Bridge loan vs. HELOC: Which is right for you?

- Published on

- 12 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

If you’re planning to buy a new home before selling your current one, you may have a lot of your wealth tied up in home equity. The challenge is accessing that equity when you need it most, whether for a down payment, closing costs, or simply to make a stronger offer on your next home.

In this post, we compare a bridge loan vs. HELOC (home equity line of credit) and explain when each option may make sense.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Bridge loan vs. HELOC: What’s the difference?

Although both products allow homeowners to borrow against the equity they’ve built, a bridge loan and a HELOC work in very different ways.

The biggest difference comes down to purpose. A bridge loan is specifically designed to help bridge the financial gap between buying one home and selling another. A HELOC is a revolving line of credit that gives homeowners flexible access to their equity whenever they need it.

Understanding how each works can make it easier to decide which option aligns with your moving plans.

A closer look at a bridge loan

Rather than waiting for your existing home sale to close, a bridge loan gives you temporary financing so you can move forward with your purchase.

According to mortgage loan officer Eric Becerra, co-founder of Empower Home Loans with more than 28 years of lending experience, the money can be used for a down payment on a new home, closing costs, or other expenses that come with buying before selling.

“A bridge loan is a short-term loan that helps you buy the next home before your current home sells. It is basically used to ‘bridge’ that gap when the equity is there, but the home has not sold yet.”

Bridge loans are often used by homeowners who:

- Have significant equity in their current home

- Want to make an offer without a home sale contingency

- Need to move before their current home sells

- Want to avoid moving twice

A closer look at a HELOC

Unlike a bridge loan, a HELOC isn’t designed solely for buying another home.

“A HELOC is a line of credit tied to the equity in your current home,” Becerra explains. “You can use it for things like the down payment, closing costs, repairs, or reserves.”

Instead of receiving one lump sum, you’re approved for a credit limit and can borrow only what you need during the draw period.

Because of that flexibility, many homeowners keep a HELOC open for years, drawing from it only when needed, such as for home improvements, emergency expenses, or large purchases, like a car, boat, or RV.

“The simple way I explain it is this: a bridge loan is tied to buying your next home quickly, while a HELOC is more like a revolving credit line that you can tap into as needed,” Becerra says.

Bridge loan vs. HELOC comparison chart

| Feature | Bridge loan | HELOC |

| Primary purpose | Help you buy a home before selling your current one | Flexible access to your home equity |

| How you receive funds | Typically a lump sum | Draw funds as needed up to your credit limit |

| Repayment | Usually repaid after your current home sells | Borrow and repay during the draw period, followed by a repayment period |

| Loan term | Short-term | Long-term revolving credit line |

| Interest rates | Often higher because of the short-term nature of the loan | Often variable and may increase over time |

| Best for | Buying before selling, avoiding sale contingencies, making stronger offers | Down payments, renovations, reserves, or ongoing access to equity |

| Flexibility | Designed for one specific transaction | Can be used multiple times during the draw period |

| Key consideration | Higher costs and shorter repayment timeline | Variable interest rates and an additional monthly payment |

Note of Interest: According to ICE Mortgage Technology, U.S. homeowners hold nearly $17 trillion in total equity, of which approximately $11 trillion is tappable.

Bridge loan vs. HELOC: Which is right for you?

The best financing option depends less on the loan itself and more on what you’re trying to accomplish with the money.

If your primary goal is to buy a new home before selling your current one, a bridge loan is designed to provide short-term financing so you can move quickly. If you’re looking for more flexible, ready-when-you-need-it access to your equity, a HELOC may be a better fit.

Here are some common situations where each option tends to make the most sense.

A bridge loan may be the better choice if…

A bridge loan is designed for homeowners who need to access their equity quickly while transitioning from one home to the next.

“Bridge loans usually make sense for homeowners who have good equity and need to move before they sell,” Becerra says.

You may want to consider a bridge loan if you:

- You’ve found your next home before selling your current one. A bridge loan can help fund your purchase without waiting for your home sale to close.

- You want to make a stronger offer. Buying without a home sale contingency can make your offer more attractive to sellers, particularly in competitive markets.

- You’d like to move only once. Purchasing your next home before selling can help you avoid moving twice, eliminating storage fees and the need for temporary housing.

- You’re working on a tight timeline. Whether you’re relocating for work or trying to secure a hard-to-find home, a bridge loan can provide short-term financing while your current home is on the market.

“A bridge loan can help when someone wants to make a stronger offer, avoid a home sale contingency, or not have to move twice,” Becerra says. “It is also helpful when the right house comes up, and they do not want to miss the opportunity while waiting for their current home to sell.”

A HELOC may be the better choice if…

A HELOC can be a good option if you want access to your home’s equity but don’t necessarily need financing that’s built around buying another home. Because it functions as a revolving line of credit, a HELOC gives you the flexibility to borrow only what you need and when you need it.

You might consider a HELOC if you:

- Need funds for a down payment. A HELOC can help cover upfront costs while preserving your savings.

- Plan to make repairs before selling. Some homeowners use a HELOC to update or prepare their home before listing it.

- Want additional financial flexibility. Because you borrow only what you need, you may pay interest on less than your full credit limit.

- Have a low interest rate on your current mortgage. A HELOC allows you to tap your equity without refinancing your existing first mortgage.

“A HELOC may be a better fit for homeowners who want access to their equity but are not necessarily trying to sell right away,” Becerra says. “It can also make sense when someone has a low rate on their current first mortgage and does not want to touch it.”

How Much Is Your Home Worth Now?

Home values have rapidly increased in recent years. How much is your current home worth now? Get a ballpark estimate from HomeLight’s free Home Value Estimator.

Bridge loan vs. HELOC: Drawbacks to consider

Both bridge loans and HELOCs can help you unlock equity from your home, but each comes with trade-offs.

Bridge loan drawbacks

“The biggest benefit of a bridge loan is speed; it can give a homeowner the ability to buy first and sell after,” Becerra says. “The downside is cost, and in some cases, the borrower has to qualify while carrying more than one payment.”

- The interest rates and fees you pay are often higher than other financing options

- The loan is intended as short-term financing

- You’ll need to be able to must qualify while carrying payments on more than one property

HELOC drawbacks

“The biggest benefit of a HELOC is flexibility; you can use what you need and only draw from it when needed,” Becerra says. “The downside is that many HELOCs have variable rates, and that new payment still has to be counted when qualifying.”

- With a variable interest rate, your payments may increase over time

- Your new monthly payment is included when lenders evaluate your ability to qualify for another mortgage

- Your home serves as collateral for the line of credit

How to qualify for a bridge loan or HELOC

While bridge loans and HELOCs serve different purposes, lenders evaluate many of the same financial factors when determining whether you qualify.

To qualify, they’ll typically consider your:

- Level of home equity

- Credit score and credit history

- Income and employment

- Debt-to-income (DTI) ratio

- Overall financial profile

The biggest difference is how lenders evaluate the loan’s purpose.

“A bridge loan lender is usually focused on how much equity is in the current home and what the plan is to pay the loan off, which is usually selling that home,” Becerra says.

For a HELOC, lenders still review your equity and financial qualifications, but they’re also determining whether you can comfortably manage an additional monthly payment alongside your existing mortgage and other debts.

Becerra explains that lenders generally look at “the available equity, the borrower’s credit profile, income, and whether they can afford the added payment.”

“The biggest mistake is waiting too long,” Becerra says. “A lot of people start asking about equity options after they have already found the next home or after they have listed their current home. By that point, some options may be harder to use.”

Because lenders often prefer to approve a HELOC before a home is listed or under contract, homeowners who think they may need one should start the conversation early.

Becerra adds, “Another mistake is assuming equity means automatic approval. Equity helps, but the lender still has to look at credit, income, debt, and the full picture.”

To avoid both pitfalls, Becerra recommends planning ahead and talking with a lender long before you begin house hunting. Counseling in advance can give you more financing options and help you move more confidently when the right home becomes available.

Bridge loan, HELOC, or Buy Before You Sell?

If your biggest challenge is the timing of buying and selling, which often requires a home-sale contingency tied to your offer, a Buy Before You Sell program can provide a more streamlined, modern solution.

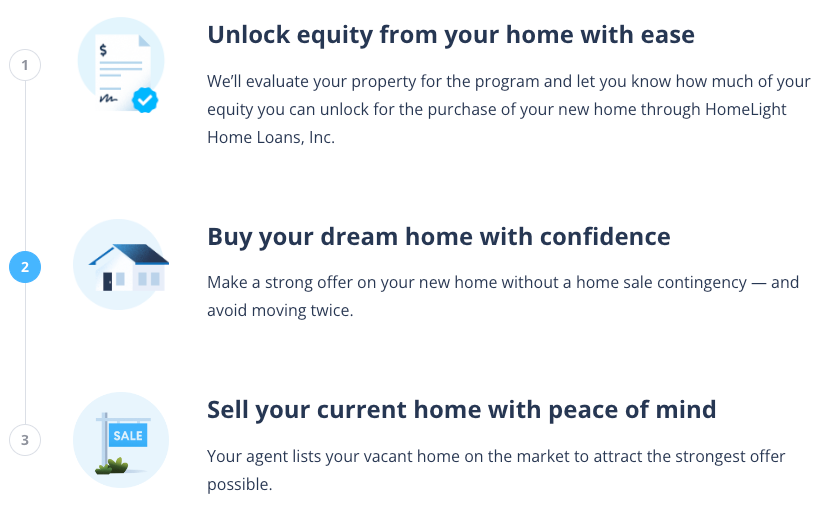

These programs, like HomeLight Buy Before You Sell, are designed to help qualified homeowners unlock their equity so they can purchase their next home before selling their current one.

Depending on the program, you can move into your new home first, prepare your old home for sale after you’ve moved out, and avoid the stress of coordinating two transactions at once.

“For a lot of homeowners, the issue is not that they lack equity. The issue is timing,” Becerra says. “A Buy Before You Sell program can help solve that by giving homeowners a cleaner path to buy the next home first, move once, and sell after.”

But perhaps more importantly, you can often remove the sale contingency from your purchase offer, increasing your chances of winning the home you want.

In a recent HomeLight Lender Insights survey, 41% of loan officers reported an increase in home purchases falling through because of contingency clauses.

How HomeLight Buy Before You Sell works:

If your home qualifies, you can get your equity unlock amount approved in 24 hours or less — no cost or commitment is required. Once approved, you can buy your next home with confidence and then sell your current home with more peace of mind. Learn more at homelight.com/buy-before-you-sell.

Frequently asked questions

In many cases, yes. Bridge loans often have higher interest rates and fees because they’re intended as short-term financing. A HELOC may offer a lower initial interest rate, but many HELOCs have variable rates that can increase over time.

Yes. Some homeowners use funds from a HELOC to cover a down payment, closing costs, or other expenses associated with purchasing their next home. Before doing so, talk with your lender about how the additional debt may affect your mortgage qualification.

The answer depends on the financing option you’ve chosen and your lender’s terms. With a bridge loan, you’ll need a plan for repaying the loan if your home sale takes longer than expected. A HELOC may offer more repayment flexibility, but you’ll still be responsible for making the required monthly payments.

Neither option is necessarily easier to qualify for. Both generally require sufficient home equity, good credit, stable income, and an acceptable debt-to-income ratio. Qualification requirements vary by lender and loan program.

Bridge loans can be structured in different ways. However, our Bridge Loan Snapshot Tool below can help you visualize what your bridge financing might look like.

Use the sliders to adjust the values and see estimated monthly interest payments, available proceeds, and the balloon payment due at loan repayment.

Know your options: Bridge loan vs. HELOC

Bridge loans and HELOCs can both help you tap into your home’s equity, but they’re designed to solve different challenges.

The right choice ultimately depends on your equity, finances, moving timeline, and long-term goals.

Becerra encourages homeowners to focus on the bigger picture before choosing a financing product.

“My advice is not to start with the loan product. Start with the strategy. A bridge loan, HELOC, or Buy Before You Sell program can all work, but it depends on the homeowner’s equity, income, timeline, current mortgage, and comfort level.”

Ultimately, Becerra says the goal isn’t simply to access your equity; it’s to create a financing plan that supports your move while protecting your financial flexibility.

Editor’s note: Loan terms, eligibility requirements, and available products vary by lender, so it’s important to compare your options and consult with an advisor before making a decision.

Header Image Source: (AI-generated)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.