What Is a Median Home Price?

- Published on

- 10 min read

-

Richard Haddad Executive EditorClose

Richard Haddad Executive Editor

Richard Haddad Executive EditorClose

Richard Haddad Executive EditorRichard Haddad is the executive editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

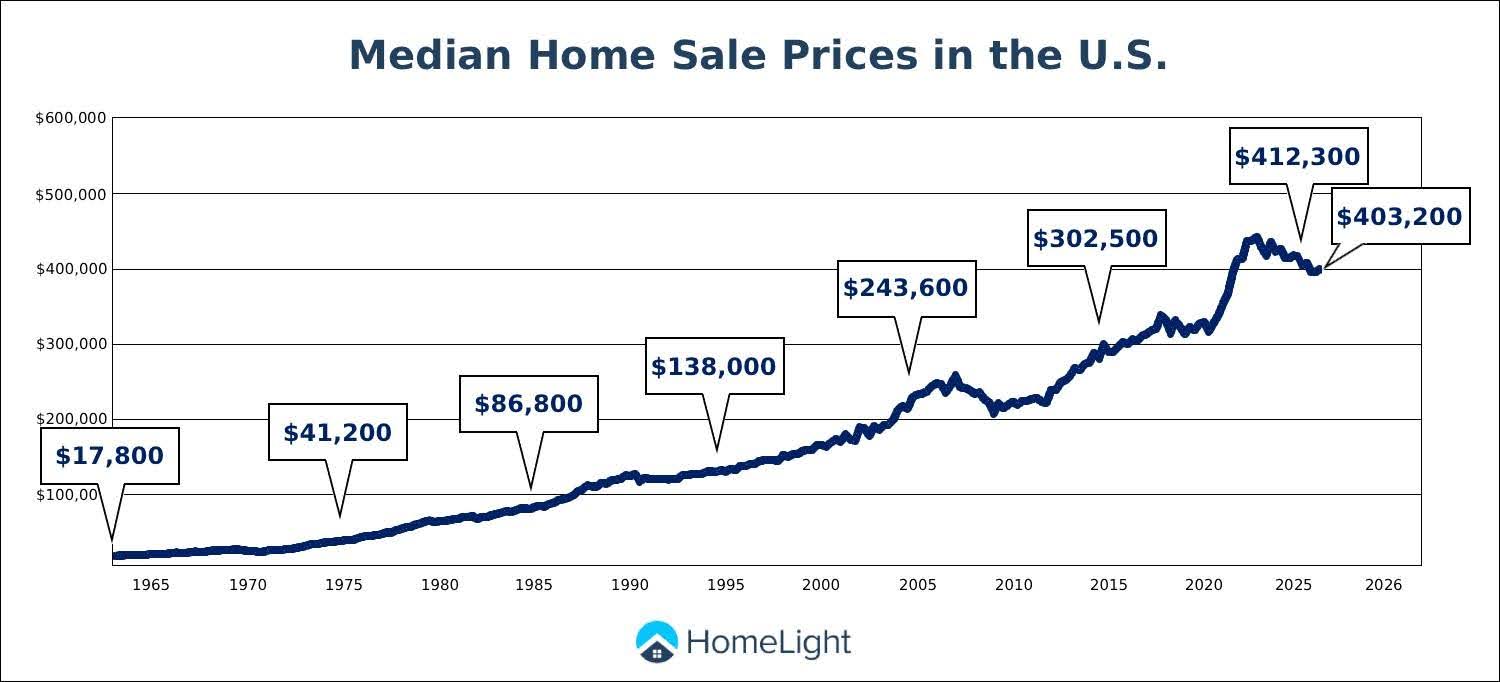

At the start of 2000, the median home price was about $165,300, and by 2025 it had risen to roughly $412,300. That’s not just a dollar increase. It means the typical home value has more than doubled over that period. In total, that’s an increase of about 149%, or around $247,000. When you look at it over time like that, it becomes clearer why many sellers ask, “What’s median home price?”

In this simple, easy-to-follow guide, we’ll break down what the median home price actually means and how people use it. We’ll also take a quick look at how it’s changed over time and give you a tool to help estimate what you could walk away with when you sell your home.

How Much Is Your Home Worth Now?

Home values have rapidly increased in recent years. How much is your current home worth now? Get a ballpark estimate from HomeLight’s free Home Value Estimator.

What is the median home price metric?

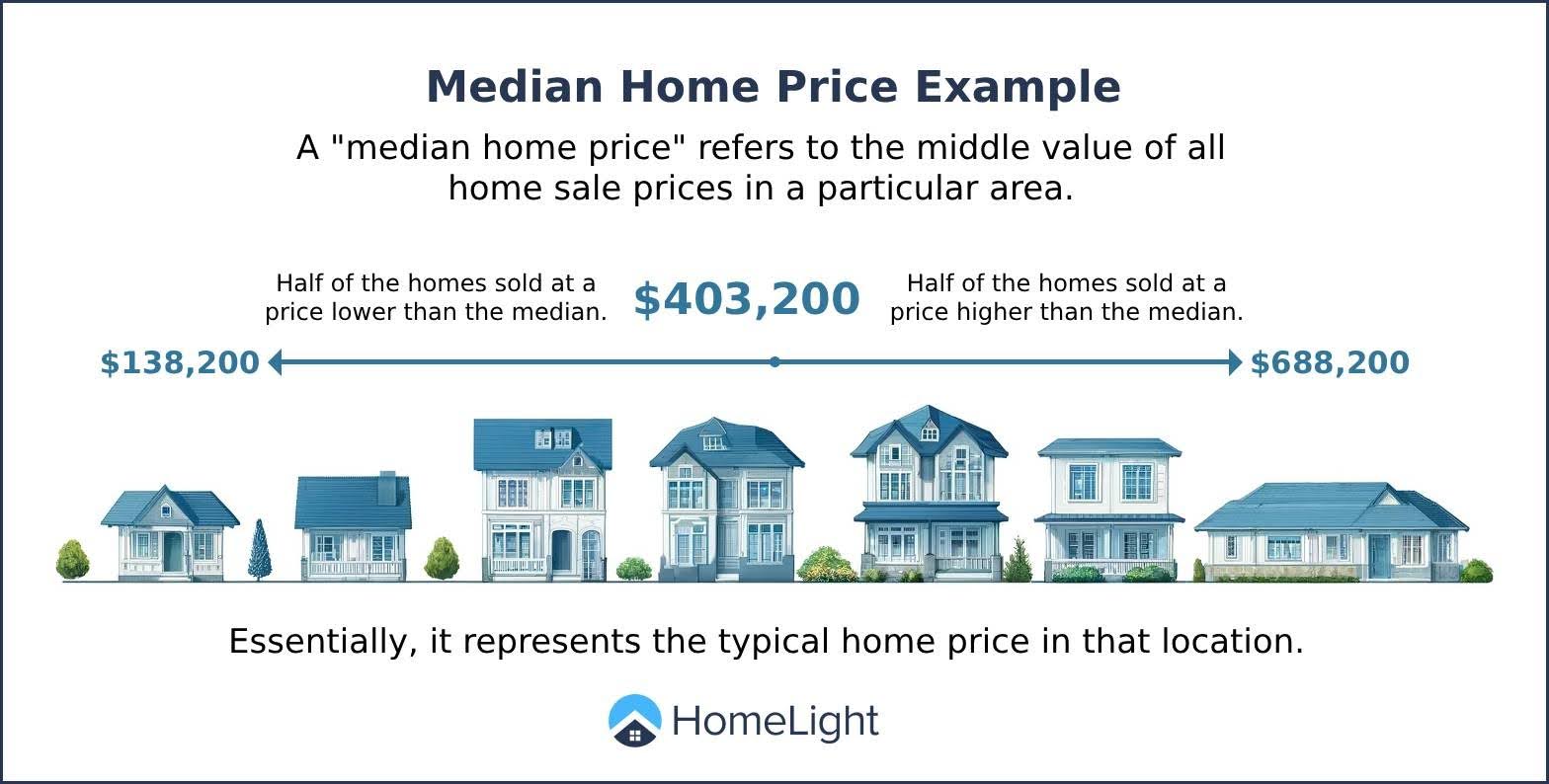

The median home price is the middle price of all homes sold in a specific area during a set time period. If you lined up every home from cheapest to most expensive, the median is the one right in the middle.

It’s different from the average home price, which adds up all the sale prices and divides by the number of homes sold. The median is usually a better snapshot because a few ultra-expensive or ultra-cheap sales don’t throw it off.

So, for example, if 101 homes sell in a city in a month, the median price is the 51st home in that lineup, not an average of all the sales.

What is the U.S. median home price?

The median home price in the U.S., based on the most recent data, is $403,200. This number gives a snapshot of home values nationwide, but it can vary widely by region, city, and even neighborhood.

If you’re considering selling or just curious about area trends, looking at your local median home price is far more relevant than the national figure. A home in a high-cost market like San Francisco will naturally have a much higher median than one in a more affordable area.

Below are the current median home sale prices in some key metro markets throughout the country:

- Los Angeles-Long Beach-Glendale: $858,500

- New York-Newark-Jersey City: $750,000

- Chicago-Naperville-Elgin: $384,100

- Dallas-Fort Worth-Arlington: $369,000

- Houston-The Woodlands-Sugar Land: $331,500

- Washington-Arlington-Alexandria: $623,400

- Miami-Fort Lauderdale-West Palm Beach: $637,100

- Philadelphia-Camden-Wilmington: $381,100

- Atlanta-Sandy Springs-Marietta: $370,200

- Phoenix-Mesa-Scottsdale: $479,600

- Boston-Cambridge-Newton: $747,900

- San Francisco-Oakland-Hayward: $1,350,000

Source: National Association of Realtors (existing single-family homes)

What’s the median home price where you live? A quick online search will usually point you in the right direction. Local Realtor associations tend to be the most accurate source for up-to-date numbers. You can also use resources like World Population Review, which breaks down median home prices by state on an interactive map.

How is the median home price used?

What does the median home price actually tell you? It’s one of the easiest ways to get a feel for what homes are really selling for in a market. It also helps show whether prices are trending up or down over time. Here’s how the median home price is used:

- Prospective homebuyers can use it to get a quick sense of what homes usually cost in an area, which helps with figuring out what they can afford, especially if they’re moving to a new state.

- Home sellers refer to it as a helpful starting point for pricing, even though they’ll usually lean more on recent comparable sales.

- Lenders look at median home prices to understand market trends and how they might affect lending decisions.

- Government agencies and policymakers use it to track affordability, plan development, and shape housing policies.

While real estate agents may consider the median home price when listing a home, their go-to valuation tool is a comparative market analysis (CMA). This is a detailed report they create from recent sales of nearby comparable homes, known as “comps.”

The median price can give you helpful context, but a CMA gives you a much more accurate read on what your home is really worth. Many real estate agents provide a free CMA when you book a consultation.

How has the median home price changed over time?

Like most other price tags, the median home price in the United States has been on an upward trend over the decades. In the early 1960s, the median sales price of houses was approximately $18,000. Fast-forward to the fourth quarter of 2025, and this figure has risen to $412,300. There have been a few rollercoaster years in between, caused by economic, social, or political factors.

Here are some big shifts we’ve seen in median home prices over time:

- 1970s inflation: High inflation pushed home prices up as building costs surged.

- Early 1980s recession: The economy slowed down, and high interest rates cooled the housing market, stabilizing or even pulling prices down.

- Early 2000s housing boom: Cheap credit, low interest rates, and speculative investments drove home prices up fast.

- 2008 financial crisis: The housing bubble burst, and home values dropped sharply across the country.

- 2020s pandemic impact: Low interest rates, remote work, and supply chain issues all combined to send home prices higher.

What makes the median home price go up or down?

Several factors influence fluctuations in the median home price:

- Supply and demand: When there aren’t enough homes and lots of people are buying, prices usually rise. When there are more homes than buyers, prices tend to fall.

- Economic conditions: A strong economy marked by low unemployment and rising incomes boosts buying power and pushes prices up. A weaker economy usually does the opposite.

- Interest rates: Lower mortgage rates make buying more affordable and bring more buyers into the market. Higher rates do the opposite and tend to slow price growth.

- Inflation: As costs for materials and labor rise, building homes gets more expensive, which can lift home prices.

- Location: High-demand areas with strong schools, amenities, and safety tend to hold higher median prices.

- Government policies: Zoning laws, taxes, and housing programs can all shape how many homes get built and how affordable they are.

Find a Top Agent With a High Sale-to-List Ratio

HomeLight can connect you with the highest-rated agents in your market. Our data shows that the top 5% of real estate agents across the U.S. sell homes for as much as 10% more than average agents.

Median sale price vs. average sale price

As noted above, the median sale price and average sale price are two different ways to measure home values. They are often confused, but they’re re not interchangeable. Here is the difference:

- Median sale price: When all homes sold in a given period or area are arranged from lowest to highest, this is the middle price. The way it’s calculated eliminates the influence of extreme high or low numbers that can distort the overall picture.

- Average sale price: This is the sum of all home sale prices divided by the number of sales. While useful in some cases, the average price can be skewed by a few very high-priced or very low-priced homes.

For example, if 10 homes sell in a neighborhood, with prices ranging from $200,000 to $1 million, the average might be artificially high due to a few luxury sales. However, the median would provide a clearer picture of what most buyers are actually paying. That’s why in most cases, the median sale price is a more reliable market indicator.

Get a free home value estimate

While the median home price gives you a general sense of what homes are selling for in your area, it doesn’t tell you exactly what your home is worth. For a more tailored estimate, you can use HomeLight’s Home Value Estimator.

This free tool analyzes recent sales of comparable homes, market conditions, and other factors to provide a near-instant online home value estimate. It’s a great starting point for sellers who are curious about their home’s potential price before listing it.

How can you estimate your home sale proceeds?

If you’re looking into your home’s value or checking out the median home price because you’re thinking about selling, it’s just as important to understand your potential proceeds. That’s the amount you actually take home after closing costs, agent commissions, and other selling expenses are deducted. You’ll also need to factor in whatever you still owe on your mortgage to get the full picture.

To get a rough estimate, try HomeLight’s Net Proceeds Calculator. This free tool breaks down the numbers and gives you a ballpark picture of your sale’s profit potential.

Hire a top agent for the highest proceeds

If you’re looking to sell your home and want the highest possible proceeds, work with a performance-proven real estate agent in your market. A seasoned local agent can help you accurately price your home, market it to the strongest buyers, and negotiate the best possible sale price.

Ready to get started? Use HomeLight’s free Agent Match platform to connect with a top-rated agent in your area who can help you navigate every step of the selling process, from preparations to close.

Frequently asked questions (FAQs) about median home price

The median home price is found by arranging all home sale prices in order from lowest to highest. The middle value in that list is the median. If there are an even number of sales, the median is the average of the two middle prices.

States like California, where the median home price is about $854,000, and Hawaii, at about $773,400, typically have some of the highest prices due to strong demand and limited housing supply. On the lower end, states like Iowa, at about $250,700, and West Virginia, at about $253,300, tend to be much more affordable. Overall, these differences highlight how much home prices can vary depending on location, demand, and local economic conditions.

For buyers, it helps set realistic expectations about what homes cost in a specific area. For sellers, it gives a quick benchmark for pricing their home competitively. It also helps both sides understand whether the market is trending up, down, or staying steady.

Header Source: (Pixabay / Pexels)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.