Can I Avoid Foreclosure and Sell My House in Maryland?

- Published on

- 13 min read

-

Cheyenne Wiseman Associate EditorClose

Cheyenne Wiseman Associate Editor

Cheyenne Wiseman Associate EditorClose

Cheyenne Wiseman Associate EditorCheyenne Wiseman is an Associate Editor at HomeLight.com. Previously, she worked as a writer for Static Media (Mashed.com and Chowhound.com) and as an editor for CBR.com. Cheyenne holds a bachelor’s degree in English from UC Davis, where she also founded and led a literary magazine called Open Ceilings. She has four years of experience writing and editing on topics including real estate, financial advising, and pharmaceuticals.

If you’re a Maryland homeowner facing foreclosure, the situation can feel frightening and overwhelming, especially when deadlines are approaching. You may be asking yourself, “Can I avoid foreclosure and sell my house in Maryland?” In many cases, the answer is yes.

Homeowners in Maryland can often sell their property before the foreclosure process is finalized. The key is understanding how Maryland’s foreclosure rules work, how much time you may have, and which selling option best fits your circumstances.

Below, we’ll explain what the foreclosure process looks like in Maryland, how long it typically takes, and whether selling before the auction date could help you avoid long-term financial consequences.

Sell Your House Fast in Maryland With a Cash Offer

Get an all-cash, no-obligation offer through HomeLight’s Simple Sale platform whenever you’re ready. Receive your offer in 24 hours and close in as few as 7 days. No showings, no repairs, no open houses. Available to sellers throughout Maryland.

According to data from ATTOM, approximately 300,000 foreclosures occur in the U.S. each year, and that number is on the rise. Based on an end-of-year report, the statewide foreclosure rate in Maryland is 1 in every 2,430 housing units. That’s roughly a 76% year-over-year increase.

Can I avoid foreclosure and sell my house in Maryland?

In most scenarios, you can sell your Maryland home while it’s in foreclosure, as long as the foreclosure sale has not yet taken place.

You may be surprised to learn that homeowners retain ownership of the property throughout most of the foreclosure process. That means you generally have the right to sell the home, pay off the loan, and stop the foreclosure before the final auction date.

“Many homeowners assume that once foreclosure starts, their options disappear. In reality, there is often still an opportunity to sell, protect equity, and minimize long-term financial damage,” says Steven Powell, a top-performing Maryland real estate agent with 26 years of experience.

“The most important step is having a conversation early. The sooner a homeowner understands their timeline and options, the more control they keep over the outcome.”

In other words, the earlier you act, the more flexibility you typically have when it comes to pricing, potential buyers, and the final outcome.

How foreclosure works in Maryland

Maryland primarily uses a quasi-judicial foreclosure process. This means the foreclosure does not begin with a traditional lawsuit, but the process still involves limited court oversight once it starts.

“One major misconception is that foreclosure happens immediately after a missed payment. In Maryland, the process takes time and involves legal notices and filings before a foreclosure sale can occur,” Powell says.

In Maryland, foreclosure generally follows these steps:

- The homeowner falls behind on mortgage payments.

- The lender delivers a notice of intent to foreclose — at least 45 days before initiating the foreclosure.

- The lender files an “order to docket” with the court, kick-starting the foreclosure.

- The homeowner receives notice and may request mediation within 25 days.

- If the issue isn’t resolved, the lender arranges a public foreclosure auction and publishes notice of the sale.

- After the auction, the court must ratify the sale before ownership officially transfers.

In Maryland, the foreclosure process typically cannot begin until a homeowner has been in default for at least 90 days after the first missed payment. However, if the loan is covered by federal servicing rules, which most mortgages are, lenders generally must wait 120 days of delinquency before filing the foreclosure case. This waiting period is intended to give homeowners time to explore loss mitigation options such as loan modifications, repayment plans, or other alternatives before foreclosure moves forward.

Because the process runs through the courts, timelines can vary depending on the lender, the court’s schedule, and whether the homeowner contests the foreclosure.

How long does foreclosure take in Maryland?

Foreclosure timelines in Maryland can vary widely, but the process typically takes 6 to 9 months from the first missed payment to the foreclosure sale. On average, that equates to roughly 180 to 270 days once the foreclosure process is underway, although delays, mediation, or court scheduling can extend the timeline.

While this may sound like plenty of time, it’s important to remember that key deadlines, such as the auction date, can arrive quickly as the case moves forward.

“Generally, homeowners have a window of several months from the initial default until a foreclosure sale. However, once a sale date is scheduled, the timeline becomes firm and urgent. My advice is simple: don’t wait for the sale date — explore your options as soon as you receive formal notice,” Powell advises.

If you’ve already fallen behind on payments or started receiving legal notices, speaking with a local expert as soon as possible can help you understand how much time you may still have and what options remain, including selling the home before foreclosure begins.

What happens if you sell before foreclosure is finalized?

Selling your Maryland home before the foreclosure sale can halt the process and help you move forward with fewer long-term financial consequences. In a successful sale, the proceeds first go toward paying off the remaining mortgage balance, along with any interest, fees, or legal costs tied to the foreclosure. Once the loan is satisfied, the foreclosure action is usually dismissed.

Acting early can also help limit the damage to your credit compared with a completed foreclosure, which can remain on your credit report for years. If your home sells for more than what you owe, you may also be able to keep the remaining equity to help support your next move.

“A completed foreclosure typically remains on a credit report for years and can delay future homeownership. By selling beforehand, homeowners often maintain more control over their financial recovery,” says Powell.

If the expected sale price won’t fully cover the loan balance, a short sale may still be possible with lender approval, which is another reason to explore your options as soon as possible.

Option 1: Selling with a top Maryland real estate agent

In many cases, working with an experienced Maryland real estate agent is the best path for homeowners who still have enough time before foreclosure. This option gives you the best chance to maximize your sale price.

A knowledgeable local agent can:

- Set a competitive price based on current Maryland market trends

- Market the property widely to attract qualified buyers

- Negotiate with buyers and, if needed, coordinate with the lender on a short sale

- Keep the transaction moving to meet foreclosure-related deadlines

“Communication is critical — with the seller, title company, lender, and buyer — to ensure deadlines are met. Experience matters because timing, negotiation, and documentation must be handled precisely,” says Powell.

Because timing is so important, connecting with a proven agent quickly can make all the difference. HomeLight’s free Agent Match platform analyzes over 27 million transactions and thousands of reviews to determine which Maryland area agent is best for your situation. To get started now, enter a few details about your home and selling timeline.

A top Maryland agent will help you make informed decisions and avoid unnecessary delays.

How fast can you sell with an agent in Maryland?

The timeline for an agent-assisted sale in Maryland depends on pricing, property condition, location, and buyer demand. In Maryland, the average days on market (DOM) — from listing to signed contract — is about 29 days. However, a carefully priced, well-marketed home may attract strong interest within days.

In urgent situations, an experienced agent can often streamline the process and help sellers move as quickly as the market allows.

“In the Hagerstown and Washington County market, well-priced homes can move quickly, particularly in affordable price ranges where buyer activity is strong. Proper marketing and exposure are essential to compress the timeline,” Powell explains.

If your timeline is especially tight, you may also want to compare this traditional path with faster alternatives, such as selling for cash to a house-buying company or investor.

Consult With a Top-Performing Maryland Agent

Homelight’s free Agent Match platform can connect you with top-performing, trusted real estate agents in your Maryland market. Our data shows that the top 5% of agents sell homes more quickly and for up to 10% more than the average agent.

Option 2: Selling for cash to avoid foreclosure in Maryland

If your foreclosure timeline is especially tight, selling your Maryland home for cash may provide a quicker, more predictable path forward. Cash buyers — which can include individual investors or Maryland area house-buying companies — typically purchase homes in as-is condition. These companies can often close in a matter of days or weeks rather than months.

The main advantage of a cash sale is speed and certainty. With no buyer financing, fewer inspections, and limited contingencies, the transaction can often move quickly enough to stop a foreclosure before the auction date. The trade-off is that cash offers are typically lower than what you might receive through a traditional listing.

“If the property requires significant repairs, has little equity, or the foreclosure timeline is extremely tight, a cash offer may be appropriate. Investors can sometimes close faster and purchase ‘as is,’ which may help in very urgent situations,” Powell says.

How much will a Maryland house-buying company pay?

Use the Cash Offer Comparison Calculator below to get rough estimates of how a cash offer in Maryland might compare to an agent-assisted sale, depending on your selling method and whether you hire a top agent.

As you can see, your cash offer amount will be considerably higher if your Maryland home is in good condition. However, in a foreclosure situation, you may not have the time or money to tackle major repairs. If you’re facing an imminent financial need, the speed and convenience of a near-instant all-cash offer can’t be beat.

Examples of cash home buyers in Maryland

If you’re researching a fast sale, you might encounter local or regional “We Buy Houses”-style companies. These buyers generally focus on quick closings and minimal seller prep. A few examples in the Maryland area include:

- We Buy MD Homes, (see customer reviews)

- Credible Homebuyers, (see customer reviews)

- Revolutionary Home Buyers, (see customer reviews)

- Yes I Pay Cash, (see customer reviews)

Because each cash homebuyer company in Maryland uses its own pricing model, timelines, and contract terms, it’s a good idea to review multiple options and compare offers carefully before making a decision.

You’ll also want to carefully vet cash-for-home companies before making a commitment. However, there is a way to move forward quickly and know you’re working with an established, trustworthy cash buyer.

Selling your house through HomeLight’s Simple Sale

HomeLight’s Simple Sale platform connects you with the largest network of vetted cash buyers in the country, including trusted buyers in Maryland. With Simple Sale, you can receive a no-obligation cash offer in 24 hours and close in days, not months.

Through Simple Sale, Maryland homeowners can:

- Request a no-obligation all-cash offer

- Sell the home “as is,” without repairs or showings

- Choose a flexible closing timeline that fits their situation

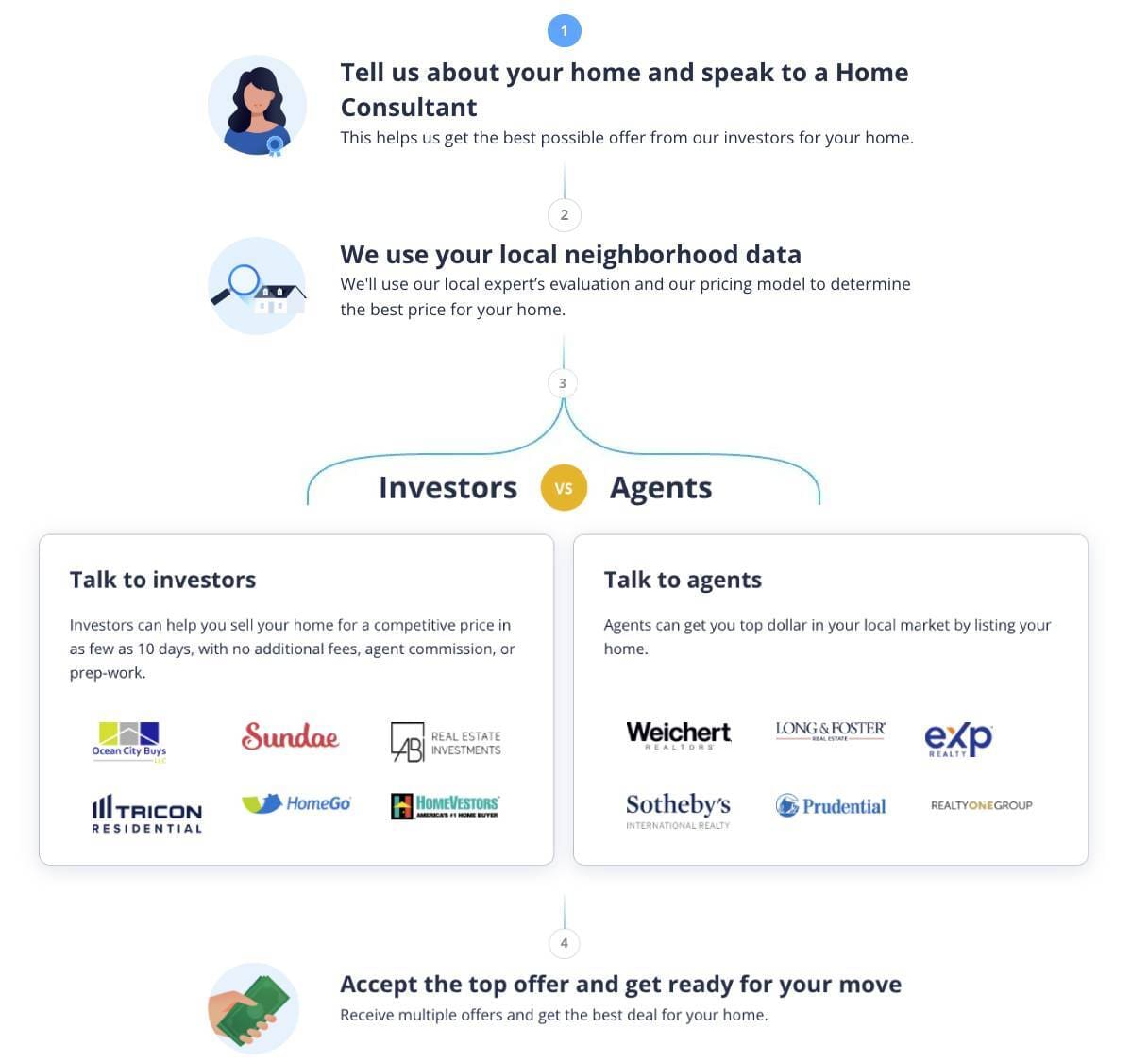

Here’s the four-step Simple Sale process:

HomeLight’s Simple Sale can provide cash offers for Maryland homes in almost any condition. To get started, fill out this short questionnaire.

Here are a few examples of what HomeLight customers are saying about Simple Sale:

Baohan Wu needed to sell his home fast. With HomeLight’s Simple Sale platform, Wu requested an all-cash offer and sold his home in about 24 days, from start to finish.

Hear Wu explain his experience with Simple Sale:

A fast, all-cash purchase offer isn’t right for every situation, but if you’re facing foreclosure in Maryland and would like a no-obligation cash offer, consider Simple Sale. You’ll also learn what a leading Maryland agent might be able to get for your home.

HomeLight maintains an A+ rating with the Better Business Bureau and has a 4.8-star customer review ranking on Google. You can read these and other HomeLight customer reviews at homelight.com/testimonials.

Which selling option is right for your situation in Maryland?

The best way to sell a Maryland home in foreclosure depends on your timeline, equity position, and financial priorities.

In general:

- Partnering with a Maryland agent may make sense if you still have time before foreclosure and want the strongest chance at a higher sale price.

- Pursuing a cash sale may be the better fit if speed, certainty, and avoiding the foreclosure auction are your top concerns.

Powell explains: “I encourage homeowners to compare net proceeds, timeline, and long-term financial impact — not just speed. A properly marketed listing often results in higher offers, even within compressed timelines. Cash buyers can be helpful in certain scenarios, but it’s important to understand what you’re giving up in price for convenience.”

Comparing both approaches side by side can help you move forward with clarity rather than urgency alone. “A trusted agent can help evaluate both paths objectively,” Powell adds.

Talk to a Maryland expert before the foreclosure clock runs out

If you’re asking, “Can I avoid foreclosure and sell my house in Maryland?” the good news is that you likely still have options. The sooner you explore your selling paths, the clearer your situation becomes. Even a brief conversation with a knowledgeable local professional can help you understand your timeline, estimate a potential sale price, and determine the next steps available to you.

HomeLight can connect you with a trusted Maryland agent through Agent Match or help you explore a fast cash offer through Simple Sale. With Simple Sale, you’ll also learn what a top agent might be able to get for your home, so you can compare both options and decide what direction feels right.

Foreclosure is a challenging situation, but with the right guidance and timely action, many Maryland homeowners can still sell, protect their financial future, and move on to what comes next.

Header Image Source: (spiroview/ Depositphotos)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.