How to Clear a Tax Lien Against Your House So You Can Sell It

- Published on

- 12 min read

-

Christine Bartsch, Contributing AuthorClose

Christine Bartsch Contributing Author

Christine Bartsch, Contributing AuthorClose

Christine Bartsch Contributing AuthorFormer art and design instructor Christine Bartsch holds an MFA in creative writing from Spalding University. Launching her writing career in 2007, Christine has crafted interior design content for companies including USA Today and Houzz.

-

Jedda Fernandez, Associate EditorClose

Jedda Fernandez Associate Editor

Jedda Fernandez is an associate editor for HomeLight's Resource Centers with more than five years of editorial experience in the real estate industry.

Dealing with debt is always difficult, and when it gets to the point that you have a lien against your house for something as serious as unpaid taxes, it’s hard not to feel the walls crashing in.

But there is hope yet.

Too often homeowners forget that they’re living in their most valuable asset — their home — and that selling this asset may be the best way out from under the specter of lien.

Stressed About Selling a House With a Lien?

Sometimes the easiest way to sell a house with a lien is to get a cash offer from an investor who is familiar with the process of resolving the title issue and can walk you through it. Take the next step by providing some information through our Simple Sale platform and we’ll help show you some potential options.

Editor’s note: This article is meant for educational purposes and is not intended to be construed as financial, tax, or legal advice. HomeLight always encourages you to reach out to an advisor regarding your own situation.

Whether you’re dealing with unpaid child support, outstanding income taxes, or property taxes owed to your local county treasurer, it’s time to face the music head on so that this tax lien doesn’t hang over you any longer or further compound with penalties and interest.

Consult this guide where we’ll start with the basics (what exactly is a tax lien?), lay out in plain terms how a tax lien impacts your ability to sell your home, and explain what your options are for moving forward — from satisfying the delinquent tax to disputing its legitimacy.

What is a tax lien on a home?

A tax lien is essentially a debt claim against your assets, your biggest one being your house. This means that you cannot sell your house and pocket any equity from the sale until that tax lien debt is satisfied.

There are three main types of tax liens:

- Property Tax Liens – These liens are placed on your house for unpaid property taxes that are due to the county or city.

- State Tax Liens – These liens are placed on the property for back taxes due to your state’s Department of Revenue (DOR).

- Federal Tax Liens – These liens are placed on your home as a result of unpaid income taxes owed to the IRS.

In most cases, you’ll be dealing with the government to resolve the tax lien, but sometimes private entities become involved, such as with a property tax lien.

Your city or county can create a tax lien certificate that can be sold to outside investors. If you fail to pay off the lien, as well as the additional penalties and interest, that private investor can then foreclose on your home as a repayment of the debt.

The upside is that a private investor may be flexible and willing to compromise on the payment timeline or the amount owed. Government entities are less likely to be flexible, and both your state’s department of revenue and the IRS are willing and able to foreclose on your home, too, if their tax liens aren’t paid in full.

Why is my tax lien higher than the taxes owed?

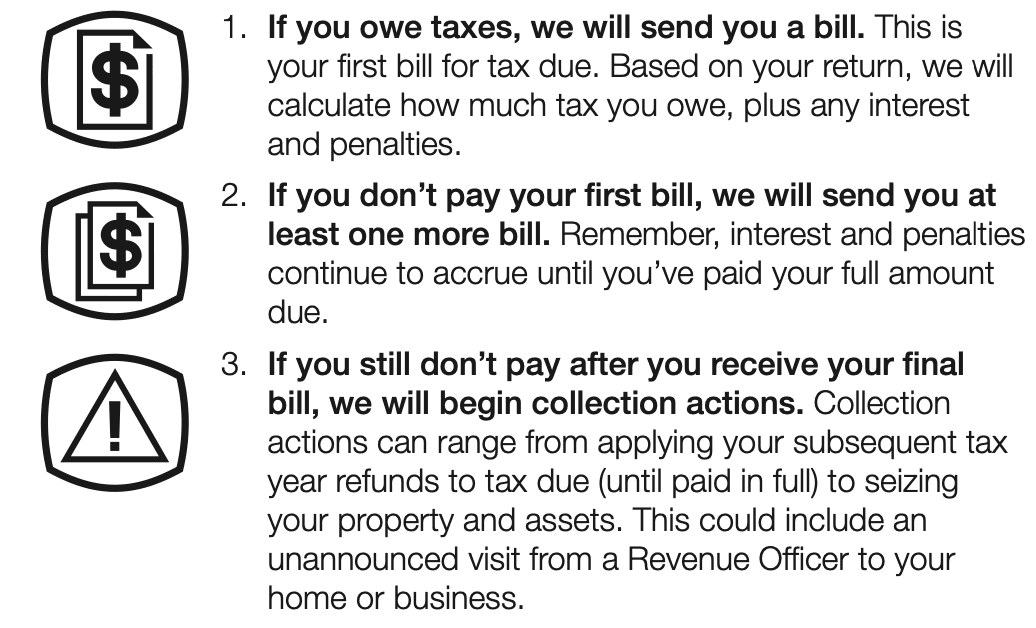

Just like any other debt owed, when you have unpaid taxes, the government is going to charge you interest and penalties when you don’t pay up on time. And sometimes, that failure-to-pay penalty can be as high as 100% of your tax debt — which can be the case with unpaid employment taxes.

Wenatchee, Washington-based real estate agent J. Perrin Cornell provides the following example:

“Let’s say you have a $5,000 lien on your property for unpaid employment taxes. If you incur that 100% penalty, then you’re up to $10,000 plus 12% interest per month. And if you let that lien sit on your property unaddressed for several years, then suddenly your $5,000 nonpayment of taxes is a debt of $20,000 or more.”

As that tax debt piles up, it’ll swiftly eclipse any equity that you’ve built up in your home.

You won’t have that same 100% penalty on all liens, but expect some kind of “late fees” to apply to various unpaid taxes. For income taxes, the federal government charges the following penalty:

“One-half of one percent for each month, or part of a month, up to a maximum of 25%, of the amount of tax that remains unpaid from the due date of the return until the tax is paid in full. The one-half of one percent rate increases to one percent if the tax remains unpaid 10 days after the IRS issues a notice of intent to levy property.”

Failure to file can also incur penalties of between 5% and 25% of the unpaid tax per month. After 60 days, you’ll face another late-filing penalty — either $450 or 100% of the tax owed, whichever is less.

That’s why it’s vital to get your lien situation sorted out as soon as possible.

If selling your home is the only way to clear your tax lien (meaning, you can’t clear the lien with out-of-pocket cash from savings), then put it on the market as soon as possible so that ongoing penalties and interest don’t shrink your equity down to nothing.

It can take more time than you’d think to clear a tax lien.

“We don’t want to wait until you’ve gotten an offer, we need to start working on your lien as soon as possible because it can take a lot of time to resolve. I have one that started in November of 2017, and we finally got it cleared in August of 2018,” recalls Cornell.

How is a tax lien discoverable?

Whether out of embarrassment or denial, many homeowners hold out hope that their tax lien problem won’t crop up until after the home sale closes.

Unfortunately, you can’t hide under a rock forever when it comes to taxes.

Tax liens are discoverable during a title search — even if the lien data isn’t an exact match.

“Tax liens will be discovered during a title examination. In Georgia, the liens can be found in the Georgia Property Records Search. The parties’ names are searched under the lien index in the county in which the property lies,” explains Sarah Stitgen, an Atlanta-based closing attorney for Cook & James.

“Often, you will find liens that are not an exact match of the name, and those will need to be further investigated. For example, the home seller may be Sarah Lee Smith and tax liens may pull up with just Sarah Smith or Sarah L. Smith. Some liens will provide the last 4 digits of SSN and can be verified with that information.”

One of the biggest mistakes you can make as a homeowner is failing to tell your real estate agent about the lien. Honestly, an experienced agent is your best ally when facing a tax lien while trying to sell your house.

“If your lien situation is simple and for a low dollar amount, you can probably resolve it with the help of your agent and a title company. But if you have a complex lien situation, you need to work through it with a qualified tax attorney or tax advisor as soon as possible,” advises Cornell.

“It may be possible to pay off your lien with a HELOC (home equity line of credit) before you sell the house, if you’ve got a lot of equity built up,” Cornell suggests. “But you cannot wait to use equity from the completed home sale to pay it off. Closing is too late to deal with a lien, you have to do it early on.”

What are my options for selling a house with a tax lien?

When you sell a house that has a tax lien on it, that doesn’t mean you’re transferring the lien with the house to the buyer. That tax debt is yours and you’ll need to deal with it before the sale can close.

Let’s take a look at your options for dealing with your tax lien.

1. Dispute the tax lien with the IRS (or other government entity)

If the tax debt that triggered the lien against your house is not yours, or you’ve already paid the lien off, then disputing the tax lien is the smart play.

But disputing a tax debt is rarely easy.

“The IRS doesn’t go away, and dealing with them comes with a lot of issues. For example, they’ll only communicate with you by letters or telephone, not email,” explains Cornell.

(Warning: If you do get an email supposedly from the IRS saying there’s a tax lien on your house, don’t engage — as it’s almost certainly a scam.)

In fact, the IRS may not even deal with you until you’ve brought in a qualified tax advisor. They don’t have to talk to your real estate agent, or the title company. They only have to talk to your tax advisor, so you need to appoint one ASAP.

For example, let’s say your tax lien was filed in error.

The IRS will withdraw the federal tax lien, but you’ll need your tax attorney to request an appeal, and you’ll need evidence to back up your claim — such as proof that the tax debt was incurred by someone else with a similar name.

If you have proof that the taxes were already paid off, but the lien is still on your house after 30 days, you may need to file a request for a certificate of release before your home sale can close.

2. Request a certificate of discharge

Another option is to request a certificate of discharge from the IRS.

“Federal tax liens need to be satisfied via payment; however, there are circumstances in which the IRS will grant a partial release for the particular property, or there may be an opportunity to obtain a certificate of discharge which will release the property but not the lien itself,” advises Stitgen.

The certificate of discharge detaches the lien from your house so that it can be sold, but it does not absolve you from the tax debt. You must still pay those back taxes to the IRS, and other personal property or assets can be seized to satisfy the tax lien.

3. Satisfy the delinquent tax

If you know you owe those taxes to the city, state, or IRS, then you’ll need to satisfy that delinquent debt before you can sell your home. For home sellers who don’t have the cash to pay it off in their savings, you may have other financing options.

“It may be possible to pay off your lien with a HELOC (home equity line of credit) before you sell the house, if you’ve got a lot of equity built up,” explains Cornell.

“But you cannot wait to use equity from the completed home sale to pay it off. Closing is too late to deal with a lien, you have to do it early on.”

In other words, you simply cannot leave the lien unaddressed until closing — even if you plan to pay it off with the proceeds — or your home sale will not close. However, you can wait to pay off the lien until closing if you make arrangements to do so.

4. Pay off the lien amount at closing

“The home seller has an option to pay the tax lien off on their own prior to the closing, but they will be responsible for obtaining a lien release from the IRS and presenting that prior to closing,” explains Stitgen.

“This can be time consuming and hold up the closing. The more common option is for the lien to be paid at the closing with proceeds from the sale.”

The closing attorney will submit the funds from the closing to ensure satisfaction of the lien.

Let’s say that Jane and John Doe have a mortgage on their home that stands at a balance of $140,000. They can sell their home for $200,000, but there’s a Federal Tax Lien of $22,000. Your tax attorney can arrange for that $22,000 to be paid out of the proceeds of the home sale at the time of closing.

What happens is this: your law firm remits payment to the IRS for the full amount, and the IRS files a release of the lien. Once that tax lien and the mortgage are both paid, the amount due to the home seller at the time of closing would be $38,000 (minus any commissions due to the Realtor and any credits, if any, to the buyer).

5. Wait for the debt to expire (which almost never happens)

If you’ve had that tax lien hanging over your head for close to a decade, then it may be wiser to wait to sell your house until the 10-year statute of limitations period ends. That will free you from the tax lien without paying it off.

But don’t hold your breath waiting for that to happen.

If the dollar amount of your tax lien is low, there is a chance that the IRS will let the debt expire, but in most cases, Uncle Sam will get his money, no matter how long it takes.

What’s more likely to happen is that the IRS will file suit against you for collection.

When the IRS files suit, this reduces the claim against you to judgment — meaning the penalties and interest will stop as your debt amount is locked in by the judgment. However, it also removes that 10-year statute of limitations. That judgment against you remains in place until it is paid in full.

What if the tax lien exceeds what you earn from the sale?

If the proceeds from your home sale are not enough to pay off your mortgage and your tax lien, don’t assume you can satisfy the remaining IRS debt on a payment plan.

“In the event that there will not be enough proceeds to pay the lien, the seller will be required to bring that money to the closing in order to fully satisfy the lien,” explains Stitgen.

“It is not typically an option to convert the remaining debt and make payments to the lien holder. Since tax debts become an automatic lien on the property, it would be highly unlikely they would remove the lien without full satisfaction.”

If you cannot come up with the cash to cover the difference between your home sale proceeds and your debts, then filing for bankruptcy may be your only option.

This won’t clear your tax lien debt, but it will make sure that the IRS gets paid.

“I had a client who both had a lien on her house and she was facing foreclosure, and the IRS would not back off until they got their $17,500. The client couldn’t afford that, so there was no way to solve it through the home sale,” recalls Cornell.

“The house went back to the bank, she filed for bankruptcy and walked away with worse than nothing, because she was now in debt. But the IRS got their $17,500 in the end from the bankruptcy trustee.”

Don’t wait to deal with your tax lien debt

Getting notification of a tax lien on your house can feel like your financial standing has just been destroyed. But don’t let yourself be buried under that tax debt. Denial and procrastination won’t make your tax lien problem go away.

The sooner you deal with a tax lien during the home sale process, the better off you’ll be. And with the assistance of a knowledgeable tax attorney and an experienced real estate agent, you’ll know all your options for selling your house with a tax lien for the best fighting chance at moving on.

Header Image Source: (Aubrey Odom / Unsplash)

- "Tax lien investing is risky for most investors. Here’s what to know before jumping in," Bankrate, Sarah Foster & Dan Kelley (August 2023)

- "INDIVIDUAL TAXES: STATE LIEN," 20/20 Tax Resolution (May 2023)

- "Understanding a Federal Tax Lien," Internal Revenue Service (December 2022)

- "What Is a Tax Lien Certificate? How They're Sold in Investing," Investopedia, Julia Kagan (June 2024)

- "What Happens If You Don't Pay Property Taxes on Your Home?," NOLO, Amy Loftsgordon (October 2023)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.