Hard Money Lenders in Michigan: Quick Financing Options

- Published on

- 12 min read

-

Sam Dadofalza Associate EditorClose

Sam Dadofalza Associate Editor

Sam Dadofalza Associate EditorClose

Sam Dadofalza Associate EditorSam Dadofalza is an associate editor at HomeLight, where she crafts insightful stories to guide homebuyers and sellers through the intricacies of real estate transactions. She has previously contributed to digital marketing firms and online business publications, honing her skills in creating engaging and informative content.

Are you searching for a way to finance your next real estate project in Michigan? Whether you’re looking to flip a bungalow in Ann Arbor or scoop up a rental property in Detroit, hard money loans can offer the quick and flexible funding solution you need. Hard money lenders in Michigan focus on the value of the property rather than your credit score, making them an attractive option for those with tight timelines or less-than-perfect credit.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

In this guide, we’ll walk you through the essentials of hard money lending in Michigan, how these loans work, their typical uses, and the costs involved. We’ll also share alternative financing options and highlight top-rated hard money lenders in the state. Whether you’re a seasoned investor or a homeowner looking for bridge financing, understanding your options will help you make informed decisions about your financial future.

What is a hard money lender?

A hard money lender is a private individual or company that provides short-term, asset-based loans secured by real estate. Unlike traditional lenders who emphasize the borrower’s credit score and financial history, hard money lenders in Michigan focus on the property’s value. They often provide financing for house flippers and rental property buyers who require quick access to funds and flexible terms.

To determine loan amounts, hard money lenders use the after-repair value (ARV), or the estimated value of a property after all renovations are completed. They lend a percentage of the ARV to manage risk and maximize investment potential.

Hard money loans come with higher interest rates, usually ranging from 8% to 15%, and have shorter repayment periods, typically six to 24 months. Additional costs include origination fees, closing costs, and points. If you fail to repay the hard money loan, the lender will exercise their right to seize the collateral property according to the loan agreement.

How does a hard money loan work?

If you’re a real estate investor in Michigan looking for quick and flexible financing, connecting with hard money lenders could be a viable option. Here’s a breakdown of how hard money loans work:

- Short-term loan: These loans usually need to be repaid within six to 24 months, unlike the longer terms of traditional mortgages. Some lenders may be willing to extend the term up to 36 months for good borrowers.

- Faster funding option: Hard money loans can be approved and funded in a matter of days, much quicker than the typical 30 to 50 days for a conventional mortgage.

- Less focus on creditworthiness: Approval is based more on the value of the property than on your credit score or income history.

- More focus on property value: These loans use the property as collateral, focusing on its loan-to-value ratio rather than your financial situation.

- Non-traditional lenders: These loans come from private investors or companies instead of traditional banks or credit unions.

- Loan denial: Hard money loans can be a lifeline for those with poor credit who have been denied traditional mortgages but have significant home equity.

- Higher interest rates: Due to the higher risk involved, interest rates for hard money loans are typically higher than those of conventional loans.

- Might require larger down payments: Borrowers might need to provide a larger down payment, often ranging from 20% to 30%, depending on the loan details and property value.

- More flexibility: Hard money lenders can offer more flexible terms and conditions, including less stringent credit score and debt-to-income ratio requirements. Hard money loans can also help homeowners avoid foreclosure.

- Interest-only payments: These loans may offer the option of making interest-only payments initially, which can be beneficial for managing cash flow during a project’s early stages.

What are hard money loans used for?

Hard money loans are tailored to meet unique financing needs in Michigan’s real estate market. They are particularly useful for investors and individuals who need quick access to funds or face challenges qualifying for traditional loans. Here are some common scenarios where hard money loans can be beneficial:

Flipping a house: For Michigan investors involved in flipping homes, hard money loans provide fast funding for acquiring and renovating properties. These loans allow investors to quickly purchase and upgrade homes, and resell them for profit as soon as possible.

Buying an investment rental property: Hard money loans allow real estate investors to act quickly when purchasing rental properties, especially those needing immediate repairs. This allows them to capitalize on time-sensitive opportunities and potentially snatch up properties before their competitors.

Purchasing commercial real estate: Hard money loans are ideal for commercial properties because they offer speed and flexibility. When quick funding is crucial to secure a deal, these loans help investors take advantage of timely opportunities.

Exploring alternatives to traditional loans: Those with significant home equity but poor credit sometimes turn to hard money lenders in Michigan. These loans rely more on the property’s value than the borrower’s credit score, making them accessible for individuals who otherwise might not qualify for a traditional mortgage.

Facing foreclosure: Individuals nearing foreclosure can use hard money loans to refinance their debts or buy time to sell their property. This can provide a temporary solution, helping them avoid the negative impact of foreclosure on their credit report.

How much do hard money loans cost?

The cost of hard money loans is generally higher than traditional loans due to the increased risk and the convenience of quick funding. Here are some typical costs associated with hard money loans:

- Interest rates: These can range from 8% to 15%, depending on the lender’s risk assessment.

- Origination fees: Lenders may charge 1% to 5% of the total loan amount as an origination fee.

- Closing costs: Additional fees at closing can include legal fees, appraisal fees, and other administrative costs.

- Points: Lenders might charge points (a percentage of the loan amount) upfront, which can add to the initial cost of obtaining a loan.

There are many online hard money loan calculators available to estimate your costs.

Alternatives to working with hard money lenders

Hard money lenders aren’t the only option when you need fast or flexible real estate financing. Depending on your timeline, credit profile, and investment goals, there are several alternatives that may offer lower costs or different terms. Below are common financing options to consider before committing to a hard money loan.

Take out a second mortgage: A home equity loan or a home equity line of credit (HELOC) allows you to tap into your home’s equity, often at lower interest rates than hard money loans.

Cash-out refinance your home: This approach lets you refinance your existing mortgage, taking out cash based on your home’s current value. It usually offers better rates than hard money loans.

Borrow from family or friends: Getting a loan from family or friends can provide flexible terms and potentially lower interest rates, making it a cost-effective option.

Use a government-backed loan program: Loans from the FHA, VA, or USDA can help with lower down payments and more favorable interest rates.

Consider peer-to-peer loans: These loans are funded by individual investors via online platforms, offering terms that might be more advantageous than those of hard money lenders.

Explore specialized loan programs: Look into loans designed for fixer-uppers or investment property refinancing, which can replace a hard money loan with better terms.

Request a seller financing option: Some sellers are willing to finance the purchase directly, which can reduce closing costs and offer more lenient eligibility requirements.

How to buy before you sell

Sometimes, the perfect home hits the market when you’re not quite ready to sell your current one. Perhaps it’s a modern three-bedroom bungalow in Grand Rapids or a rare mid-century modern home in Kalamazoo. If you’re a Michigan homeowner who wants to buy a new home before selling your current one, HomeLight offers a streamlined solution.

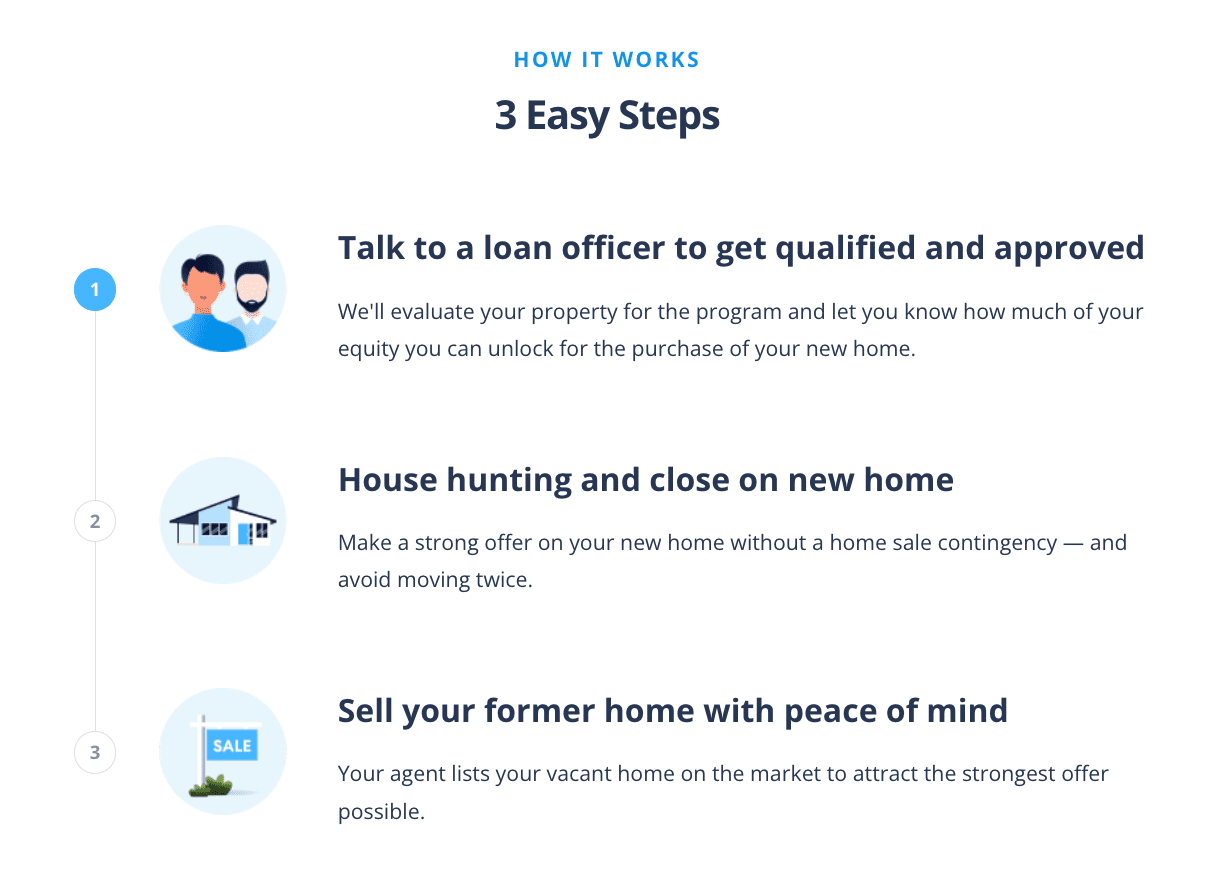

The Buy Before You Sell (BBYS) program allows you to tap into the equity of your existing home and make a stronger, non-contingent offer on a new property. If your home qualifies, you can get your equity unlock amount approved within 24 hours, with no cost or commitment required. Once approved, you can purchase your new home confidently, then sell your current home vacant, avoiding the inconvenience of moving twice.

Here’s how HomeLight Buy Before You Sell works:

While BBYS comes with a flat fee based on your current home’s sale price, the potential savings in other areas could outweigh the cost. For instance, you might save on moving expenses, temporary housing, and possibly even the purchase price of your new home. Additionally, HomeLight’s BBYS fees are typically much lower than the interest rates on hard money loans, which range from 9.5% to 12%.

3 top hard money lenders in Michigan

Michigan real estate investors have several solid options when it comes to hard money financing. The lenders below are known for fast closings, flexible terms, and broad experience with Michigan’s local markets. Here are three top hard money lenders in Michigan to consider for your next deal:

MINO Lending Solutions

Founded in 2021, MINO Lending Solutions is a full-service, nationwide mortgage originator focused on financing real estate investors. It’s headquartered in Detroit and brings more than 70 years of combined industry experience to its financial services. MINO Lending Solutions has closed over 250,000 loans and offers funding from $50,000 up to $75 million, supporting investors on projects ranging from smaller deals to large-scale portfolios.

Lending clientele: Residential, commercial, multi-family, and development Investors

Loan criteria: Up to 65% LTV (hard money loans)

MINO Lending Solutions earned a high A+ grade with the Better Business Bureau (BBB) and boasts a 5-star rating on Google based on over a hundred reviews. Clients appreciate the company’s responsiveness and ability to deliver on promises, particularly in urgent and complex situations.

They highlight the team’s ability to move deals to the finish line efficiently while providing strong support throughout the process. Many consider Mino their go-to lender, citing consistent results and a smooth overall experience.

Website: minolending.com

Phone number: 866-646-6536

Premium Hard Money

Premium Hard Money has been providing investment property financing to real estate investors in Detroit since 1995. Over the years, the company has funded more than 2,500 loans across Michigan, earning a reputation as a trusted lender for both commercial and residential real estate projects.

The firm offers loans of all sizes, specializing in single- and multi-unit residential properties in need of renovation, as well as financing for local builders and developers undertaking new construction projects throughout metro Detroit. With preliminary approvals available in as little as 24 hours and full loan closings in just five days, Premium Hard Money is designed to provide investors with fast, reliable access to capital.

Lending clientele: Residential, commercial, and development investors

Loan criteria: Contact Premium Hard Money for details

Premium Hard Money earned a 5-star rating on Google, as clients praise the company’s customer service, quick turnaround, and organization. Some reviewers note how simple and stress-free the loan process is, with clear guidance every step of the way. Others appreciate the team’s ability to close deals quickly without sacrificing professionalism.

Their responsiveness and attention to client needs stand out, making the experience smooth and dependable. Overall, investors trust the company to deliver consistent results and support for their investment goals.

Website: premiumhardmoney.com

Phone number: 248-759-8777

Lima One Capital

Since its founding in 2011, Lima One Capital has been dedicated to empowering real estate investors to improve properties, neighborhoods, and communities. Founded by two U.S. Marine Corps veterans, the company approaches every deal with the grit, determination, boldness, and integrity that reflect its Marine Corps roots.

Over the years, Lima One has set the standard for private lending excellence, serving thousands of clients across 46 states, including Michigan. The team has successfully closed over 29,000 loans, generating more than $10 billion in funding for real estate investors.

Lending clientele: Residential and commercial real estate investors

Loan criteria: Up to 75% LTV

Accredited with the BBB since 2013, Lima One Capital reflects an A+ rating. Its Google Business Profile received 4.2 stars from satisfied clients. Some share that they’ve partnered with the company for several years, successfully financing rental properties and fix-and-flip projects in different places. Others appreciate the team’s market expertise, responsiveness, and professional yet approachable style.

Lima One provides competitive rates and financing solutions tailored to investment goals, helping clients grow their single-family rental portfolios. Their consistency, transparency, and dedication to investor success have made them a trusted partner.

Website: limaone.com

Phone number: 800-390-4212

Investing in real estate?

Hire an investor-friendly real estate agent who can help you get access to off-market properties at a discount and assess potential rental income based on market trends. HomeLight can connect you with investment property specialists at no cost.

Should I partner with a hard money lender in Michigan?

Deciding whether a hard money loan is right for you in Michigan depends on your specific needs and real estate investment goals. This type of financing is well-suited for real estate investors who need fast funding for projects with quick turnarounds or when traditional financing isn’t an option. If you’re prepared to handle the higher costs and shorter repayment terms, a hard money lender in Michigan might be the perfect fit for your next investment venture.

For homeowners who want to leverage their home’s equity, HomeLight’s Buy Before You Sell program offers a compelling alternative. Instead of grappling with high interest rates, you’ll pay a flat fee while benefiting from a stronger offer on your new home and a smoother moving process.

As with any major financial decision, align your choice with your long-term strategy and consult with a financial advisor. If you’re looking to connect with real estate professionals in Michigan who have a roster of reliable hard money lenders, let HomeLight introduce you to top agents who can guide you through your investment journey.

Header Image Source: (Qingwa / Deposit Photos)

Editor’s note: This post is for educational purposes only and should not be considered financial advice. HomeLight encourages you to consult your own advisor.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.