America’s House Price History: Does Homeownership Still Pay Off?

- Published on

- 10 min read

-

Melissa Rudy Contributing AuthorClose

Melissa Rudy Contributing Author

Melissa Rudy Contributing AuthorClose

Melissa Rudy Contributing AuthorMelissa Rudy is a seasoned digital journalist with 15 years of experience writing web copy, blog posts and articles for a broad range of companies. When she can’t buy or sell homes, she settles for the next-best thing: researching and writing about all things real estate-related.

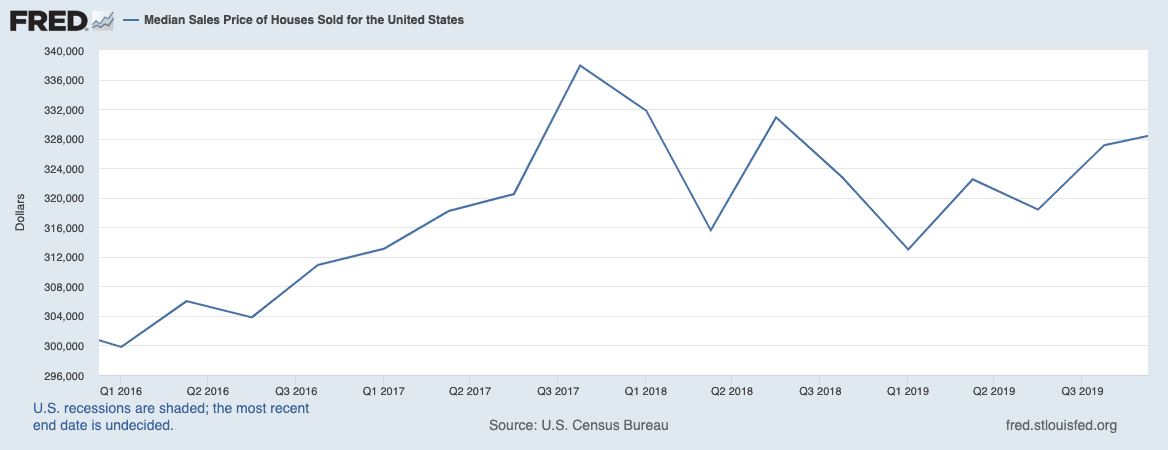

You’ve heard relatives and friends assure you many times over: “Real estate is a safe bet! You don’t want to throw your money away on rent.” But if you looked at the Census Bureau’s measure of median new home prices from the three year period of 2016 to 2019, the zig-zags might worry you as a sign of volatility:

Can you trust that your home will be worth more than what you bought it for by the time you’re ready to sell?

Let’s look to America’s house price history for answers.

We asked a PhD economist, chief house appraiser, and top real estate agent to go back in time and walk us through some of the earliest available aggregate data for U.S. home prices through now.

Home values over the decades: Up and to the right

Erik Pogwist, chief appraiser of Incenter Appraisal Management, a national provider of valuations, inspections, and data products for lenders across the country, says that in spite of the inevitable plateaus or downturns over the years, home values tend to rise over the long term.

Sherry Ajluni, a top real estate agent in Cumming, Georgia, agrees. “Even if home prices go down over the next couple of years as inventory goes up, they will most likely be back up by year three or four,” she says.

The data backs them up. According to Black Knight, a longstanding real estate and mortgage analytics company, annual home price growth has seen a 25-year average of 3.9%. In 2019, average yearly price gains slipped slightly to 3.8%, marking the first shrink in gains since 2012.

In September of 2020, Black Knight reported a staggering 14.2% increase in home prices, far above the 25-year average. Driven by low mortgage interest rates and a shortage of inventory, it was the biggest yearly spike seen in more than 15 years.

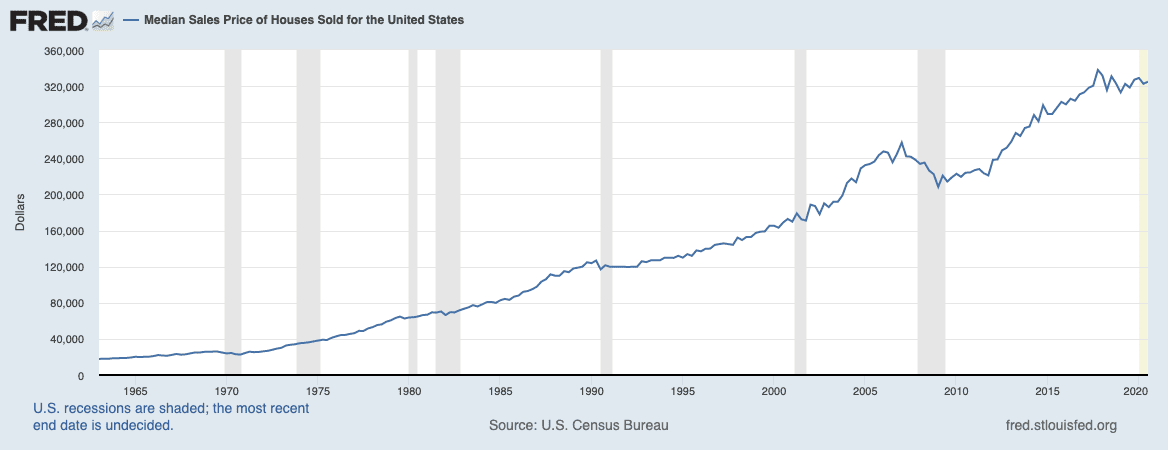

According to the U.S. Census Bureau as aggregated by the Federal Reserve Bank of St. Louis, the median sale price of new residential homes has steadily increased over the decades.

In the below chart, you’ll see short-term price fluctuations from one month (or year) to the next, which can feel substantial to homeowners at the time. Also notice the sharp dip from 2007 to 2009 triggered by the subprime mortgage crisis and subsequent housing market crash.

But when you take in the long view, it’s clear that home values do appreciate and recover from short term fluctuations. Notice that the potholes look a lot shallower than they did above, when the chart zoomed in on a shorter three-year span.

| Year | Median sale price |

| 1965 | $20,200 |

| 1970 | $23,900 |

| 1975 | $38,100 |

| 1980 | $63,700 |

| 1985 | $82,800 |

| 1990 | $123,900 |

| 1995 | $130,000 |

| 2000 | $165,300 |

| 2005 | $232,500 |

| 2010 | $222,900 |

| 2015 | $289,200 |

| 2020 | $329,000 |

Source: (U.S. Census Bureau/ Federal Reserve Bank of St. Louis)

It’s important to note that the data above represents home prices in the new construction segment, which account for only around 10% of home sales. Existing home sale metrics are tracked by the National Association of Realtors (NAR) and published on a monthly cadence as well. But there are limits on how that data can be used outside of NAR.

Although new construction prices typically trend higher than the prices of existing homes on the market, they remain a useful representation of broader home price trends and appreciation patterns over the decades. For example, in the chart above, you can see the impacts of the housing crash reflected in new home prices in 2005 ($232,500) to 2010 ($222,900).

Factors that drive up home prices

Homeowners can help boost their property value by making strategic upgrades and keeping up with routine maintenance. But when viewing America’s house price history from a broad lens, it’s most telling to look at the major events that have shaped property values in this country and the biggest forces that drive movement in the real estate market over time.

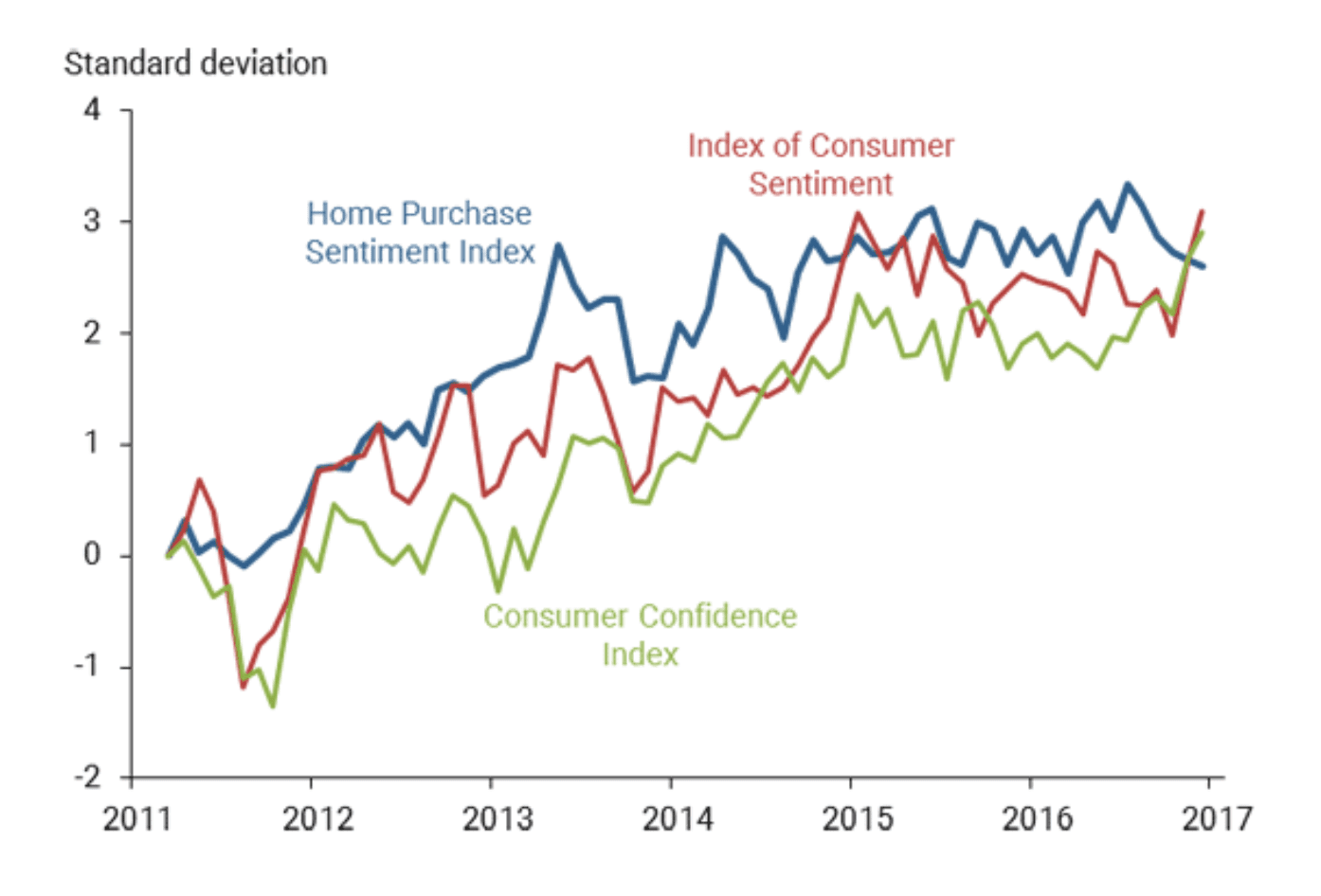

Consumer confidence

Each month, Fannie Mae conducts a survey of 1,000 consumers to gauge their sentiments on the housing and mortgage market. Using the results of this National Housing Survey (NHS), Fannie Mae then creates the Home Purchase Sentiment Index (HPSI), which measures consumers’ confidence in the current housing market — in other words, whether they feel it is a good or bad time to buy a home. Higher consumer confidence usually means people are more open and willing to buy, which translates into higher housing demand and the potential for values to rise.

In May of 2020, at the height of the first wave of the COVID-19 pandemic, the HPSI fell to 63, its lowest level since November of 2011. Sidelined by business closures, layoffs, and reduced income, consumers weren’t too keen on house-hunting. But the following month, the Index began to climb again, reaching 76.5 in June as consumers recognized that the low supply, growing demand, and escalating house prices had created a strong seller’s market. By October of 2020, the Index had recouped more than 60% of the losses incurred by the pandemic.

The HPSI has seen other dips and peaks over the years. After steadily rising for a couple of years after the Great Recession, it plummeted again in 2013 in response to what was known as the “taper tantrum,” a period of instability in the bond markets. Later that year, the Index resumed its climb.

The takeaway here is that consumer confidence has its ups and downs, but if you look at the Index numbers in context over the years — similar to what we’ve seen with home prices — they tend to trend upward.

A change in government regulations

New leadership, new zoning laws, or other legislation can change the demand for property in an area. As one example, if the government issues tax credits, deductions, or other subsidies, the resulting boost to consumers’ income levels could cause an influx of buyers and trigger an increase in home prices.

One national example of this was the U.S. government offering the First-Time Homebuyer Tax Credit in 2008 as a way to encourage homeownership and boost the economy during the Great Recession. On a local level, California passed new legislation in 2020 that relaxes the requirements and expands the earning opportunities for owners of accessory dwelling units (ADUs). One of the biggest changes is that homeowners can now rent out ADUs for an added revenue stream.

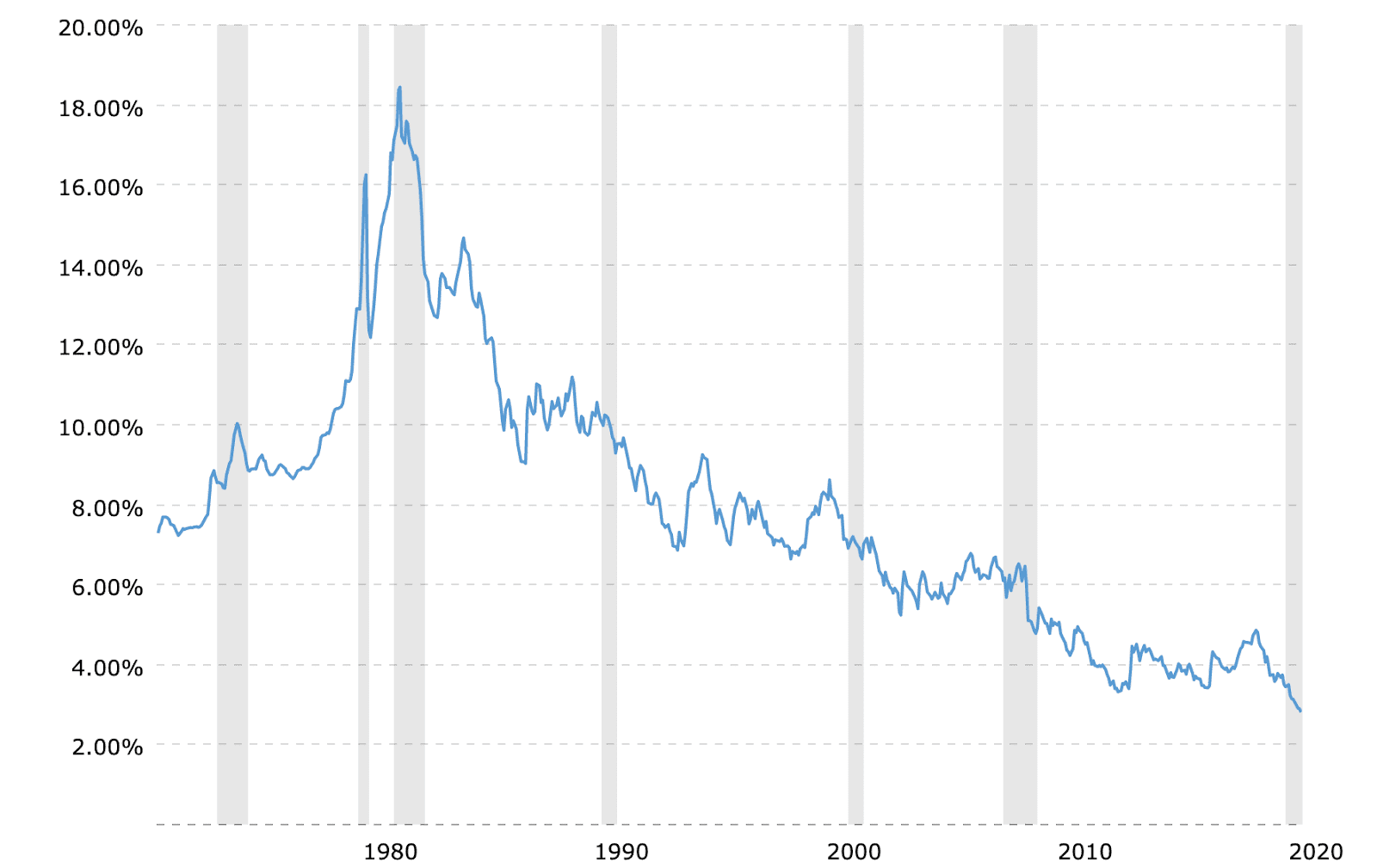

Low mortgage interest rates

When mortgage rates drop, it tends to trigger a flurry of activity among potential buyers who are lured by the promise of interest savings. As more people enter the housing market, there is greater competition for the available listings, which in turn causes prices to go up. This was seen in the summer and fall of 2020, amid the COVID-19 pandemic: As of October, mortgage rates were at near-historic lows of 2.81%, leading to a flurry of active buyers and a shortage of inventory.

It might seem like mortgage rates have a mind of their own, but there are many factors that impact how they behave — like the Federal Reserve Bank adjusting the money supply, the state of the bond market, housing market trends, the rate of inflation, and the overall health of the economy.

30 Year Fixed Mortgage Rate – Historical Chart

A thriving employment sector

There’s a reason that home prices soared more than 20% in Northern Virginia when Amazon announced in 2018 that it would build its new headquarters in Arlington — and similarly, why home prices dropped 15% in New York City when Amazon nixed its initial plans for a second headquarters in the Big Apple. The addition of a large employer, new headquarters, or distribution center tends to bring an influx of new employees and other businesses, thus driving up the housing demand and prices. For example, Aljuni says that her Atlanta housing market got a big boost a few years ago when Mercedes-Benz relocated its headquarters to the area, creating hundreds of jobs.

Proximity to a more expensive market

If an upscale, highly desirable area has low housing inventory or the price point is just too high, some buyers may seek properties in neighboring communities. “This can cause values to increase, as the larger market becomes too costly for some buyers looking for more reasonable housing costs, which drives up demand and values in the smaller local market,” explains Pogwist.

One example of this phenomenon is the massive spillover of buyers looking to flee New York City and settle into New Jersey suburbs. As reported by The New York Times in August 2020, New Jersey saw an average 44% boost in home sales compared to last year. This influx of demand caused home prices to skyrocket in city-adjacent neighborhoods.

The same effect has been seen in Tacoma, Washington, as people who can’t purchase homes in the competitive Seattle market are heading south to nearby Tacoma, where real estate prices are now twice as high as they were five years ago.

Low inventory

If there is a rush of buyers in an area but not enough homes to meet the demand, that typically creates a “seller’s market,” as prices tend to spike and buyers are forced to make more competitive offers.

The critical number here is months of supply, which measures how many months it would take for the homes currently on the market to sell at the existing pace of home sales. As an example, if there are 80 homes listed and 20 homes sold each month, that means there would be a four-month supply of properties. When you hit less than six months of supply, you enter seller’s market territory.

In the new construction segment, a shortage of materials can also slow down the building of homes. The pandemic disrupted the lumber industry in spring and summer of 2020, as sawmills ceased operations and led to a backlog. Meanwhile, there has been a growing demand for timber among DIY renovators who suddenly found themselves at home with the time to tackle projects. The lumber shortage has led to a slowdown in construction and a ramp-up of prices.

In terms of existing home sales, older homeowners choosing to keep their homes into their retirement years can also contribute to low inventory. While the traditional course of action has been for empty nesters to sell their bigger homes and downsize, baby boomers are increasingly deciding to remain in their homes during their golden years, which has led to housing shortages for up-and-coming buyers in many areas.

Natural disasters

Given their destructive nature, it might seem that earthquakes, floods, hurricanes, wildfires, and other catastrophic events would have an equally disastrous impact on home prices. But as Dr. Frank Nothaft points out in his research on natural hazards, although these crises tend to trigger a spike in mortgage delinquencies locally, they can also cause an increase in home prices in surrounding areas. This is because people who have been displaced from their homes are forced to find new housing, and they generally prefer to stay in the same general area.

Risk factors that can cause home values to fall

Despite a homeowner’s best efforts at finding a desirable property and keeping it up-to-date and well-maintained, there are many extenuating circumstances that can send home prices downward.

Recession

When an economy is crippled by a recession, people generally have less disposable income and are hesitant to make big purchases like a house. “In a recession, more people are unemployed and cannot pay their mortgages,” Tenpao Lee, Ph.D., a professor of economics at Niagara University, told HomeLight. “Therefore, in a recession, the demand for a home will decline and the supply for a home will increase. Home prices will inevitably decline.”

The Great Recession is the most recent example of an extreme economic downturn that had a direct impact on home prices. Starting in the mid-1990s, home prices began to climb, reaching an average of $207,000 in the year 2000 and then peaking at $314,000 in 2007. Escalated home prices, lenient lending criteria, and a deluge of subprime mortgages all contributed to the bursting of the housing bubble, triggering what was essentially a free-fall of the U.S. economy.

During the recession that spanned 2007-2009, home prices plummeted 33%, resulting in millions of homeowners going underwater on their mortgages and many even losing their homes. The recovery was slow but steady. By 2018, according to CoreLogic, average home prices had climbed back up to 1% higher than their peak in 2006.

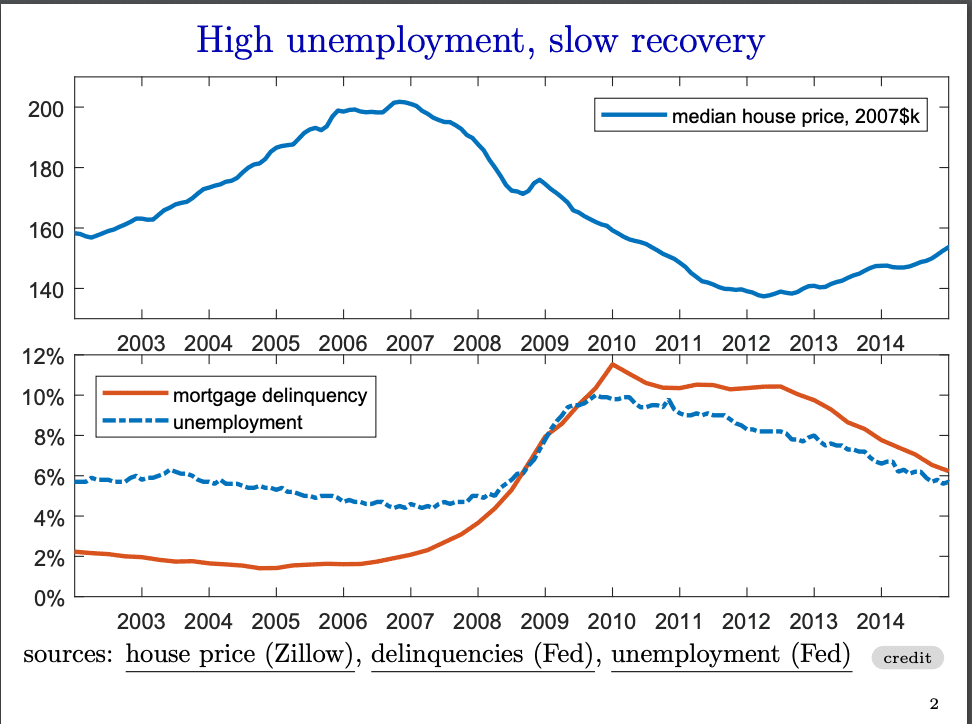

High unemployment rates

High unemployment puts home prices at risk. This chart from a Stanford Economics study shows how as unemployment rates spiked during the Great Recession, the median home price plummeted in tandem. Job insecurity puts people at risk of mortgage delinquency, and if enough people can’t pay their mortgage, a subsequent glut in foreclosures can create a rush of supply that drags down home values.

A surplus of inventory

If there is an excess of inventory but not as many buyers, it becomes a “buyer’s market,” where a motivated seller may consider lower offers to compete with other available homes. Going back to the months of supply metric, if there is more than a six-month supply of homes, buyers have the upper hand.

Sometimes a surplus arises from a boom in demand. In the run-up to the housing crash of 2007-2008, lax lending regulations resulted in a flurry of demand from buyers. Homebuilders ramped up production in anticipation of sustained future demand. When the crash slowed demand to a crawl, you saw an excess of newly built homes on the market — i.e., blocks and blocks of empty McMansions.

How does your home fit in?

With so many different factors causing housing prices to shift up and down, what do you need to know about your own home’s value? While a house can be a lucrative investment, for most homeowners it’s about more than sheer profit — it’s a place to create roots, enjoy life with loved ones, and create lasting memories.

At the same time, the financials matter. You need the value of your home to at least cover the fees for selling a house, which can be up to 10% of the sale price. The good news is, history is in your favor: Most homeowners tend to come out on top in the long run, and the longer they stay, the more they gain.

Header Image Source: (Ramona Zepeda / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.