How Top Agents Approach Writing a Comparative Market Analysis

- Published on

- 8 min read

-

Melissa Rudy Contributing AuthorClose

Melissa Rudy Contributing Author

Melissa Rudy Contributing AuthorClose

Melissa Rudy Contributing AuthorMelissa Rudy is a seasoned digital journalist with 15 years of experience writing web copy, blog posts and articles for a broad range of companies. When she can’t buy or sell homes, she settles for the next-best thing: researching and writing about all things real estate-related.

Your listing agent comes to you with a fairly thick package of paperwork and says: “Here’s the comparative market analysis (CMA) for your house — let’s talk about what we should sell it for.” For some sellers, a cursory glance through the pages may suffice before they move on to getting their house live on the market. However, others are more curious to know: How do you write a comparative market analysis? What goes into this process?

The standard Comparative Market Analysis can span over 30 pages long and be confusing to digest with such a dense mix of data, tables, and housing market jargon. So, we spoke with a couple of top agents in two different parts of the country to simplify it all for us. As we pulled back the curtain, it became clear that “writing” a comparative market analysis has a lot more to do with gathering the correct information and knowing how to analyze it than it does penning great prose.

Here we’ll break down the process of putting together a CMA into five basic steps:

- Do a deep dive into the subject property.

- Gather up your comps using a tight radius.

- Evaluate each comparable property individually.

- Look at overall market trends.

- Reconcile your findings.

With that overview in mind, we’ll now go through each part in further detail — letting the pros guide us!

1. Do a deep dive into the subject property.

You may have a baseline understanding of a CMA, but a quick refresher: A comparative market analysis is a tool that your listing agent will use to help determine the appropriate market value of your home. It pulls in a bunch of details about nearby properties of a similar size and style that have recently sold in your area, and uses their sale prices as a benchmark when setting your home’s list price.

Your home is the star of the CMA, so the document should start with a profile of the property. Rick Fuller, an experienced real estate agent in Contra Costa County, California, spends a lot of time studying the characteristics of the home being sold. “The more information we have on the property, the more likely we’ll arrive at the right price that aligns with the market value,” he says.

The CMA should include all of the key details about the property that could impact its value, such as:

- Address, community, and neighborhood

- Square footage and number of stories

- Property photos

- Age

- Number of bedrooms and bathrooms

- Location, accessibility, and parking

- Type of flooring

- Type of foundation

- Lot size and features

- Type of heating, cooling, and roofing systems

- Any renovations and upgrades

- Highlights and features (i.e, garage, finished lower level, great views, pool, fencing, security system, high-end finishes, etc.)

- Sales history and value adjustments over the years

2. Gather up your comps using a tight radius.

Once the agent has done due diligence on the focal property, it’s time to widen the scope to see how it measures up to the surrounding homes. That involves looking at sales comps, which are similar homes that have recently sold in the area.

Laurie Cappuccio, a top real estate agent in Reading, Massachusetts, has created hundreds of CMAs in her 24-year career. When gathering sales comps, she starts by looking at nearby homes that have sold in the past six months. To make sure she’s comparing apples to apples, she takes the time to fine-tune the list of properties so that they’re as similar as possible to the subject home.

How many comps should be included?

Cappuccio points out that the number of comparable properties she comes up with will depend on the time of year and the state of the market. “There is no fixed, set number of homes to include,” she says.

Fuller generally aims to have at least 20 total properties in his CMAs, split into four different categories:

- At least five active listings: Homes that are currently on the market

- At least five pending properties: Homes that are under contract but have not yet closed

- At least five sold properties: Homes that have recently closed

- At least five expired/withdrawn homes: Homes that were listed on the market, but were then removed without being sold

How close do the comps need to be?

Generally speaking, the closer the comps are to the subject property, the more accurate the CMA’s assessment will be. That said, the distance of the comps will vary by neighborhood. If the subject property is in a rural area or a community where houses have sprawling acreage, the comps may have to be several miles apart, Fuller explains. But for others, they may be located in the same subdivision.

The distance may also increase if the property has unique features that are tough to match. For example, Fuller sometimes has to look farther out to find homes that have a similar view, pool, lot size and orientation, design style, or some other specific characteristic.

3. Evaluate each comparable property individually.

After coming up with the high-level list of comps, the agent will do a deeper dive into each of the individual homes, including key information like:

- Photo and map of location

- List price and current estimated value

- Year built

- Number of bedrooms and bathrooms

- Square footage and lot size

- Garage information

- Information on roofing and HVAC systems

- Additional features (i.e., fireplace, pool, view, upgrades, etc.)

- School district

- Description/summary of the property

Most CMAs will include a chart with key features across multiple properties, making it easy to scan and compare.

4. Look at overall market trends.

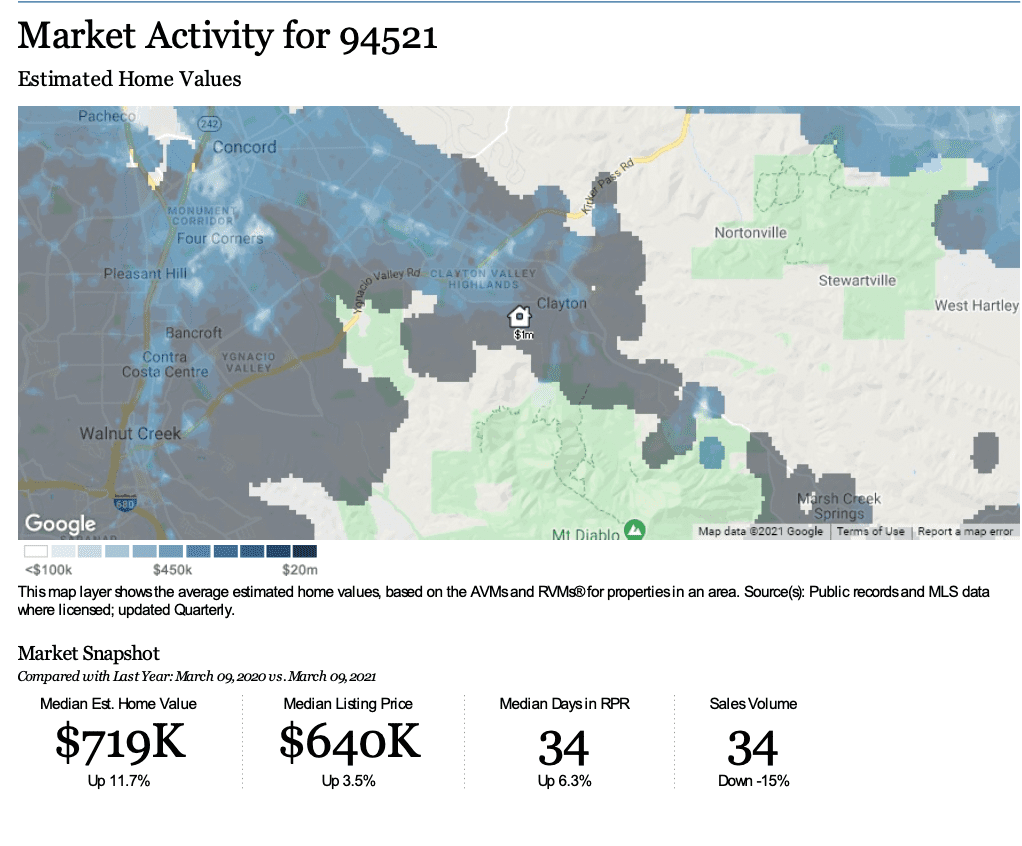

While it’s important to “zoom in” and research individual properties in the area, the CMA should also “zoom out” to look at an overall market snapshot of what’s happening sales-wise in the area. Fuller includes a color-coded map that shows how pricing fluctuates in different neighborhoods, and also presents the median estimated home value, the median listing price, the median number of days on the Realtors Property Resource (RPR), and the sales volume. This analysis provides a valuable context when determining the sales price of the subject property based on where it falls in the map.

The CMA should also look at other trends in the market, such as:

- List price vs. sales price

- Average price adjustments

- Median home value vs. median listing price

- Median sale price vs. sales volume

- Median listing price vs. listing volume

- Median sale price by square footage

- Price range of homes sold

- Age range of homes sold

5. Reconcile your findings.

After gathering all of the comparable properties (sold, active, pending, and withdrawn) and analyzing the market trends, Fuller moves on to the reconciliation stage, where he crunches the numbers to determine the trajectory of the real estate market.

“Are values going up or down? If they’re going up, we may set the price higher. If they’re going down, we may price it lower,” he explains.

Most of Fuller’s reconciliations end in a price range rather than a fixed number. “Most homeowners select a range based on condition, how quickly they need to sell, or outside circumstances like loan modifications, a short sale, or a pending foreclosure,” he says. “When we can list their property within a price range, that gives them some flexibility.”

Cappuccio doesn’t always include recommended pricing in her CMAs. Instead, she prefers to make it more of a conversation. “When I start my meeting, I ask the homeowner for their expectations of what their home is worth,” she says.

“We also talk about the importance of intelligent and realistic pricing. While their home may have great features, they need to realize that unless it’s a cash deal, it still has to appraise for the sale price.”

Should a homeowner consider doing their own CMA?

Do you need a real estate agent to create a CMA for you? Technically, you could cobble together your own DIY comps analysis by searching for recent home sales in your area, then creating a chart comparing all of the property details and features. You can also check out online tools, like HomeLight’s home value estimator, to plug in an address and find out the approximate value of a property.

That said, selling a house and transitioning to a new one isn’t exactly a low-stress life event — especially when juggling work, family, and other obligations. If you’ve got your hands full and time is in short supply, it can be a game-changer to have an experienced agent in your corner to crunch the numbers. Plus, with an agent’s experience in creating countless CMAs, they can likely do it faster and more accurately. In addition, an agent’s seamless access to MLS data helps them get a complete picture with all the necessary information more efficiently.

“Homeowners may try to guess at the value of their home by getting online estimates or talking to their neighbors, but those methods don’t take into account an assessment of market value,” says Fuller. “They can’t determine the home’s condition, upgrades, views, and market trends. Only the CMA can accurately do this.”

Header Image Source: (89stocker / Shutterstock)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.