Your Guide to Buying a Home in the Sunshine State of Florida

- Published on

- 17 min read

-

Jody Ellis, Contributing AuthorClose

Jody Ellis Contributing Author

Jody Ellis, Contributing AuthorClose

Jody Ellis Contributing AuthorJody Ellis is a freelance writer with more than 15 years of experience in the writing industry. Her work includes copywriting and content marketing for real estate professionals, stories covering real estate trends and housing markets, and varied articles on decor and design. In addition to buying and selling several homes herself, she's also owned and managed rental properties, and previously worked in mortgage lending.

-

Madeline Sheen, Contributing AuthorClose

Madeline Sheen Contributing Author

Madeline Sheen is a passionate writer and editor with experience in real estate, personal finance, and mortgage content. Along with serving as an associate editor for HomeLight, she’s worked in the mortgage industry since 2019 and holds a BA in Communications from California State University, Monterey Bay.

When you think of Florida, the first thing that comes to mind might be Disneyworld®, Miami, and of course those endless miles of white sandy shoreline. And while those are all great perks, there’s a lot more to the Sunshine State than amusement parks and beaches.

Florida, which averages 237 sunny days a year (hence the Sunshine State moniker), is known for its generally mild climate and an abundance of outdoor activities. Living here means having options between larger, more urban cities, smaller communities with that hometown feel, or coastal towns with the beach at your front door. Florida also tends to be economically friendly, with no state income tax and a homestead exemption to help homeowners reduce their property tax obligations.

With all these benefits, it makes sense that Florida’s population is booming. U.S. Census reports show population growth of more than 14% from 2010 to 2020, pushing it up to the third most populous state in the country.

Ready to make Florida your home? We researched everything you need to know about buying a house in Florida, and spoke with top agent Maria Raymer, who works with 67% more single family homes than the average agent in Jacksonville, Florida, to get expert insight into the steps required for buying a home in Florida.

Looking for An Affordable Home in the Sunshine State?

Working with a knowledgable buyer’s agent is your key to success when buying a home in Florida. Use HomeLight’s agent matching tool to find a top agent in your area in under two minutes.

Steps to buying a home in Florida

Let’s dive into the steps of buying a house in Florida:

1. Assess your readiness

Before you start looking for homes in Florida, you want to determine if you’re ready to purchase one. Consider factors such as how long you plan to be in the area, if you have steady employment, and if you have enough money saved for not just the down payment, but for closing costs, maintenance, property taxes, and more. Homebuyers in Florida pay an average of approximately 2.58% of the home’s purchase price in closing costs when purchasing a home.

During this time, review your credit score and determine if it’s considered excellent, good, fair, or poor. Typically, the higher your credit score, the lower your interest rate will be, which saves you money over the life of the loan. You may want to pay off any collections accounts, dispute errors on your credit report, and pay down your credit card balances before you start shopping for a home.

2. Saving for your down payment

The median home price in Florida is $415,762 as of July, 2022. So, expect to spend somewhere around that number depending on what part of Florida you’re purchasing in, the home’s age and condition, and the size of the property, among other factors.

Different loan programs will require different down payment amounts, but you do not always need to put 20% down when buying a home. A survey completed by the National Association of Realtors found that first-time homebuyers put just 7% down on average in 2021.

Raymer says that for her clients, especially first-time buyers, she suggests an FHA loan, which only requires 3.5% down. “FHA is really one of the best options,” she advises. She adds that Florida also has numerous down payment assistance programs, many of which are tied to state bond money. “The programs can come and go, but buyers can google current programs and see what they qualify for,” she says.

Consider the following down payment assistance programs in Florida:

- Florida Assist (FL Assist): The Florida Assist program will loan up to $10,000 in closing costs on approved FHA, VA, USDA, and conventional mortgage loans. The loan is repaid as a 0% interest second mortgage, which is deferred until the homeowner either sells, refinances, or no longer occupies the property.

- HFA Preferred and HFA Advantage PLUS Second Mortgage: As part of their first-time homebuyer program, eligible Florida buyers can receive between 3% and 5% of the total loan amount in a forgivable second mortgage. The second mortgage is forgiven at 20% per year, over a 5-year term. Buyers must obtain a conventional first mortgage through Florida Housing, and must meet certain income and credit requirements.

- Florida Hometown Heroes Housing Program: For buyers who work the front lines of public safety or healthcare, as well as military members and childcare employees, the Florida Hometown Heroes program offers lower than market interest rates on standard mortgage loans, as well as up to 5% of the mortgage loan amount in down payment and closing cost assistance. Buyers must meet specific income and purchase price limits, and must be currently employed in one of the approved occupations.

3. Get preapproved for a mortgage

Getting preapproved for a mortgage will help you determine how much you can afford, which will then inform your home search. It’s always smart to shop around for the best rates and terms, so be sure to research a few different lenders during this process.

You can also ask family, friends, your buyer’s agent, and attorneys for mortgage lender recommendations. When choosing a mortgage lender, ask for a detailed cost breakdown, review the terms you are being offered, and compare loan types.

According to the US Consumer Financial Protection Bureau (CFPB), there are three general categories of mortgage:

Conventional

There are two types of conventional loans — conforming and non-conforming. A conforming conventional loan will meet or exceed the guidelines set by Fannie Mae and Freddie Mac which are government-sponsored enterprises (GSEs) that purchase conventional loans. Guidelines for a non-conforming loan will vary more widely depending on the lender.

Typical requirements for a conventional loan may include:

- Minimum credit score of at least 620

- Maximum debt-to-income (DTI) ratio of 43%

- Minimum down payment of 5%, though some programs allow for a 3% down payment

- Maximum loan amount of $647,200 in most counties; $970,800 in high-cost counties

- Typically requires private mortgage insurance (PMI) if the down payment is less than 20%

Non-conforming loans are for borrowers who do not fit into the guidelines set by Fannie and Freddie and are not eligible to be purchased by them — jumbo loans are an example of this because they offer loan amounts above the limits set by Fannie and Freddie.

FHA loans

An FHA loan is insured by the Federal Housing Administration and available from FHA-approved lenders. An FHA loan is unique in that borrowers are able to use a down payment assistance program for the entire down payment. Requirements to qualify for an FHA loan may include:

- Minimum credit score dependent on down payment amount:

- 580 = 3.5% down payment

- 500-579 = 10% down payment

- An upfront mortgage insurance premium

- Mortgage insurance premium (MIP) paid monthly for the life of the loan

- DTI of 43% or lower

- Must be borrower’s primary residence

Similar to conventional conforming loans in this way, FHA loans have loan limits that vary from county to county. For example, in Alachua County, FL, the maximum loan amount is $420,680 for a single-family home, while in Monroe County, FL the loan limit is $710,700.

Special programs

VA loans: For veterans, service members, and surviving spouses. Loans backed by the VA offer 0% down payments for those who qualify. Different lenders will have different requirements, however, VA-backed loans do not have a universal maximum DTI requirement.

USDA loans: These loans are backed by the United States Department of Agriculture and are for lower income borrowers in “rural areas.” To determine if the area you are purchasing in is eligible for a USDA home loan, use this eligibility map. These loans also offer 0% down for qualified borrowers.

4. Research the market and determine where you would like to buy

Now that you know more about preparing to purchase a house and down payments, it’s time to decide where you want to live. Do you want to live near family and friends, start over in a new city, live on the coast, or in a more rural area? Consider work commute times, average house prices, and things to do in each area that you’re thinking about living in.

Some great places to consider when buying a house in Florida include:

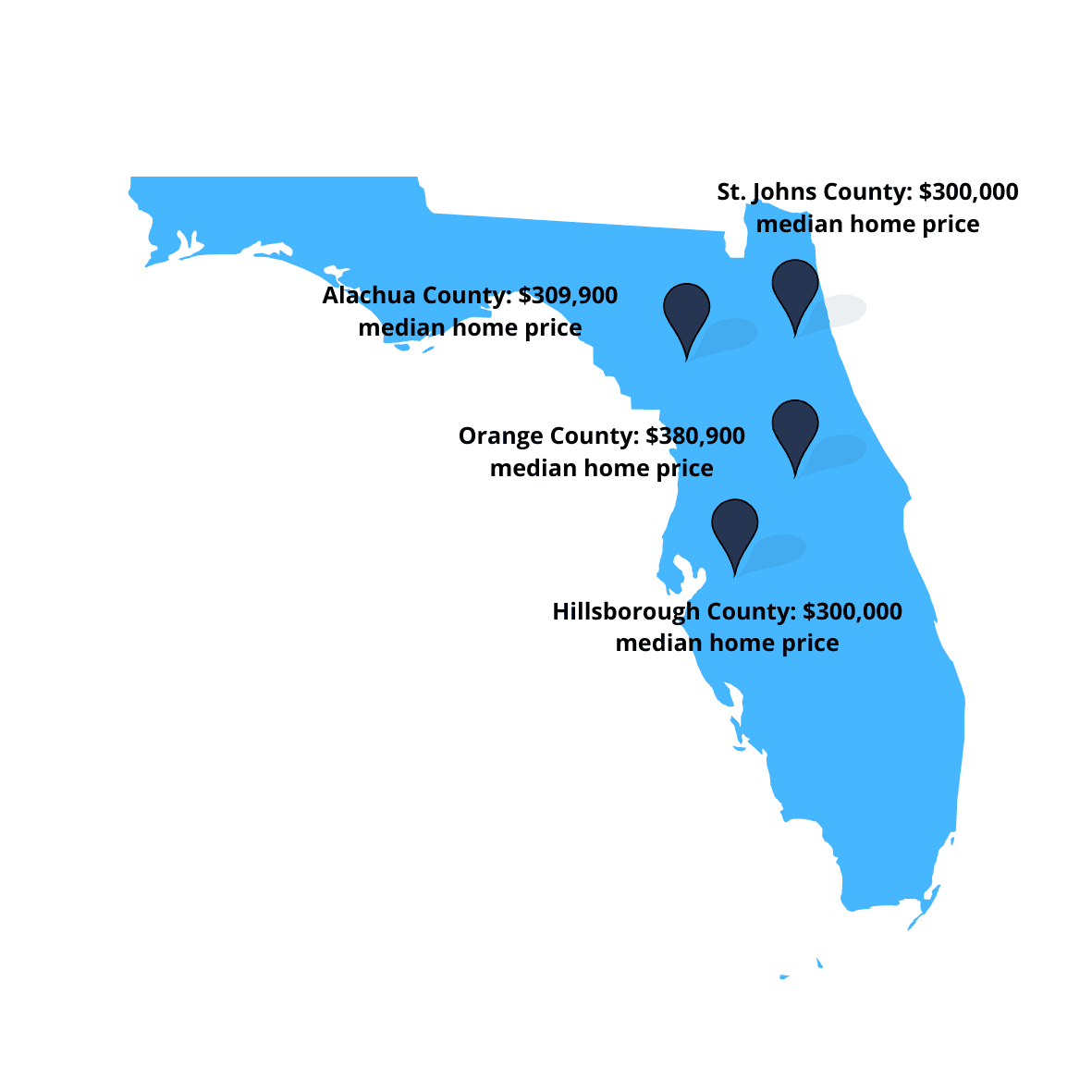

St. Johns County: Ranked #1 for best counties to live in Florida, the coastal county of St. Johns includes the communities of St. Augustine, Ponte Vedra Beach, and Nocatee. Known for having some of the best schools in the state, St. John’s is a popular region for families — and if you love being near the ocean, there are more than 40 miles of beaches to explore. St. John’s popularity does mean home prices might be a bit higher, with a median home price of $420,000 as of July, 2022.

Hillsborough County: Hillsborough is Florida’s fourth most populous county, and includes the city of Tampa, as well as smaller communities like Riverview and Sun City Center, a very popular 55+ only suburb. The current median price for sold homes here is $300,000, an increase from 2021, but still lower than other areas. Hillsborough has a rich history, with numerous historic homes and sites, all of which the county works to maintain and preserve. Living here also means access to more than 170 parks, excellent schools, and of course, beaches!

Alachua County: Located in the north-central part of Florida, Alachua County is home to the University of Florida, which is part of the city of Gainesville. Much of the county’s economy centers around the school, and it is the county’s largest employer. This county is a smaller, family-friendly region, without the tourist component of some of the beach areas, and homes here sold for a median of $309,900 in July, 2022. The county boasts several amazing fresh water springs, as well as close proximity to a variety of lakes and rivers, making it a great place for hiking, fishing, and camping.

Orange County: Amusement park fans will rejoice at the idea of living in Orange County, home to the bulk of Disneyworld’s resorts, as well as Universal Studios and Universal’s Volcano Bay. Cities here include the county seat of Orlando, and smaller communities such as Apopka, Winter Garden, and Maitland. As of July, 2022, homes in Orange County sold for a median of just over $380,900, and the county was recently ranked as the “Best County for Young Professionals.”

5. Find a local Florida agent

Real estate agents almost always appreciate it when their clients come to them to start home shopping after getting preapproved for a mortgage. This typically means that a buyer is ready to go and can start making offers. Choose a knowledgeable agent that specializes in representing buyers in the area you want to purchase in.

Your buyer’s agent will be able to help you create a wishlist, set up viewing appointments for you, tell you more about what’s going on in the neighborhood, negotiate on your behalf, and connect you with other vendors such as a title company, insurance agent, and home inspector. Real estate agents are also incredibly knowledgeable on the homebuying process as a whole and can hold your hand throughout the process to keep closing on track.

6. Start shopping for homes in Florida

Once you start your hunt for the perfect Florida home, you’ll find a wide range of home types, styles, and locations. Whether you’ve dreamed of living right on the beach, or want a high-rise condo in the middle of a big city, Florida offers a bit of everything!

As far as home styles go, new construction is trending toward a country style, says Raymer. “There are a lot of front porches, and they tend to have a cottage feel,” she says. Buyers will also find a lot of coastal home designs, as well as a good number of condos and townhomes.

While families relocating often means a more competitive market during the summer months, Raymer notes that at least during this year (2022), it hasn’t been as busy as the previous couple years. “We didn’t have the summer selling season that we usually have, but we did have a very strong first quarter,” she says. Regardless, she recommends that buyers who really want a deal should consider doing their house hunting during the winter months, especially the holidays. “People who sell during the holidays are serious about it and motivated,” she says, “which means buyers might be able to negotiate a bit more.”

With the shifts in the market, there’s more room for negotiation, but you still need to make a reasonable offer. I would say don’t come in at less than 3% lower than the asking price.

Maria Raymer Real Estate AgentCloseMaria Raymer Real Estate Agent at RE/MAX Specialists PV5.0Currently accepting new clients

Maria Raymer Real Estate AgentCloseMaria Raymer Real Estate Agent at RE/MAX Specialists PV5.0Currently accepting new clients

- Years of Experience 39

- Transactions 683

- Average Price Point $365k

- Single Family Homes 580

7. Make a strong offer

Working with your buyer’s agent to craft a winning offer can sound overwhelming. In competitive markets, cash offers could be more likely to be accepted by sellers with multiple interested buyers. While it is not always recommended to completely waive contingencies to impress a seller, you might consider pairing down to just the inspection contingency and financing contingency to remain competitive. Get creative with your offer — you may want to offer a larger earnest money deposit, schedule a quick closing, or even consider letting the seller rent the house back from you for a certain period of time.

The slight softening of the housing market around the country has also impacted Florida, but Raymer cautions buyers against making low-ball offers. “With the shifts in the market, there’s more room for negotiation, but you still need to make a reasonable offer,” she says. “I would say don’t come in at less than 3% lower than the asking price.”

Components of an offer when buying a house in Florida include:

- Purchase price

- Closing date

- Earnest money deposit amount

- Contingencies: Financing, home inspection, and appraisal

- Closing cost stipulations: Who pays for what, and if you’re asking the seller for a credit to use toward closing costs

- Home warranty

- Personal property: Such as appliances or furniture

8. Send your earnest money deposit

Your earnest money deposit, also known as a “good faith deposit,” is an amount of money you agree to pay the seller to indicate that you are serious about purchasing the home. This is usually between 1% and 3% of the purchase price. However, a higher deposit can be more attractive to sellers and make your offer stand out in competitive markets.

Whether or not you get your earnest deposit money back if you decide to back out of the sale depends on the contract. If you decide to back out of the purchase for any reason not specified in the contract, you could forfeit your earnest money. Be sure to review the contract with your real estate agent and attorney before making any decisions.

9. Order a title search

Ordering a title search can be done any time after your offer is accepted, but it’s a good idea to do it as soon as possible because it may take a couple weeks for the title search to come back, especially if the title company is backed up. Who customarily chooses the title company can vary by state and even county — but if it is the buyer’s choice, your real estate agent or mortgage lender will likely have a recommendation.

The title company will issue a preliminary title report that will be reviewed by all parties including your lender and will include items such as property tax information, easements, CC&Rs, deed restrictions, liens, and any judgments against the title of the home. Any liens, encumbrances, or judgments against the property will need to be removed before the buyer can close on the property.

In addition to liens or judgements, there are a few other title issues that might crop up. These include:

- Errors in a prior deed

- Illegal deeds

- Missing heirs

- Boundary/survey disputes

Most of these are easily resolved, but you may need the help of an attorney if there are any major disputes.

10. Shop for homeowners and specialty hazard insurances

Homeowners insurance is always recommended and it is almost always required if you’re financing your home with a mortgage. The average yearly cost of homeowners insurance in Florida is $1,960.

Depending on the home’s location, buyers may also be required to purchase flood insurance, which, in Florida, averages $629 per year.

11. Order inspections and appraisal

If you’re applying for a mortgage, your lender will most likely order the appraisal and you will pay for it. You will be responsible for ordering your own inspections with the help of your buyer’s agent, again, at your own cost. Your agent can recommend a licensed home inspection company if you don’t have one. The home inspector will schedule a date and time to inspect the house and depending on its size, it may take a couple of hours to complete.

Some common issues in homes in Florida include:

- Water damage

- Insufficient grading for drainage

- Foundation issues

- Roof damage

A good inspector will check for all of these things, and present you with a comprehensive report of their findings. Raymer says buyers should also consider separate inspections for termites, HVAC systems, and swimming pools.

12. Negotiate repairs

Remember that everything is negotiable. If you have an inspection contingency in your contract, and the inspection report comes back with tens of thousands of dollars of necessary repairs, it’s time to negotiate.

“There is definitely more room for negotiation these days than in previous years,” says Raymer, who also notes that buyers should still stick to those repair items that affect health and safety.

Talk to your buyer’s agent and come up with a plan for what to ask for during negotiations. Do you want a credit for the leaky roof or would you rather a licensed contractor repair it prior to settlement? If the house needs two new toilets, are you willing to walk away if the seller refuses to budge during negotiations? Keep the bottom line in mind, but don’t nitpick. Home inspectors are meant to be thorough. Focus on major repairs that need to be done ASAP and are going to be costly.

13. Final walkthrough

This is to verify that agreed-upon repairs have been completed and the condition of the home is satisfactory. The final walkthrough is usually done a day or two before the closing date. With the help of your agent, check that all plumbing, electrical, and HVAC units are on and working. If personal items such as the dining room chandelier and the washer and dryer were included in the contract, make sure they’re still in the house.

Buyers should never attend the final walkthrough without their agent, and they should bring along the repair addendum to the purchase agreement for the house. Your agent will be able to keep you on task as to verifying repairs are complete, and having the repair list in hand will ensure you don’t miss anything.

If you find that the necessary repairs were not made, or that there were damages left behind by the seller, notify your agent immediately so they can rectify the situation before closing.

14. Closing time!

You made it! After what might feel like a long wait, your closing date is set and you’re ready to move into your new home. The closing process in Florida is fairly straightforward, with everything processed through the title company.

Keep in mind that there can also be occasional snafus that can affect your closing date. As a buyer you’ll want to make sure of the following:

- Don’t buy any big-ticket items that could affect your credit score prior to closing

- Don’t change or quit your job

- Make sure you understand and follow instructions for your down payment funds, whether the title company requests a wire transfer or you’re bringing in a cashier’s check (no personal checks allowed!)

- Verify that your legal name is on all of your documentation, and that it’s spelled correctly.

The title can take a day or two to record after closing, but once you sign off on all the closing documents, you’ll be given the keys to your new home and can start moving in!

With so many location options, types of homes, and varying price points, buying a house in Florida might feel overwhelming, but it doesn’t have to be. Pairing with an experienced Florida agent who knows the market, the best places to live, and can help you through the entire homebuying process is the best way to make your dream of Florida homeownership come true.

Header Image Source: (Richard Sagredo / Unsplash)

- "Conventional loans," Consumer Financial Protection Bureau

- "Tackling Home Financing and Down Payment Misconceptions," National Association of Realtors (January 2022)

- "Closing costs in Florida," Finder (June 2021)

- "Florida Was Third-Largest State in 2020 With Population of 21.5 Million," United States Census Bureau (June 2021)

- "Market Statistics," Orlando Regional Realtor Association (June 2022)

Find top real estate agents near me

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.