15 Steps to Buying a House in California

- Published on

- 15 min read

-

Steph Mickelson, Contributing AuthorClose

Steph Mickelson Contributing Author

Steph Mickelson, Contributing AuthorClose

Steph Mickelson Contributing AuthorSteph Mickelson is a freelance writer based in Northwest Wisconsin who specializes in real estate, building materials, and design. She has a Master's degree in Secondary Education and uses her teaching experience to educate and guide readers. When she's not writing, she can be found juggling kids and coffee.

-

Fran Metz, Contributing EditorClose

Fran Metz Contributing Editor

Fran Metz is a freelance content writer, editor, blogger and traveler based in Las Vegas, Nevada. She has seven years of experience in print journalism, working at newspapers from coast to coast. She has a BA in Mass Communications from Fort Lewis College in Durango, Colorado, and lived in Arvada for 15 years, where she gained her experience with the ever-changing real estate market. In her free time, she enjoys 4-wheeling, fishing, and creating digital art.

With 39 million people who call the Golden State home, California is the most populous state in the US and ranks third in total area behind Alaska and Texas. With this in mind, buying a house in California can feel overwhelming. With so many people and rising home prices, it can be downright intimidating.

But, it doesn’t have to be! We’re here to walk you through our 15-step guide for buying a home in California. With the help of Daniel Del Real, a top agent in Modesto, California, who works with 75% more single-family homes than the average Modesto agent, we’ll give you the information you need to purchase your dream home and succeed as a California homebuyer.

Find a Top Agent To Help You Buy Your California Dream Home

If you are looking to buy a home in California, a buyer’s agent is a necessary partner. Find a top agent in just a few minutes to jump-start your homebuying journey.

Make sure you buy within your means, [but] if the right property comes along and it’s the one that you really want and it’s the neighborhood that you need within your price point, then you go for it!

1. Assess your financial situation and future goals

We can’t always predict what the future holds — let’s be honest, we probably didn’t see ourselves locked down because of a pandemic or foresee the crazy real estate market that followed.

As of 2024, California’s real estate market is showing signs of growth, with home prices expected to rise by 6.8% in 2025, bringing the median price to about $869,500. While home prices have recently experienced some fluctuation, the combination of easing mortgage rates and an increasing supply of homes for sale suggests a potential increase in home sales. This could be an ideal time for buyers entering the market after a period of high competition.

To get started on evaluating your financial situation, take a look at your credit score and determine where it lands on the scale between poor and excellent. Typically, the better the score, the greater your chances of qualifying for an affordable mortgage. If you find that your score could use some improvement, consider disputing any errors on your credit report, paying down some of your debt, or settling any accounts that are in collections.

Del Real says it’s important to understand the reason you’re buying a home — to gain needed space, as an investment, or with future needs in mind — and to “make sure you buy within your means.” But, he adds, “If the right property comes along and it’s the one that you really want and it’s the neighborhood that you need within your price point, then you go for it!”

2. Determine how much you can afford

Living in California can be pricey. Determining what you can afford in California is a bit more complex than in other states due to factors like higher homeowners insurance rates and special assessments, like Mello-Roos districts. Despite these challenges, California buyers can take advantage of down payment assistance and first-time homebuyer programs that help make owning a home more achievable. With the right resources, your California dream home may be closer than you think.

A great place to start is with an affordability calculator, like this one from HomeLight. You can enter details such as your income, credit score, zip code, and down payment amount to get an estimate of what you might be able to afford.

3. Research special programs for down payment assistance

There are organizations in California that offer down payment assistance and first-time homebuyer programs to help make the dream of owning a home a reality. These are often loans in the form of a second mortgage with their own interest rates and payback requirements. Some programs available to low-to-moderate income homebuyers and first-time homebuyers include:

Golden State Finance Authority (GSFA)

- GSFA Platinum® Down Payment Assistance Program — Down payment and closing cost assistance up to 5% of the mortgage loan amount.

CalHFA

- MyHome Assistance Program — This is a program for government loans and for conventional loans that offers deferred-payment junior loans for 3.5% and 3% respectively to help with the down payment and closing costs.

City-specific options

- To find out if your specific city has affordable housing options or programs, you can contact your city directly.

Note: Individual program details frequently change. Please visit a company’s website for the most up-to-date information. Not all lenders offer these programs, and in some cases, a lender will need to be specifically approved to offer them.

4. Shop for a mortgage and get preapproved

When you start buying a home in California, getting preapproved for a mortgage is a smart move — it’ll show you how much you can actually borrow. But don’t just settle on the first lender you find. Shop around for both different lenders and mortgage types to see what works best for your situation. There are a lot of options, and finding the right fit can make a huge difference. Here are some loan types you might want to check out:

Conventional loan

There are two types of conventional loans — conforming and non-conforming. A conforming conventional loan will meet or exceed the guidelines set by Fannie Mae and Freddie Mac which are government-sponsored enterprises (GSEs) that purchase conventional loans. Guidelines for a non-conforming loan will vary more widely depending on the lender.

Typical requirements for a conventional loan may include:

- Credit score: A minimum score of 620 is typically required, though a higher score may improve your chances of securing better rates.

- Debt-to-income (DTI) ratio: The maximum allowed generally is 43%, but some lenders may accept slightly higher ratios with compensating factors.

- Down payment: The minimum often is 5%, but there are some programs that allow as little as 3% down, especially for first-time homebuyers.

- Loan limits: The standard conforming loan limit is $647,200 in most California counties, with higher limits in areas considered high-cost, topping $970,800 in certain counties.

- Private mortgage insurance (PMI): If the down payment is less than 20%, PMI typically is required to protect the lender.

Jumbo loans

Jumbo loans are used when the loan amount exceeds the conforming loan limits, which generally is $766,550 in most counties and up to $1,149,825 in high-cost areas, including counties like Los Angeles, Marin, Orange, San Benito, and San Francisco. The loan limits are reviewed and adjusted each year, based on changes in the housing market and county-specific conditions. Jumbo loans are especially common in California, where home prices often exceed these limits.

Typical guidelines for a jumbo loan might include:

- Minimum credit score: Generally about 700, but many lenders may require a score of 720 or higher, depending on the size of the loan and the borrower’s financial situation.

- Debt-to-income (DTI) ratio: Lenders typically prefer a low DTI, often about 36%, though some may accept up to 43% in certain cases.

- Down payment: A 20% down payment is common, though some programs may allow less if other conditions are met.

FHA

An FHA loan is insured by the Federal Housing Administration and available from FHA-approved lenders. An FHA loan is unique in that borrowers are able to use a down payment assistance program for the entire down payment. Requirements to qualify for an FHA loan may include:

- Credit score: A minimum credit score of 580 is required for a 3.5% down payment. For borrowers with a credit score between 500-579, a 10% down payment is needed.

- Upfront mortgage insurance premium (UFMIP): FHA loans require an upfront mortgage insurance premium, which typically is 1.75% of the loan amount. This is often rolled into the loan balance.

- Mortgage insurance premium (MIP): Borrowers also will pay a monthly MIP for the life of the loan unless they put down at least 10%, in which case MIP will be removed after 11 years. If the down payment is less than 10%, the MIP stays for the entire loan term.

- Debt-to-income (DTI) ratio: The FHA typically requires a DTI ratio of 43% or lower, although some lenders may accept higher ratios with compensating factors.

- Primary residence: FHA loans are available only for homes that will be used as the borrower’s primary residence.

Veterans Affairs (VA)

VA loans are available to eligible service members, veterans, and certain surviving spouses. There are two types of VA loans: the rare VA direct home loan and the more common VA-backed home loan. Here’s what you need to know about the requirements:

Eligibility: VA loans are open to service members, veterans, and eligible surviving spouses. Specific eligibility criteria vary by service length and type of discharge, and can be verified through the VA or a Certificate of Eligibility (COE).

- Types of VA loans:

VA direct home loans: These loans come directly from the VA, but they are less common.

VA-backed home loans: These are provided by approved lenders and are backed by the VA, offering advantages like no down payment and no private mortgage insurance (PMI).

- Credit score: While the VA doesn’t set a minimum credit score, lenders typically require one in the 620 to 640 range, depending on the loan and lender.

- Down payment: In most cases, no down payment is required, which makes VA loans a top choice for eligible veterans and service members. However, higher loan amounts may require a down payment.

- VA funding fee: Borrowers usually need to pay a funding fee between 1.25% and 2.15% of the loan amount. This fee helps sustain the program and can be rolled into the loan.

The main draw of VA loans is the ability to buy a home without a down payment and without the added cost of PMI, making them an ideal option for qualified veterans and service members.

CalHFA

The California Housing Finance Agency (CalHFA) has approved lenders that can qualify first-time homebuyers for a variety of home loans. Loans are approved based on:

- Credit, income limits, and other loan requirements from the CalHFA lender

- The home must be the borrower’s primary residence

- Completion of homebuyer education counseling

Once you’ve completed your mortgage application — which might only take you as long as it takes to gather all of the documentation that’s needed to verify income, debt, and assets — you can be preapproved for a mortgage in as little as one business day.

At this stage, you should go for preapproval instead of just prequalification. Prequalification is fast and gives you a rough idea of what you might qualify for, but preapproval means the lender takes a closer look at your financials to figure out exactly what you can borrow. Keep in mind, even with underwritten preapproval, you could still be denied a loan later in the process if your financial situation changes.

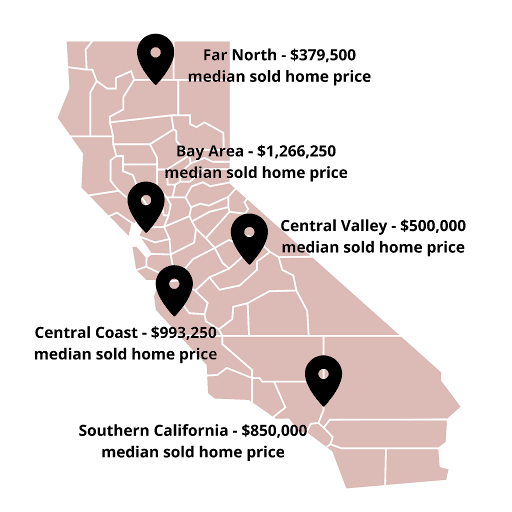

5. Research the market

When exploring the California housing market in 2025, it’s important to consider factors like median home prices, average days on market, location-specific features, schools, and potential risks such as wildfires and earthquakes. Let’s dive into some key areas in California, along with their current median home prices and average days on market, based on the latest data from the California Association of Realtors® and other sources.

Southern California

- Median sold price of existing single-family homes: $850,000

- Median days on market (average of all counties): 37

- Counties include: Riverside, San Bernardino, Los Angeles, Orange, San Diego, Ventura, Imperial

Central Coast

- Median sold price of existing single-family homes: $993,250

- Median days on market (average of all counties): 52

- Counties include: Monterey, San Luis Obispo, Santa Barbara, Santa Cruz

Central Valley

- Median sold price of existing single-family homes: $500,000

- Median days on market (average of all counties): 57

- Counties include: Merced, Sacramento, San Joaquin, Placer, San Benito, Stanislaus, Kings, Madera, Fresno, Kern, Glenn, Tulare

Bay Area

- Median sold price of existing single-family homes: $1,266,250

- Median days on market (average of all counties): 50

- Counties include: Alameda, Contra Costa, Napa, San Mateo, Solano, Sonoma, Marin, San Francisco, Santa Clara

Far North

- Median sold price of existing single-family homes: $379,500

- Median days on market (average of all counties): 63

- Counties include: Butte, Lassen, Plumas, Siskiyou, Shasta, Tehama, Trinity

6. Find a local agent

Working with a local agent who is very familiar with the market in your target area is the key to a successful homebuying experience in California.

Del Real suggests finding someone who will “coach you on a micro level about specific neighborhoods.” Buying a home is a huge investment, so having someone who is able to be honest and explain what you could expect in the future is important.

A good real estate agent will walk you through the process, explaining what is happening — and why. They will communicate with you in a way that you’re comfortable with — whether you need straight talk or a little sugar coating — and keep you in the loop along the way.

It’s important to do your due diligence when deciding which agent to hire. Here are a few things to look for:

- Experience with your home type and budget: Ensure the agent has experience working with properties in your price range and the specific type of home you’re seeking. This ensures they have the right skills and knowledge to navigate your needs.

- Client feedback: Take the time to read agent reviews and testimonials from past clients. Look for patterns in their feedback — are the reviews mostly positive? Does the agent seem like someone you’d feel comfortable working with during this important process?

- Personal rapport: Never underestimate the value of a good connection. Homebuying is a big decision, and you’ll want an agent who understands the emotional highs and lows of the process, as well as the practical details. A strong personal rapport can make all the difference in navigating this journey smoothly.

7. Start the house hunt in earnest

Let’s be honest, if you’re looking for a new home, you’ve probably been scouring online home listings for a while. Well, now it’s time to get down to business, narrow down your list, and start going to open houses and scheduling showings.

Make a list of your “need to haves” and “nice to haves.” The clearer you are on what you need, the easier the process will be. For instance, if you have three kids, a one-bedroom home probably isn’t going to cut it, but you may be able to compromise on the size of the kitchen or number of bathrooms.

In this market, even though it’s showing signs of cooling off a bit, you may not get exactly what you want. So it’s important to know where you’re willing to compromise and where you need to stand firm.

Your agent will help you navigate available homes and help you decide when or if you need to settle. Del Real says we’re moving out of the period when people had to settle for a home when inventory was low but they were still getting an amazing interest rate. Now, he says, “In a way, you’re settling on [rates], but you get a selection of homes.”

When choosing a neighborhood or city for your new home, it’s important to think about potential risks like earthquakes, floods, fires, and tsunamis. The MyHazards website is super helpful — just type in an address and check out the specific risks in that area. Also, make sure to go over the seller’s disclosure carefully. It’s worth taking your time to make sure you know about any possible issues with the property before moving ahead.

8. Make a strong offer

Once you’ve found the right California home, the next step is to make an offer. With the current market conditions, homes may stay on the market longer, but it’s still important to act promptly. Depending on the area, you may want to move quickly to avoid losing out, especially if you’re in a competitive market.

There are a few things you can do to make your offer more appealing to a seller — and it’s not all about price. Sure, offering above asking is one strategy, but your agent can guide you through what makes the most sense, depending on the market.

In today’s market, strengthening your offer depends on the situation. If you’re in a competitive market, reducing or eliminating contingencies, increasing your earnest money, or making cash offers to bypass financing contingencies can make your offer stand out. In a slower market, where there’s more supply and less demand, you have more flexibility to include contingencies and negotiate a lower price.

Del Real notes that he sees more sellers in California accepting VA or CalHFA loans than he has in the past few years. As the market slows down, he says that sellers are more willing to consider buyers with these types of financing.

If you’re looking to negotiate on the purchase price, Del Real suggests having the seller give credits that will allow you to pay for mortgage discount points, effectively lowering your interest rate and saving you money over the life of the loan. Del Real suggests finding a seller “that’s willing to give you a 2% credit to buy down your rate.” This allows the buyer to make a higher offer while potentially paying less over the life of the loan.

9. Send your earnest money deposit

The earnest money deposit typically is between 1% and 3% of the purchase price, though it can vary depending on the market and location. In a competitive market, offering a higher earnest money deposit can help make your offer stand out and show the seller you’re serious. But it’s important to understand that if you back out of the deal for reasons not specified in the contract, the seller could keep your earnest money. On the other hand, if contingencies — such as inspection or financing — aren’t met, you may be able to get the earnest money back. Always be sure to review the terms of your contract to know your rights.

10. Order an inspection and get an appraisal

Although it’s not required by law to have a home inspection before buying a property, it’s always a smart move to get one, in addition to the appraisal your lender will arrange. A home inspection can help uncover potential issues that may not be obvious, giving you peace of mind before moving forward with the purchase.

During the home inspection, a licensed inspector will check for visible damage or issues throughout the home. They will examine the structure, plumbing, HVAC system, and more. They won’t, however, be paying attention to the decor, paint color, or other aesthetics.

Depending on the location and specific characteristics of the home, you may need to arrange for specialized inspections, such as for termites or other pests, sewer systems, chimneys (especially if the standard inspection raises concerns), and radon. These additional inspections can help identify issues that may not be covered in the general inspection but are important for your peace of mind.

Your mortgage lender will order an appraisal to determine the value of the home and see if your purchase price lines up with the appraised value of the home.

11. Shop for homeowners and specialty hazard insurance

Homeowners insurance in California averages about $1,480 annually — but that doesn’t include specialty hazard insurance.

While standard homeowners insurance might cover damages that result from wildfires, if you are in a high-risk area, it may be difficult to obtain an insurance policy. If you have trouble getting a standard insurance policy, the California FAIR Plan will provide basic fire coverage, and the Difference in Conditions (DIC) policies complement the FAIR Plan policy to provide coverage similar to traditional homeowners policies. The best way to determine the cost of a policy is to enter the home’s address in the FAIR Plan Dwelling Premium Calculator and then work with a broker to get a quote for coverage.

For earthquake coverage, you can price out policies with the California Earthquake Authority to find a cost estimate and then talk with your home insurance company. The average cost of earthquake insurance varies by city, with Alameda costing $6.47 per thousand dollars of coverage which equals a yearly premium of $3,233 on a $500,000 home, and Fair Oaks costing $2.46 per thousand dollars of coverage which equals a yearly premium of $1,230.

12. Negotiate repairs

If the inspection reveals issues with the home, you may want to go back to the seller to negotiate repairs or request credits toward repairs before closing. In California’s recent competitive market, sellers have often declined repair requests. However, as the market shifts and cools, even slightly, sellers may become more open to negotiations and compromise.

13. Order a title search

A title company will issue a preliminary title report that will be reviewed by all parties, including your lender, and will include items such as property tax information, easements, CC&Rs, deeds, deed restrictions, liens, and any judgments against the title of the home. All of this is done to confirm that the seller has the legal right to sell the property and that the title is “marketable,” meaning it’s clear of any legal issues that could affect the transfer of ownership.

Before they can sell, the seller will have to take care of any liens, encumbrances, or judgments against the property so you can legally take ownership once the sale is finalized.

14. Final walkthrough

The final walkthrough is your opportunity to inspect the property one last time. It’s the moment to confirm that all agreed-upon repairs have been made and that the home is in good condition before you sign the closing papers and officially take possession of your new home.

15. Close on your new home

On the scheduled date, you’ll meet with a notary to sign your final loan and closing documents from escrow. You’ll then wire or provide a cashier’s check for your down payment and closing costs to escrow. Your lender also will send their portion of the funds to escrow. Once everything is disbursed, the deed and note will be recorded with the county. Finally, you’ll receive the keys to your new home!

Know the market and work with an agent

The best way to buy a house in California is to educate yourself about the market, and our simplified 15-step guide is a great start. Home prices in California are high, but buying a home, according to Del Real, “lets you secure your lifestyle, have the pride of ownership, build memories with your kids, and control the school district your kids go to and the neighborhood that you want to live in.”

Partnering with a knowledgeable California agent is essential for a smooth homebuying experience. Our Agent Matching Tool connects you with top agents in your area, helping you find the perfect fit to guide you through your California home buying journey.

Writer Madeline Sheen contributed to this post.

Header Image Source: (Paul Hanaoka / Unsplash)

- "C.A.R. releases its 2025 California Housing Market Forecast," California Association of Realtors® (September 2024)

- "Conventional loans," Consumer Financial Protection Bureau

- "Conventional loan requirements for 2024," The Mortgage Reports, Barbara Ballinger (January 2024)

- "What is mortgage insurance and how does it work?," Consumer Financial Protection Bureau (May 2024)

- "Eligibility requirements for VA home loan programs," U.S. Department of Veterans Affairs (April 20242)

- "Average homeowners insurance cost in November 2024," Bankrate, Natalie Todoroff (November 2024)

- "How Much Does Earthquake Insurance Cost in California?," Value Penguin, Lindsay Bishop (August 2023)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.