A Homebuyer’s Ultimate Guide to Rent-to-Own Homes: What You Need to Know

- Published on

- 14 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

You’ve been scrolling real estate listings for a while, feeling the tug between craving stability and not wanting to rush into one of the biggest purchases of your life. Maybe you want more time to save money, improve your credit, or simply feel more confident before buying.

That’s why many people look for a flexible path that lets them ease into ownership without the pressure of an immediate purchase. In this ultimate guide to rent-to-own homes, we break down the process, benefits, and risks to help you decide.

Work With a Top Agent to Find a Rent-to-Own Home

When considering a rent-to-own home, working with a real estate agent experienced in these types of deals can help you navigate the process and find a great deal.

Why rent to own?

People often explore rent-to-own options when traditional home buying feels a little out of reach, whether because of savings, credit requirements, or timing. It’s an approach that gives potential buyers more flexibility while they work toward a stronger financial footing. Before diving into how it works, it helps to understand why many people choose rent-to-own in the first place.

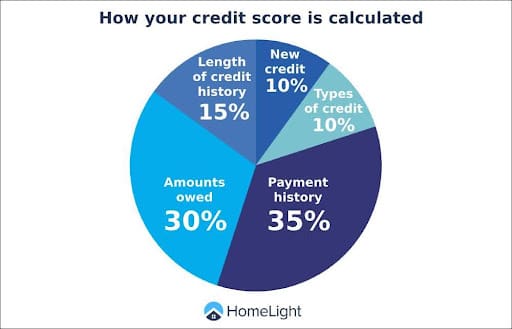

1. Build or improve your credit

One of the main reasons some buyers consider a rent-to-own arrangement is to gain extra time to improve their credit scores before applying for a mortgage. While you can qualify for an FHA loan with a credit score as low as 580, having a higher score can secure you better interest rates. For conventional loans, the minimum credit score requirement typically is 620.

Opting for a rent-to-own home lets you move into the house you want today while working on your credit. This way, when you’re ready to purchase, your improved credit score can help you qualify for a mortgage that fits your budget and financial goals.

2. Build your work history

If you just moved to the country or you just entered the workforce, then you might not have a deep enough work history to qualify for a mortgage loan. Typically, lenders will want to see at least two years in the same career, and preferably at the same company. For those embarking on a brand-new career path, it might be more difficult to qualify for a loan temporarily.

So if you don’t want to wait until you’ve got two years of work history under your belt to start shopping for a house to buy, a rent-to-own home might work nicely for your situation.

3. Save money

Buying a house is costly. You’ll need to cover the down payment, usually at least 3% for a conventional loan or 3.5% for an FHA loan, and closing costs, which can range from 2% to 5% of the loan amount. If a 20% down payment isn’t realistic, consider a loan with mortgage insurance (PMI), which adds a monthly premium. However, if you save 20%, you can avoid PMI. Some local programs might let you put down less.

Bottom line on money: The more you can save, the better. A larger savings cushion provides flexibility if appraisals come in low and helps avoid the surprise of high closing costs. With a rent-to-own option, you can live in your future home now while saving to buy it later.

4. Pay off debt

Lenders generally prefer a debt-to-income (DTI) ratio that keeps your mortgage expenses below 36% of your monthly take-home income. However, some lenders may accept a higher DTI, up to 50%, depending on the buyer’s financial profile and other factors. A lower DTI improves your chances of qualifying for a mortgage and offers more favorable terms.

If you’re working on paying down significant debt, doing so can improve both your credit score and DTI. This increases your chances of qualifying for a loan with better rates.

Rent-to-own can be a great option if you’re actively reducing debt. You can move into your future home right away and focus on improving your finances, making it a less stressful way to transition into homeownership while managing ongoing obligations like student loans or car payments.

5. Move into your dream house

Sometimes, you know exactly what will work for your family and your situation, but you’re not quite in the position to buy it. Instead of buying a transition home or starter home, some buyers might opt to skip that step and move into their ideal house today.

A rent-to-own home will allow a first-time homebuyer, or another buyer who can’t quite afford to buy their dream home today, to move into it anyway — then get themselves into solid financial shape to buy it with a mortgage in a year or three.

6. Secure a home through people you already know

Some rent-to-own agreements occur between close friends or family members, where both parties already have an established relationship and a history of trust. In these cases, the buyer likely is familiar with the property and may just need more time to save for a mortgage or improve their financial situation.

If a family member or close friend offers a rent-to-own deal for a house that is temporarily out of the buyer’s affordability range but within reach in the near future, this option can provide a quicker path to homeownership. It allows the buyer to start living in the home while working toward the financial goals needed to secure a mortgage and make the purchase permanent.

7. Avoid multiple moves

Moving can be a stressful, time-consuming process, and the thought of doing it repeatedly is enough to make anyone hesitate. If you have kids or pets, adjusting to a new home and new routines can be especially challenging. From finding the best coffee shop to figuring out the best place to walk your dog, it takes time to truly settle in.

With a rent-to-own home, you only need to move once. By the time you secure your mortgage and make the purchase official, you and your family will already be familiar with the area and the home, making the transition into permanent ownership seamless and stress-free.

»Learn more: Is Rent To Own a Good Idea? What It Is and When It Makes Sense, Explained

How do rent-to-own homes work?

A rent-to-own agreement involves two stages: renting the home and then buying it after the rental term. Typically lasting one to three years, the rental contract sets the home’s purchase price. During the rental period, the buyer pays rent and an option fee, which is an upfront, non-refundable payment that secures the tenant’s right to buy the home later and may sometimes be applied toward the down payment.

Monthly rent is usually higher, with the “extra” amount being applied toward this goal. The contract also outlines who handles home maintenance during the rental phase. After the rental term ends, the buyer applies for a mortgage to complete the purchase under a standard home sale agreement.

Rent-to-own: Lease purchase vs. lease option

There are two main types of rent-to-own agreements: lease purchase and lease option. Both involve renting a home for a set period, but the outcome differs.

- Lease Purchase: The buyer is committed to purchasing the home after the rental period. If they back out or can’t secure a mortgage, they risk losing any payments made and may face legal consequences.

- Lease Option: Once the lease ends, the buyer has the option — but not the obligation — to purchase the home. If they choose not to buy or can’t get financing, they can walk away without penalties, though whether they keep any money paid toward the down payment depends on the contract.

These agreements offer flexibility, but it’s essential to understand the terms to avoid unexpected outcomes.

»Learn more: How Do Rent-to-Own Homes Work? The 4 Steps to Homeownership

What to expect during the rent-to-own process

The rent-to-own process typically follows these key steps:

- Market research: Understand local market values, rent rates, and neighborhood trends to make an informed offer.

- Find an agent or lawyer: An agent can help, but a real estate lawyer is essential for reviewing the contract and protecting your interests.

- Search for homes: Rent-to-own properties can be harder to find, so an agent’s help is invaluable in navigating legitimate options.

- Make an offer: Submit a rent-to-own proposal outlining the lease term, sales price, and conditions, then negotiate with the seller.

- Evaluate the property: Always get a home inspection before moving in, even if you’re not immediately buying. It helps clarify maintenance issues.

- Get an appraisal: Have the home appraised to ensure the future purchase price is fair and reflects current market values.

- Conduct a title review: Verify the property’s legal standing to avoid potential fraud or title issues.

- Renegotiate terms: Based on the inspection and appraisal, you may renegotiate the price or terms before finalizing.

- Pay the option fee: Typically, 1% to 5% of the home’s price, the option fee reserves the option to purchase at the end of the rental term.

- Move in: Document the home’s condition and settle in while preparing financially for the future purchase.

- Work on finances: Use the rental period to improve credit or save for a down payment.

- Apply for a mortgage: As the rental term ends, apply for a mortgage to finalize the purchase.

- Confirm contract terms: The house enters official contract status for sale.

- Conduct final inspections and appraisals: Consider another inspection or an updated appraisal before closing.

- Prepare for closing: Factor in closing costs, 2% to 5% of the loan, and be ready for this final step.

- Close the sale: Sign documents, transfer ownership, and celebrate homeownership!

By following these steps, you’ll navigate the complexities of rent-to-own agreements and set yourself up for success when transitioning from renter to homeowner.

»Learn more: How to Get Into Rent-to-Own: 12 Steps to Homeownership

How to understand rent-to-own contracts

Rent-to-own agreements blend a lease and a purchase contract. As noted above, there are two main types: A lease option, which allows you to choose whether to buy the property later, and a lease purchase, which commits you to buying. Most experts recommend opting for a lease option unless you’re certain you’ll qualify for a mortgage.

Key components of a rent-to-own contract:

- Term: This specifies how long you’ll rent before buying, typically one to three years.

- Purchase price: The price is often set upfront but should be based on future market projections.

- Option fee: This is usually 1% to 5% of the home’s price, credited toward your purchase if you buy, but non-refundable if you decide not to.

- Monthly rent: Your monthly rent is often higher than the average, with some portion credited toward your down payment.

- Renewal clause: This lets you extend the contract if you need more time.

- Maintenance and fees: You may be responsible for upkeep and minor repairs, while the seller covers insurance. You also might handle property taxes or homeowners association (HOA) fees.

Given the complexity, it’s wise to consult a lawyer to ensure fair terms and protect yourself from scams. You also might consider negotiating for a warranty on home systems during the rental period.

»Learn more: What’s the Catch with Rent to Own Homes? 7 Reasons to Beware of These Deals

What are the rent-to-own pros and cons?

A rent-to-own agreement can offer benefits for both buyers and sellers, creating an arrangement that provides flexibility and potential financial advantages.

For buyers, it’s an opportunity to improve credit, save for a larger down payment, and establish job stability while living in the home they plan to purchase. Sellers, on the other hand, gain a steady income stream and the assurance of a committed buyer, often without the hassle of preparing the property for sale.

While there are advantages on both sides, it’s essential to consider the pros and cons before entering a rent-to-own agreement.

Pros for buyers

- Improve credit: Rent-to-own agreements offer time to boost your credit score while living in the home you plan to buy. This can help if you’re not ready for a mortgage yet.

- Save for a larger down payment: Set home prices allow you to save for a larger down payment while living in the home, which could reduce your mortgage costs.

- Build job history: Rent-to-own provides an opportunity to establish job stability, something lenders value when applying for a mortgage.

- Lower debt-to-income ratio: Extra time to pay down debts improves your chances of qualifying for a mortgage with a better debt-to-income ratio.

- Test-drive the home: Rent-to-own gives you the chance to experience the house and neighborhood before committing to a long-term purchase.

- Potentially lock in a lower price: If the market appreciates, you may secure a lower purchase price, building instant equity.

- Make home savings automatic: Higher-than-market rent premiums are often applied toward your down payment, helping you save over time.

- Avoid moving twice: Renting-to-own means fewer moves, as you’ll eventually own the home you already live in.

- Skip bidding wars: You can avoid competition from other buyers in a rent-to-own agreement, which can be especially valuable in a hot market.

- Have peace of mind: Living in the home gives you time to assess if it’s truly right for you.

- Improve your dream home: Some agreements allow you to make cosmetic changes while renting, helping you personalize the home.

Pros for sellers

- Avoid prep work: Sellers don’t need to stage or renovate the property, as the buyer is already committed.

- Secure a steady income: Sellers receive a steady stream of rent, potentially higher than market rates, plus an option fee.

- Take advantage of a committed buyer: A buyer is already lined up, with the terms and timeline clearly outlined.

- Possibly sell above market value: Depending on the terms, the seller may benefit from price appreciation and potentially sell for more than the current market value.

Rent-to-own agreements come with risks for both buyers and sellers. Buyers face upfront costs, market fluctuations, and the possibility of losing money if they don’t purchase the home. Sellers may experience delayed sales and the risk of a buyer defaulting. Both parties should carefully review the terms and evaluate the potential risks before committing.

Cons for buyers

- Face high upfront costs: The option fee and higher rent payments may add financial pressure.

- Stick to the commitment to buy, regardless: If circumstances change, backing out could be challenging, and you may forfeit your upfront payments.

- Deal with market fluctuations: A declining housing market may make the pre-set price less advantageous.

- Risk losing money: If you decide not to buy or can’t secure a mortgage, you may lose your option fee and part of your rent premium invested for the down payment.

- Deal with strict contract conditions: Rent-to-own agreements often come with strict terms, and failing to meet even small conditions could void the contract.

Cons for sellers

- Risk waiting too long to sell: Sellers may need to wait longer to complete the sale and could lose other potential buyers during the rent-to-own period.

- Lose the sale: If the buyer doesn’t purchase the home, the seller may miss out on an immediate sale and have to find another buyer.

- Handle property repair or maintenance costs: Sellers may still be responsible for major repairs or upkeep, depending on the agreement terms.

Rent-to-own can be a helpful option for both buyers and sellers, but it requires careful consideration of the terms, market conditions, and potential risks for both parties. It’s essential to read the contract thoroughly and ensure both sides understand their commitments.

»Learn more: Are Rent-to-Own Homes Worth It? The Pros and Cons

How to find rent-to-own homes

You’ve read all about rent-to-own homes, and you’re sold on the idea. Now, how do you find one?

Unlike homes for sale, there isn’t a listing portal for rent-to-own homes where you can enter your preferences and see what’s available. Here’s how to find rent-to-own homes:

1. Work with an agent

Real estate agents are formidable allies to have in your corner when you’re trying to rent-to-own a house, in part because of their networks. An expert who’s been operating in the area for several years will know homeowners who are ready to sell, landlords who are tired of the business, and other real estate agents with their own networks of sellers, homeowners, and other agents.

Working with a real estate agent who’s familiar with rent-to-own deals can be one of the best first steps you can take to find a rent-to-own house.

2. Find a brokerage that has a rent-to-own program

Real estate brokerages or teams sometimes will provide their own rent-to-own programs to help buyers get their foot in the door. This helps the brokerage generate business while simultaneously giving buyers an opportunity to own a house that they would not have had otherwise.

One example is Kenna Real Estate in Denver, which offers a “lease with a right to purchase” program for certain households.

This step overlaps somewhat with the next. Many brokerage-based rent-to-own programs are connected through companies like Home Partners. If there’s a brokerage in your area known for facilitating rent-to-own transactions, asking your agent for introductions can be a smart next step.

3. Explore rent-to-own programs

Approximately 20 to 30 rent-to-own companies operate in the United States, comprising a mix of larger, well-established players and smaller regional providers.

Some of the most well-known companies include Home Partners of America, which buys homes for buyers and rents them back with the option to purchase, and Divvy, a startup that gives renters up to three years to buy their home or walk away.

Other companies in the space include Pathway Homes, Landis, and Dream America, all of which are working to make homeownership more accessible through flexible rent-to-own options. These firms offer alternatives for buyers who may not qualify for a traditional mortgage but still want to work toward owning a home, giving them more flexibility and a clearer path despite credit or financial challenges.

»Learn more: These Rent-to-Own Homes Programs Can Help You Get Into That House

4. Approach a seller with a languishing property

Even in a fluctuating market, some homes still struggle to sell. If a property has been listed for a while without attracting buyers, it could be a prime candidate for a rent-to-own proposal. This option can offer sellers a way to generate income while keeping the potential sale on the table, giving buyers the chance to test out the home before committing to a purchase.

Sellers and even homeowners who want to get out from under a house, but who can’t find a buyer today, could benefit from considering a rent-to-own deal. They might prefer to sell the house outright today if possible, but rent-to-own would be the next-best option for them, and it’s one they’re often willing to consider.

5. Talk to a landlord

Not every landlord is a “happy” landlord, but while many are eager to sell, the transition from “landlord” to “seller” isn’t always obvious or smooth. Some may hesitate because the property needs repairs or renovations before it can be fully marketable. Others might not have the financial flexibility to go without rent for a month or two while the home is on the market. In such cases, a rent-to-own proposal can be an attractive option, allowing landlords to generate income while still working toward a sale.

If you’re currently renting and happy with your living situation, your landlord can be a great place to start when considering rent-to-own options. Even if you’re not completely sold on your current home, reaching out to your landlord is still worth considering. They may own other properties that better suit your needs and be open to a rent-to-own arrangement.

If your landlord isn’t interested, don’t worry. Take some time to connect with other landlords. Explore local rental listings, whether in your area’s classifieds or on platforms like Craigslist, to find owners of multiple properties. If they’re open to conversation, it never hurts to reach out and ask if they’d be willing to discuss a potential rent-to-own agreement. You might just find the right fit.

6. Use a foreclosure portal

Websites like foreclosure.com, realtytrac.com, and the Department of Housing and Urban Development’s (HUD) site provide listings of homes where the homeowner has fallen behind on mortgage payments, and the property is either heading into foreclosure or already in the process.

With a pre-foreclosure listing, you can approach the homeowner to explore the possibility of a rent-to-own agreement. Many people in this situation have the chance to catch up on overdue payments, so even a home currently in foreclosure could be a viable rent-to-own option if the homeowner is able to resolve their mortgage arrears.

»Learn more: Best Foreclosure Websites to Find Homes

7. Ask around

Your real estate agent likely has a broad network of contacts, and so do you. One of the most effective ways to find a rent-to-own opportunity is by tapping into your personal and professional circles. Reach out to friends, family, and acquaintances to see if anyone might be considering selling or renting out a property in the next year or two.

Social media can help spread the word, but don’t overlook the power of direct outreach. Send a text, email, or private message asking if anyone knows of a home that could be available for a rent-to-own arrangement. Be sure to share your preferred contact method, so interested parties can easily get in touch. This personal approach can often uncover opportunities that aren’t widely advertised.

»Learn more: The 8 Best Methods for Finding a Rent-to-Own Home

What are the common maintenance responsibilities of rent-to-own buyers?

In a rent-to-own agreement, buyers usually take on more maintenance duties than traditional renters. These responsibilities vary, but some common tasks include:

- Cleaning gutters: Prevent water damage by clearing gutters at least once a year.

- Replacing air filters: Change HVAC filters every 60 to 90 days to ensure efficient system performance.

- Landscaping: Mow the lawn, water plants, weed gardens, and maintain curb appeal.

- Cleaning fridge coils: Regular cleaning of coils to keep the fridge running smoothly and efficiently.

- Cleaning dryer vents: Remove lint buildup in vents to prevent fire hazards and optimize dryer function.

- Keeping up with heating and plumbing maintenance: Handle annual servicing of heating systems and plumbing, like septic tank pumping.

- Updating paint: Touch up chipped or peeling paint on interior and exterior surfaces.

- Sealing windows properly: Recaulk windows if needed to prevent drafts and improve energy efficiency.

- Fixing plumbing problems: Tackle issues like under-sink clogs and drainage problems.

Be sure to review your contract to clarify which responsibilities are yours, especially regarding major repairs.

»Learn more: Rent-to-Own Home Maintenance: Who Does What, and Who Pays for It?

Step one: Talk to an expert

Connect with a top-rated local real estate agent who can help you navigate rent-to-own options near you.

Finally: Are rent-to-own homes really real?

Yes! You really can rent-to-own a home. We found five examples of rent-to-own homes out in the wild, including:

- An investor who believes in homeownership and altruism

- A buyer who signed a lease-purchase agreement for his dream home

- A Columbus, Georgia, renter who signed a five-year lease option agreement

- A Los Angeles tenant who leveraged rent-to-own flexibility

- A seller who didn’t have the funds to get their house market-ready immediately

Only you can decide whether a rent-to-own deal would be the best option for you and your household. Talking over your options with an experienced real estate agent who understands all avenues to homeownership will get you that much closer to owning your dream home.

Writer and former HomeLight editor Amber Taufen contributed to this post.

Header Image Source: (Roger Starnes Sr. / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.