Income, Equity, and Credit: The Basics of Bridge Loan Requirements

- Published on

- 7 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

It’s a conundrum countless families need to solve: how to buy a new home when you need to sell your current house to fund the purchase. For many homeowners, the solution is a bridge loan, a short-term financial assist that fills the gap in this real estate riddle.

In this guide, we’ll walk through the basics of bridge loan requirements and common hurdles you may face. We’ll also share a modern Buy Before You Sell program alternative that helps you buy your next home first without the complexity and stress of piecing together a traditional funding puzzle.

Yes, You Can Buy Before You Sell. Why Move Twice?

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

What is a bridge loan?

A bridge loan is a short-term financing option that’s designed to “bridge” the gap between buying your next home and selling your current one. Instead of stressing about timing, you can access your equity early to make an offer with confidence.

Here’s how it typically works:

- You take out a loan secured by the equity in your current home.

- The loan covers part of the down payment on your next home.

- Once your current home sells, you pay off the bridge loan — usually within six to 12 months.

This tide-over arrangement can be a lifesaver, especially in competitive markets, but it comes with higher costs and tougher qualifications than a standard mortgage.

Bridge loan requirements: What lenders look for

Credit score

Most lenders want to see a solid credit history, with minimum scores often ranging from 650 to 700. A stronger score can help you qualify for better rates.

Equity in your current home

You’ll usually need at least 20% equity in your current home to qualify. Lenders want assurance that your property has enough value to secure the loan.

Debt-to-income (DTI) ratio

Your DTI — the percentage of your monthly income that goes toward debts — typically needs to fall below 43% to 50%. If your debt load is too heavy, lenders may hesitate to approve you.

Income and employment stability

Lenders want proof that you can handle payments during the short loan term. Expect to provide pay stubs, tax returns, or other documentation of steady income.

Loan-to-value (LTV) ratio

Your LTV compares the loan balance to your home’s value. For bridge loans, lenders often cap this ratio at 70%–80%, meaning you can’t borrow against the entire value of your home.

If you’re curious how much your home might be worth, try HomeLight’s Home Value Estimator. You’ll see a real-world ballpark value estimate in less than two minutes.

Bridge loan requirements example

Here is an example of a typical bridge loan scenario:

- Current home value: $400,000

- Remaining mortgage balance: $250,000

- Available equity: $150,000 (meets the 20%+ equity requirement)

- Credit score: 680 (falls in the 650–700 minimum range most lenders want)

- Debt-to-income ratio: 40% (within the 43%–50% range)

- Bridge loan amount: $60,000 to help fund the down payment on a new home

With this setup, you’d be carrying two mortgage payments temporarily, plus the bridge loan. Once your $400,000 home sells, the bridge loan is paid off in full. The more equity you have, the higher your bridge loan amount can be. It’s also important to consider the loan costs.

Bridge loans typically carry interest rates 2%–3% higher than conventional loans, plus closing and origination fees ranging from 1% to 3% of the loan amount.

Common hurdles when applying for a bridge loan

Meeting the bridge loan requirements is the first step. Managing the loan and your home sale isn’t always simple. These are some of the challenges you may face:

- Higher costs: Bridge loans often come with higher interest rates and fees than traditional mortgages, which can quickly add up.

- Short repayment window: Most bridge loans need to be repaid within six to 12 months, so the timing of your home sale matters a lot.

- Two mortgages at once: Until your current home sells, you may be carrying two mortgage payments plus the bridge loan — a financial stretch for many homeowners.

- Risk if your home doesn’t sell: If you are selling in a slow market or your home sits longer than expected, you could be stuck with a loan that’s tough to repay.

Before you commit to a bridge loan, it’s important to explore all your options and have a solid plan in place. It’s wise to consult with a financial advisor or trusted real estate professional.

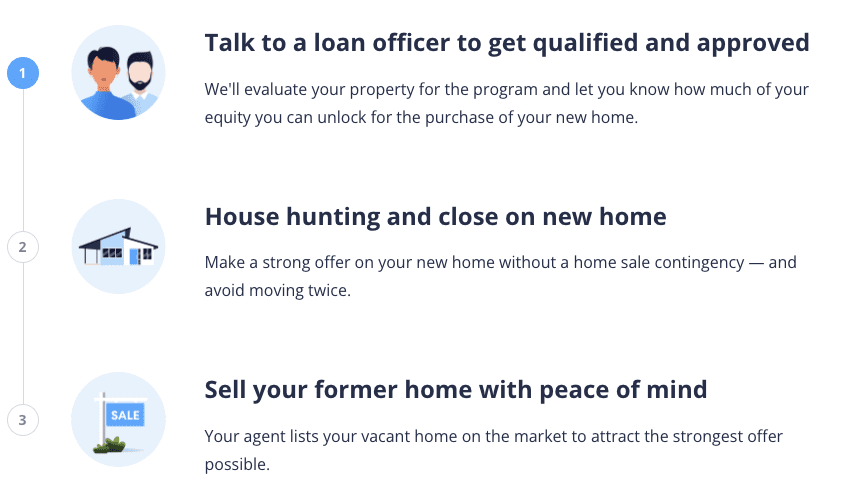

A modern alternative: HomeLight’s Buy Before You Sell program

If the strict requirements or risks of a bridge loan don’t feel like the right fit, HomeLight’s Buy Before You Sell program offers a simpler path. Instead of juggling two mortgages or worrying about high fees, you can unlock your home’s equity to buy your next house first.

Here’s how Buy Before You Sell works:

- HomeLight helps you access the equity in your current home upfront.

- You can make a strong, non-contingent offer on your new home.

- Once you’ve moved in, you can sell your old home on the open market — possibly for a higher price than you’d get selling under pressure.

With Buy Before You Sell, you get the convenience of moving on your own timeline. It’s designed for homeowners who want the best of both worlds: flexibility and financial peace of mind. To get started or see FAQs about program costs and restrictions, visit homelight.com/buy-before-you-sell.

Key takeaways: Look beyond bridge loan requirements

Bridge loans can be a useful tool when you need to buy before you sell, but meeting the requirements can be tough — and the costs add up quickly. If you have strong equity, a solid credit score, and the income to handle two mortgages, a bridge loan may be worth considering.

But for many homeowners, there’s a better solution. With HomeLight’s Buy Before You Sell program, you can move into your next home first, then sell your old one with less stress and more control.

If you are unsure about your next move or you are just looking into your options, consult with a local real estate agent familiar with bridge loans and buy-before-you-sell programs.

HomeLight’s Agent Match platform can connect you with a top-rated agent in your market. Our free tool analyzes over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs.

Editor’s note: This post is for educational purposes, not financial advice. If you need assistance with a bridge loan, HomeLight encourages you to reach out to your own advisor.

Header Image Source: (Rigucci/DepositPhotos)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.