What Is My Home Worth? A Guide to Finding the Value of Your House

- Published on

- 13 min read

-

Lori Lovely, Contributing AuthorClose

Lori Lovely Contributing Author

Lori Lovely, Contributing AuthorClose

Lori Lovely Contributing AuthorLori Lovely edited the Real Estate Home section for the Indianapolis Star and covered the annual Dream Home construction and decor for Indianapolis Monthly magazine. She has written guides for selling houses and more.

-

Richard Haddad, Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

Whether you plan on selling your home, want to refinance to take advantage of lower interest rates, or wish to know how much equity has accrued to borrow against it for renovation or for personal expenses beyond the home, a home valuation can give you clarity. It helps guide smart decisions for renovations, borrowing, or other financial moves. With this insight, you can plan your next steps with confidence.

A Quick (And Free) Way to Check Your Home Value

Get a preliminary home value estimate in as little as two minutes. Our tool uses information from multiple sources to give you a range of value based on current market trends.

A home’s value isn’t just a number. It’s a combination of location, upgrades, market conditions, and even the little quirks that make your place, well, yours. Knowing what drives your home’s worth gives you the power to plan renovations, time a sale just right, or figure out how much you could borrow without losing sleep. Think of it as getting the full backstage pass to your property’s value.

This FAQ sheet and our expert, Desiree Carroll, a top agent who sells 14% quicker than the average Bethlehem, Pennsylvania agent, will guide you through the ups and downs of acquiring an accurate home value estimate and explain what makes property values fluctuate. We’ll also give it to you straight about online valuation tools.

1. How can I estimate the value of my home?

There’s more than one way to determine the value of your home. Some of the best and easiest include:

- Use an online valuation tool, such as HomeLight’s Home Value Estimator (HVE), or an automated valuation model (AVM)

- Talk to an experienced real estate agent

- Request a professional appraisal

- Check public records

Your choice will depend on your reasons for wanting a home valuation.

- If you just want a rough estimate for your own personal knowledge, using an online valuation tool to get a free home appraisal should suffice. However, if your goals include refinancing or selling, home valuation tools typically don’t have enough data to provide an accurate valuation.

- If you’re considering accessing your home’s equity in a home equity line of credit (HELOC) or a cash-out refinance, your lender will typically require a third-party appraisal, which can cost several hundred dollars or more.

- If you’re considering selling your home, consulting a real estate agent is an affordable choice because most professionals provide a comparative market analysis (CMA) as part of their services.

2. How does HomeLight’s online home value estimator work?

HomeLight’s online home value estimator works by combining details you share about your home with data pulled from public records and multiple market sources to generate a real-time estimate based on current trends. To make the estimate more personalized, it also includes a short questionnaire that accounts for your home’s property type and condition—something many online tools skip.

In addition to the estimate, HomeLight provides a list of top local agents with proven track records for strong sale prices, giving you expert insight into accurate home pricing.

That said, like most online valuation tools, the estimate isn’t exact. While it relies on hard data, it may not fully capture your home’s upgrades, additions, or unique condition.

HomeLight’s valuation also includes the Simple Sale price. With Simple Sale, you can request an all-cash offer to buy your home. If you accept, you can pick the move date and get your home sold fast without the hassle of making repairs and having buyers come into your home. We estimate a home’s Simple Sale offer price to be around 90% of market value.

Find out what your home might be worth in two minutes and connect with a top agent with HomeLight’s Home Value Estimator. Whether your journey ends with learning your home’s ballpark value or this information is merely the first step on a path toward refinancing or selling your home, this is a great starting point.

3. Should I pay for a professional appraisal?

“An appraisal provides the most accurate valuation,” Carroll says. The caveat is that it is one person’s opinion at one moment in time. The appraised value can be very different three to six months later since an appraisal is largely based on what has recently sold in the area.

If you’re considering refinancing your home or are interested in a HELOC, your lender will typically require an appraisal performed by an independent third party. The cost of a professional appraisal varies by region, with appraisals in the Pacific Northwest usually commanding higher prices than in the South.

Thankfully, however, the Dodd-Frank financial reform from 2010 dictates that a professional appraiser’s fees must be reasonable and customary for the geographic market.

Keep in mind that different loan types, like FHA, VA, and conventional, will have different appraisal requirements.

4. Can I get a home valuation from an agent if I’m not selling my home right now?

Most real estate agents provide you with a CMA as part of their listing services. A thorough CMA, which often exceeds 30 pages of detailed examination, is a tool that should provide a professional valuation of your home, comparing your property with similar properties in the neighborhood (known as comps) as well as the current market.

Some agents charge $100 to $200 for compiling a CMA. Many charge nothing.

“I don’t get paid for a CMA,” Carroll states. She considers it part of relationship building. In an industry based on referrals and client relations, she likes to help past clients in the hope of future business. “Not everything we do is compensated.”

Some states don’t allow real estate agents to get paid for creating a CMA. “You would have to be an appraiser if you’re paid.” Her brokerage (as well as some states) doesn’t even permit its agents to be paid for a Broker Price Opinion (BPO) in which a real estate broker offers a written estimate on a home’s valuation based on expert judgment.

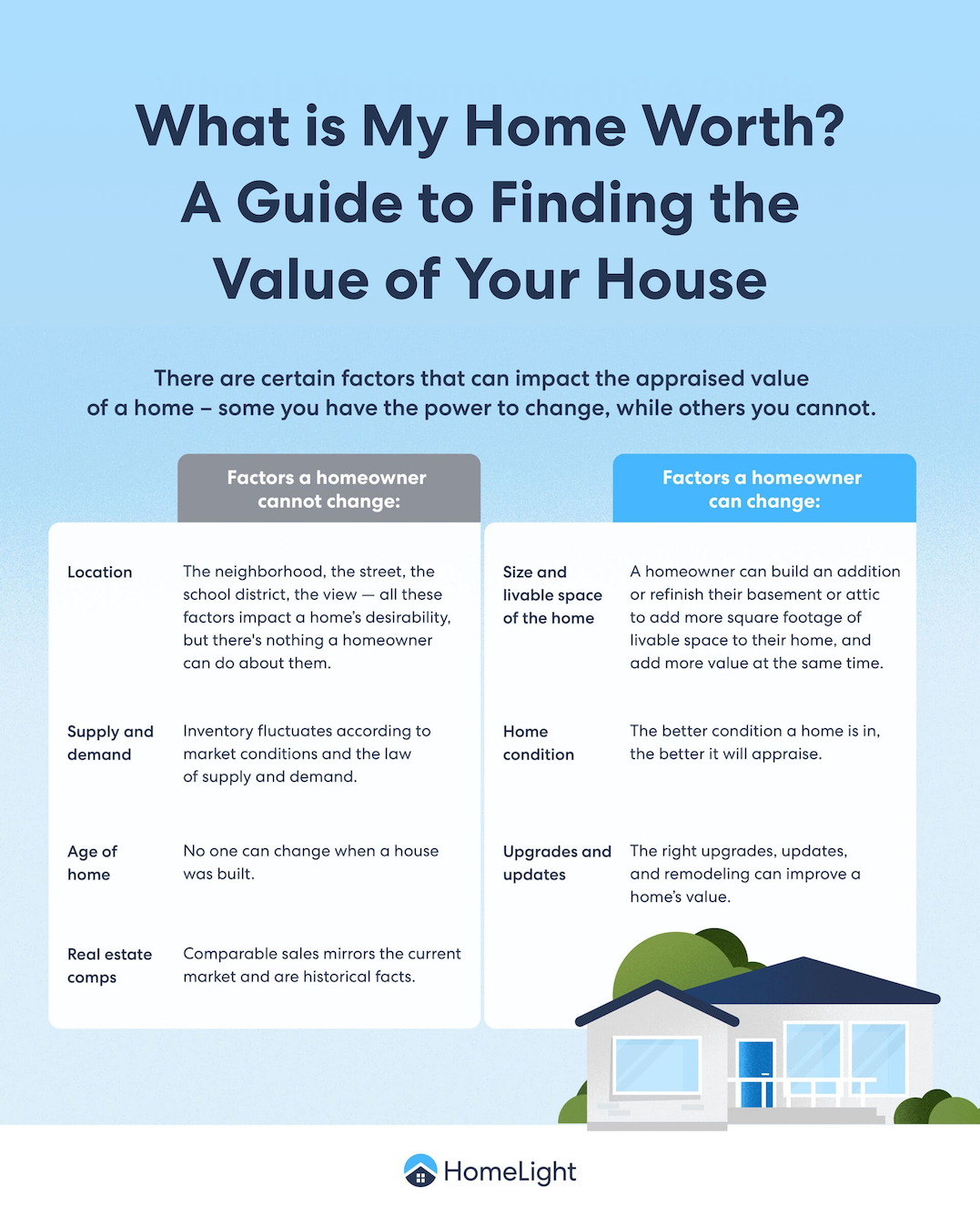

5. What factors impact appraised home value?

Some things increase your home’s value, while others hurt your home’s value. There are things on both those lists that cannot be changed, but there are also things on both lists that can be.

Factors that you cannot change

- Location: The neighborhood, the street, the school district, the view — all these factors impact your home’s desirability, but there’s nothing you can do about them. According to the University of Washington’s research, homes adjacent to nature parks and open spaces have an 8%-20% higher value than comparable properties. Data from the National Association of Realtors (NAR) reveals that 16% of recent homebuyers, with 34% of homebuyers aged 35-44, were influenced by the quality of their school district when looking for a new home.

- Supply and demand: Inventory fluctuates according to market conditions and the law of supply and demand. When supply is low and demand is high, your home’s value will increase. Conversely, when supply is plentiful and demand is low, your home’s value will decrease.

- Home’s age: Everything ages. You can’t change when your house was built. In some cases, an older home can be worth more, due to architectural details lacking in new construction. Its condition is often more important than age.

- Real estate comps: Comparable sales mirror the current market and are historical facts. But because most real estate agents prefer comps no older than six months, it’s a moving target, and as the market fluctuates, so do the comps, reflecting on your home’s value at any given time.

Factors that you can change

- Size and livable space: You can build another story or room, or refinish your basement or attic to expand your home’s square footage of livable space, adding more value to the property. Be aware that basement square footage doesn’t add as much value as above-ground spaces and may not be included in your home’s overall square footage. Adding an accessory dwelling unit (ADU) or mother-in-law suite may increase the value of a home by as much as 38%.

- Home’s condition: The better condition your home is in, the better it will appraise. Home appraisers rate your home’s condition based on the amount and degree of repairs required. However, due to limited supply and peak demand, Carroll says the condition is not as “prevalent” as it was five or six years ago.

- Upgrades and updates: The right upgrades, updates, and remodeling can improve your home’s value. For example, well-landscaped homes are worth up to 7% more. Even minor updates like new fixtures and paint can add to your home’s value.

6. Does a messy house affect an appraisal?

Technically, decor, moveable items, and cleanliness aren’t supposed to impact an appraiser’s assessment of your home. Human nature, however, intervenes.

Messy, dirty, or cluttered homes can impart an “I don’t care” attitude and lead an appraiser to wonder if the home has been properly maintained. Cases of extreme clutter can hinder an appraiser’s access, affecting the appraisal results negatively.

But it all depends on the market, Carroll says. In a seller’s market, it’s not as important as it is in a buyer’s market.

If I list a home for $300,000 that sells for $320,000, the comp has just gone up, even if the home appraised at only $275,000.

7. What makes property values go up or down in any given time period?

As mentioned, property values fluctuate over time. There are several reasons for this, including:

- Zoning regulations: Zoning regulations are municipal laws defining permitted uses for each area. Typical zoning use is divided into residential, commercial, agricultural, and industrial, but can also be mixed. In addition, zoning ordinances can limit building height, restrict sound, and impose many other regulations, including home density. Zoning restrictions can impact a buyer’s decision.

- Interest rates: The rates borrowers pay to finance a home loan rise and fall. When interest rates fall, buyers are able to borrow more money, and home prices also tend to rise. When interest rates rise, buying power decreases, and home prices typically slow their growth or fall.

- Overall state of the economy: The general health of the economy affects real estate value. The economy is measured by economic indicators such as the gross domestic product, employment data, manufacturing activity, and the price of goods. Typically, when the economy is slow, the real estate market is as well and causes home values to drop, whereas economic growth boosts home values.

- Supply chain and material costs: The rising cost and limited supply of lumber, steel, aluminum, and other construction materials drive up housing costs.

- Politics: Politics can impact the economy, particularly if the government stimulates the consumer climate. This could be in the form of legislative action to lower interest rates or tax incentives. Sometimes, the political leanings of a geographic region can impact the value of real estate.

- Disasters: Whether natural, like a hurricane or tornado, or man-made, like many fires, disasters can impact the value of the unaffected properties as a result of a decrease in supply and an increase in demand from displaced homeowners. Additionally, some sellers make improvements to their homes after a disaster, which can increase their homes’ value.

- Bidding wars: In a seller’s market, where demand exceeds supply, buyers may bid higher than the list price to win the property. “If I list a home for $300,000 that sells for $320,000, the comp has just gone up,” Carroll explains, “even if the home appraised at only $275,000.” Conversely, in a buyer’s market, where homes are plentiful and demand is low, buyers have more negotiating power, which can push home values down.

8. Are home appraisals public record?

In general, home appraisals are not public record. However, some portions of an FHA appraisal are released to an FHA website and may be accessed for up to six months.

In many states, public records will reveal limited information, such as recent sales prices, number of beds and baths, and square footage. However, there are a handful of non-disclosure states in which no information is made public.

In non-disclosure states, sale prices in a real estate transaction are not disclosed or recorded as public record, whether to protect the homeowner’s privacy or the value of the industry’s multiple listing service (MLS).

However, the National Association of Realtors explains on its website that non-disclosure states “cannot withhold sold data from MLS data feeds.” The restrictions on disclosing this data relate only to the public display of information.

When it’s difficult to assess a home’s value with anything but an appraisal, it usually leads to under-valued homes.

9. What will my house be worth in 5 years?

Carroll likes to say that you never lose in real estate if you hold onto property long-term. Depending on your goals, however, you could lose money if you buy or sell at the wrong time.

Being able to predict your home’s value in five years can help you plan. You can start by consulting the Federal Housing Finance Agency FHFA HPI Calculator to get an idea of what a home previously purchased would sell for today. It takes into consideration the average rate of appreciation of all homes in the area.

The easy-to-use calculator asks you to input your state, the quarter and year you purchased the property, and the original purchase price. It then calculates how your home’s value has increased over the timeframe by referencing appreciation trends for the area.

It’s a ballpark figure. For a truly accurate assessment, ask an experienced agent to provide an opinion that takes into consideration specifics about your property and developments in the neighborhood.

10. What will my house be worth in 10 years?

Historically, median home values have seen a steady price growth increase since the 1960s. Carroll mentions what real estate agents call a “seven-to-ten-year swing,” which refers to the typical housing cycle where prices rise for several years, peak, then cool or decline before beginning another upswing. “I’ve talked to economists; the predictions have been accurate.”

Until COVID-19, that is. The U.S. housing market exceeded the ten-year upswing, in part due to the COVID effect and its ripples in the supply chain. “Once the pandemic hit,” Carroll recalls, “we thought it was [the beginning of] the downturn. But it didn’t happen.”

The housing market took off during the pandemic, but by 2024 to 2025, things started to cool down. Mortgage rates have been hovering around the 6% to 7% range, price growth has slowed to modest gains, and while more homes are hitting the market, inventory is still tight. In a market like this, Carroll advises clients to “strategically think of where you want to be” and try to gauge the market’s future.

Looking at the general trend of America’s home price history can help predict potential trends 10 years in the future. However, even this extensive historical data cannot account for unexpected dips and surges in the market.

Find Your Perfect Real Estate Agent

We analyze over 27 million transactions and thousands of reviews to determine which agent is best for you based on your needs.

The best equation to estimate the value of your home

Whether you’re just curious about your home’s value or need an estimate for something more urgent, like refinancing, applying for a home equity loan, checking your property taxes, planning an estate, settling assets, or going through a divorce, you can get a rough idea using an online valuation tool. However, note that AVMs don’t consider upgrades or improvements to your home or neighborhood, which diminishes their accuracy.

HomeLight’s Home Value Estimator can be your convenient starting point for a free valuation. For a better idea of your home’s value, HomeLight’s HVE can direct you to a local top real estate agent, who can provide an even better estimate by preparing a CMA that presents a very accurate snapshot of your home’s value.

You can try to do the legwork yourself by consulting public records, but an experienced agent will have more knowledge about the neighborhood and properties in general, not to mention greater access to other sources of information, such as the MLS.

For the most accurate estimate of your home’s value, order an appraisal. An independent professional appraiser can provide the most precise evaluation of what your home is worth.

Header Image Source: (Jonnelle Yankovich / Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.