement.

- Attorneys could use comps to determine the value of a client’s home when drawing up a will.

How to find comps in your area

There are a number of ways to find comps depending on how much time you want to invest. Here’s a list of places to start your search for comps:

1. Use a trusted real estate website

Real estate websites pull non-proprietary information from the MLS into searchable databases that let you filter listings by specifics that match your own home. Most importantly, the majority of these sites allow you to filter out all but sold properties.

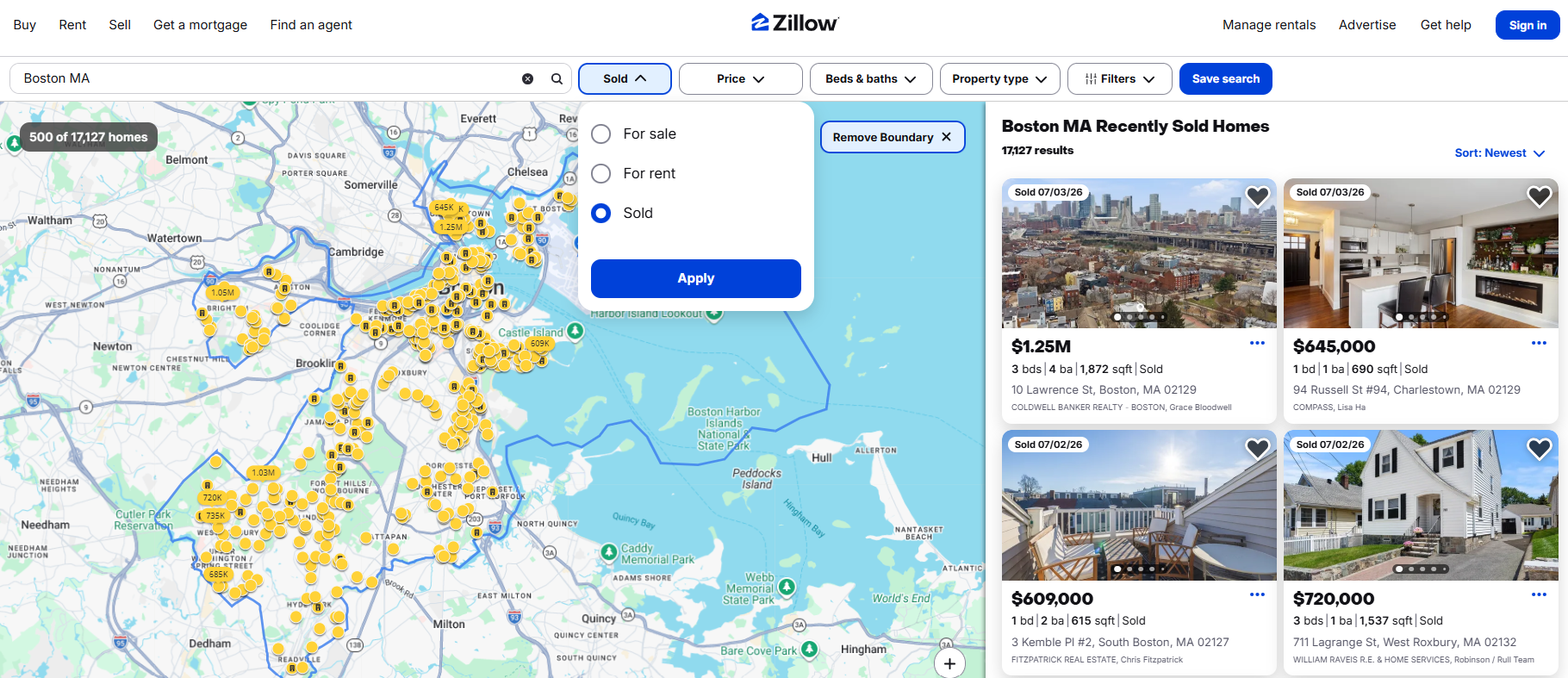

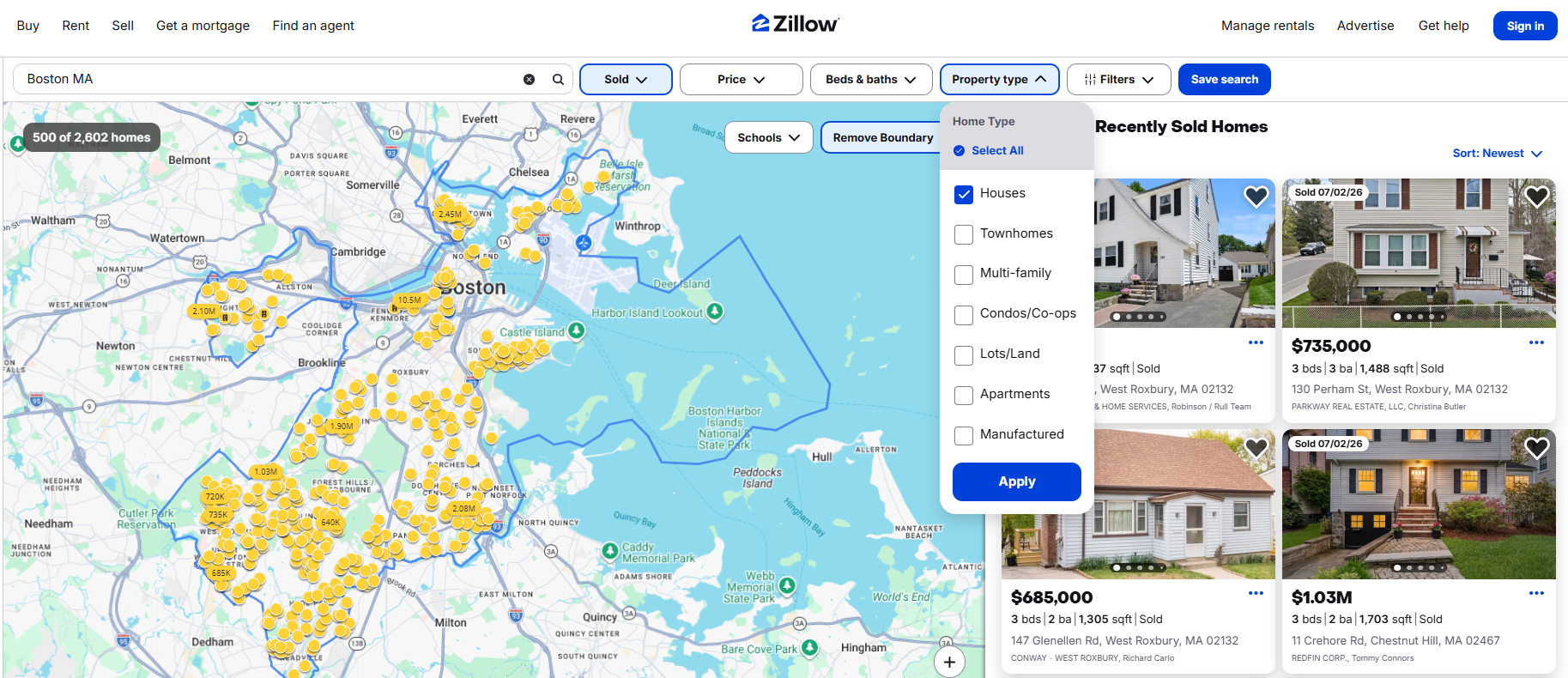

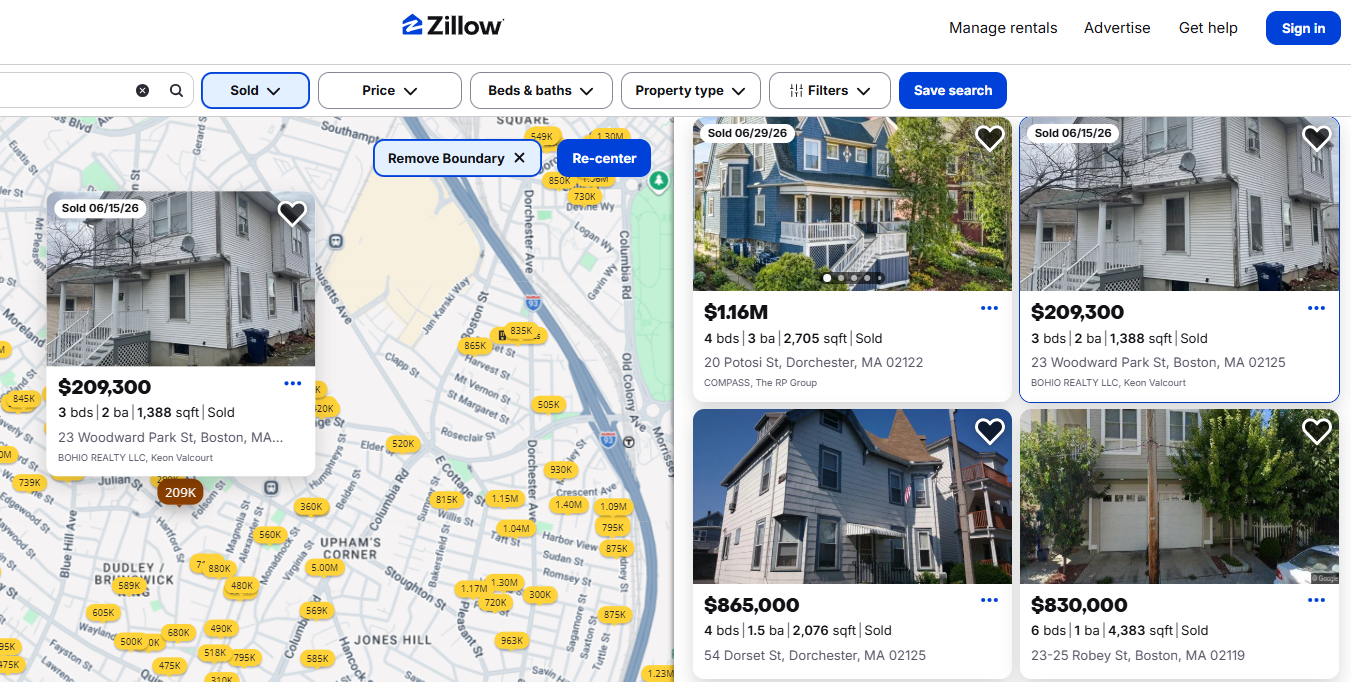

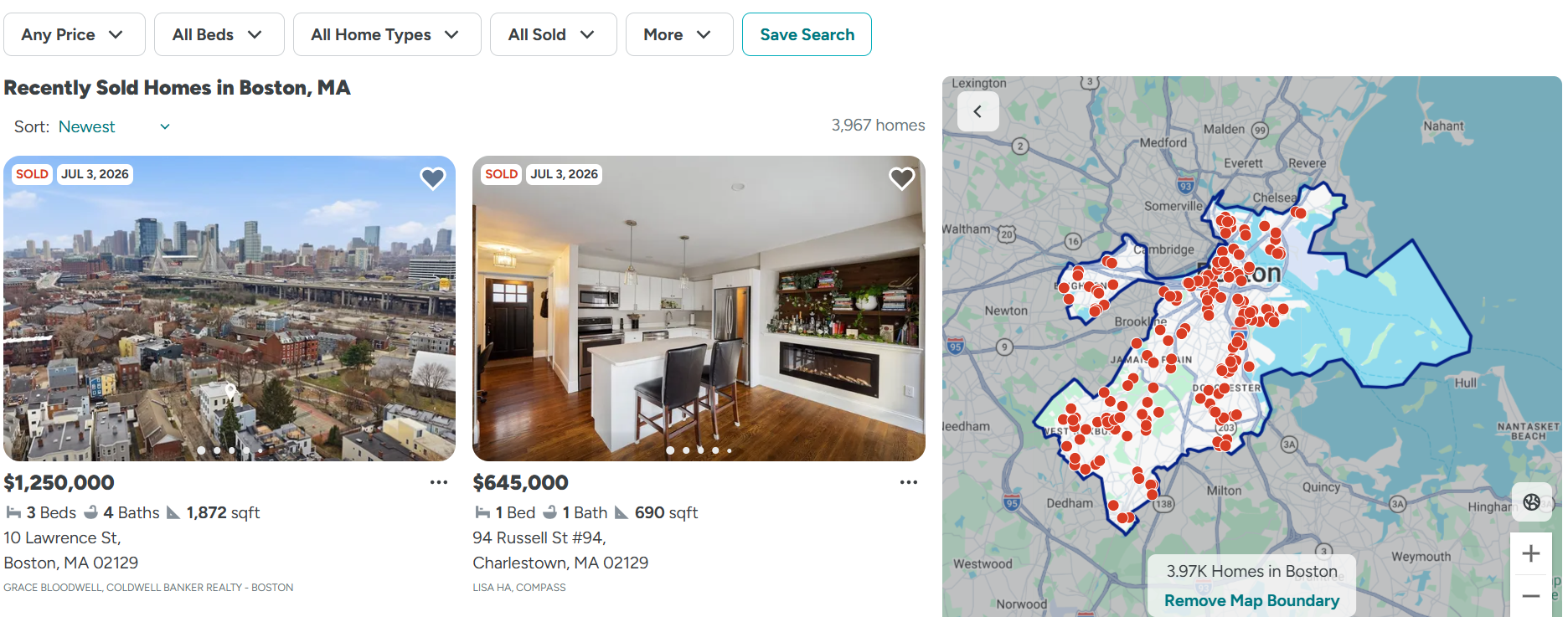

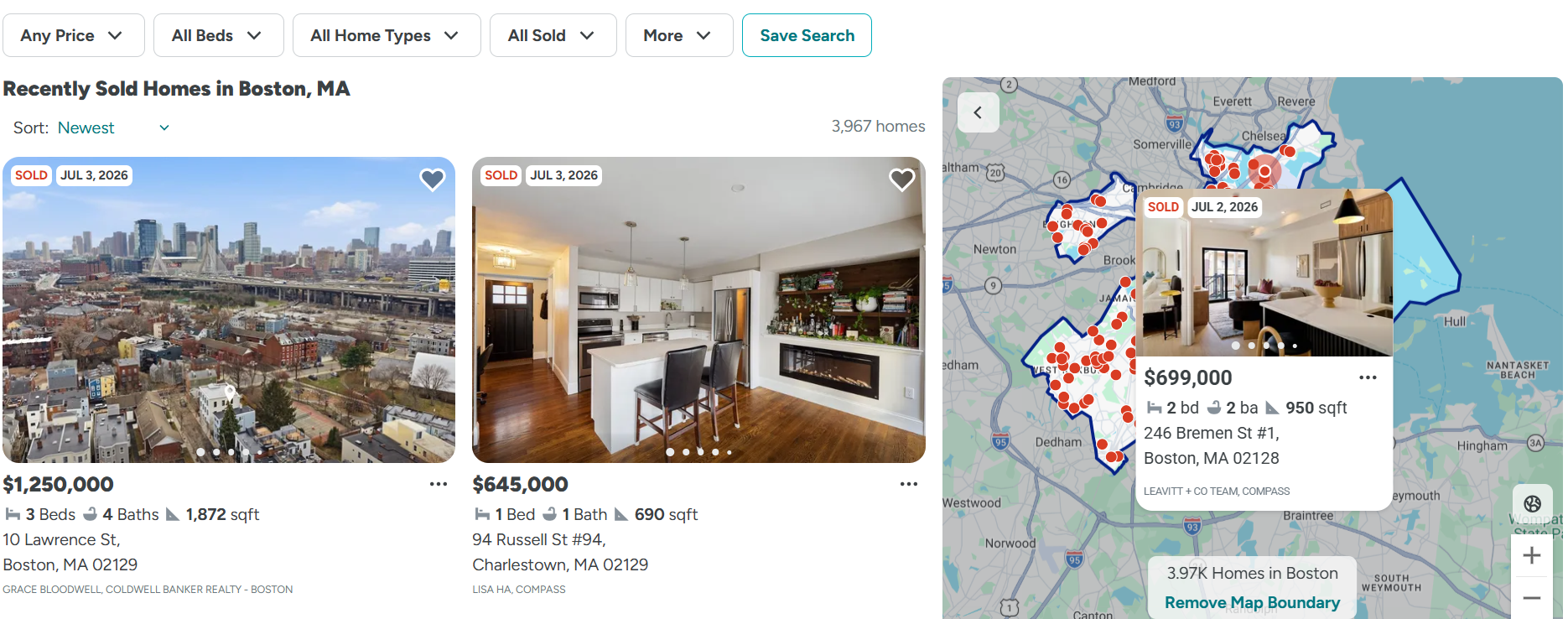

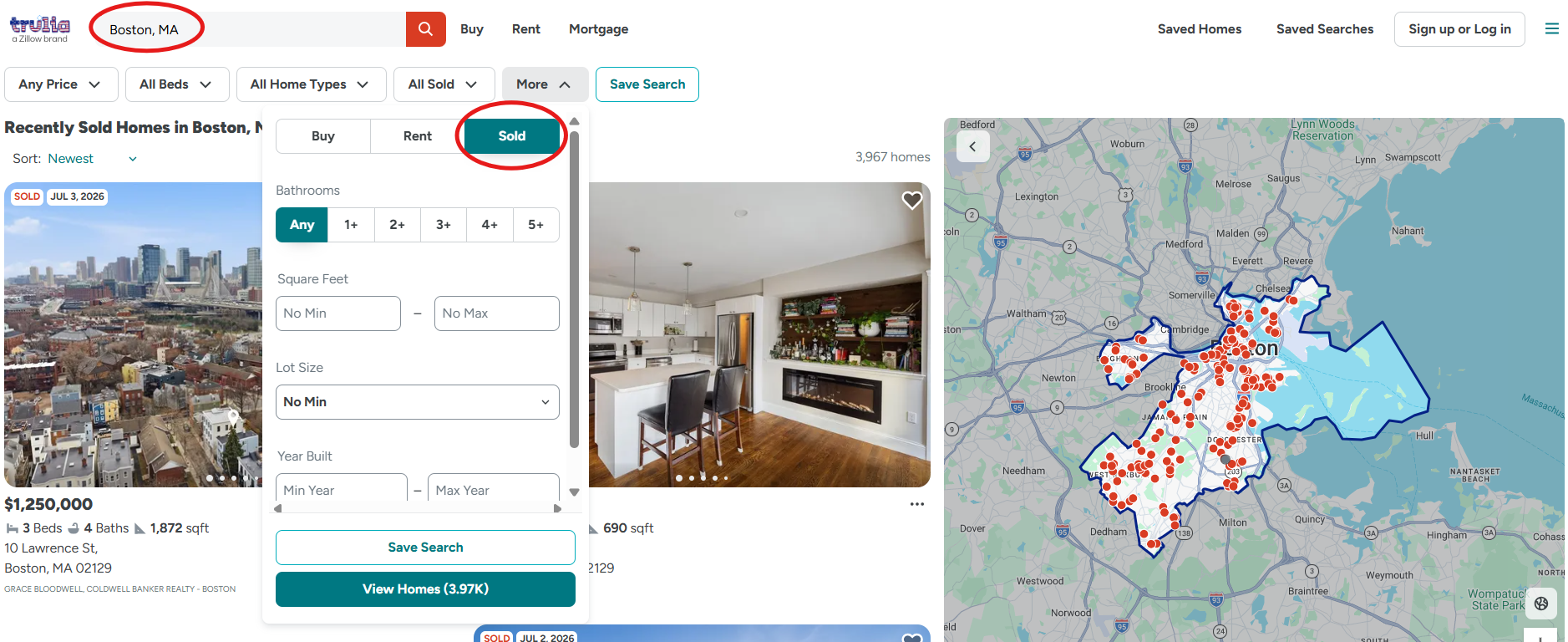

Zillow

Start your search for comps on Zillow by typing your city and state into the search bar. Or, you can type in a zip code. If you live in a large city, like Boston, you can also search by neighborhood.

At the top of the screen, under “For sale,” filter for “Sold” so you’re only seeing the yellow dots. On the upper-right, be certain you are sorting by “Newest” listings so you are looking at the most recently sold properties.

Now click on “Property type” at the top and select the style of property, such as “Houses,” “Townhomes,” or “Condos.”

Zoom in on your area, then your neighborhood, and find your house to use as a reference point. Look for comps in the closest proximity to your own location that match your home’s characteristics. Click on a property to see details, such as the address, number of bedrooms and bathrooms, square footage, and the date it sold.

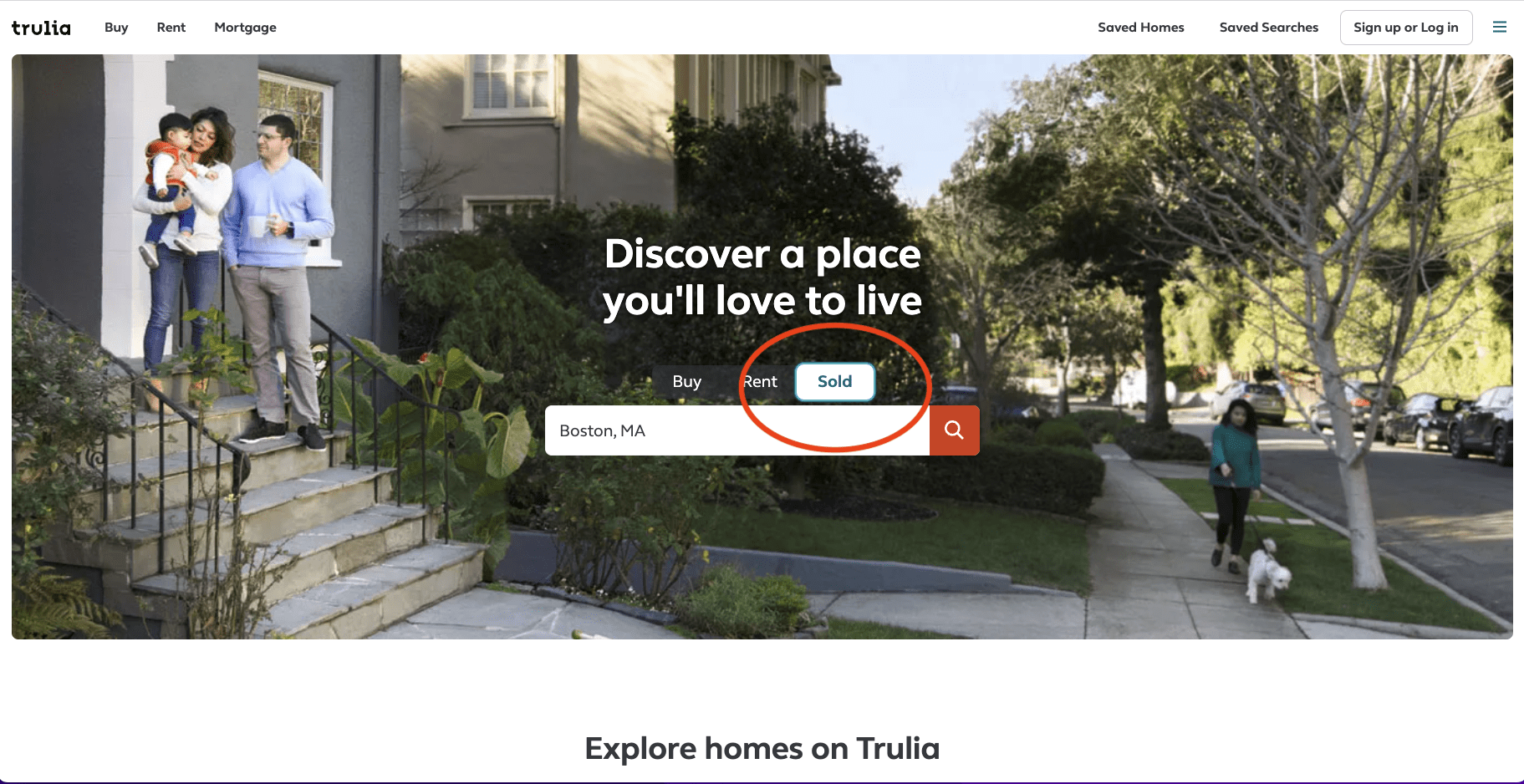

Trulia

Trulia provides several ways to access sold homes data through its public records database.

On the homepage of Trulia.com, click the “Sold” button and enter the name of your city.

Like Zillow, you’ll see the newest recently sold home listings with each property plotted on an interactive map. You can zoom in on your neighborhood and see sold properties near your home.

Hover your mouse over a property for a quick pop-up glance showing the home’s size, address, and selling price. Click on a property listing or map marker to see additional details.

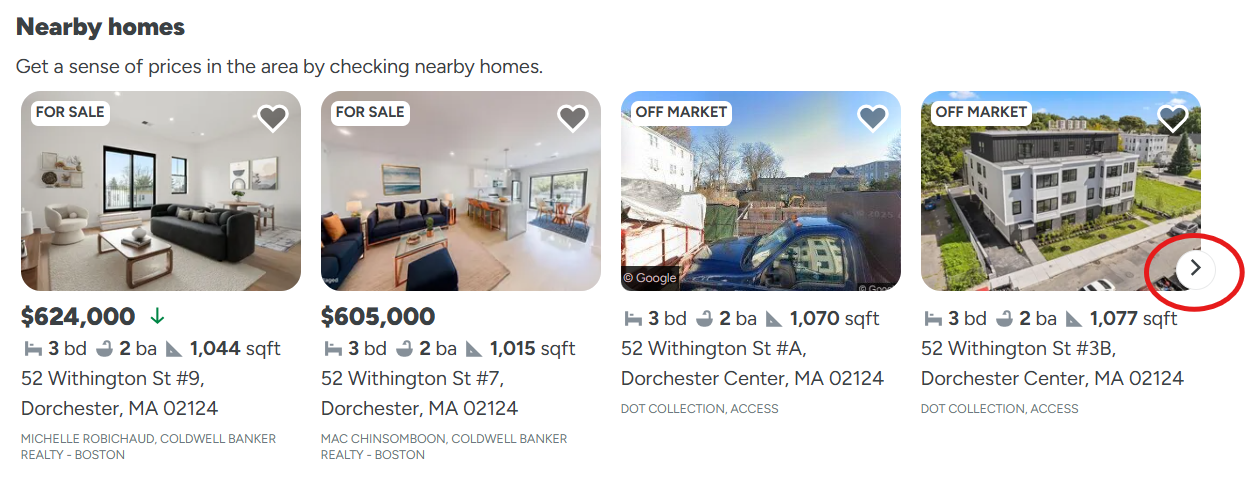

For some listings, if you scroll down on the detail page you will see an image carousel showing off-market homes sold near the property you selected. Click through the carousel to view more sold homes.

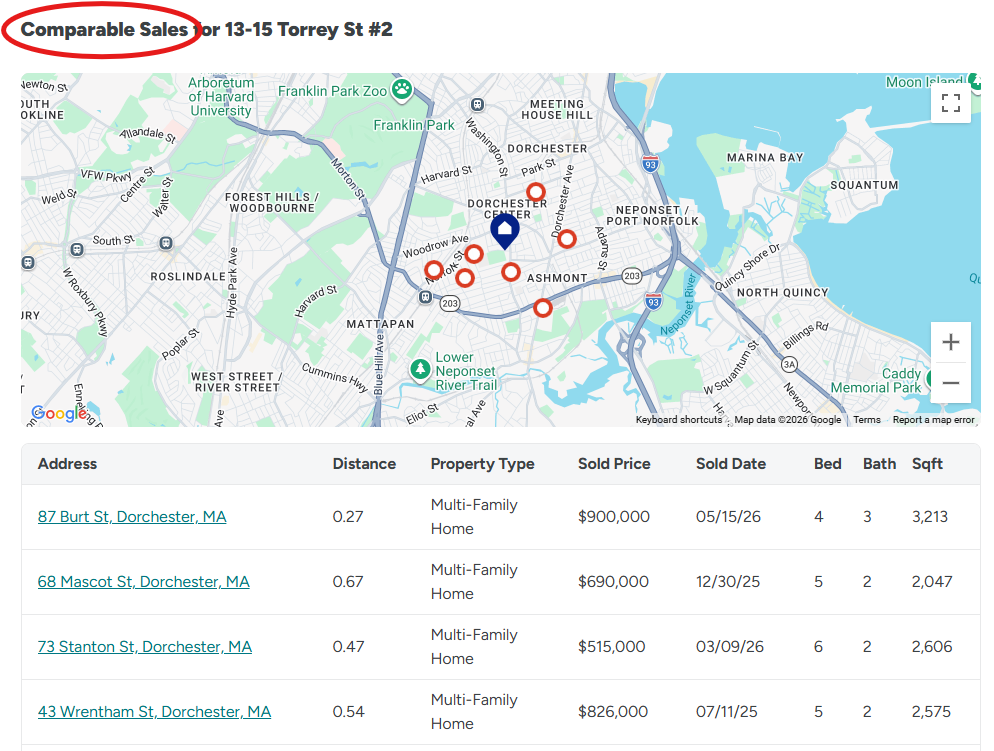

Another way to see recently sold homes on the Trulia city map page is to enter your address in the search bar on the upper left. On your home’s detail page, scroll down to the section called “Comparable Sales” to see a list of comps.

Pro tip 1: Trulia’s profile of your home’s address offers up this list of comparable sales already curated for you based on:

- Distance to your home

- Property Type

- Sold Price

- Sold Date

- Beds

- Baths

- Square footage

Not all of Trulia listings have the “Comparable Sales” feature. For some properties, you might instead see the “Off-Market Homes” image carousel with nearby homes and their sold dates and prices.

Pro tip 2: For a fast jump, select your state or major city from this Trulia site map page, then enter your city name or ZIP code in the search bar. Now, simply select “Sold” under the more menu.

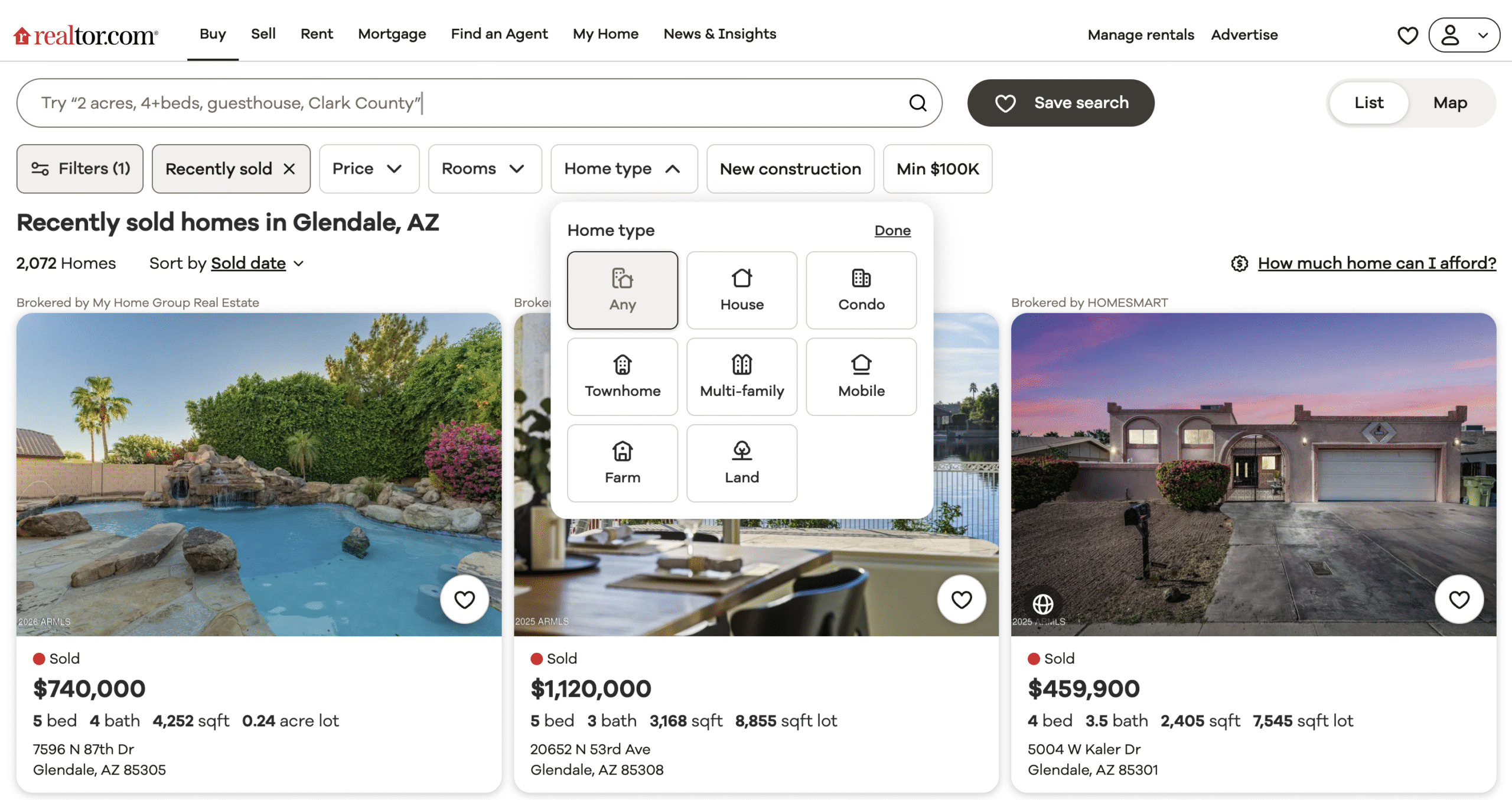

Realtor

Realtor provides a search portal of “Just Sold” properties. Enter your city and state and start browsing from there.

On the top of the results page, you can filter by property type (house/condo/farm ranch/land), the number of bedrooms, bathrooms, and other criteria. By default, the homes are sorted by sold date.

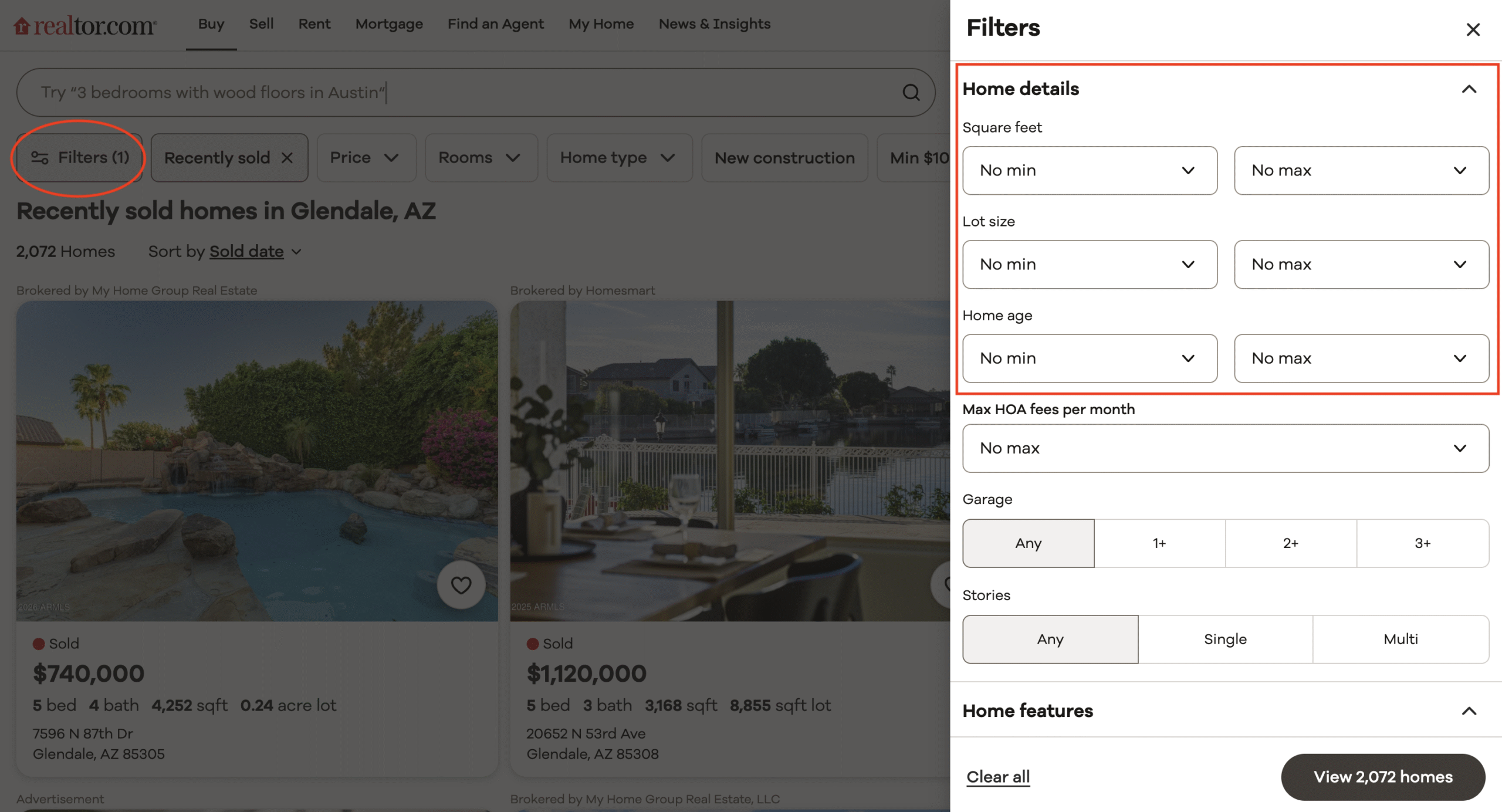

Pro tip: Assembling comps through Realtor requires a bit more legwork, as you can’t zoom in on a map or by ZIP code/neighborhood to narrow down the “Just Sold” listing pool in your city. As you can see in the screenshot below, a search for “Just Solds” in Glendale, AZ, serves up 2,072 results alone. But under the “Filters” option, you can also filter by:

- Keywords (pool, waterfront, basement, gated)

- HOA fees

- Home size

- Lot size

- Home age

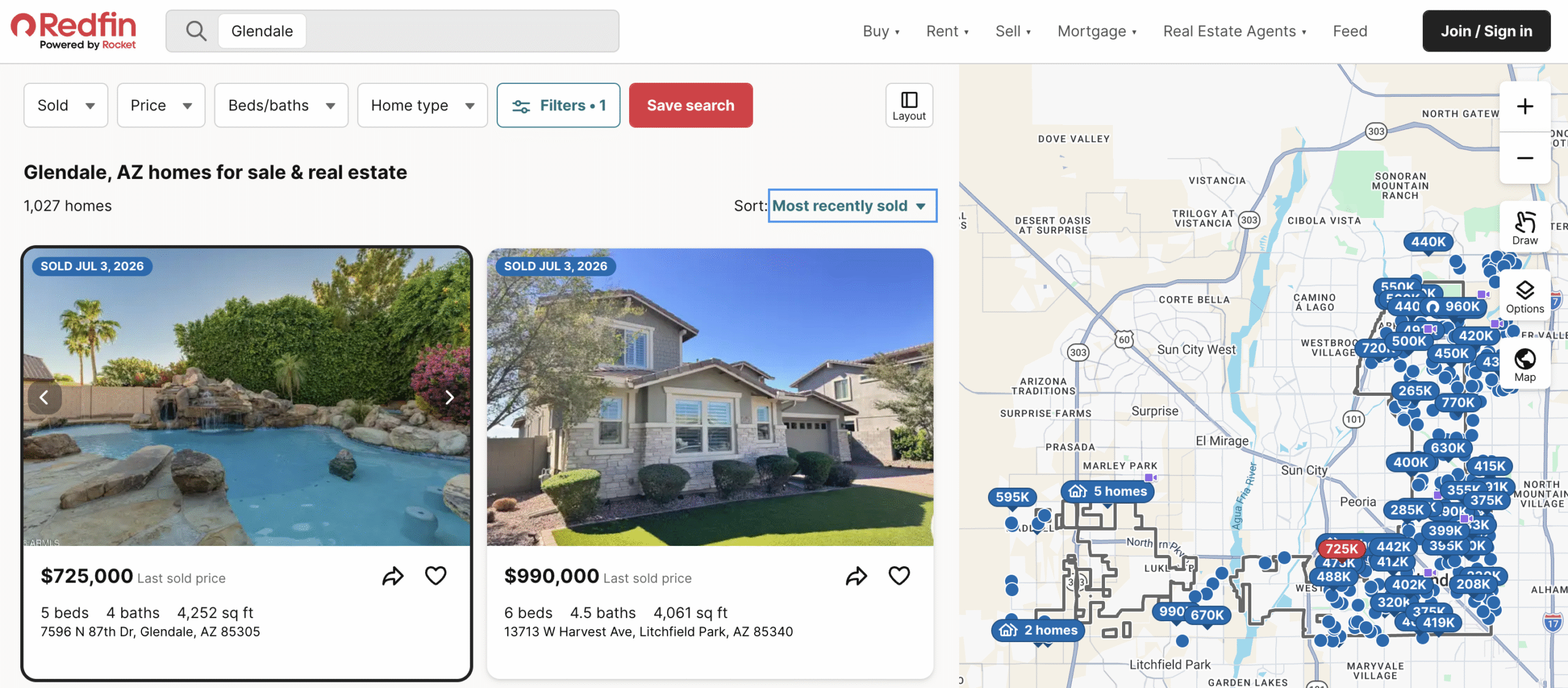

Redfin

Search your city on Redfin’s website. Then, choose “Sold” under the “For Sale” dropdown. Use the blue listings to find comps for your house.

Pro tip: Redfin lets you narrow down your “Sold” listings by time frame — so you can search for listings that sold last week, all the way up to listings that sold in the last three years. For the purposes of finding comps, remember that the more recent, the better.

What are some drawbacks of online comps tools?

As great as these online tools are, they do have drawbacks.

Inaccurate “sold” prices: Agents largely use these sites as marketing tools. They provide the photos, descriptions, and details on their available listings directly to target buyers who are house shopping online. But once a home sells, updating that data isn’t a priority.

Swecker advises, “There’s a large percentage of Realtors® that do not give their sold data to the online sites because it has to be manually entered.” So even when a listing is marked as “sold” on these sites, the dollar amount given may still be the list price, not the sold price.

The sold price may also fail to reflect any seller concessions, or money the sellers had to pay to repair the garage, replace the carpet, or cover the buyer’s fees at closing.

Outdated, incomplete listing information: Online real estate listing sites pull their property data from the MLS, and they may refresh hourly, daily, or weekly. Only the MLS will have the most up-to-date data, and not every listing portal will have complete location coverage. For-sale-by-owner (FSBO) listings could have listed a non-compliant bedroom or included a basement in square footage when that’s not allowed in your state.

Listings missing from the MLS: There may be some nearby home sales that won’t show up on these online sites because they were never entered into the MLS in the first place.

Known as pocket listings, these are private listings that agents sell for their clients within their own private network of buyers. Even if they aren’t in the MLS, the sold prices on these pocket listings can impact your home’s current market value.

Recent property upgrades not mentioned online: Many homeowners perform upgrades and small remodeling projects before listing their homes for sale. If a homeowner added an extra bathroom or remodeled the kitchen just before selling their house for $500,000, those property details might not have been updated on the online listing sites. Not realizing this, you may mistakenly group a property into your comps pool without realizing it’s actually off in bathroom count, or without adjusting your list price for the upgraded kitchen.

The bottom line? Be careful when using online data to figure out your home’s worth.

2. Search public property and sales records

Public records are another good source, though you can’t filter them like a website. It can also take a while for recent sales to update, though the sale price will be accurate. There are a number of sources that can provide information about home sales prices.

County property sale

Some counties provide online search tools. Typically, you’ll need to know the street name or parcel number to begin your research. Or, you can go to the local courthouse or county records office.

In county sales records, you will be looking at the negotiated final price, not the listing price. County records typically don’t indicate if any seller concessions were involved, such as credits for repairs or closing costs.

City websites

Searching for the name of the city or town along with the word “assessor” online should lead you to the assessor’s website. A city’s assessor evaluates properties for tax purposes. Generally, they have accurate data about the number of beds and baths because it’s used to calculate the taxes due.

3. Use a free automated valuation model tool

Another way to check comps is to use a reputable online home value estimator, also called an automated valuation model (AVM) tool. These tools pull in market sales data, analyze and compare it to your property, and return a suggested list price.

Try HomeLight’s Home Value Estimator. After answering seven simple questions about your house, it calculates a value in just two minutes.

AVMs are not as accurate as other valuation methods, such as a comparative market analysis (CMA) or a home appraisal, but they are often free and can provide an initial baseline you can use as a ballpark estimate.

4. Ask a real estate agent for a comparative market analysis

A comparative market analysis (CMA) is a report that many licensed real estate agents produce for free in hopes of attracting new home seller clients. The agent can access the multiple listing services (MLS) to compile a report that analyzes six to 12 local comparable sales and then establish a list price. A CMA will also look at current market trends, inventory levels, price per square foot, and days on market (DOM).

Agents also bring the human touch. An algorithm can’t capture an agent’s local knowledge. They’ll know about a new planned development that could raise prices, if a grocery store is being built close by, or other non-monetary factors that could raise or lower a price.

A CMA isn’t an appraisal, but it can often accurately determine a home’s current estimated value.

Request a CMA From a Top Agent Near You

Try our free Agent Match tool now to request a comparative market analysis on your home. We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs.

How can I be certain comps are accurate?

Look for the following signs that the sales you’ve selected are accurate comps.

Compare only sold homes: We’ve said it before, but it bears repeating. Only sold listings count.

Pay attention to the listing description: Look for keywords and phrases that you think describe your home — close to a bus stop, remodeled bathroom, new roof.

Study the photos carefully: How big is that backyard? Does the half bath have carpet on the floor? Look closely and zoom in on the photos to take notes on similarities and differences.

Visit the property and check out the area: Sometimes nothing compares to driving through the area and realizing that there’s a pizza parlor next door, or that a home is close to a community pool.

Be certain it’s the same type of home: A ranch isn’t comparable to a Victorian, and will attract different buyers.

Adjust for seasonality or market conditions: If you’re listing in the spring or early summer, just as the market heats up, you can probably command a higher price than if you’re selling mid-winter.

Partner with a top agent familiar with the area: Real estate agents have direct access to the most accurate comps data in the MLS. They also have years of experience studying shifts in local market trends and are your best source for determining a home’s value.

Accurate house comps help empower home sellers

Once you have accurate comps, you have a more realistic idea of what you could get for your home. There are a few instances — a highly unusual property for the area, a home in a rural area with a farm attached — where you might need the services of a professional appraiser. But for most homeowners, you’ll be able to find what you need online.

Comps help determine the selling price for your home, or its value for a home equity line of credit or refinance. While a seller can pull some data themselves, there’s no substitute for an experienced agent who knows the local market and recognizes the pricing pitfalls that home sellers need to avoid.

If it’s time for you to talk to an agent, get connected with a top agent in your market through the HomeLight Agent Match platform. They’ll know the ins and outs of your market, and the best listing price for your house.

Header Image Source: (Patrick Chin/ Death to the Stock Photo)

FAQs about finding comps

“Bracketing comps” is a technique used by real estate appraisers to ensure an accurate valuation of your home. It means that the appraiser will select comparable properties that are both superior (better) and inferior (not as good) to your home in terms of features, condition, or size. This helps to establish a realistic value range for your property by placing it between homes of higher and lower value, rather than only comparing it to homes that are exactly like yours or only better/worse.

Yes, while active listings don’t reflect actual market value until they sell, expired and withdrawn listings can offer valuable insights. These are homes that were on the market but didn’t sell, or were taken off the market by the seller. Analyzing them can help you understand prices at which homes failed to sell in your area, providing a crucial lesson on potential overpricing or market resistance. This data can help you avoid making similar pricing mistakes with your own property.

It’s important to physically inspect comps and their immediate surroundings, as online photos and data alone may not capture every detail. Driving or walking by a comparable house allows you to assess the exterior condition, noting things like cracks in the driveway or missing shingles. You should also “scan the area” to understand nuances of the location, such as whether a home is on a quiet cul-de-sac or a busy road, or its proximity to public transportation lines. These on-the-ground observations can significantly influence a home’s appeal and value.

Yes, seasonality can significantly affect home prices and selling speed, and it’s wise to consider it when analyzing comps. In many real estate markets, homes tend to sell more quickly in the spring and early summer. Conversely, homes might take longer to sell in the fall and winter, and sellers might sometimes lower their prices in these slower seasons to attract buyers. Understanding these typical seasonal fluctuations can help you make more accurate pricing adjustments for your home, especially if your comparable sales data spans different times of the year.

Real estate investors analyze comps with a keen eye on potential profit and return on investment. They go beyond just the basic features, meticulously examining the location, size, condition, and amenities of a property relative to recent sales to determine its fair market value and to negotiate a suitable purchase price. Investors also heavily factor in the cost of any necessary repairs or renovations, and how those improvements will impact the “after repair value” (ARV) of the home, which is crucial for their profitability. They often look for properties where they can add value through renovations to maximize their return.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.